Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class' return. The information below regarding returns therefore differs from the returns in other share classes.

Before making any final investment decisions, please read the prospectus, its Annual Report, and the KID of the relevant Sub-Fund here

This material is marketing communication

Monthly Newsletter Coeli European – August 2023

AUGUST PERFORMANCE

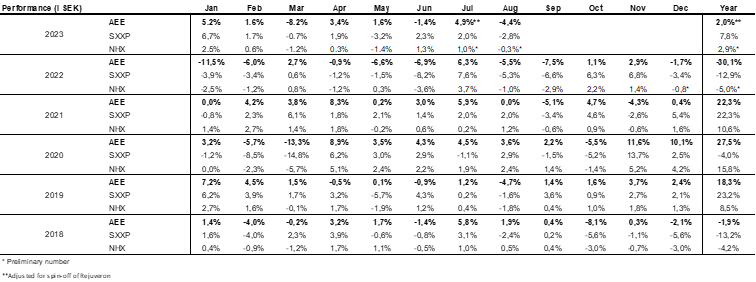

The fund's value decreased by 4.4% in August (share class I SEK). The Stoxx600 (broad European index) decreased during the same period by 2.8% and HedgeNordic's NHX Equities decreased provisionally by 0.3%. For 2023, the fund has decreased by 5.8%. Adjusted for the spin-off of Rejuveron, the fund's value has increased by 2%. The Stoxx600 and NHX Equities have risen by 7.8% and 2.9% respectively during the year.

EQUITY MARKETS / MACRO ENVIRONMENT

At the start of August, the rating agency, Fitch, downgraded the US credit rating causing turbulence in the financial markets. After three days, the broad European index had fallen by three percent, and it looked similar in most geographic markets. In contrast to July, there was no quick recovery, but the downward pressure continued with, in many cases, high volatility, something we also had a taste of and which we will return to.

By the end of the month, the broad European index had fallen 2.8%, compared with the S&P 500, which was down 1.6% (measured in local currencies). Small and mid-caps were under significant pressure and had fallen at most by a whopping 7.5%. The month's return for Carnegie's small company index ended at -4.4%.

After a flawless and strong reporting period for the fund in July, we now experienced what small deviations in relation to expectations can cost in the short term. Of our six reporting companies in August (Rugvista, Surgical Science, ISS Storskogen, Carel and Pets at Home), only Rugvista gave a positive return of 12% on the month (+35% year-to-date). Surgical Science, ISS and Storskogen were under significant pressure, and we elaborate on that in the portfolio company section of this letter. The fund's return ended despite significant negative returns from the above-mentioned companies at -4.4%, including the weakening of the Swedish krona in August (-3%!) which had a negative impact of approximately -1%.

The central banks’ continued hawkish communication contributed to driving up interest rates during the month. The image below shows the Swedish 10-year government debt interest rate, which rose from around 2.5% to a maximum of 2.85% during the month. A strong movement which in turn put pressure on share prices. The corresponding German interest rate level started the month at the same level as the Swedish one but ended the month at around 2.45%. Sweden is facing headwinds from many directions, and we will come back to that.

Source: Bloomberg

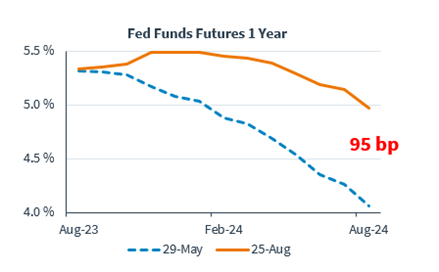

The diagram below shows the fixed income market expectations of how high the Fed will raise interest rates and when the interest rate cuts will begin. The blue curve shows how the expectations looked at the end of May and the orange shows how it looks today. A difference of almost one percentage point, which is huge in this context. Underlying this means that corporate profits and private consumption have been stronger than expected, but unfortunately it looks like it will be at the cost of higher interest rates and for a longer period. It does not favor risk appetite in the stock market, but on the other hand is largely discounted already. The development is completely in line with what the American central bank wants and desires.

Source: Kepler Cheuvreux

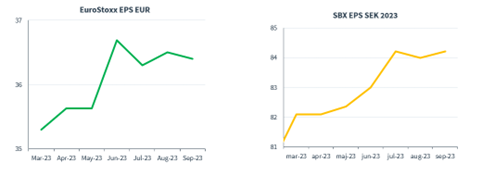

The stronger profit development has resulted in the following development in profit per share for the USA, Europe and Sweden. All geographies have higher expected profit levels compared to last spring.

Source: Kepler Cheuvreux

The annual central bank conference in Jackson Hole on August 24-26th had kept the financial world on edge for several weeks. It was surprisingly undramatic, and Fed chief Jerome Powell's message is that they are now more data-driven, in other words, they wait and monitor effects, unlike in the past where they raised the interest rate without blinking an eye. It feels highly reasonable after raising interest rates 525 basis points since March 2022.

Public confidence in central banks probably did not increase dramatically after Powell described the situation as: "We are navigating by the stars under cloudy skies". It was topped by ECB chief, Lagarde, who quoted a philosopher: "Life can only be understood backwards, but it must be lived forever". It has similarities to the oracle in Delphi 700 BC, who gave answers that no one understood. One difference was that she inhaled toxic volcanic fumes and thus achieved a slightly delirious state, the oracle that is.

It reinforces our view that the ratio of central banks' power to competence is skewed, harms and continues to disadvantage the wider economy. The effects of interest rate increases tend to take 9-12 months before you can see the effects in the real economy. If the same is true this time, then we have seen half of the effects of implemented interest rate increases. The ECB should also wait, but they will most likely raise the interest rate at least once more in September.

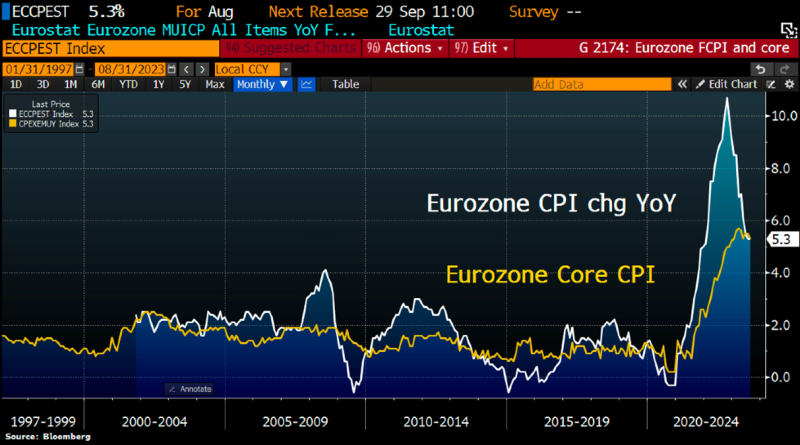

Below is the development of Eurozone inflation. Core inflation is falling slowly, and we hope and believe the pace will accelerate during the autumn.

Source: Bloomberg, Holger Zschaepitz

A rebound was on the cards at the end of the month and weak US labor market data fueled it further (reducing the risk of more interest rate cuts) and we experienced, in many places, the best stock market day since the beginning of June. Right now, bad news is good news for the stock market, but ideally not too bad.

Source: Bloomberg, Holger Zschaepitz

After a strong period of US macro data, the past month has started to show some signs of weakness. Below is the Citigroup Financial Surprise Index.

Source: Bloomberg

Germany, Europe's economic engine, is struggling with a China that is slipping precariously and with continued high inflation.

Source: The Economist

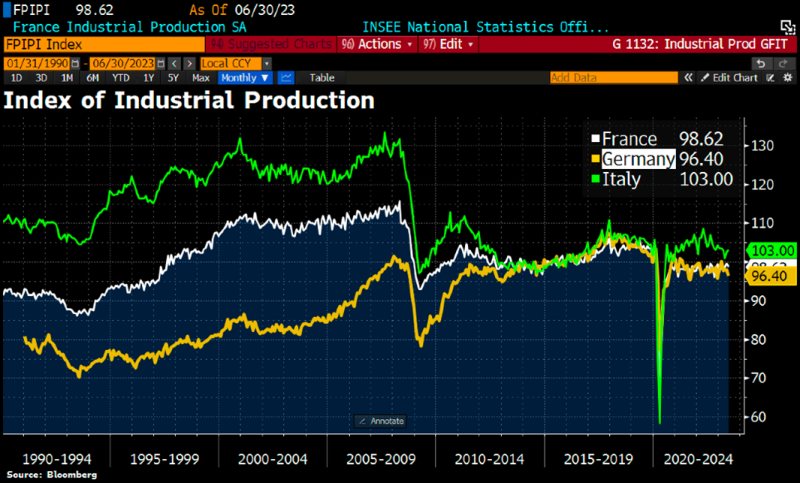

The picture below shows French, German and Italian industrial production which at best is at the same level as in 2007! Germany's flagship industries of car manufacturing and mechanical workshops are stagnating. We had Renault (founded in 1898) visiting the office a few days ago and the mood became somewhat strained when we noted that Renault's market value is a little over one percent of Tesla's. The flipside of the coin is that it is easy to find undervalued companies in Europe. In Renault's case, you get paid to own their profitable core business when you take out the financial business and their 43% stake in Nissan.

Source: Bloomberg

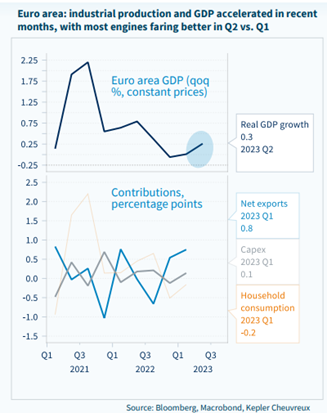

Despite these problems, European economic growth has turned slightly upwards in recent months driven by increased exports, increased investment and increased private consumption. Good!

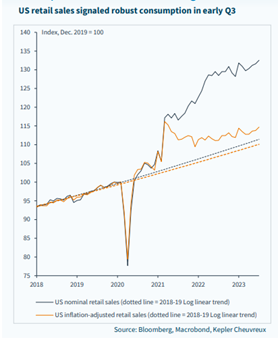

American consumption is above the long-term trend line. A huge difference compared to here in Sweden.

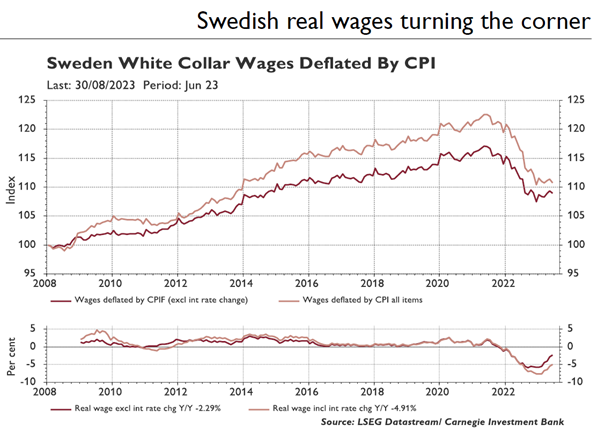

However, there are several indications that the worst is behind us in Sweden and that real wages and consumption will soon start to rise. Here we go towards brighter times!

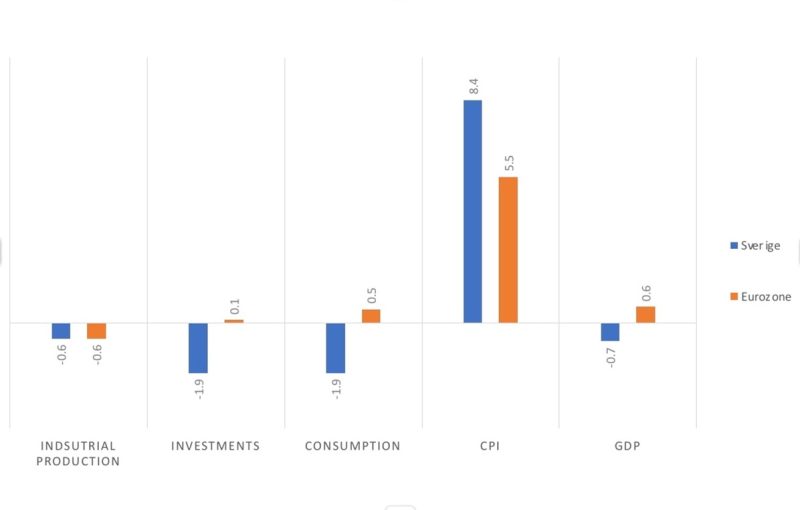

The image below shows Sweden's development this year compared to the Eurozone. Sweden has the same weak development in terms of industrial production, significantly lower investments, significantly weaker consumption, significantly higher inflation, and significantly weaker GDP development. Anyone still wondering why the Swedish krona is so weak when foreigners see the same picture, get tired and sell their Swedish assets? We ignore that we have now reached 100 bombings this year, as well as putting most of our political energy into curbing Koran burnings and flirting with Turkey and Hungary to join NATO. However, a certain conclusion of the image below is that Sweden fared significantly better than the eurozone during the Covid crisis. Sweden is also superior to the eurozone in terms of the state of government finances, but this is less important in a flow-driven currency trade.

In last month's newsletter, we told you about Trelleborg, which was asked by the Riksbank (Swedish Central Bank) to stagger its exchange activity over two weeks after a large corporate transaction, in order not to move the prices too much. As of the last July, foreigners had sold Swedish shares for approximately 400 billion, which is just under 3 billion per day. If this is true, which we have reason to believe, one might ask why we have a currency that cannot handle normal flows? To quote Annika Winsth, chief economist at Nordea: "The weak krona is not just a problem for the Riksbank, import companies and travelers abroad, but is also starting to become a societal risk."

Source: Coeli European, Consensus Economics

There is always someone who is worse off! The Russian ruble has lost about 50% of its value in one year, which is very gratifying. The screws are being tightened and the pressure on Putin increases every week. He also needs to get himself a new chef. As expected, Wagner boss Prigozhin had a tragic accident that is likely to spark a new high level of turbulence and internal conflicts within Russian domestic politics. Given Russia's dependence on the Wagner group in Ukraine and Africa, there may well be further setbacks for Putin and his yes-sayers. Setbacks they didn't foresee before the anticipated accident.

Albanian President Edi Rama jokes about the accident:

https://twitter.com/RasimReiz/status/1697564273071792428

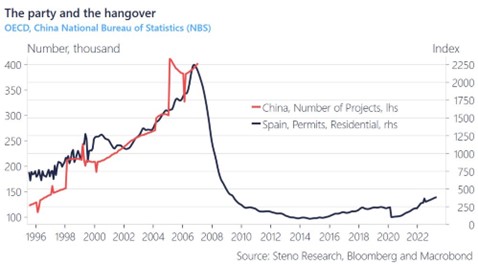

Steno Research has produced the image below, which is a convergence between the Spanish real estate bubble that burst in 2008 and the current Chinese real estate market, which is struggling to say the least. We'll see if there are similarities going forward, but China is facing its biggest economic challenges ever.

As long as we don't end up here again. During August, the Vietnamese EV producer Vinfast (electric cars) was listed on the Nasdaq stock exchange via a SPAC. In 2022, it produced 7400 cars, and the market capitalization reached 190 billion dollars, making the founder, Pham Nhat Vouon, the second richest person in the world. He owns 99.69% of the company, so not the most liquid stock.

Source: Bloomberg

The oxygen must have run out in the meeting room when the Nobel Committee, after a "long principled discussion", invited the ambassadors of Russia, Belarus and Iran to this year's Nobel dinner. Sweden's leading brand is being dragged in the dirt by a bunch of extremely tone-deaf individuals with unimaginably bad judgment. Half an hour after the King said on Saturday morning that he was doubtful whether the royal couple would come, the Nobel Committee changed its mind. Well done, King!

Source: Steget Efter

Source: Business Ukraine mag, X

Portfolio Companies

Surgical Science

After two consecutive successful reports, Surgical Sciences' Q2 report came in August. Sales were about five percent worse than expected, while operating profit was slightly better than expected. Even though sales were lower than the market expected, the mix was good: The highly profitable license revenues grew by a whopping 67% in the quarter. The fact that license revenues make up an increasingly large share of total sales is the most important thing for our investment thesis.

The cash flow was extremely strong and the company's net cash ended up at SEK 574 million, which corresponds to around 7% of the current market value.

Despite an apparently well received report, the share price fell a full 21% on the day of the report. Overall, we think it can be attributed to the CEO’s word. As part of a market analysis in the CEO's speech, it was mentioned that increased competition is expected in the future, and thus lower market shares as a result. This is nothing new to us – it would be strange if a business with Surgical Science's profitability and growth prospects was never exposed to competition. At the same time, we believe that the barriers to entry are high: the company's technology edge ought to be significant after many years of a one-sided focus on surgical simulation. In addition, the total market is not very large, which should reduce the appetite for larger players to start competing.

When we were in contact with the company, it was confirmed that there is no new player on the market that has changed the competitive landscape. Even when the company set its financial goals, i.e., to reach sales of 1.5 billion Swedish kronor with a margin of 40% in 2026, it took into account that it could possibly lose market share (from their dominant position today). The company also believes that the technological advance has never been greater.

Our conclusion is that if the price fell mostly on the company's competitive comments, it is due to unfortunate wording on the company's part (and possibly a misinterpretation on the part of the stock market).

By and large, our own estimates are unchanged after the report release. For the company to reach its sales target, we expect that from 2023 it will need to achieve around 17% annual growth per year at group level and we think it looks increasingly likely that the company will succeed in this. We feel more secure in the financial ambition today than 6 months ago. At the same time, the share price is unchanged since the beginning of the year, and we have therefore taken advantage of the situation and bought more shares at attractive levels.

ISS

The ISS mid-year report contained a lot for the market to digest, with both positives and negatives. The company's outlook for organic growth was raised, while guidance for profitability and free cash flow were unchanged. At the same time, the company chose to take a larger write-down in France, which has been an underperforming segment where management has not succeeded in turning the business around as hoped. The idea is now to sell the French business, which we believe is good in the long term. The stock fell 11% in August and is now valued lower than in many years with single-digit earnings multiples. This even though the company has done most things right in recent years.

Storskogen

We see our opportunistic (smaller) position in Storskogen as our clear mistake this reporting period. The company's cash flow remained strong, and, despite bad economic times, profitability was relatively good. On the other hand, organic growth for sales and operating profit was worse than expected. The stock fell sharply on the day of the report, a whopping 27%. We thought this was excessive (the negative estimate revisions were around 5–10%) but note that companies with the slightest underperformance this reporting period were heavily penalized.

Bonesupport

Bonesupport was one of the positions that cost the most in negative returns for the fund in August. It is one of the Stockholm Stock Exchange's best stocks this year, so a combination of profit taking, no news and low turnover caused the stock to fall by 16% in August. Several Swedish med-tech stocks had a similar development during the month. We had reduced our position slightly at higher levels and we have taken the opportunity to increase our holding during the weakness. Bonesupport trades at EV/S 8x on our 2025 estimates.

SLP

SLP made a positive contribution to the portfolio during August, outperforming the property index which was unchanged on the month. SLP is the real estate stock with Swedish holdings that performed best this year, with an increase of around 19%. For the whole year, the real estate index (SX35GI) has fallen 3.5%, which so far is not as bad as the headlines in the newspapers say. Otherwise, no news in SLP.

Corem

During August, Corem was once again the portfolio's best share with an increase of around 13%. Since the turn of the mid year, the share has risen by 58%. The likely explanation for the rise is, apart from a very weak first half of the year, news about property sales in CEO, Rutger Arnhult's, holding company M2. At the end of the first half of the year, M2 sold four properties for a property value of just over SEK 1 billion. The market has been (and probably still is to some extent) concerned about M2's debt, so these sales were welcomed by the market, and reduce the risk in Corem.

The sale of parts of the associated company Klövern to Nrep on July 3rd was also a very important deal for Corem with a strong liquidity effect of as much as 1.4 billion. After the sale, Corem owns 17% of Klövern. In August, both Rutger Arnhult and M2 bought shares in Corem for a total of SEK 14.3 million, a very good signal.

Another factor that speaks for the real estate sector going forward is that the bond market is showing some signs of awakening. When Castellum issued a two-year bond on August 31st, the spread was 215 points over Stibor. Significantly lower than 6-9 months ago. Fabege also issued a 200 million bond that same week at a price of 200 basis points above Stibor. Compare with the banks' credit spread of around 160 points - clearly positive signals from a market that has been completely closed for a long time.

Source: Bloomberg

Rugvista

After three strong reports, Rugvista came out with another strong report in August. For the fourth quarter in a row, expectations were beaten, and the share was rewarded with an increase of around 6%. Sales came in 5% above expectations and margin strengthened to 9.1%, driven by a strong gross margin and lower marketing costs compared to last year. Worth noting is that conversion has increased despite less marketing. Our interpretation of that is that the new website that was rolled out during the year is working well. There is probably more potential in the new website as it takes a few months for Google's algorithms to calibrate.

The company also mentioned that July started strongly with continued sales growth and organic growth. At the time of writing, the stock has risen by 32% this year, while the operating profit has been revised up 35% for 2023e. If the macroeconomic conditions do not deteriorate significantly from here, we think that the Rugvista share will continue to be undervalued.

Pets At Home

During the month, British Pets at Home also reported. The numbers came in roughly as expected. At group level, revenues grew by 8%, of which 7% in retail operations and 16% in veterinary operations. The stock fell 4% in August, in line with the market.

Carel Industries

The Italian ventilation company, Carel Industries, also reported its Q2 report in August. The company reported organic growth of a whopping 16% and at the same time beat EBIT expectations by 10%. During the year, we have built a medium-sized position in Carel, which we have followed for a long time, and hope to return to the subject in the future. The stock was largely unchanged in August.

Short positions

The short portfolio contributed positively during the month, where our short positions on the Swedish small company index worked best.

Exposure

The net exposure at the beginning and end of the month was 85% and 88% respectively.

Summary

We ended last month's newsletter with a view that the short-term outlook is moderate. That was correct, but the decline was stronger than expected. The reasons we mentioned last month were typical outflows from equity funds in August, that CTAs had a high equity exposure, and that a lot of short sales had been covered in July. There were also, as usual in August, low trading volumes, which combined with typical large outflows pressured share prices more than expected. And the smaller the company, the more constrained the liquidity, which also left a clear mark on the share prices of those companies. A small data point is that on Friday, September 1, it was the second lowest trading volume of the year.

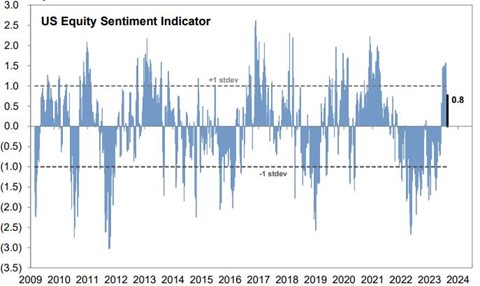

The image below shows the Goldman Sachs sentiment indicator. A clear cut in the curve, but still in positive territory. The last days of the month were significantly more positive with one of the year's best stock market days included.

Source: Goldman Sachs

Despite some turbulence in recent weeks, the development of the volatility index for shares and interest rates respectively was relatively undramatic. It can also be deduced that the volatility in Europe has during the year been higher compared to the USA (top image of the two). Overall, the VIX index is at historically low levels.

Source: Kepler Cheuvreux

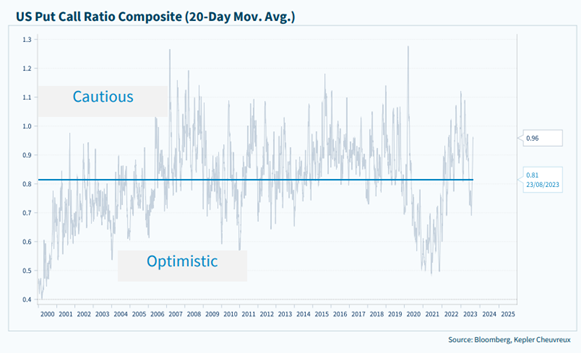

As usual, the demand for put options is at its lowest when the stock market delivers a positive return and vice versa. The relationship between issued call and put options plunged in July and picked up again in August and about a week ago showed a cautious positioning, which is positive for the future.

Illustrated another way, the dark blue line shows the performance of the S&P500 and the white line implied volatility for put options, which is a clear indication of demand for put options. At the beginning of the month when the stock market fell, demand increased sharply and in the last days of the month when the stock market rebounded the volatility of options fell sharply (and the prices) and we are now at the same level as in July again. Put options are like home insurance, you must have it in place before the house burns down or it can be expensive.

Source: Goldman Sachs, Bloomberg

Below shows the dividend yield on US stocks relative to the 30-year interest rate. Something in the equation is not right. Usually, the dividend yield on a bond is significantly higher than the 30-year interest rate, but now the reverse is true. If we are to return to a normal situation, either the dividend yield must rise (because of falling share prices) or the interest rate must begin to fall. Our view is that interest rates will start to fall.

Source: Bloomberg, Holger Holger Zschaepitz

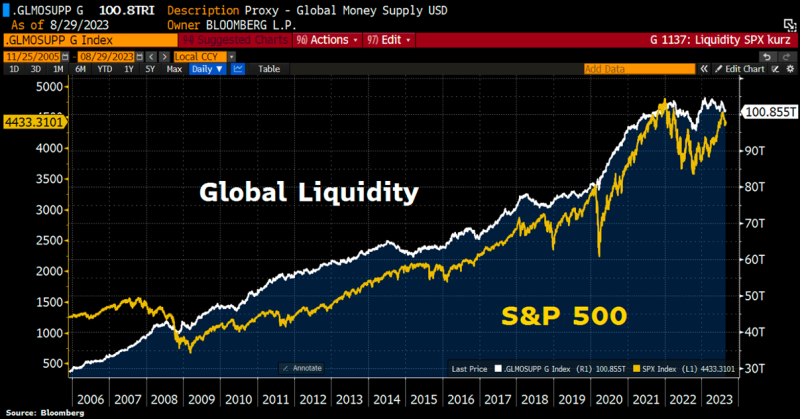

Cash is king! The correlation between liquidity in the global financial system and the performance of the S&P500 is very high.

Source: Bloomberg, Holger Holger Zschaepitz

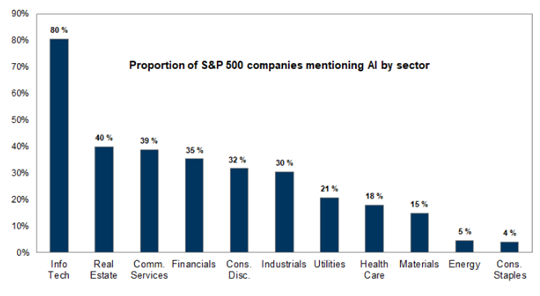

After the end of the reporting season, it can be stated that the AI hype has flourished on a broad front, at least when it comes to talking about it.

Source: Goldman Sachs

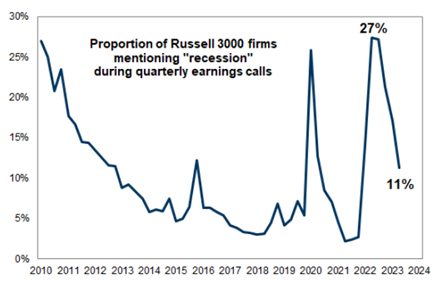

Companies in the Russell 3000 index seem to be more optimistic about the future. Only 11% of the companies mentioned the word recession in their quarterly statements. A completely normal level seen over many years.

Source: Goldman Sachs

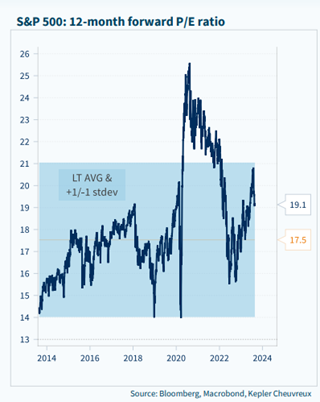

The decline in August has pushed back valuations on the US stock markets from historically high levels.

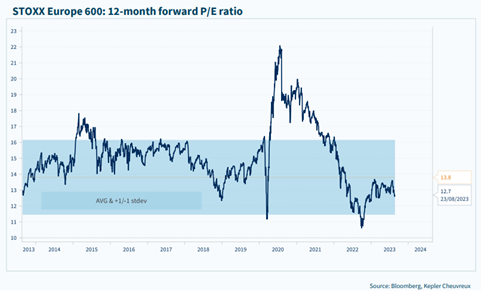

The corresponding picture for Europe shows that we are down to historically low levels.

The UK, with its self-harming behavior with Brexit, has clearly been re-evaluated since midsummer 2016 and is valued at a whopping 50% discount to the USA. We have 23% exposure to the UK as there are many well-run companies there that deliver good value to us as owners.

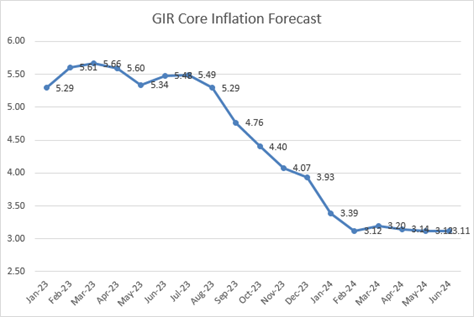

Goldman Sachs forecast for Eurozone inflation.

Source: Goldman Sachs

The stock market is looking forward to interest rate cuts.

Source: Themarketear.com

We stand by our market view that the stock markets will be higher at the end of the year than today. September usually shows a negative return and may well offer the same this year, although we think we jumped on that wagon back in August. For those of you who like statistics, the first half of September is historically the second worst period of the year, only beaten by the second half of February.

There are some positive factors now compared to a month ago. We are at lower levels in general and the sharp decline in the first weeks of August has, according to calculations by Goldman Sachs, meant that large important CTA's now must start buying shares again after selling large amounts in August. That, together with large repurchases, will have a positive impact, everything else being equal. Compared to a month ago when there had been record volumes in terms of covering short positions, the market is now in a position where short positions have increased quite a bit in August.

Inflationary pressure is likely to continue to fall during the autumn, which should have a positive impact on central banks' actions (even if their actions are best left unpredicted). Recently published US labor market statistics have come in at levels that make the Fed's job easier, at least here and now.

Finally, we are one month closer to a seasonally historically strong period. Among our own holdings, we see a good or very good upside, which is the most important thing for the fund's performance in the long run.

Source: Sentimenttrader.com, Jay Kaeppel

As previously communicated, we now focus only on long positions, which means significantly more analysis capacity given to what we are most passionate about; finding more or less undiscovered companies that have the ability to develop well on their own, driven by their ability to create value, an attractive price at the time and a strong management.

In connection with the fund changing its strategy, the existing share class hedge for SEK/Euro will be closed. This means that the fund's share classes will not be hedged in the future and thus fluctuate with exchange rate changes in SEK/Euro. In the past, a currency change has not affected the NAV rate; for example, when the krona weakened in 2023, it has had no positive effect on the NAV rate. This is a natural change in connection with the fund's investment strategy going from a long/short equity fund to an actively managed long only equity fund. Considering that the Swedish krona usually strengthens when it is risk on and vice versa, these movements will probably counteract each other and, other things being equal, will reduce the volatility of the fund on a daily basis, which in that case is positive.

We thank you for your interest and wish you a wonderful September!

Mikael & Team

Malmö on September 5th, 2023