This material is marketing communication.

Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class’ return. The information below regarding returns therefore differs from the returns in other share classes.

Before making any final investment decisions, please read the prospectus, its Annual Report, and the KID of the relevant Sub-Fund here.

DECEMBER PERFORMANCE

The fund’s value increased by 0.1% in December (share class I SEK), while the benchmark increased by 1.3%. Since the change of the fund’s strategy at the beginning of September 2023, the fund’s value has increased by 26.5% compared to an increase of the benchmark by 24.3%.

Source: Coeli European

* Adjusted for spin-off of Rejuveron

** Includes September 1 (strategy change to long-only implemented September 4 2023)

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

EQUITY MARKETS / MACRO ENVIRONMENT

The past year was anything but calm and quiet. It got off to a sprint with the DeepSeek story in January, which quickly put real pressure on American tech companies. After that, we experienced Vice President, JD Vance's, anti-European speech at the Munich Security Conference, which caused European defence stocks to rise sharply. Shortly after, followed a disgusting bullying of Ukrainian President Zelensky in the White House. The crescendo came on April 2nd when President Donald Trump gave a farcical presentation of the new tariffs that would be widely implemented. In less than an hour, he had single-handedly created unprecedented economic and political chaos throughout the world.

Before we move on, a few comments about December. Europe had a significantly stronger development than the US, where the expected Santa Claus rally failed to materialize. The S&P500 closed down every day for the last four days of the year, a feat that has only happened twice before since 1950. Although the movements were modest, 99 out of 100 companies on the Nasdaq were down on the last trading day of the year, which was the weakest performance on December 31st since 1990.

Source: X

For a few leading indices, the development in December was as follows, all measured in percentage and in local currency: Stoxx600 2.7, MSCI European Small Cap 2.3, Carnegie Small Cap Index 0.3, S&P500 -0.1 and Nasdaq -0.7.

The fund rose by 0.1% in December, which was 1.2% worse than our benchmark. For the full year 2025, the fund rose by 4.2%, which was 9.3% worse than the benchmark. Since the strategy change in 2023, the fund has risen by 26.5% compared to our benchmark, which rose by 24.3%. The Swedish krona continued to strengthen during December, which affected the fund's return (in the SEK class) negatively by -1.2%. The corresponding figure for the full year was -5.2%.

The fund's best contributors in December were Bawag (+12%), Babcock (+10%) and Konecranes (+6%). The worst contributors were Asmodee (-9%), Verisure (-16%) and Hill & Smith (-5%). Bawag and Babcock belong to the red-hot segments of banking and defence stocks. Bawag rose last year (excluding dividends) by 59% and Babcock by a whopping 148%.

Asmodee's decline in December is difficult to explain and is likely entirely flow-driven. Swedish small-cap funds have been plagued by significant outflows throughout the year, but especially during the last quarter of the year, which has led to forced sales, and we have a strong belief that the stock will be a significant contributor in 2026. Verisure's decline is largely explained by the fact that it rose almost 8% in the last minutes of November 28th, when passive blind index funds bought shares at the close completely without price discipline at a price of 16.52 euros per share. A month later, the share closed at 14 euros and that says everything about index management as a phenomenon.

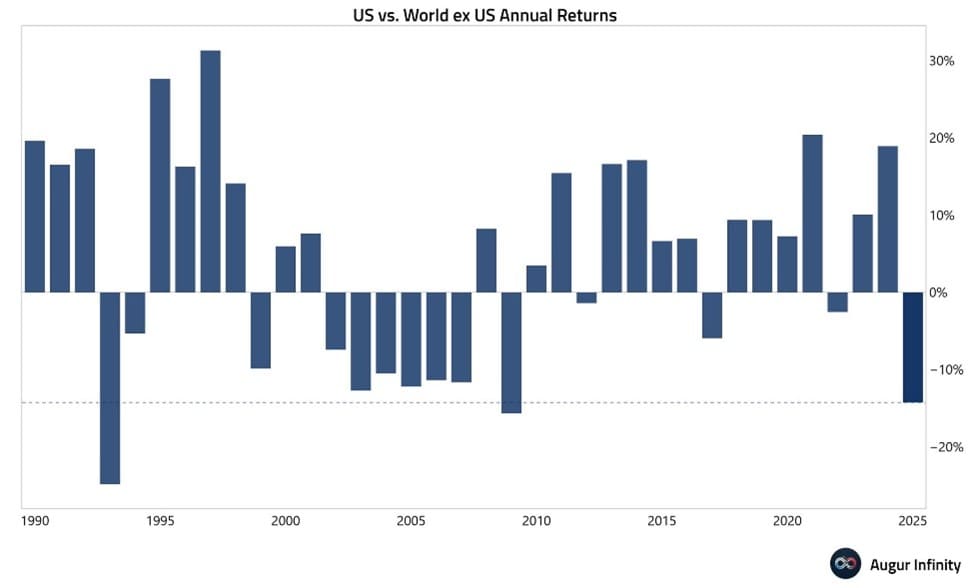

Below is a summary of the development for 2025. The column second farthest to the right measured in local currency and farthest to the right measured in SEK. In summary Europe performed significantly stronger than the USA in 2025. S&P500 rose by 17% compared to SXXP600 which rose by 32%, measured in USD. The second thing to note when studying the picture below is that SEK had a very strong 2025 while the dollar had a historically very weak year, see also the development in Asia measured in SEK.

Source: Bloomberg

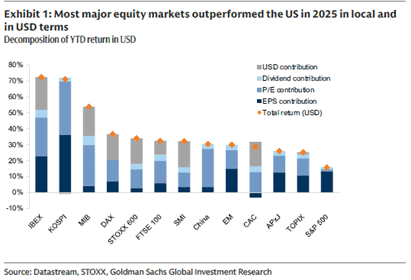

In the US, returns were concentrated to the large tech companies. In Europe it was banks that stole the show, see image below, where the sector was, once again, the winner for the fifth year in a row.

Source: Bloomberg

At its darkest, in April, investors were depressed. As is often the case, it was an excellent indicator of when to take on more risk. The fund made significant and successful purchases of Asker shares at the time, which were partially sold a month later at a 40% premium.

Source: X

The broad European index rose 27% from its lowest level when people were most depressed.

Source: Bloomberg

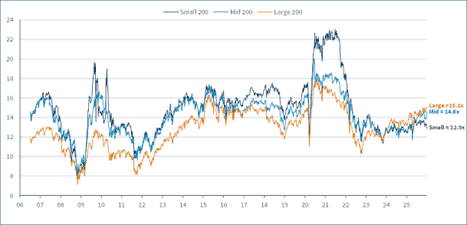

The development of SMID in relation to larger companies over the year.

Source: Goldman Sachs

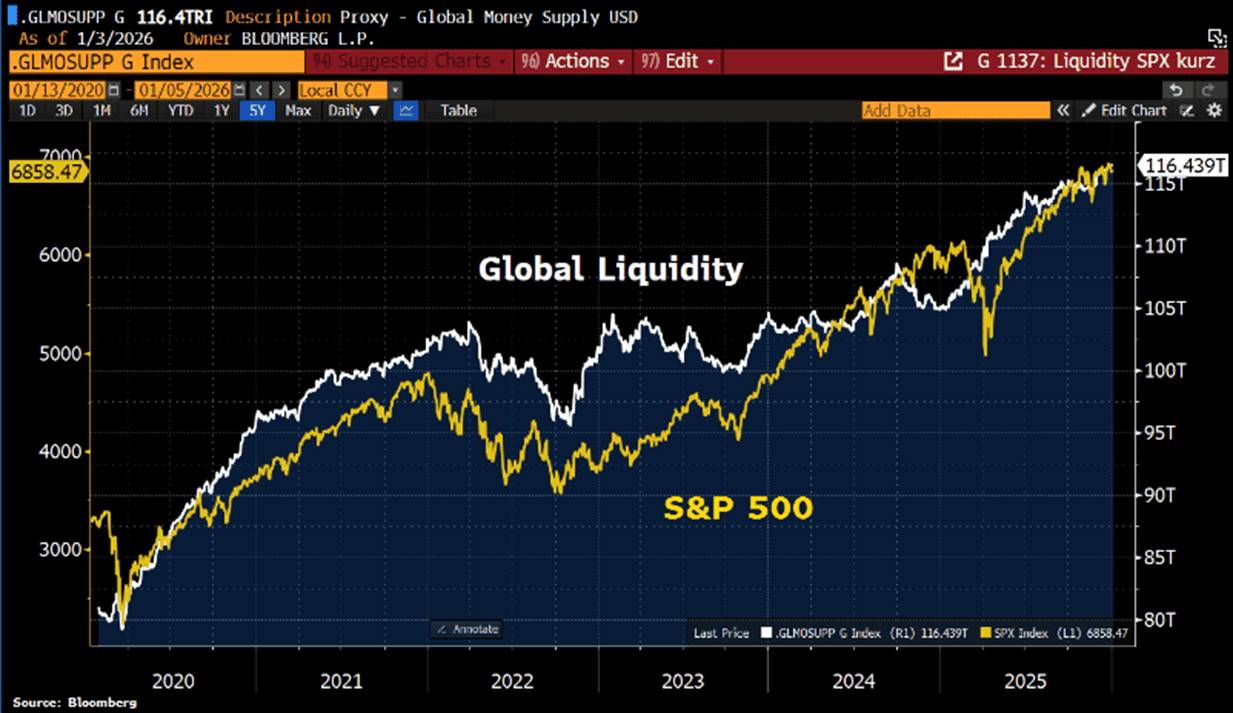

The correlation between global liquidity and stock market performance is very high. The prospects for liquidity to continue to support the stock market in 2026 are considered decent.

Source: Bloomberg

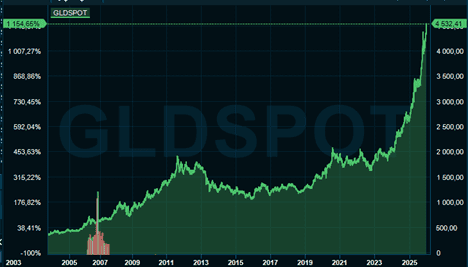

Various metals performed strongly in 2025, especially the precious metals gold and silver which rose by 67 and 158% respectively. Below the gold price since 2005. A growing distrust of US government bonds likely contributed to the gains.

Source: Infront

In the past, the price of copper was a reliable indicator of how the economy would develop. This is probably still true to some extent, although a huge investment need in electrification and a weak dollar were strong contributors to the copper price rising by 42% in 2025.

Source: Bloomberg

Gold also outperformed bitcoin in 2025, which had a relatively weak year with a 6% negative performance (measured in a weak dollar). Below is the development of gold and bitcoin (green line) since 2023.

Source: Bloomberg

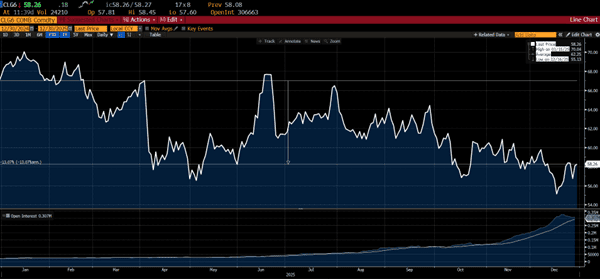

At the beginning of 2025, the oil price was a concern, and the consensus was that an accelerating economy and some bottleneck problems at production stage would create an upward price pressure. That did not happen, rather the oil price fell by 15% (measured in SEK by a whopping 29%). Good for the world economy!

Source: Bloomberg

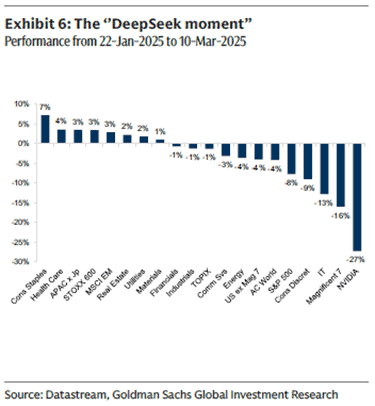

When the Chinese AI service DeepSeek became known in early 2025, American tech stocks came under significant pressure.

The weak dollar hides a historically large return discrepancy in 2025 between the US and the rest of the world.

Illustrated in relation to various relevant indices and measured in USD.

On December 5th, an 84-year-old international rules-based post-war order came to an end (the Atlantic Declaration created by Winston Churchill and Franklin D Roosevelt) when the new US national security strategy was published. The US now openly portrays Europe as a bigger problem than Russia and that they will support nationalist and right-wing populist forces. Europe is facing “civilizational annihilation”. Russia was content and cheerful when stating that the US strategy “in many respects corresponds to our view”. Russian press wrote that Trump is closer to Putin than the leaders of Europe.

The US State Department’s updated website on the Atlantic Declaration now states: Milestones in the History of US Foreign Relations has been retired and is no longer maintained. What abysmal darkness. Polish Prime Minister Donald Tusk was clear. “Right now, 500 million Europeans are begging 300 million Americans for protection against 140 million Russians – who have not been able to overcome 50 million Ukrainians in three years.

Source: Michael de Adder

At the time of writing, it became known that the United States had captured Venezuelan dictator Maduro and flown him to the United States. Is this further evidence of the new world order where the big countries do as they please and do not care about international law? Is the next piece of the puzzle that China takes on Taiwan? Europe is absolutely right in investing enormous amounts in building up their defence capacity. Polymarket is currently giving Donald Trump a 14% chance of winning the 2026 Peace Prize. That feels generous.

Source: Kluddniklas, Eriksson25

When you thought the absolute bottom had been reached, below is Republican Katie Miller after Trump's press conference on Venezuela and Maduro. It is an extremely serious attack on an ally and loyal NATO member.

Source: X

Below is last year's news concentrated into one image. Inflation and the Chinese doll Labubu are at the top - it's hard to come up with a sensible conclusion.

Source: Axios Visuals

Time collectively names AI architects “Person of the Year.” Is the front page below another excellent contraindication?

Source: Time

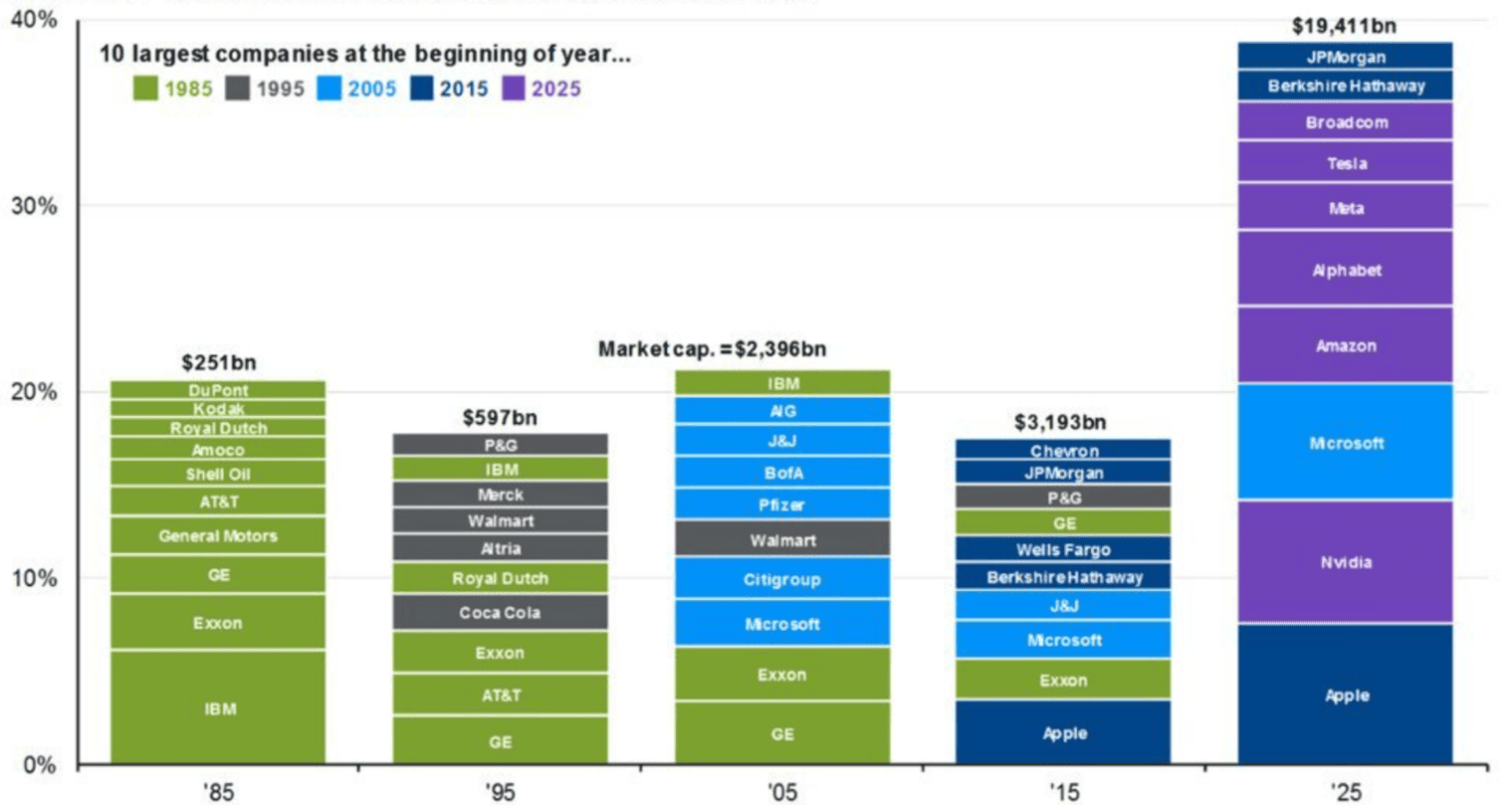

Interesting picture showing the largest companies in the US at different times. Four companies from today were on the list 10 years ago. 20 years ago, only Microsoft was on the list. There will probably be major changes in the next 10 years again, and what will the list look like then?

Source: X

PORTFOLIO COMPANIES

Volution

In an otherwise news-poor month for our portfolio companies, Volution released an update for the start of the fiscal year ending in July 2026. Organic growth landed at five percent – slightly higher than many analysts had hoped for – and margins were at similar levels to the previous year despite integrating a previous acquisition that is margin-dilutive. Another set of positive figures slightly above expectations from Volution.

In addition to the results, another acquisition was announced. This time it is Australian “AC Industries”, which sells ventilation equipment for underground mines. Our initial calculation indicates that the acquisition adds around 6-7% to Volution’s profit before any synergies.

AC Industries “benefits” from the fact that their products wear out quickly in the harsh climate of underground mines, which means that around 70% of sales are of a recurring nature. Historically, AC Industries has grown by double digits and most recently had an EBITDA margin of 36%. Volution is paying EV/EBITDA 10x for the acquisition and plans to help the company commercialize globally, as it is currently primarily exposed to the Australian market for obvious reasons.

Despite this news, Volution shares rose only by 2% in December.

Asmodee

Asmodee shares had a tough month without major news and fell 9%. As we described in the previous letter, we believe that the share deserves to be higher given the latest report. Looking at various external indicators, there is much to suggest that the strong numbers will continue for upcoming report releases, even if the odds are against them. The company has recently refinanced a bond on better terms and has received a higher rating from one of its credit institutions.

Bonesupport

The discrepancy between Bonesupport's share price and its operational performance was, to say the least, remarkable during the year. That said, it can be stated that the market was inflated towards the end of 2024 when the price peaked at just over SEK 400 per share. Apart from the impact of the US dollar, which is significant here, the underlying estimates are largely unchanged since the beginning of the year. As of the third quarter, Bonesupport had almost 85% of its sales in US dollars. During 2025, the dollar lost 17% against the Swedish krona. Even if the fund sold a large part of its holding at the beginning of the year, with hindsight, we would have sold the entire position. With the share price halving in 2025, it is now back to levels not seen in two years. During the same period, profits have more than doubled.

Last year, the share also rose to become one of the most short-listed on the Stockholm Stock Exchange. This is always concerning, but we note that several new and different short-selling theses have been successively presented during the year and so far, the company has continuously shown that these have not been correct.

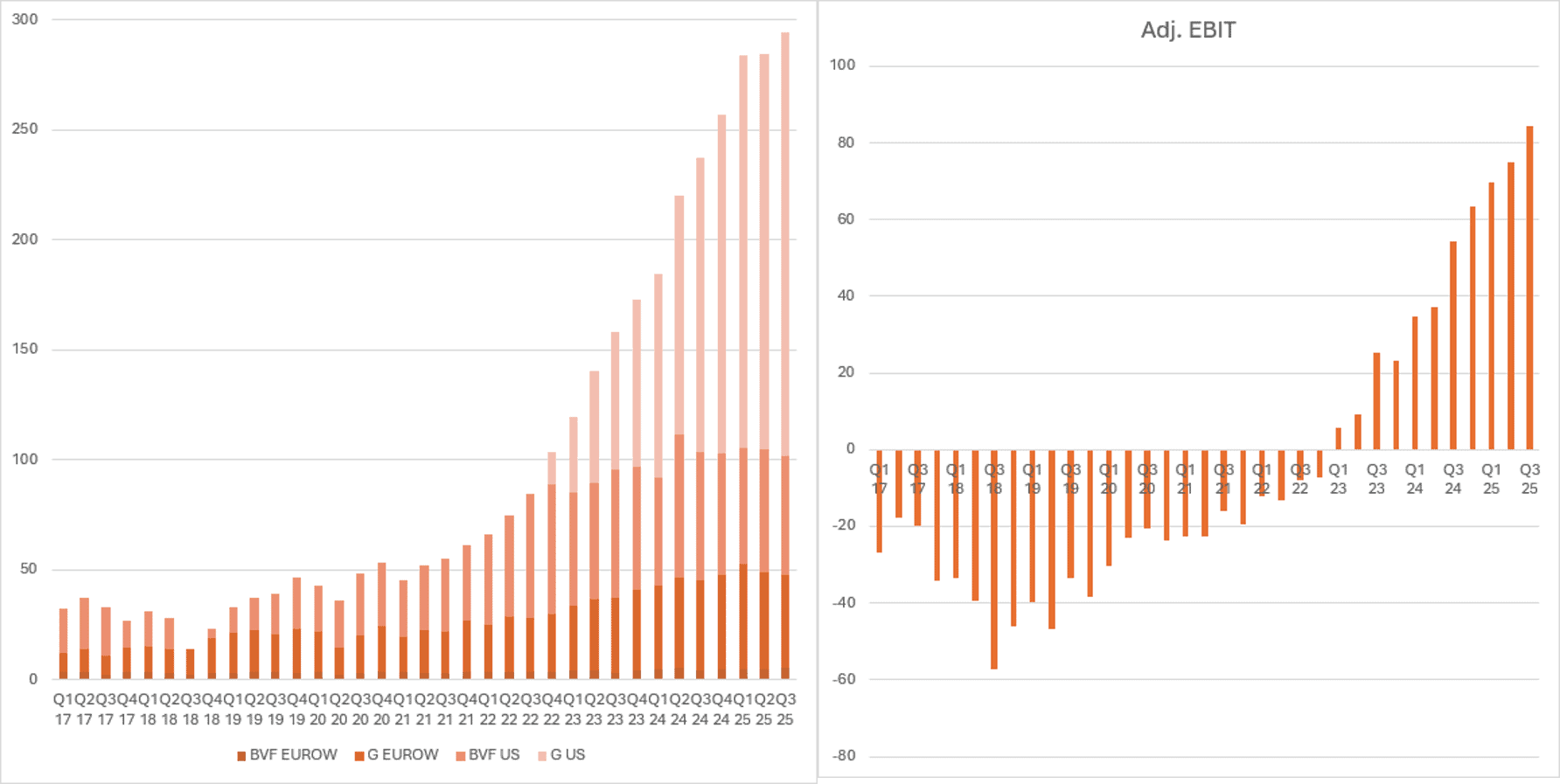

The report for the third quarter was approximately 3% worse than expected, but the company was clear in connection with this that the full-year forecast of at least 40% growth remains accurate. The weakness in the report was found in Europe and within Cerament BVF. Cerament G in the US, on the other hand, grew 57%, adjusted for currency. Since the beginning of 2025, organic growth has amounted to 41%. Bonesupport is now valued at just over 17 times operating profit for 2027, which implies that growth could decline relatively sharply without the valuation appearing strained. We have no reason to believe anything other than that the company will reach its forecast.

Sales by product and geography as well as adjusted operating profit are reported below.

Source: Bonesupport, Coeli European

SUMMARY

2025 was in many ways an extreme year with wide spreads in returns between countries, sectors and small and large companies. Reflecting on this with over more than 30 years in the industry, it has been one of the most complicated years and despite a strong proprietary analysis with positive results, the fund has underperformed the benchmark significantly in 2025. Something we are obviously disappointed and frustrated with.

An important message is that all the underperformance came in the first quarter, while the performance during Q2-Q4 has been, more or less, in line with the market. In other words, the fund has not had a weak year but more correctly described, a weak first quarter.

A partial explanation for why the fund has not had a stronger performance is, simply put, that some of our largest positions have not performed strongly. Take SLP as an example; it has risen by a modest 6% compared to our benchmark, which has risen by 13.5%. The fact that SLP has developed 16% better than the Swedish real estate sector does not help much.

The fund's strongest contributors in 2025 were:

- Scandic Hotel

- Babcock

- Bawag

- Konecranes

- Euronext (sold, also among the strongest contributors in 2024)

The fund's worst contributors were:

- Bonesupport (was among the strongest contributors in 2022–2024)

- 4imprint (sold)

- HBX Group (sold)

- Viscofan (sold)

- Asmodee

By far the largest negative contribution came from Bonesupport, which fell by a full 51% in 2025. As mentioned, several times before, it was a large holding at the beginning of the year, and during January we significantly reduced our position. More than half of the year's loss in Bonesupport came in the fourth quarter (share price -36% in Q4) and in terms of size it is now a smaller position (outside the top 15). It is crucial for the company that it now meets its full-year forecast as there has been a lot of speculation of them issuing a profit-warning. Something we do not believe they will do but instead present a result in line with what has previously been communicated.

Aside from the fact that our largest positions were not the top performers there has been several extreme market movements which have affected the fund's return in various ways.

- Record-high difference in returns between different geographies.

- Very large spread in returns between growth and value stocks.

- Record-high sector concentration in Europe with bank and defence stocks as clear winners.

- The valuation difference between SMID and large companies is record-high and is now higher than during the 2008 financial crisis.

- A historically very large difference in returns between high- and low-quality companies.

- Historically large currency movements.

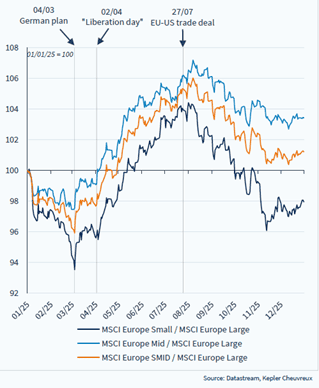

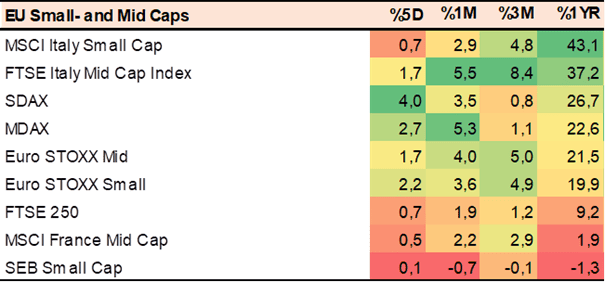

1) We have not been able to confirm this, but 2025 probably showed the largest difference in returns between geographies in modern times. The Italian Small Cap Index was a winner among smaller companies in 2025, and this is partly because there are a lot of banks included in the index. UK ended at 9% but adjusted for the pound falling 6%, the return in euros is only 3%. Sweden is at the bottom, and it is now the fifth year in a row (!) that smaller companies have performed worse or in line with larger companies. It is near impossible to estimate how this has affected the fund's returns, but with around 45% exposure to the British and Swedish stock markets, it certainly has not helped.

Source: Bloomberg, Coeli European

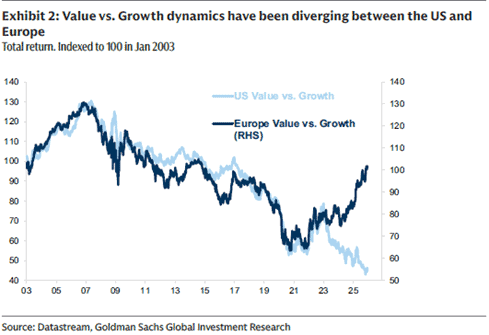

2) In the US, growth companies have been clear winners in 2025, while the reverse was true in Europe. The trend has benefited our positions in, for example, Scandic and Bawag, while having had a negative impact on our position in Bonesupport.

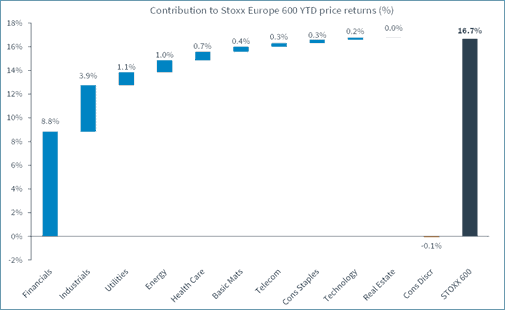

3) Banks account for just over half of last year's rise for the SXXP600. Industrials, with strong contributions from defence stocks, come in at a solid second place. The fund has about 10% of its capital invested in Austrian Bawag and British Babcock. Banks and defence stocks have a total weight of about 16% in the broad index.

Source: Kepler Cheuvreux

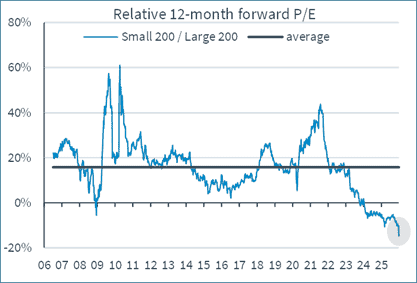

4) The valuation difference looks interesting to say the least. Outflows have created large price anomalies.

Source: Kepler Cheuvreux

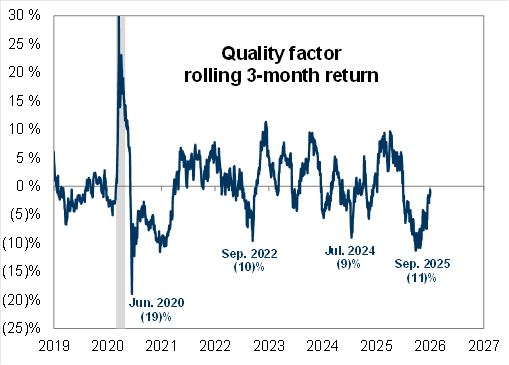

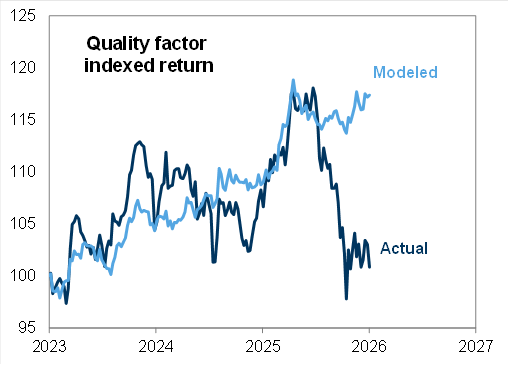

5) An expected acceleration in economic activity probably contributed to lower quality companies (higher leverage) performing significantly better than quality companies since April last year. The fact that interest rates rose significantly from April (German 5-year from 2 to around 2.5%) was probably the biggest factor that put pressure on companies with a higher valuation (higher quality). This undoubtedly contributed to the fund's underperformance during the year.

Given the strong underperformance for quality companies over the past six months, see image below, and the fact that quality companies usually perform better in the long term, we believe that this may be reversed this year.

Souce: Goldman Sachs

6) The US dollar plummeted last year, enthusiastically encouraged by the US administration. The pound also fell sharply and the self-harm from Brexit in 2016 is gradually eating into the British economy.

The dollar fell by 11 and 19% respectively against the euro and the krona. The pound fell by 6 and 14% respectively against the euro and the krona. The euro fell by 5% against the krona, which was also its negative contribution to the fund's performance in 2025.

Below USD/EUR since the financial crisis in 2009. With another 2-3 expected interest rate cuts from the Fed in 2026, an overwhelming consensus view is that the dollar will continue to weaken this year. When almost everyone has the same opinion, it doesn't take much for the outcome be exactly the opposite.

Source: Bloomberg

Looking ahead, the outlook looks relatively positive, as reflected by analysts and investors. When Bloomberg recently asked 21 strategists about the outlook for the US stock market in 2026, they all had a positive outlook driven by sustained growth, falling inflation and solid corporate profits. Some noted that there are some macro risks and that valuations are high.

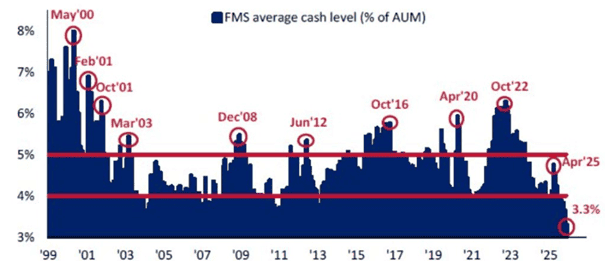

A positive market outlook has led to unusually low cash levels among managers.

Source: Bank of America

The positive outlook has also meant that the performance of the S&P500 (green) has been completely decoupled from the Bloomberg Economic Surprise Index (white). The reading of that is that the market expects a proper acceleration in the US economy.

Source: Bloomberg

Continuing on to Europe; Goldman Sachs has an economic model that includes profit growth, interest rates, inflation and several other parameters. The model, when run together with the development of quality companies, usually correlates well, but since this summer the correlation has broken. A good reason why we believe quality companies will perform well this year.

Source: Goldman Sachs

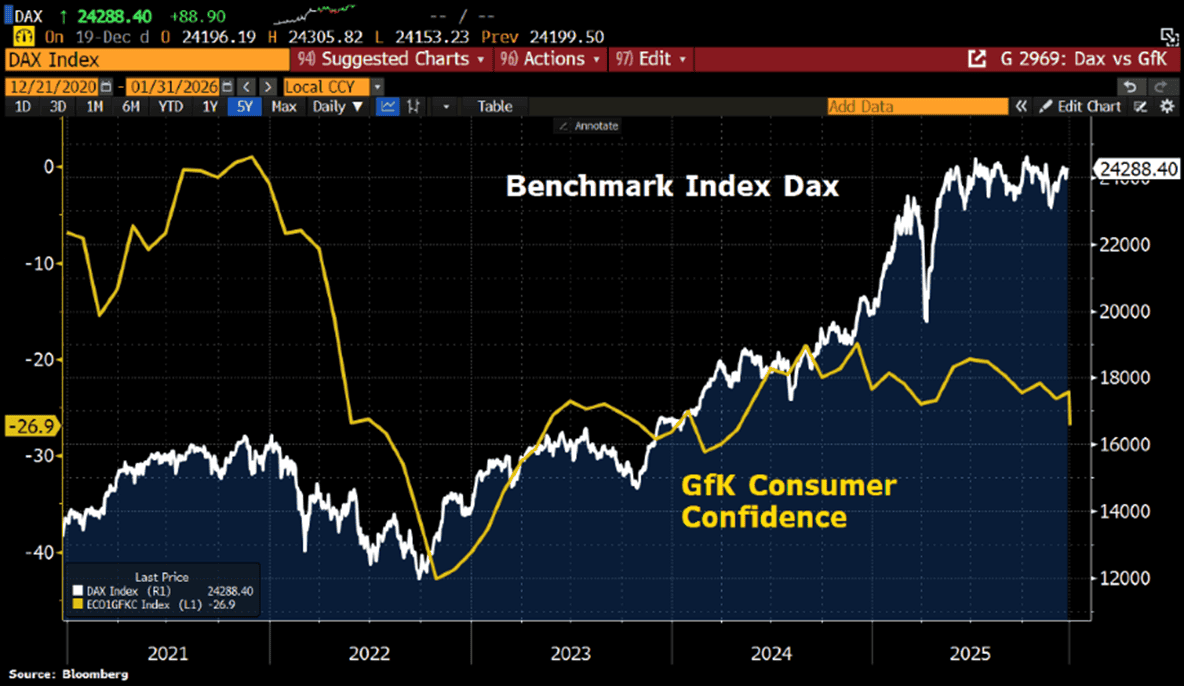

We now have, in various regions, a K-shaped economy, e.g. Germany below, where the stock market is rising while consumers are becoming increasingly depressed. The problem with this type of economy is that a minority are happy (shareholders) while a majority are feeling the effects of a sluggish labour market and savings that are starting to dry up. Will public spending and investment be enough to turn the tide? If Sweden is a leading indicator, things are starting to look bright.

Source: Bloomberg

The K-shaped economy is most clearly visible in the United States, where American households own more than 50% of the stock market. The top 10% of households account for 87% of total ownership and the top one percent own more than half (!) of total household ownership.

The US national debt is approaching 120%, which is unsustainable in the long term (it was 65% 20 years ago). Both Democrats and Republicans have increased the US debt burden enormously in recent years to finance wars, pandemics, financial crises and global recessions. Resistance is becoming evident and the weakening dollar is clear sign of this. In 2024, the US spent $850 billion on defence spending and a whopping $880 billion on interest expenses…

Blaming the Fed, as Donald Trump does, is at best, a way to score easy political points. If the Fed sets interest rates too low, inflation expectations increase and long-term interest rates start to rise. The election of a new Fed chairman this year is also a potential source of turbulence this year, with a new dovish strategy orchestrated by President Trump. We suspect that the administration will push ahead for as long as it is possible to push the problems ahead. Will the next president be handed a recession?

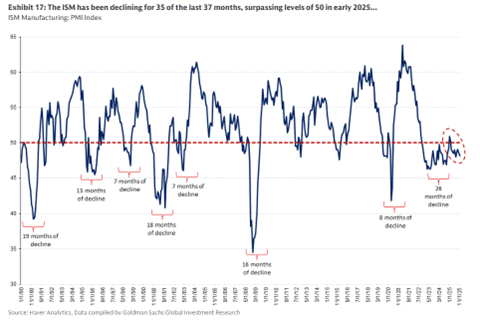

The German economy is still showing no signs of accelerating after three years of zero growth. The monthly purchasing managers' index unexpectedly fell in December to 47.7 from 48.2. In contrast, the index for the French manufacturing industry rose from 47.8 to 50.6. For the eurozone as a whole, the purchasing managers' index fell from 49.6 to 49.2. As a reference point, the index crossed 50 in Sweden at the beginning of 2025 and was 54.6 in December, while the US was at 51.6. The services sector for the eurozone continues to be above the 50 mark, most recently at 52.6.

Source: Haver Analytics

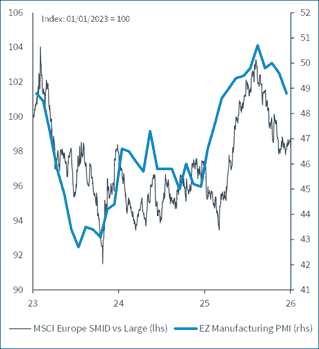

SMIDs have historically performed stronger than large companies when PMIs are rising and vice versa.

Source: Kepler Cheuvreux

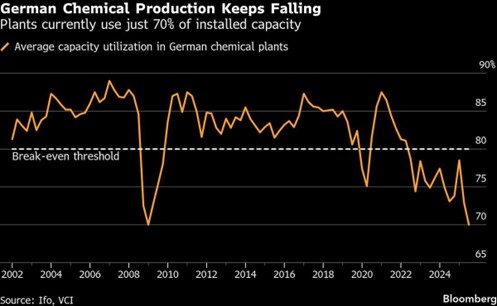

Things are looking tough in German industrial activity, to say the least.

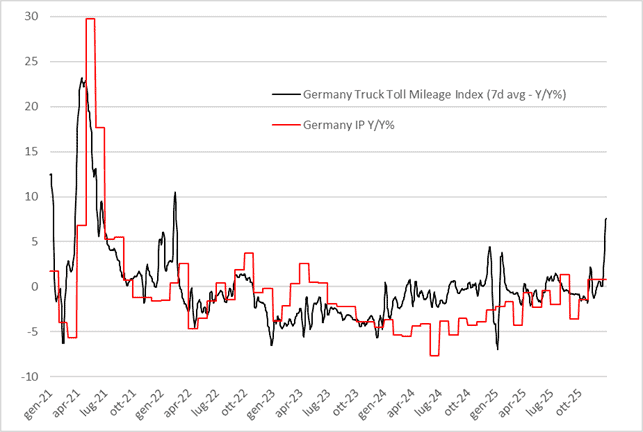

For those of you who are depressed about Germany having three years of zero growth, we would like to convey that the DAX has risen by 76% during the same period. This is significantly better than the S&P500, which rose by 63% during the same period, and the OMX30, which rose by 46%, all measured in euros. It cannot be said enough; the underlying economy is not a mirror image of the stock market.

It's darkest before the sun rises, right? In December, a German index was published that shows the miles driven by German trucks on a rolling 7-day basis. Is it a trend break or a false start?

Source: X

During the holidays, we also received encouraging data showing that European housing construction took a significant step up in November with +5.8% in construction starts and +14.4% in permits to start construction.

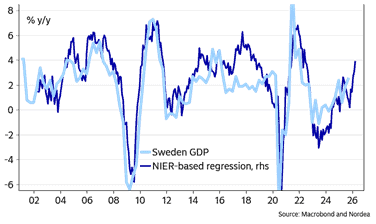

Below is a potpourri of images from Nordea's barometer-based GDP model, which has risen sharply in recent months and in the image below indicates higher GDP growth in 2026 for Sweden than what the market expects. If this is true, it will most likely benefit smaller companies in particular and that, combined with five years of mediocre returns, could lead to several years of excess returns for smaller companies.

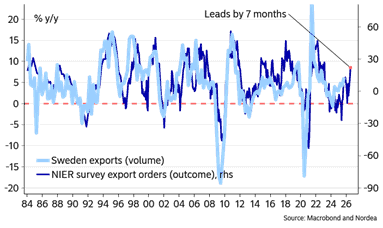

The export order intake, which is so important for Sweden, now looks to be picking up.

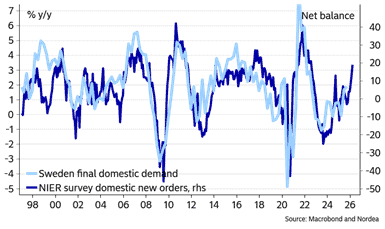

Domestic market orders (especially important for smaller companies) are even stronger than export orders, which indicates strong domestic demand next year.

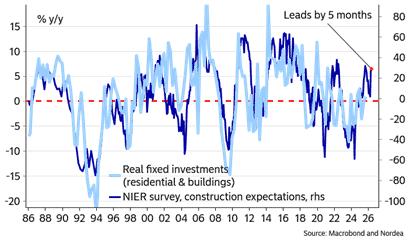

Construction companies continue to indicate better demand for 2026, which is a heavy contributor to Swedish GDP and has been a real drag for several years.

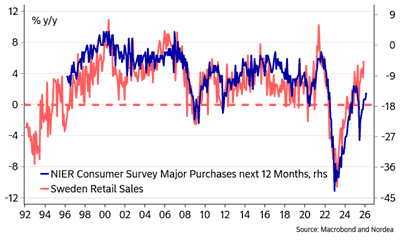

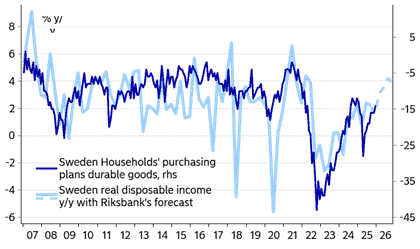

Households have started to consume.

Driven by sharply increased disposable income.

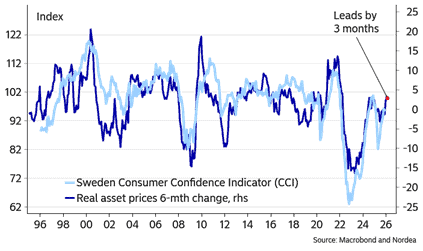

Rising house prices are driving consumer confidence.

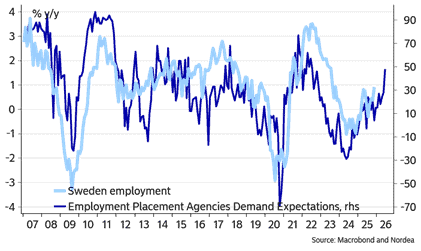

There has been rapid and clear improvement in short-term agency staff demand, which is a good indicator that companies are starting to consider hiring more personnel.

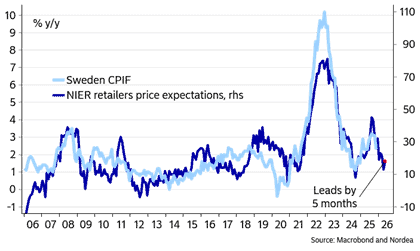

Retailers have been right so far about falling prices and that looks set to continue.

Over the holidays, Per Jansson, Deputy Governor of the Riksbank (Swedish Central Bank), was out and commented that he sees increased risks of inflation becoming too low. “A number of factors that will exert significant downward pressure on price increases.” Got it!

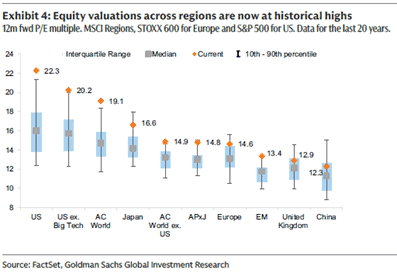

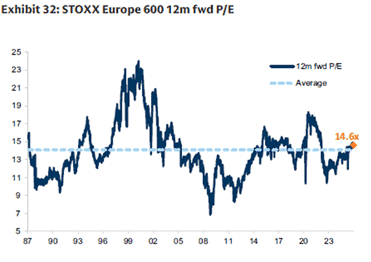

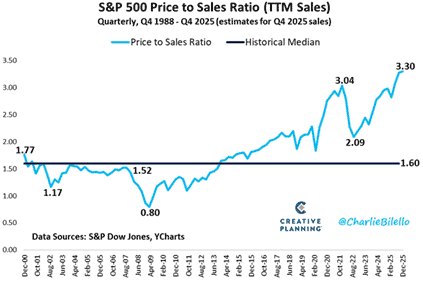

Summary of current valuations; there are several regions that stand out with historically high multiples.

This does not apply to Europe, which is in line with its historical average.

Source: Goldman Sachs

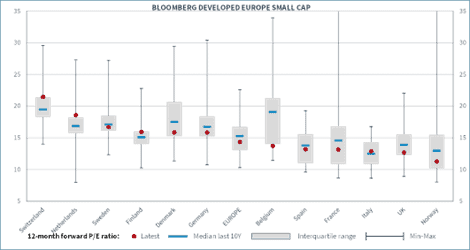

Current P/E ratio for European SMIDs, the 10-year average and median.

Source: Bloomberg Mid & Small cap indicies, Kepler Cheuvreux

Below are the valuations of European SMIDs and large companies 2006–2026.

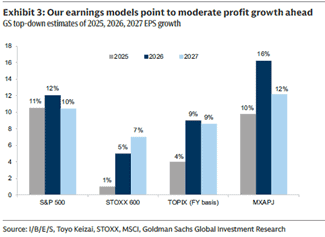

Profits look set to grow nicely in 2026 if estimates are met.

Expected profits for SMIDs are rising significantly more than for large companies. This is not yet reflected in share prices.

Source: Kepler Cheuvreux

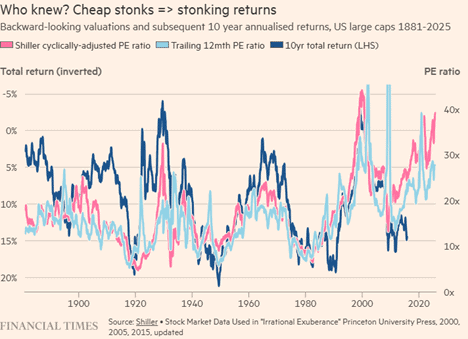

If we were to try to summarize all the above, it is probably not a wild guess to believe that Europe's stock markets will continue to benefit from inflows from international investors. An erratic American president, to say the least, has made most people realize that the overexposure that has been had for many years (which has been right) to the American stock market probably needs to be adjusted in line with the increased political risk that also spills over into the American dollar. Furthermore, hoping for continued multiple expansion feels optimistic.

Well aware that we said the same thing last year and that we are biased, the conditions for smaller European companies this year are good, and if we can soon start to see an acceleration of growth and profits, very good. With record low valuations in relation to larger companies at such extreme levels as today, the conditions are excellent for several years of excess returns for smaller companies.

We note that despite several stock markets being close to or around record levels, small cap funds have had significant outflows last year, not least during the last quarter of the year where we, on several occasions, saw a very clear pattern. We cannot remember experiencing this before. If it can only slow down or even turn around to inflows, it would be marvellous.

Valuations for smaller companies in the short term are rarely a driver, but in the long term they play a larger role. The combination of record low valuations relative to larger companies, an expected acceleration in growth, continued expected interest rate cuts from the world's central banks, huge stimulus packages, likely continued inflows to the European stock market AND record high valuations of US companies, is an arrangement we would blindly accept any day of the week.

When the party is on, it can be difficult to keep track of how many gin & tonics are being consumed (so I've read), but there will also be a sobering process. One must have very strong faith in the US and US companies to believe in continued stock market euphoria. Valuations play a big role in the long term and that is why we are optimistic about European small companies over the coming years.

Finally, I would like to extend a warm thank you to my team, Cecilia, Fredrik and Gustav, who have put up with me for another year and who have contributed in a remarkable way through thick and thin. Thank you!

Most importantly, thank you to you, the shareholders, who make all of this possible for us. Many thanks!

With the best wishes for a successful and healthy 2026.

Mikael & Team

Malmö, January 9th, 2026

IMPORTANT INFORMATION. This is a marketing communication. Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested. Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.