Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class' return. The information below regarding returns therefore differs from the returns in other share classes.

Before making any final investment decisions, please read the prospectus, its Annual Report, and the KID of the relevant Sub-Fund here

This material is marketing communication

Monthly Newsletter Coeli European – February 2024

FEBRUARY PERFORMANCE

The fund’s value decreased by 0.8% in February (share class I SEK), while the benchmark increased by 0.5%. Since the change of the fund’s strategy at the beginning of September this year, the fund’s value has increased by 9.3% compared to a decrease of the benchmark by 0.4%. Both measured in SEK.

* Adjusted for spin-off of Rejuveron

** Includes September 1 (strategy change to active long-only as of September 4, 2023). Please Note: On the 4th of September 2023, the strategy of the fund officially changed from a European long biased equity long/short fund to a European active long only fund. Simultaneously, the name changed from Coeli Absolute European Equity (AEE) to Coeli European.

EQUITY MARKETS / MACRO ENVIRONMENT

Another intensive reporting month is over, and we are, overall, satisfied with the results from our companies. The fund fell by 0.8% compared to the benchmark index, which rose by 0.5%. The biggest positive contributors in February were Biotage, Cargotec, Lindab, LVMH and Diploma, which rose by 18, 19, 9, 9 and 6% respectively. The biggest negative contributor was Rugvista which, after five strong quarters, released a report that was below expectations. Adjusted for one-off effects, the report was more or less in line with expectations. A decline of 13% was, in our opinion, an overreaction. More about that later in the company section. Our Swedish property shares also had a weak month with Corem falling 12% and SLP falling 5%.

February's big themes were, firstly, a strong inflation figure on February 13th, which led to the worst trading day since October last year. At the end of the week, however, several of the world's stock markets had closed at new highs. Impressive to say the least. On the last day of the month, the January figure for the Fed's favourite measure (the consumption deflator, PCE) was published, which was exactly in line with expectations and a certain relief was immediately visible in the form of rising share prices. The inflation rate in the US is now the lowest since the beginning of 2021!

Source: X

The second theme was rising interest rates and a much more conservative estimate of when and how many rate cuts there will be this year. For example, the US 10-year interest rate rose from 3.9% at the beginning of the month to around 4.3%. Despite that, we got to experience the S&P500 above the 5000 level for the first time. Also, in Germany and France, the index rose in February by 4.9 and 3.9%, respectively, to new highs.

Our area of focus, small companies, did not experience the same euphoria and the asset class was overtaken by the large broad indices. It is very unusual for the S&P500 to reach an all-time high at the same time as the Russell 2000 is in a bear market state (same development in Europe). The last time it happened was in 1998 and then the development for the next 12 months was as below.

Source: Goldman Sachs

Despite recent rising interest rates, we are somewhat surprised that small caps did not have a better start to the year (even though November and December were very strong). We have received several positive economic news in recent months, which typically tends to favour small companies more than large companies. They are less diversified and thus more sensitive to economic developments than larger companies. We maintain our view that the asset class is likely to have a good 2024, with falling interest rates becoming a strong driver.

The third talking point was of course Nvidia, which is the world's best stock so far if you are looking for AI exposure. The company delivered on extremely high expectations and the figures that were published are breathtaking. In 10 years, the market capitalization has risen 220x and is now around USD 2000 billion. To put things into perspective, that's more than the GDP of Spain with 50 million inhabitants. No one has ever seen a similar development and Nvidia's report contributed to continued positive sentiment on the world's stock markets.

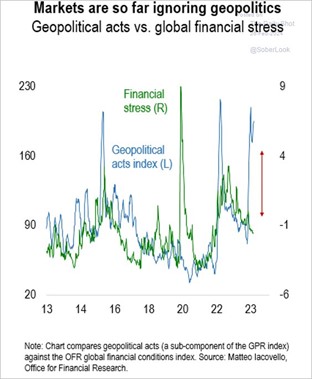

The financial stress in the systems is relatively low. Geopolitically, however, things are on red alert in many places. The markets are ignoring the development so far, which has been correct. So far, we have not seen any major spillover effects, but the human suffering is unbearable in many places.

The fourth talking point during the month was Donald Trump discussing NATO on a Saturday in Conway, South Carolina. He recounted a conversation he had with “a president of a great country”. The president of the great country had asked Trump if the US would protect them if, hypothetically, they had not paid NATO. The answer from Trump was: "No, I would not protect you. In fact, I would encourage them (Russia) to do whatever the hell they want”. You can say a lot about Donald Trump, but at least he is clear. The statement sent European defence stocks soaring for the rest of the month.

Source: CNBC

Nikki Haley, Donald Trump's main opponent to become the Republican presidential nominee, tweeted the following clip about when Trump discussed Putin a few years ago on Fox news. https://twitter.com/NikkiHaley/status/1759024750561464802

The standings are even between Republicans and Democrats, and it will be an interesting autumn. For an average European it is difficult to understand that a man who supported the storming of Congress and has numerous charges against him, can be re-elected.

Source: Goldman Sachs

Paul Krugman, economist, and debater who won the Nobel Prize in Economics in 2008, is also an influential New York Times columnist. Krugman notes that Trump's desperation to delay payment of the $454 million he was ordered to pay for deliberately exaggerating his financial position shows that he, de facto, lied. He doesn't have the money. Trump has started a crowdfunding to help finance the fine. At the end of February, the collection had reached 0.3% of the amount. Keep fighting!

The great threat to the European economy last winter is a thing of the past. Low European gas prices are also putting pressure on Swedish electricity prices, which during some days in February were almost down to zero. Very pleasing.

Source: Financial Times, X

Low energy prices contribute to continued downward pressure on inflation. In its recently published forecast, the National Debt Office has adjusted down the expected inflation rate (KPIF, excluding interest rate changes) to 1.7% for both 2024 and 2025. A whole percentage point lower than in the previous forecast!

Source: SCB, Riksgälden

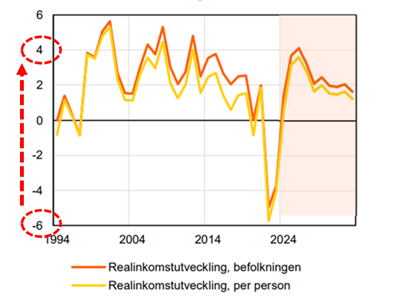

Even SBAB believes that ordinary CPI will drop to close to zero next year. SBAB also expects that households' real disposable income will soar from minus 6% to plus 4%. It is a huge improvement and contributes strongly to the expectation that Sweden's GDP growth will be at the top in Europe next year and also when compared to the US (3% in Sweden compared to current forecasts of 1.3% for the Eurozone and 1.7% for the US). It was a long time ago since the prospects for a strengthened krone looked so good.

Source: SBAB

Recession as a search term on Google has crashed and optimism is beginning to flourish.

Source: X

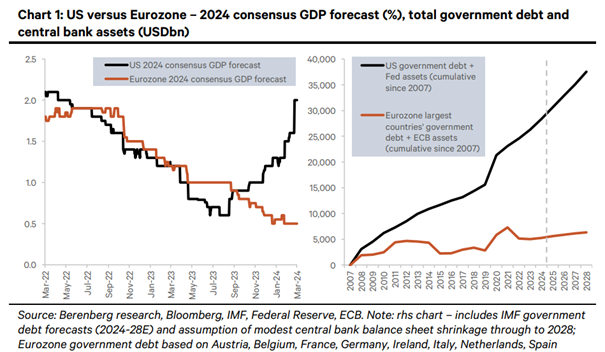

Revisions for the American economy have been brutal the last six months. Europe is lagging as usual, but we are probably close to a turnaround here as well. As can be seen in the picture below, the budget discipline has been mediocre for the last 15 years in the US. For how long can this go on?

PORTFOLIO COMPANIES

Biotage

Biotage was one of the fund's great joys during February. Ahead of the Q4 report, which was released during the month we had noted two things that made us believe in a good delivery:

1) In the last report (Q3) inventories had increased significantly, suggesting that the next quarter could be good.

2) The management had made valiant attempts to convince the analysts that the company's latest acquisition, Astrea, has a strong business that fluctuates a lot between quarters. Maybe to the positive in Q4? The feeling was that management was very confident with Astrea's development.

3) Astrea clearly has longer sales cycles than the rest of Biotage, which meant that management should have good visibility of what is delivered and when.

We thought these ingredients combined stirred up a great cocktail. And so, it turned out to be, with an adjusted EBITDA result that was around 60% better than expected – exceptional! The big explanation was precisely Astrea, whose sales were 50% better than expected.

The stock had been strong before the report after sector colleagues Sartorius and Lonza delivered better than expected in January. The stock nevertheless rose 14% on the day of the report and another 10% the day after. Biotage is one of the few platform companies in its niche that remains listed in the Nordics. We wouldn't be surprised if some major industrial players are eyeing up Biotage.

Below is the course development over the past year. We increased our position all the way down last autumn and going into the report it was the fund's largest position. Four months after the lowest level in October, the share has risen with more than 100%.

Source: Bloomberg

Bonesupport

Bonesupport's stock has been a great performer and has risen 129% in one year. The stock had thus developed very strongly before the report. Adjusted for currency and non-recurring costs, Bonesupport delivered results in line with expectations, having beaten estimates five quarters in a row. This was interpreted as a sign of weakness by the market and the share fell approximately 5% on the day of the report and as much as 9% the following day. We took advantage of the turbulence and bought more shares.

We have not made any changes to our estimates following the report. Carnegie's analysts were with Bonesupport at the AAOS (American Academy of Orthopedic Surgeons) in San Francisco and felt that the interest in Bonesupport's products is very high in the US. Carnegie also released a major update on penetration and the market in the US and raised the target price from SEK 235 to SEK 285.

SLP

The logistic property company SLP released a report in February where the management result was 4% better than expected. Rental income increased 42% compared to last year and we believe SLP can continue to make opportunistic acquisitions in 2024 with its strong balance sheet.

SLP trades at a premium of 3% to our estimated net asset value at the end of 2024, with an unchanged yield requirement. It's way too cheap for a real estate company with a high yield requirement (5.9%) and very strong growth. Should the yield requirement not fall in 2024, it will most likely do so in 2025 and thus drive the NAV development.

Cargotec

Cargotec submitted a report on the first day of the month. The company's operating profit was 9% worse than the estimate. Even more important though was that order intake was 5% better than expected, which the market took note of. Subsequently, order intake grew by 11%, which indicates that the development may have bottomed out at this point. The share was rewarded with an increase on the report day of approximately 6%.

Despite the strong rally over the past month, the stock is still cheap at around 9x earnings. The company also has a strong balance sheet and net cash. Work on dividing Cargotec into several companies continues and it is likely that the Kalmar subsidiary will be listed on the stock exchange on the first of July this year if no other player buys the company.

Corem

Corem announced a result in line with our and the market's expectations. Indexed rental income has compensated a lot for increased financing costs. The company's average interest expense had actually fallen during the quarter, which is partly explained by the fact that some expensive bonds were bought back. Net lettings were negative in the quarter with -7 million, but for the full year net lettings were +83 million. During the year, properties were sold for 14.6 billion with a profit effect of 626 million including dissolved tax.

In total, Corem has made a downward revision of its property values by 11% during the year and by 14% since the highest levels in spring 2022. The average yield requirement used in the valuation at the end of the year was 5.8%, which is to be compared with 4.9% in Q1 2022 This has pushed the net asset value to SEK 17.6 at the end of the year (to be compared with the share price around SEK 9.50). The share was under strange pressure in connection with the presentation of the results and this may be because investors perceived a reduced dividend from SEK 0.40 to SEK 0.10 negatively. We have pushed for a scrapped dividend as we think it is much better for the company to buy back expensive debt as soon as possible. We took advantage of the price pressure and increased our position. So did principal owner Rutger Arnhult, who on three occasions announced the purchase of shares for just over 4 million.

Corem is one of the real estate companies that will benefit the most when interest rates retract. Partly in terms of reduced interest costs and thus an increasing cash flow and partly in terms of a falling yield requirement that begins to build up the net asset value again.

Campari

In November, after the last quarterly report, we began cautiously buying into Campari. The company is a shining star in the beverage industry with a premium brand portfolio that drives growth to levels well above that of the industry. The most important drink, Aperol (24% of total sales) had an organic growth of 23.1% in 2023. The second most important drink is Campari with 10.7% in organic growth (11% of total sales). Since 2019, the group has organically grown by as much as 60%, but at the same time the operating margin has fallen slightly. The reasons for this are rising agave prices (raw material for tequila), generally rising costs due to inflation, and also increased depreciation, when production capacity was increased to meet the high demand.

The quarterly result was almost 30% better than expected and the share rose 5-6% initially. It later turned out that one reason for the strong result was that marketing costs were reduced, and adjusted for that, the result was in line with expectations. The next day, the stock fell a few percent. With a very high probability, margins will improve significantly this year while sales growth continues. It is falling agave prices as well as lower glass prices that will come through with full force in the second half of this year. We are not yet fully invested but think today's valuation of 22x and 20x respectively in P/E numbers for 2025-2026e is attractive given all the quality Campari possesses.

Euronext

Euronext, which owns several European exchanges, came out with another solid report in February. The result was somewhat better than analysts had expected. Although the stock has risen more than 20 percentage points better than the index since the initial purchase, the company is still valued below its historical average on forward-looking earnings. This is even though the share of revenue that comes from non-volume-related revenue (stock trading, etc.) has risen to 58% in 2023, compared to 44% in 2018. This has made the business more predictable, which we believe should be valued at a premium.

London Stock Exchange

Another exchange that we own is the London Stock Exchange. However, the income is highly diversified and only a very small part of the income comes from the trading of shares in London. Most of the company's revenue is instead generated from various types of data operations – among other things, the company sells real-time prices, risk data and indices (FTSE Russell). As in the case of Euronext, the moats are high and the earnings predictable. During the month, figures for the full year 2023 were reported which were in line with expectations.

CVS Group

The veterinary company once again reported results that were in line with expectations. However, management's outlook was cautious, citing inflation and weak macro trends. That, combined with the fact that there is an ongoing case with the CMA (Competition and Markets Authority) that keeps the stock market on a leash, caused the price to fall 13% in February. The influence on the fund's development for the month was clearly limited because we have a small position in the company.

Rugvista

The Rugvista share had a weak month with a decline of -13%. In February the company's Q4 report was released which had better organic sales than we expected, but with an EBIT result that was 23% worse than what the analysts had expected. If we take the liberty of adjusting for a negative currency effect and what can be considered non-recurring costs, we; however, arrive at an operating result quite well in line with the estimates. The most important thing for us is that sales develop positively while we see leverage in the new platform rollout, and we think we saw that in the Q4 report. The stock is valued on our estimates at a low 10x and 9x EBIT for 2024e and 2025e respectively.

Surgical Science

The second disappointment of the month came from Surgical Science. The company's results came in strongly during the advance predictions. Even adjusted for a relatively large currency loss, the result was weak. The reason is particularly attributable to weak sales within the Educational Products business leg. Having said that, the most important thing is that the company's OEM leg is developing strongly – in 2023 the company managed to grow license revenues within this leg by 50%. The management affirms that they continue to strongly believe in the company's financial goals for 2026 - should these be achieved, there is great potential for the share.

SUMMARY

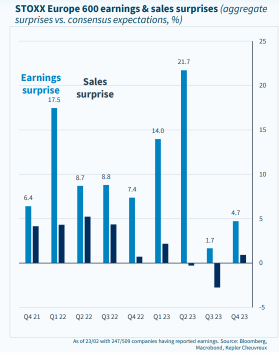

The reporting season is now largely over, and the conclusion is that the companies have once again delivered good results. In Europe, it is primarily the profits that have surprised positively, while turnover growth has been somewhat more modest. Below illustrates the deviations for the companies within the broad STOXX 600 index.

Despite earnings beating expectations, 2024e EPS estimates in Europe have fallen slightly in recent weeks. Analysts have either been too optimistic and/or the companies have been cautious with their outlook at the beginning of the year. This contrasts with the United States, where estimates have risen slightly. However, both geographies offered rising share prices in February except for the self-torturer Great Britain, which continues to develop weakly. Various studies have concluded that Brexit has so far cost the UK £140 billion a year, which equates to a total of 6% of GDP. Since the Brexit election, the FTSE100 has risen, measured in euros, by a mediocre 13%...Well done.

Source: UBS

At the moment there is an unusual amount to be happy about when it comes to economic development. Inflation is falling, interest rates are falling, real wages are rising, bottlenecks have disappeared, European valuations are low, expectations are relatively low, and it currently looks like economies are soft landing. It is no coincidence that many stock markets trade at record highs. Below are some flash headlines from the end of the month from two Fed members.

*BARKIN: INFLATION IS COMING DOWN, SHOULD BE CHEERING 2.4%

*GOOLSBEE: WOULDN'T BE SURPRISED IF JANUARY INFLATION WAS NOISE

*FED'S GOALSBEE: I BELIEVE FED FUNDS RATE IS QUITE RESTRICTIVE

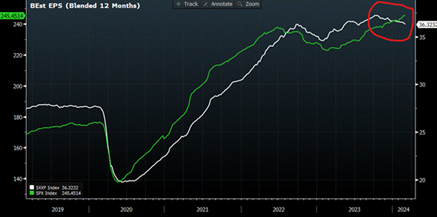

The image below on the left shows a surprise index that contains a number of economic sub-components. Europe is on the move from low levels. A major warning should be issued to the ECB, that if they continue to build on their weak track record, they will cut rates too late and unnecessarily create an extension of the downturn. Our view of the ECB's strategy is that they are sitting and waiting to see what the Fed will do. One of the problems with the uninspiring strategy is that the US and the Eurozone are in completely different economic phases. Following European inflation data on Friday, March 1, which was slightly higher than expected, the ECB is now expected to make its first interest rate cut in June, cutting rates by a total of 0.92% this year.

The pictures below also explain why we are somewhat surprised that small caps had a somewhat mediocre start to the stock market year. This also applies to American small caps.

The answer (we think) to why small caps are lagging in the lead-up to 2024, is the recoil we've had with rising interest rates. This asset class, as we all know and have experienced, dislikes rising interest rates. But it seems reasonable to believe that we will see the opposite effect when interest rates gradually fall during the year.

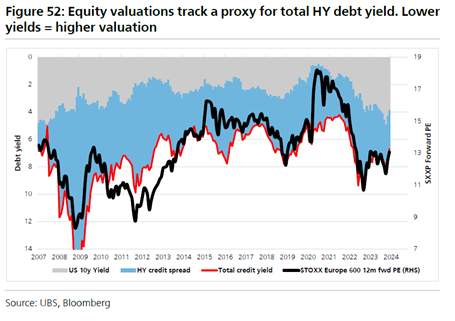

The image below shows, just like the image above, that it is still the interest rate that determines valuations in Europe. Companies' earnings are of course important, but it was a falling interest rate that largely drove share prices upwards during the last quarter of last year. The correlation between P/E ratios, inverted interest rates and credit spreads is close to 1. With high probability, the correlation will persist as interest rates fall, thus driving up multiples and valuations.

We are at slightly overheated levels. Below is the Goldman Sachs sentiment indicator for the US stock market.

Source: Goldman Sachs

If history is to repeat itself again, prices will go downhill since The Economist has published the front page below.

Source: The Economist

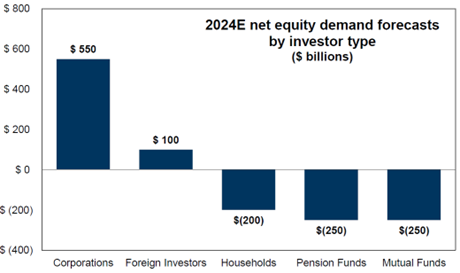

In the US, it is the companies that are expected to be the biggest net buyers of US stocks this year. An observation that the undersigned made during this year's first reporting season is that there have probably never before been so many and large buyback programs announced by European companies. That's a big change in a relatively short period of time and for us it signals optimism, strength in balance sheets and what we hope is frustration at overall low valuations. We applaud the development and a step in the right direction to create shareholder value with our (your) capital.

Source: Goldman Sachs

The last month has seen gains in several places and Europe is asserting itself well. That Europe is undervalued is not news. But the combination of the US being at high levels, at the same time as European companies have announced many new buyback programs, is a catalyst that attracts new and welcome capital to the market. The picture also clearly shows that investors believe in a turnaround in the sluggish Chinese economy.

Source: Goldman Sachs

Another way to illustrate low values in Europe.

In summary, the economic outlook in Europe, after two difficult years, is better than it has been for a long time and after the summer there may be a visible improvement all around us, not least in Sweden. That combined with low expectations, with a large element of scepticism, is an unusually attractive combination.

After an intense February, we are now entering a period where we can spend more of our time on analysis of existing and potentially new companies.

Thank you for your interest!

Mikael & Co

Malmö March 6th, 2024