Monthly Newsletter Coeli European – August 2024

This material is marketing communication.

Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class’ return. The information below regarding returns therefore differs from the returns in other share classes.

Before making any final investment decisions, please read the prospectus, its Annual Report, and the KID of the relevant Sub-Fund here.

August Performance

The fund’s value decreased by 1.9% in August (share class I SEK), while the benchmark decreased by 1.5%. Since the change of the fund’s strategy at the beginning of September last year, the fund’s value has increased by 24.3% compared to an increase of the benchmark by 10.0%.

Source: Coeli European

* Adjusted for spin-off of Rejuveron

** Includes September 1 (strategy change to long-only implemented September 4 2023)

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

Equity Markets / Macro Enviroment

The fund fell by 1.9% compared to the benchmark index which fell by 1.5%. The corresponding figures for the whole year are 16.4 and 11.6% respectively. The fund's best contributors were Scandic Hotels, the London Stock Exchange and SLP. LVMH also contributed meaningfully as we increased our position from depressed levels and the stock closed 12% higher at month-end. The worst contributors were Commerzbank, Syensqo and 4imprint.

The weakening of the Swedish krona last month reversed to a strengthening of two percent and thus affected the fund's return negatively. The strengthening of the krona is positive, and it should continue as the focus shifts to fundamental data and a continued increased risk appetite. We are looking forward to being able to cross over to Copenhagen without having to call the bank.

It was, to put it mildly, an unusual month where the opening offered historic declines that were then followed by almost equally historic climbs. At the end of the month, the market was broadly unchanged. Not one of the proudest periods in the history of the financial industry. One personally had to endure criticism at home when returning from work in the evenings, as it was questioned what oneself and everyone else in the financial industry were up to during the days.

On Monday, August 5, the Nikkei index plunged 12.4%, the biggest drop since the October crash of 1987. That led to large and broad declines of 7-10% worldwide before slowing down. We have yet to hear a reasonable explanation for how this could happen. We took it easy, traded carefully and continued with our company analysis.

Source: Bloomberg

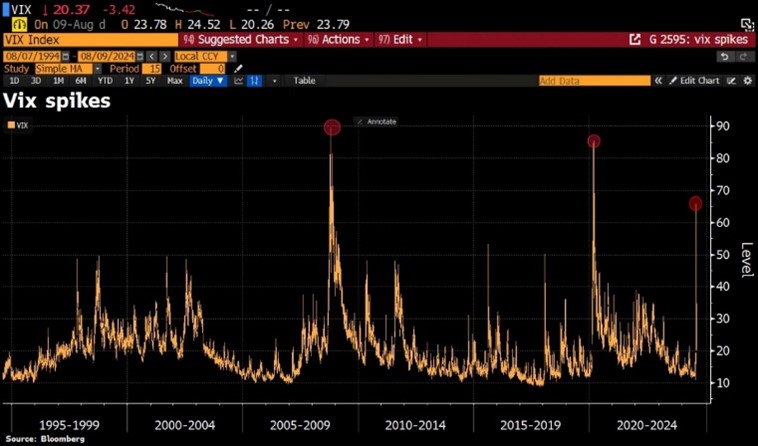

The volatility index, VIX, showed the highest level since the financial crisis of 2008 and the Covid crash of 2020. How is that possible? Because the Bank of Japan raises interest rates by 25 basis points? Our guess is that passive capital and various CTAs were strong contributors to these movements. You buy all the way to the top, turn around and then sell. In mid-August, according to statistics from Goldman Sachs, they came back in force and bought again. The question that arises, who invests in these funds?

Source: Bloomberg

After the crash on August 5th, the Nikkei index rose by 24% and thus the entire decline was recovered.

Source: Bloomberg

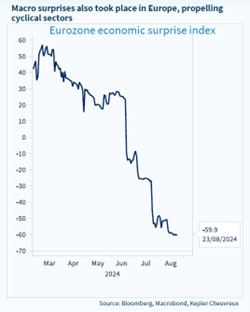

The European economies continue to show unchanged low activity with modest growth figures at best. Expectations of an acceleration have not been met in recent months. If one is to pick out something positive about it, it is that inflation is now down to around target levels and that interest rate cuts will, with a very high probability, continue in the autumn.

Source: Bloomberg, Macrobond, Kepler Cheuvreux

At the end of the month, Germany announced inflation data at low levels. The same was also reported for the Eurozone and the USA. Very good.

Source: Bloomberg

The US has also surprised negatively in recent months, from high levels, with a somewhat slowing economy. Note the correlation with a two-year interest rate that has plummeted since last spring.

Source: Bloomberg, Macrobond, Kepler Chevreux

The Fed was clear in its communication from Jackson Hole on August 23rd: “The time has come for policy to adjust. The direction of travel is clear”. In principle, it feels like a forgone conclusion that the Fed will announce its first interest rate cut in September. That message was appreciated by the stock market, and on that day the Nasdaq rose by 1.5% while the Russell2000 rose by a whopping 3.2%. As we have mentioned many times before, small-caps is the asset class within equities that are most sensitive to interest rate changes and we are expecting several interest rate cuts.

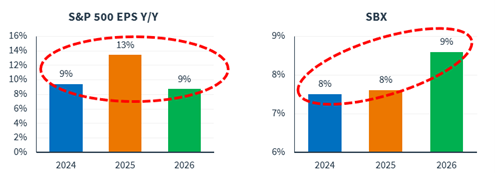

Interest rate cuts in combination with the below expected profit growth is a powerful cocktail to drive stock market development in the next two years. SBX is a broad Swedish index and the corresponding profit growth for Europe is 6, 8 and 9%, which gives 25% in three years.

Source: Kepler Chevreux

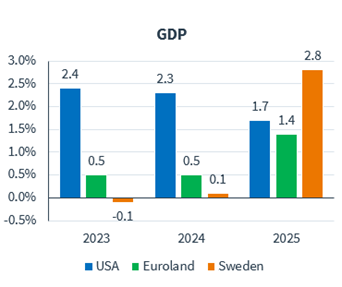

Next year's expected GDP growth looks good, and Sweden is likely to be among the winners.

Source: Kepler Chevreux

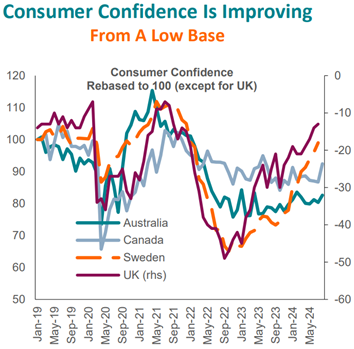

GDP growth is driven, among other things, by increased consumer activity. From deep lows, consumers are now waking up. The change will be most noticeable in Sweden, where there are large loans at variable rates. Satisfied consumers are an important component of a strong stock market.

Source: BNP Paribas

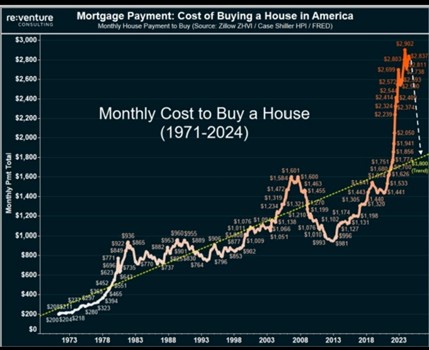

Even hard-pressed American homebuyers are expected to face a brighter future.

Source: Zillow ZHVI/Case Shiller HP / FRED, Win Smart

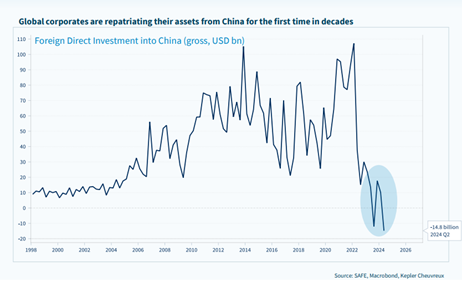

In China, however, most things are still pitch black. There are many reasons why foreign capital is fleeing the country. Europe is affected more than the USA and Germany is the country in Europe that is most affected.

Source: SAFE, Macrobond, Kepler Chevreux

Finally, the world's most important company, Nvidia, released its quarterly results at the end of the month. They once again showed absolutely unparalleled numbers which were followed closely by anyone with any interest in stocks. It feels a bit bubbly when people gather at sports bars and follow the reporting. https://x.com/SoundDobad/status/1828915502158360765

In a survey of roughly 3,000 employees at Nvidia, 37% stated that they now have more than $20 million in assets. Nvidia has created enormous value for many.

Source: X

Source: SHENEMAN

Portfolio Companies

Carel Industries

As previously mentioned, Carel has been one of the fund's weaker stocks this year. Possibly (and hopefully) this month's Q2 report marks a bottom. Even though the operating profit was around five percent worse than expected, the share rose on the day of the report. We guess that the report reaction reflects already low expectations. In addition, the company's management sounds more hopeful about the future as they begin to see signs that the market is improving in the important refrigeration segment.

The main problem this year has been that Carel was hit by the sharp reduction in the heat pump market. Although this market only makes up around 10–15% of sales, the impact has been significant as the area lost more than half (!) of its sales in the first half of 2024. Carel, which is a subcontractor to heat pump manufacturers, is not only affected by low demand from the end customer but also because the heat pump producers have large stock supplies. Over time, this should normalize and during the second half of the year, Carel will see simpler comparison quarters.

In the long term, our thesis is that Carel should be a company that can grow with high single-digit numbers, which combined with expanding margins and additional acquisitions gives double-digit growth in earnings per share. The stock rose by 5% in August and has fallen by 28% in 2024.

Accelleron

As we wrote in the previous monthly newsletter, Accelleron came up with a reverse profit warning in July. The principal figures for the first half of the year were thus known and we did not think there would be much drama in conjunction with the release of the report. Having said that, we note some incremental positives from the August 27th report release: The company's acquisition from last year of Italian fuel injector company, OMT, appears to be progressing very well. We also note that non-recurring costs related to the company's spin-off fell as guided. Finally, Accelleron's China exposure appears to be lower than we previously thought, which we think is positive.

Accelleron shares rose 2% in August and have thus risen 69% for 2024.

4imprint

The month's largest negative contributor was British 4imprint, even though the company's half-year report was 9% better than expectations in terms of operating profit. Management also mentioned that they believed it would meet analysts' estimates for the full year. At the same time, it was flagged that the American market for gift advertising had softened. Previously, it was believed that growth would be higher in the second half of the year, but the new stance is that it is expected to grow roughly as in the first half of the year.

With worse macroeconomic data, 4imprint's sales tend to be negatively affected, and during August we saw just that. Historically, 4imprint has taken market shares when the market has softened. The reason for that is that the company tend to maintain a high marketing intensity as well as all staff. This means that once the market returns to growth, 4imprint is stronger than its competitors, which in turn leads to market share gains. On our estimates and with a large net cash position, the stock is trading at EV/EBIT 11x and 10x for 2025e-2026e, which we think is attractive given the growth and yield.

The 4imprint share fell by 14% in August and has thus risen by 15% for 2024.

Scandic

Scandic was the fund's best performing stock during August with an increase of 5.5%. During the summer, basically all major convertible owners were redeemed early. At the same time, short selling has decreased from roughly 20% at the end of May, to today's 5%. In addition to this, the Norwegian real estate company, Eiendomsspar, has been flagged as the largest owner. We assume that Eiendomsspar has a good grasp of the market as they are also the Chairman and largest owner of Pandox. At the end of 2023, Scandic accounted for 36% of Pandox's hotel properties. Scandic trades at a low 7x and barely 6x EV/EBIT for 2025e and 2026e respectively.

Syensqo

We chose, in August, to sell our shares in Syensqo. The company is a spin-off from the Belgian chemical company Solvay. The stock trades at P/E ~10 at 2026e, which is a 30-35% discount to similar companies. Part of the case has been that the company should continue its refinement towards specialty chemicals, which should close the valuation gap. It also makes significant investments for future growth. In connection with their quarterly report, which showed a slightly lower profit than expected, some of these plans were put on hold due to a worse market outlook. Despite an attractive valuation, we judged the headwind to be too great for the stock to be a future winner. The share fell by 9% in August, but we continue to monitor the development.

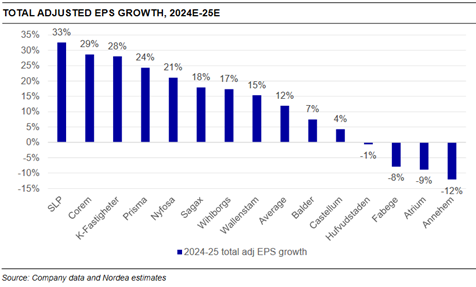

SLP/Corem/Balder

Our property shares SLP, Corem and Balder were together the best contributors of the fund during August. We attach a picture from Nordea, where SLP and Corem are at the top in terms of next year's average profit growth. If the Riksbank's (Swedish Central Bank) interest rate path takes effect, our guess is that the figures below will be even better. We still retain a high proportion, around 10%, of real estate in the portfolio.

Summary

American small-caps, despite good conditions, recently ended their worst half-year ever compared to the S&P500. It is highly remarkable and is likely due to a unique time for large technology companies combined with the fact that the proportion of passive capital has increased significantly in recent years. Reasonably, risk/reward should be excellent from here.

Source: Bloomberg

The development of European companies in recent years is reminiscent of the American ones. Since the downturn began in early 2022, European small-caps (white line) have fallen 11% compared to the broad European index (red line) which rose 8%.

Source: Bloomberg

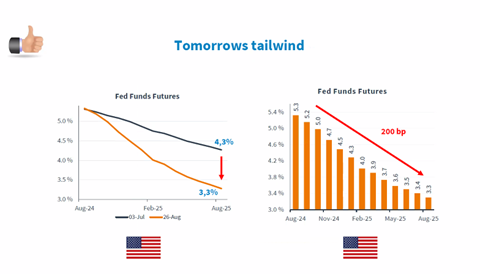

In just one month, expectations of where the Fed's key interest rate will be in a year have dropped from 4.3% to 3.3%. This means that the interest rate over the next 12 months is expected to drop by as much as 200 basis points. That's a huge change and is high-octane fuel for many asset classes, including equities, where small-caps have historically benefited the most.

Source: Kepler Chevreux

In addition, European small companies are expected to report profit growth of 17, 13 and 18% for 2024-2026e respectively. That gives a valuation of around 11x and 10x for 2025e and 2026e. That's 56% profit growth in three years and more than double compared to the broad market. What more could you ask for? The future looks unusually bright.

Source: Bloomberg

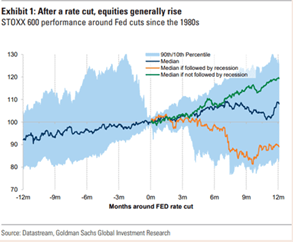

Below the performance of the broad European index after the Fed cut interest rates (data since 1980). The green line shows that the median development 12 months later yields 20% assuming the economy does not enter a recession. If there is a recession at the same time, the corresponding development is -12%. Our long-term view is that there will not be a recession.

Source: Datastream, Goldman Sachs Investment Research

For smaller companies, the development is even better. See the image below. Also note the valuation in the lower image. After all, you must play the ball where it lies and now it feels a bit like it lies, for small companies, on the penalty mark. Now the ball just needs to go into the goal as well.

Source: Jefferies

Current valuation of Europe compared to the USA. Even adjusted for the Magnificent 7, the premium is currently 42% which is record levels.

Source: Kepler Chevreux

Below illustrates how European SMIDs (small and medium-sized companies) have developed relative to large companies since 1995. After a strong July, SMIDs were again relatively weaker in August.

Source: Kepler Chevreux

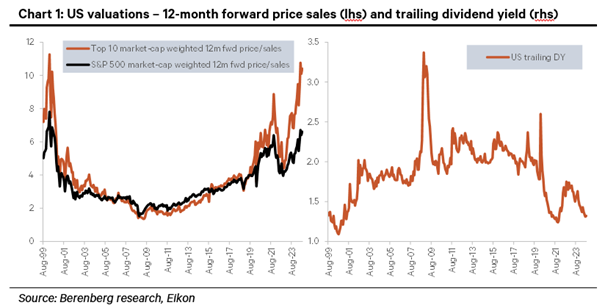

Below is the valuation of the US stock market measured as P/S and dividend yield. It is now back at previous high levels from 1999. However, the quality of the companies in the index is much, much better today than then.

All in all, our view is that we have the best financial conditions in many years. The big worry is still the geopolitical situation. But if we allow ourselves to exclude that and just focus on the economic fundamentals here and now, our best estimate is that we have two more good years ahead of us. There will also be large discrepancies between companies and sectors. A good environment for stock pickers, like us.

We are now rolling into September, which almost always offers volatility. Maybe we got it already in August? We feel that we have a balanced portfolio that works both in ups and downs scenarios. Our excess returns have come from individual stock picks and our concentrated portfolio. We believe that will continue to be the case.

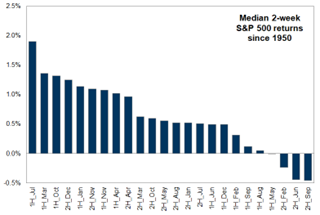

Below shows two weeks of returns of the US stock market since 1950. We also have a turbulent US election ahead of us, but then the winter season approaches, which is usually a strong period and which, this time, is likely to be accompanied by interest rate cuts from most of the world's central banks.

Source: Goldman Sachs

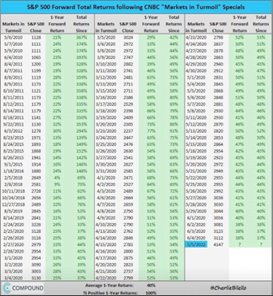

We end with an entertaining image that shows the one year forward return following the CNBCs “Markets in Turmoil” reporting where dramatic music always makes it sound like doomsday has arrived.

Source: CharlieBiello

Thank you for your interest and continue to enjoy the wonderful summer!

Mikael & Team

Malmö, September 4th 2024

IMPORTANT INFORMATION. This is a marketing communication. Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested. Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.