Monthly Newsletter Coeli European – December 2024

This material is marketing communication.

Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class’ return. The information below regarding returns therefore differs from the returns in other share classes.

Before making any final investment decisions, please read the prospectus, its Annual Report, and the KID of the relevant Sub-Fund here.

December Performance

The fund’s value decreased by 0.6% in December (share class I SEK), while the benchmark decreased by 0.8%. Since the change of the fund’s strategy at the beginning of September last year, the fund’s value has increased by 21.4% compared to an increase of the benchmark by 9.5%.

Source: Coeli European

* Adjusted for spin-off of Rejuveron

** Includes September 1 (strategy change to long-only implemented September 4 2023)

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

Equity Markets / Macro Enviroment

So, another year has passed with what the writer feels like the speed of light. As usual, there has been a deluge of extraordinary events, and the definition of a normal year is becoming increasingly difficult to formulate. Among many other things, we experienced an assassination attempt on President-elect Donald Trump, soldiers from North Korea fighting in Europe against Europe, pagers exploding in Syria and Lebanon with several thousand injured and an unknown number of fatalities, an American election with Trump as a clear winner and then Christmas Day when Finnish police officers boarded the Russian ship, Eagle S, on suspicion of cable sabotage. Just to name a few events that stand out.

But we start in December, where many of us waited for the Santa Claus rally. This did not happen, and several leading indices developed as follows, all measured in percentage and local currency: Stoxx600: -0.5, MSCI European small cap: -0.4, DAX: +1.4, S&P500: -2.5, DJI: -5.3, Nasdaq: +0.5 and Russell 2000: -8.4 (after rising by 10.8 in November).

Source: HEDGEYE

The fund fell in December by 0.6%, which was 0.2% better than our benchmark. For the full year 2024, the fund rose by 13.7%, which was 2.5% better than our benchmark. Since the strategy change in September 2023, the fund has risen by 21.4% compared to our benchmark, which has risen by 9.5%.

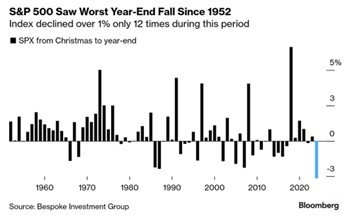

It was a pale finish to a good stock market year with the S&P500, measured from Christmas Eve onwards, having its worst end to a year since 1952!

Source: Bespoke Investment Group

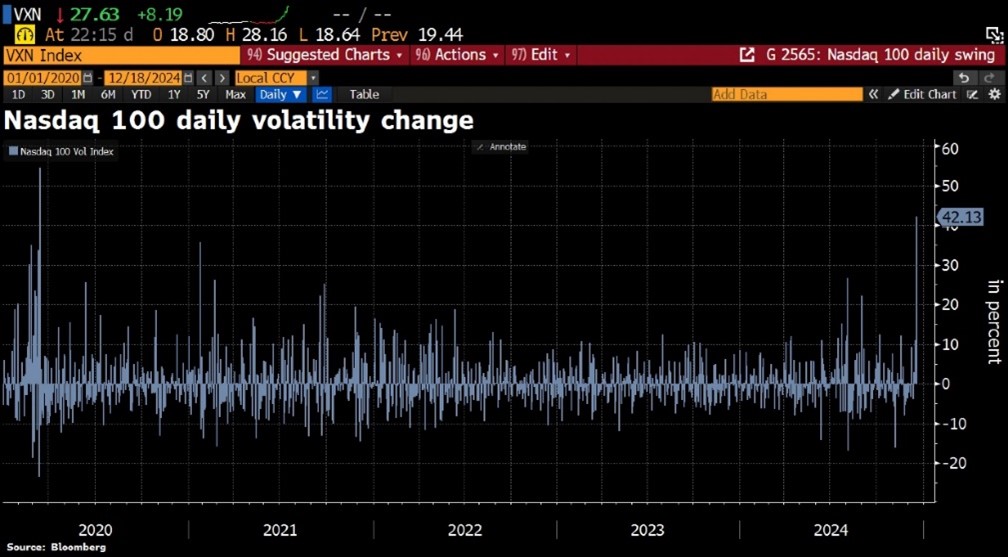

The weak end to the year may have to do with the fact that the Fed communicated in its last meeting on December 18th that the number of interest rate cuts next year will likely be only two as opposed to the expected three. That sparked some panic that day among fully loaded investors who all but wiped out all the gains built up after the early November election. The Nasdaq fell that day by 3.6%, the dollar strengthened considerably, and the American 10 Year Note went above the 4.50 level. The following day, there was also pressure on Asian and European shares. Below shows the VIX index which exploded higher after the Fed meeting.

Source: Bloomberg

Sweden's Riksbank (Central Bank) also lowered the key interest rate in December, and since May it has lowered the interest rate by 150 basis points to the current 2.50%. Switzerland also cut interest rates by halving the rate from 1.0 to just 0.50%. The market's view is that their policy rate in six months is down to 0.0%, which is interesting on many levels.

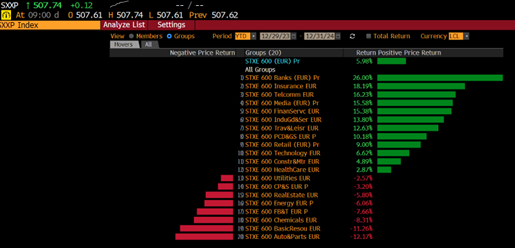

For the fourth year in a row, the banking index beat the broad market and was the best sector in 2024 with +26%. It is gratifying in many ways, not least as it is the banking sector that has been the root of much evil in Europe after the financial crisis almost 20 (!) years ago. The worst was the automobile index, which comes as no surprise to readers of this letter. What is more surprising to us is that real estate was significantly behind, producing a negative return of 5.8%, despite many tailwinds for the sector. It should now be well placed for a strong performance in 2025.

Source: Bloomberg

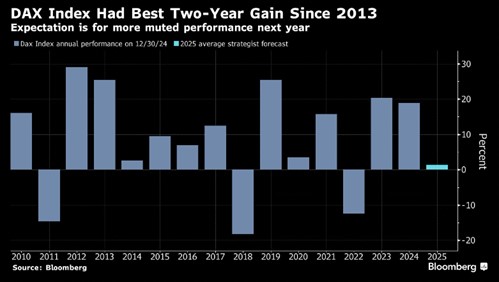

The best of the major European indices was, perhaps somewhat paradoxically, the German DAX which rose by 18.8% after rising by 20.3% the year before and thus had its best two-year period since 2013 (+43% compared to, for example, the OMX30 at 22%). Despite significant political and economic problems, the German stock market has therefore delivered a very strong return in the last two years.

Source: Bloomberg

The explanation for the somewhat contradictory performance is that the stock market does not reflect the economy, neither in Germany nor elsewhere, and it is also a standard answer we give to why one should invest in European shares. In addition, and more importantly for us, there are always opportunities that have not been captured by the large investor collective among the smaller companies.

In the last 20 years, Germany's GDP has risen by 87% compared to the DAX, which has risen by 414%.

Source: Bloomberg, Holger Zschaepitz

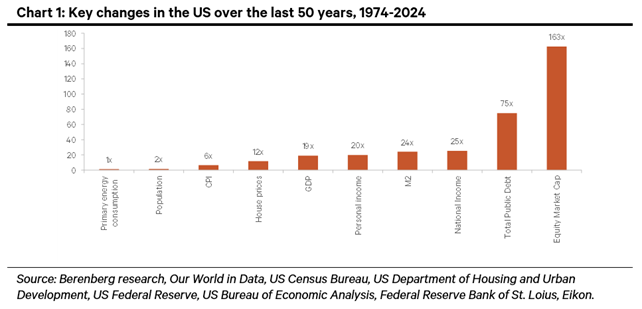

If we leave Germany for a moment, the picture below for the USA is interesting. The total market capitalization in the USA has increased by 163x in 50 years. Index has only developed a modest 85x with additional dividends of course.

Back to Germany where the difference between the economic reality and the stock market can be illustrated with the image below. Small and medium-sized companies, the SDAX and MDAX, fell last year by 1.8% and 5.7% respectively, while the large companies rose 18.8%. The smaller companies have a significantly higher proportion of domestic operations, which better reflects Germany's stagnant economy.

Source: Bloomberg, Holger Zschaepitz

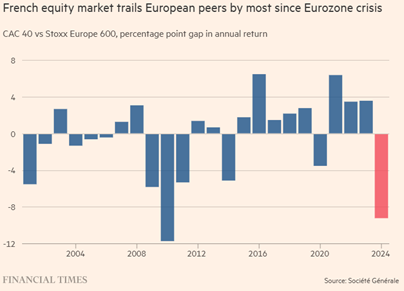

Another leading European index, the French CAC, had a weak year, in contrast to the DAX, with a -2.1% return. Not since the euro crisis has the CAC performed so much worse relative to the Stoxx600. 20% of the CAC index are consumer-related companies with luxury companies such as our own LVMH contributing negatively to this year's development. Luxury companies' weak development last year is largely due to China's weak development.

But the political crisis that began in June has also contributed markedly. With its fourth government in a year (!), the current administration has a challenging starting position to say the least. President Macron suffered another setback in December when Moody's downgraded France's credit rating from Aa2 to Aa3.

Source: Financial Times, Société Générale

The political crisis has meant that the French state, which has had a negative budget deficit every year since 2001 (!), now must pay a higher interest rate than, for example, Greece. The average negative budget deficit in France between 1959-2023 has been -2.57%! The highest level was in 1959 with +1.50% and the lowest level in 2020 was -8.90%. If French citizens today are surprised by the development, the politicians have been exceptionally bad at conveying and explaining how the world works and what it looks like. Reality always catches up and now the French state is to some extent in the hands of investors who will buy French government bonds in the coming period. Certainly, interesting to follow.

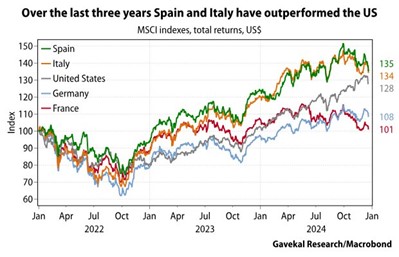

Stock markets in southern Europe developed better than northern Europe last year. At the time of writing, Spain has for the past three years developed in line with the S&P500, which is impressive given the strength of the US during the period.

Source: Gavekal Research/ Macrobond

The American stock market was in the spotlight last year with an unusually strong development. For the first time since 1998 and 1999, the S&P500 rose by more than 20% annually for two consecutive years. It was a combination of strong inflows, an American economy that once again surprised positively, the FED's interest rate cuts and, not least, the enormous interest in AI. Nvidia alone accounted for 21% of the S&P's increase last year - unparalleled.

The Nasdaq 100 rose by 25% and has thus risen 14 of the last 16 years. For the past 10 years, the big American technology companies have been running circles around everything else.

Source: Bloomberg

It took 7398 days for Nasdaq to rise from 5,000 to 10,000. From 10,000 to 20,000 it took only 1645 days.

Source: CNBC

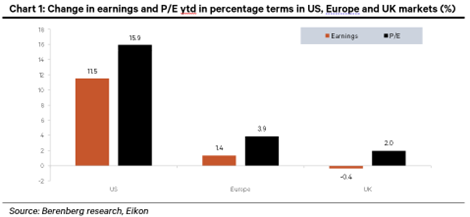

The image below shows the distribution between earnings growth and rising earnings multiples that resulted in the 2024 price development for the US, Europe and the UK. It looks a little thin in Europe.

The Chinese stock market rose 11.6% in 2024 after falling for three years straight. In Hong Kong, the stock market rose by 18.3% after falling for four years in a row.

Other strong stock markets last year were Taiwan +32% and Japan +20%. However, everything pales in comparison to Argentina where the somewhat unorthodox president, Javier Milei, has had great success with inflation, growth and a strengthened peso. Argentina's stock market rose last year, measured in euros, by 124% after rising 56% in 2023.

Source: X, The American Conservative

The value of bitcoin shot up sharply after Donald Trump was elected president. Last year's increase ended at 120% and the value of Bitcoin is now close to USD 2000 billion, which is almost equivalent to the market value of companies such as Alphabet and Amazon.

Source: Bloomberg

BlackRock, the world's largest asset manager, broke a new record in 2024 when it launched a new ETF that invests exclusively in Bitcoin. In 11 months, AuM went from 0 to 50 billion USD. No other ETF has ever had a similar development in assets under management.

Another thing that stood out at the end of 2024 was that, according to investigators, Russia likely intentionally destroyed infrastructure by using anchors to tear data cables on the bottom of the Baltic Sea. A symbolic visit to the topical vessel, Yi Peng 3, with representatives from Finland, Denmark, Germany and Sweden was all that could be achieved.

Finland was more direct when, during Christmas Day, they boarded and seized the ship Eagle S, which attacked four data cables between Estonia and Finland. Admittedly, it is not directly comparable to the Yi Peng 3, as the Eagle S is not Chinese and to quote Edward Lucas, Senior Adviser and Senior Fellow at the Center for European Policy Analysis, "Germany's garbed government was not involved either".

Source: Kluddniklas

Elon Musk featured during the holidays on Welt am Sonntag and praised the right-wing party AfD (Alternative for Germany) for its excellence. "The AfD, even though it is described as far-right, represents a political realism that resonates with many Germans who feel concerns are ignored by the establishment". Welt's editor-in-chief wrote in a direct reply that Musk's political diagnosis was reasonably correct, but that he completely forgot the geopolitical perspective, which for the AfD includes Germany leaving the EU, a desire for the West to end sanctions against Russia and start trading with Russia instead. They also want the Nord Stream gas pipelines to be put back to use.

Unsurprisingly, the criticism from many was weighty about both the content itself, and the fact that the post was at all published. Regardless, the responsibility rests heavily on the next government in Germany. How it turns out has significance not only for Germany but also for Europe.

In conclusion, and when we drove around Denmark in December and visited various companies, we were captivated by this article in Börsen (Denmark's Financial Times). A new ETF has been created that only invests in companies that do not consider any ESG-related issues.

Source: Börsen

Portfolio companies

Volution

During the month, our UK ventilation company released an update on developments during the period August to November. Organic growth is still positive at 2.5%, with a margin that exceeds last year's. The coming months have simpler comparative figures, which should mean that Volution can at least reach the analysts' estimate of around 3% organic growth for the year.

The focus for Volution in 2025 is to integrate the big acquisition of Australian Fantech. We wrote about the acquisition in our monthly newsletter for September and stated there that Fantech should contribute to an increased profit per share of at least 10%. The acquisition, together with an end market that can possibly recover after a couple of years of tougher development, provides the conditions for the Volution share to be able to also develop well in 2025.

In December, the stock rose 1%. For 2024, the stock rose 29%.

Diploma, Rotork och 4imprint

As a group, the fund's other UK holdings had a weak month ranging between 4-6% in negative returns without any news being released. For the full year, Diploma and 4imprint have returned 19 and 7% respectively. Rotork is a relatively new holding for the fund.

Biotage

Biotage was one of the fund's top contributors in December with no news. As previously mentioned, the company was excluded from the Stockholm Benchmark index last November when we took the opportunity to increase our position. The stock rose 19% in 2024, and we think this could be a winning stock in 2025. The valuation is a low 15x EV/EBITDA in 2026 on our estimates, while we have received several signs that the underlying market is accelerating. The stock rose 6% during December.

Scandic

With an extra dividend in December of SEK 2.50 per share (3.7% dividend yield) and a share price that rose 1.6%, Scandic was one of the fund's best contributors last month. In addition, the company started its buyback program, where it has so far bought back just over 1 million shares, which corresponds to half a percent of outstanding shares. We also see incoming data showing that the end of the year looks to be a bit better than what the market has been expecting.

The company will hold a capital markets day in February, which we believe, and hope will be a positive event. A little anecdote is that the last time a capital markets day was held was on February 18, 2020, a few days before the pandemic hit hard. It was also CEO Jens Mathiesen's first public event. We think the timing will be better this time!

Bonesupport

Bonesupport was the fund's best contributor, both during December and for the whole year. The stock rose 6% in December and a whopping 106% for the whole year. Despite large numbers, we think the rise is justified. In addition to beating the estimates on the first three reports, the company has received approval for the use of Cerament BVF for the indication "interbody fusion" in the spine. The application is for the USA and the extraordinary thing is that the approval only took 10 days (normal processing time is 90 days). We suspect that clinical data from studies is so strong that there is nothing to discuss. Just a few weeks later, the company received market approval for the indication “open fractures” in the US. Cerament G is the first and only combination product to be approved in the US for this indication.

During the autumn, the important SOLARIO study was presented, which shows that bone replacement with local antibiotics enables reduced systemic antibiotic treatment. Bone replacement materials such as Cerament G and Cerament V achieve equally good infection prevention with a short systemic antibiotic course of a maximum of seven days, compared to the previous minimum of four weeks. The group also had significantly fewer and milder side effects with the lower antibiotic course. This is a big step towards Cerament G/V being recognized as the standard of care in the treatment of skeletal injuries. Another nice piece of news in December was that Bonesupport is now included in the Stockholm Stock Exchange's executive room, Large cap. Well done!

Summary

We are, overall, happy with 2024, although there were a few things we could have done better. What has been distinct in our management during the year is that we have always had a clear view of the market, which has been correct, except for the end of the year. Even more important is that we made few mistakes in our company analysis and always had a strong understanding of valuation and events that affected the share price. On the occasions where we have had irrational price movements, we have in many cases gone against the market and most of the time added value. At an individual company level, it has also paid off not to sell too early in Bonesupport as the market gradually discovered this phenomenal company during the year.

The best contributors for the year were (again) Bonesupport, Cargotec/Kalmar, Accelleron and Euronext. These positions accounted for a total of nearly 90% of the reported full-year result.

What we are undoubtedly most dissatisfied with during the year is our holding in Campari, which we started investing in in late summer 2023. A woeful communication to the market in September led to the resignation (or firing) of the newly appointed CEO, which was then followed by a very weak Q3 report in October. We were wrong and took the consequences of it and reduced it to currently only an observatory position. Naturally, we are unusually humble from here, but after falling 39% in 2024 while consumer purchasing power is on the rise, there should be room for a rebound in 2025. The stock market value of this company with all its well-known brands is now down to a low 7 billion euros.

Another disappointment was the development of the real estate sector. Throughout the year, we have held just over 10% of the fund in Swedish real estate, and during the first months of the year this was concentrated to SLP and Corem. Then Balder was added at the expense of Corem and it is these three companies that we still own. Corem is clearly the smallest and SLP the largest with a current position of approximately 7%. The development for the full year for Swedish real estate was a big disappointment with a return for the sector of only -2%. Since the peak at the beginning of October, the sector index fell by a full -17%, which we still don't quite understand. The spread of our holdings' full year return was very large with SLP at +19.8%, Balder +7.8% and Corem's very weak –37%! From here, we have a strong opinion that the sector will develop well in 2025.

Looking back a year, our summarized view was as follows:

- We expected a decent stock market year in 2024.

- The conditions for good stock picking were better than in several years.

- Falling interest rates and inflation should be able to provide extra strong development for small and medium-sized companies where the positioning was also modest.

- We expected strong inflows into the stock market.

- European shares had a good starting point as the valuation was at a record low in relation to American shares, while at the same time European small companies in relation to larger companies were at their lowest level in 20 years.

- Falling interest rates and inflation would make people happier, not least in Sweden, and economic activity should be able to pick up in a few quarters.

- We did not expect an American recession.

- The outcome was that we got to experience a decent and, in some markets, an unusually strong stock market year, so that was right.

- Stock picking worked well, so that assumption can also be considered to have been achieved.

- The smaller European companies developed as a group only in line with the larger companies, so here we were wrong. In Germany and the USA, for example, it even fared significantly worse.

- There were strong inflows to the stock market, but unfortunately it did not go to Europe to any great extent, but most of it landed in the USA.

- The record low valuation of European stocks relative to US has reached new record levels, so we were wrong to think the gap would close. Small companies in comparison to larger companies are traded at roughly unchanged levels compared to a year ago.

- Interest rates have fallen significantly, and inflation has long since been defeated (new problems may arise, however) and we are seeing a strong recovery in consumer confidence. However, economic activity has not picked up as we and many others predicted. It is now expected to take place in the coming quarters.

- There was no US recession this time either and the strength of the US economy surprised the vast majority of people, so that was also right.

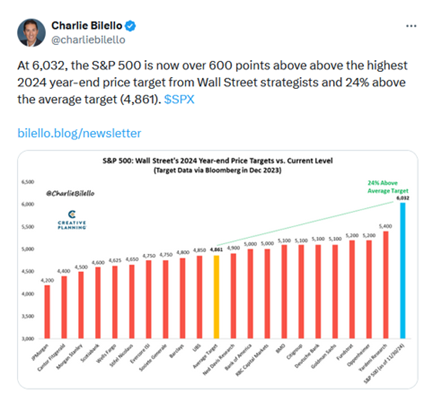

All strategists at well-known firms again had too cautious assumptions for the US stock market in 2024. We had the same picture last year which showed exactly the same thing, that is, all had too cautious assumptions. Heads up all strategists, this is not acceptable.

Source: @charliebilello

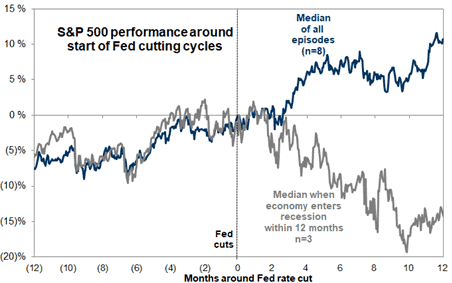

We also had this picture a year ago as one of the drivers for how we viewed the outlook for 2024. It has now been four months since the Fed started cutting US policy rates, so if history is to repeat itself, not much happens in the first half of the year and then starts to rise in the second half of the year. It sounds like a possible scenario as in six months we should know what the new tariffs look like and what the consequences will be.

Source: Goldman Sachs

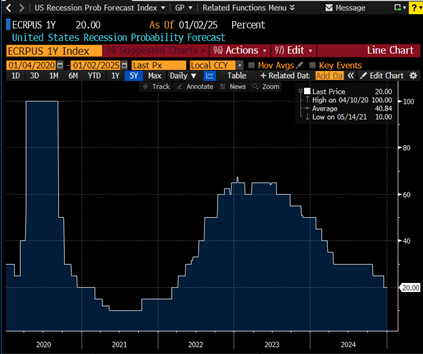

The probability of a US recession now is down to 20% according to the consensus, compared to closer to 60% by the end of 2023. A huge difference.

Source: Bloomberg

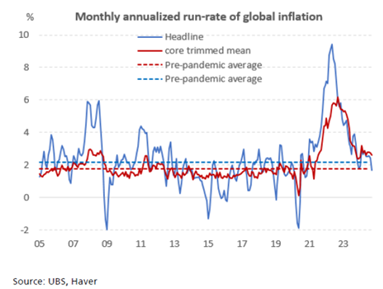

What a development for inflation in the last two years and with all the consequences it brought for the world economy. We'll see what happens now that the new US administration will most likely impose new punitive tariffs.

.

Source: UBS, Haver

Would the last one out please turn off the lights. The Chinese 10-year yield has had a complete meltdown and continues to signal major problems for the Chinese economy.

Source: Bloomberg

The reverse is true for the US 10-year yield. What is very unusual is that the 10-year interest rate rises sharply after the FED starts lowering the interest rate as it did in September. It sends a signal from the bond market that it may be wrong to cut interest rates when the economy is as strong as it is. Or perhaps a more long-term signal that budget deficits are too high. We shall see, but this could develop into a minor storm in 2025.

Source: Bloomberg

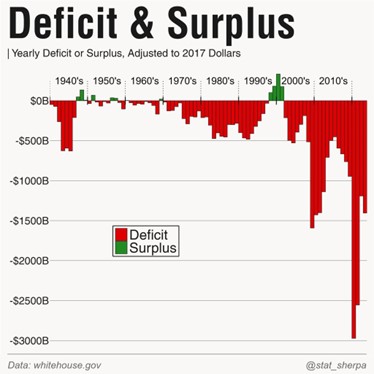

Rising interest rates combined with huge budget deficits is not a good combination.

Source: whitehouse.gov, @stat_sherpa

However, it is not something that has affected the sentiment of the American stock market. It is at an absolute peak level and according to the picture below, the consumer will soon go into a complete state of euphoria.

Source: University of Michigan, Goldman Sachs

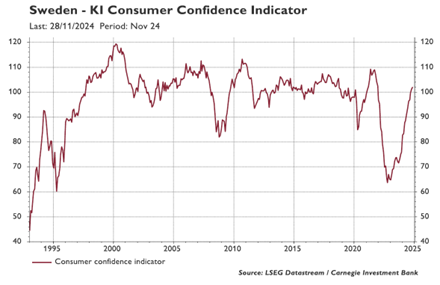

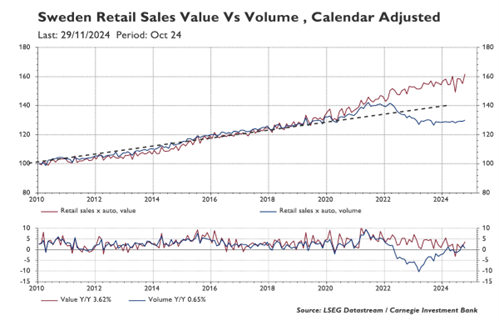

From completely bombed out levels, this is already happening in Sweden, which is probably the country in Western Europe that was hit hardest by rising inflation and interest rates.

Source: Carnegie, LSEG Datastream

Swedes' consumption is slowly starting to recover from an unprecedented inflation shock. It also means a little more inflow into the equity markets instead of most of the disposable income going toward interest payments.

Source: Carnegie, LSEG Datastream

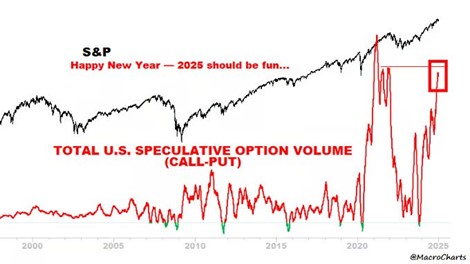

Another way to look at the sentiment of the US investor - the relationship between outstanding call and put options. The mood is bordering on euphoric.

Source: X, @Macrocharts

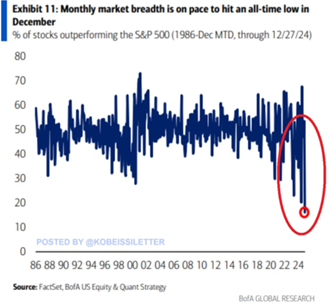

As you know, we do not invest in US stocks, but given their importance, we naturally keep an eye on it and show below a few observations.

The optimism that US investors experienced and are experiencing in combination with an extremely concentrated rally is unusual and could backfire. Below shows the breadth of the market over the last 40 years. It is an extremely small selection of stocks that has driven the US stock market. Only 10% of the stocks in the S&P500 have recently had a stronger performance than the S&P500 as a whole.

Source: BofA Global Research

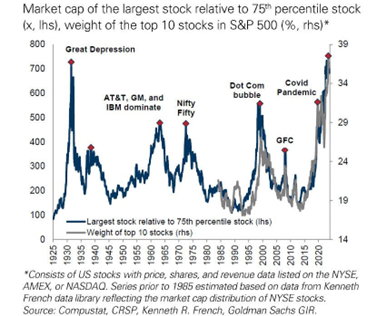

The 10 largest companies in the S&P500 are now nearly 800x larger relative to the 75th percentile. The last time we were at these levels was during the great depression almost 100 years ago.

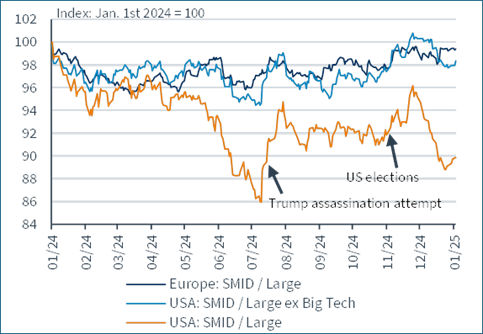

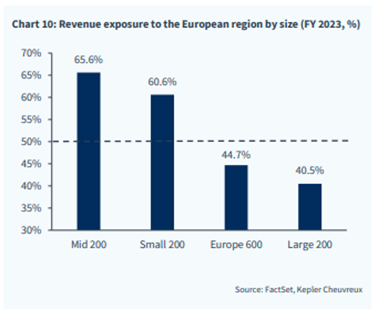

In the USA, smaller companies have had a significantly weaker relative price development and December offered a proper downward movement. Interestingly, European small companies tend to develop better over time than the corresponding American companies. One reason for that is probably that 40% of the American companies included in the small company index have negative earnings compared to only 10% for the European ones.

Source: Kepler Cheuvreux

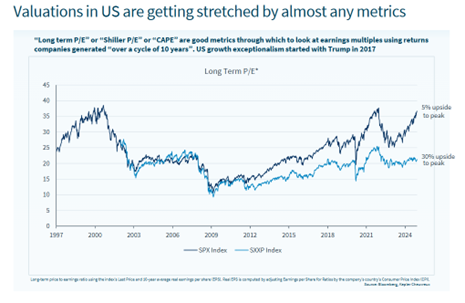

Shiller P/E for US and European stocks below. Price divided by the last 10 years' earnings adjusted for inflation.

Source: Kepler Cheuvreux

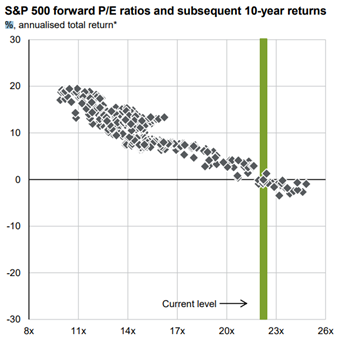

Below is a historical valuation at each given time and since then the following 10 years' return. Either there will be a very mediocre return going forward for US stocks or the market is underestimating the companies' earnings. We don't know, just observing.

Source: Goldman Sachs

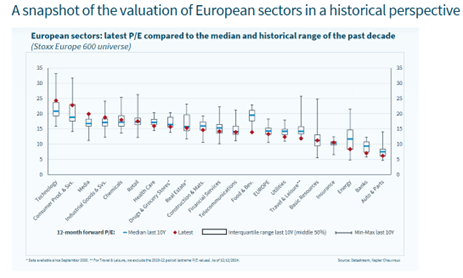

What then do the conditions look like for European small and medium-sized companies. Better than in many years is the short answer and below are several images to illustrate and explain our positive outlook. Current European sector valuation. Most sectors are at historically low levels.

Source: Datastream, Kepler Cheuvreux

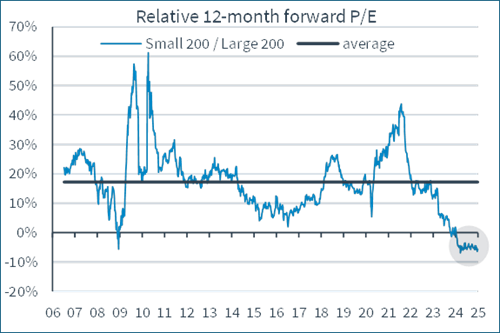

European smaller companies' valuation relative to large companies. The smaller companies are valued today at a larger discount than during the financial crisis. It feels strange, but avalanches of passive blind capital are probably part of the explanation.

Source: Kepler Cheuvreux

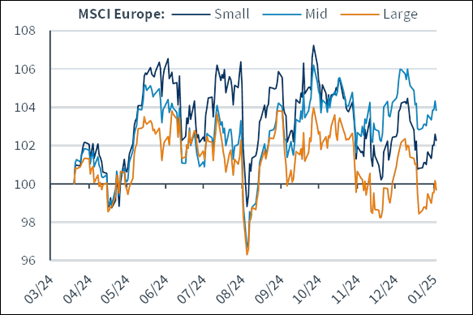

In the last six months, smaller companies have developed only a few percent better than larger companies.

Source: Kepler Cheuvreux

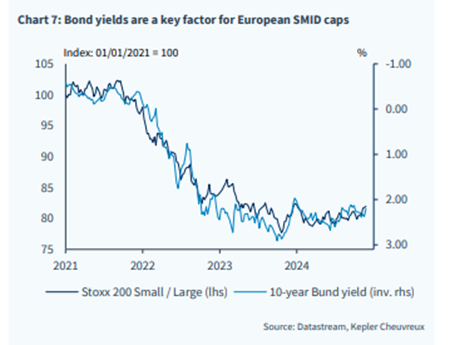

The relationship between small and large companies in relation to the inverted interest rate. Small companies are the most interest-sensitive share class, which is clearly visible in the image below when interest rates, in 2022, rose sharply. Smaller companies have performed marginally better than the larger ones in the past six months, but there should be significant potential here going forward when European interest rates likely continue to fall.

Source: Kepler Cheuvreux

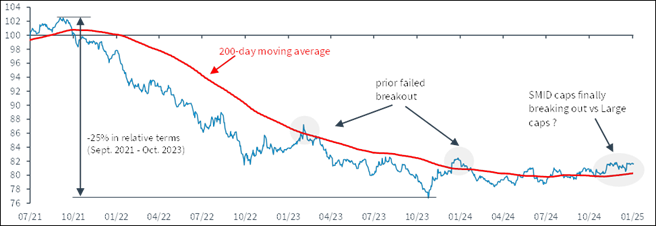

Are we witnessing an ongoing break-out in Europe for smaller companies in relation to larger companies?

Source: Kepler Cheuvreux

Smaller companies should have fewer problems with future tariffs as they have more domestic operations in relation to larger companies.

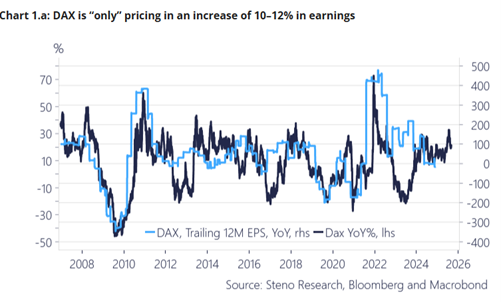

The German stock exchange is currently pricing in 10-12% profit growth. In addition, investors generally have an extremely modest positioning towards European shares. A low valuation combined with reasonable profit expectations is a good cocktail for a good stock market year. The corresponding profit expectation for the USA is around 20-25% and the positioning is sky high.

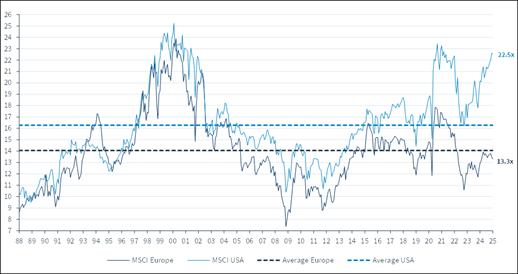

Current valuation measured in P/E ratios for the US and Europe.

Source: Kepler Cheuvreux

A new relative low for Europe compared to the US.

Source: Kepler Cheuvreux

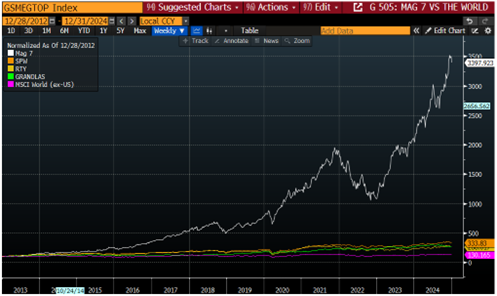

We save the best picture for last. It was Charles Schwab's global investment strategist, Jeffrey Kleintop, who produced the data and created the image. It shows that if you take Nvidia out of the S&P500, measured in the same currency and since the market reversal in October 2022, the US and Europe have returned the same with a slight advantage to Europe. You should bear in mind that "S&P499" contains the six other companies in “Magnificent”. Let that sink in and then include the two previous images on valuation as well as the extreme positioning found in both the US and Europe. It's a good line-up for another interesting investment year.

Source: Charles, Schwab, Macrobond, Financial Times

In conclusion, several important prerequisites are in place to achieve a positive stock market year in 2025 and on our home turf, Sweden, things look unusually good. A competitive business environment in combination with strong state finances means that Sweden, unlike many other countries, can afford an expansive fiscal policy without in any way jeopardizing international trust. But as a small export-dependent country, we are highly dependent on the outside world and there is certainly no shortage of worries out there. On the other hand, these will one day fade away and it could happen already this year, which is highly anticipated for many reasons.

German and French politics determine much of the direction and speed of Europe and the coming months will be important. The global economy is undergoing one of the biggest changes ever with AI development and it is happening at a speed and scale rarely seen. And finally, the one that trumps all the above, the effects of the new US administration on the world economy. It is safe to say that none of us will be bored!

Finally, I would also like to extend a big thank you to my team, Cecilia, Fredrik and Gustav, who contributed greatly during the year in various ways and often under great time pressure. Amazingly well done!

And then most importantly, to you, our friends and investors. Many thanks for your positive input and feedback in 2024 and we wish you all a successful and healthy 2025.

Mikael & Team

Malmö, January 10th, 2025

IMPORTANT INFORMATION. This is a marketing communication. Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested. Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.