Monthly Newsletter Coeli European – February 2025

This material is marketing communication.

Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class’ return. The information below regarding returns therefore differs from the returns in other share classes.

Before making any final investment decisions, please read the prospectus, its Annual Report, and the KID of the relevant Sub-Fund here.

February Performance

The fund’s value decreased by 2.7% in February (share class I SEK), while the benchmark decreased by 1.3%. Since the change of the fund’s strategy at the beginning of September, 2023, the fund’s value has increased by 19.4% compared to an increase of the benchmark by 13.6%.

Source: Coeli European

* Adjusted for spin-off of Rejuveron

** Includes September 1 (strategy change to long-only implemented September 4 2023)

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

Equity Markets / Macro Enviroment

The frequency and magnitude of political and economic news over the past month have been at peak levels, reaching a crescendo on the evening of Friday, February 28th, with Zelensky's visit to the White House. There, he endured a particularly unseemly reception, and the new administration showed its true colours to the entire world. On the economic front, the reporting season is now largely over, and the aggregate outcome was clearly satisfactory, with European companies continuing to perform well.

The chaos created when President Trump, with a high tone and at a furious pace, breaks alliances and structures that have existed for 80 years is particularly worrying. After the latest statements, there is no doubt that the USA no longer has the same role in world politics. Martin Wolf, perhaps Europe's most influential journalist and active at the Financial Times, wrote an article titled: "The US is now the enemy of the west." That article was published before Trump and his eager vice president and bully JD Vance, with all desired clarity, showed the whole world that the USA is now on Putin's side. A few hours after Zelensky was thrown out of the White House, the American embassy in Stockholm took down its Ukraine banner. How did we end up here?

The outcome of the German election delivered a more hopeful glimpse of the future. The political situation is beginning to stabilize somewhat, although there are major challenges. The pressure on those in power to start stimulating the economy is massive.

The broad European indices continue to develop strongly, with the German DAX continuing to lead. The smaller companies in Europe are performing about half as well so far, and this is because (according to us), when capital flows into Europe, it needs to be put to work as quickly as possible, and it is the most liquid companies that are first on the list. If this thesis is correct, the smaller companies will catch up soon.

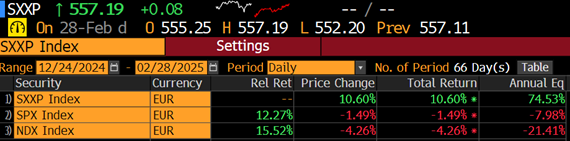

The image below shows the YTD development for the major stock markets. The column second from the right shows the development this year measured in local currency. The far-right column is measured in SEK. In February, the SXXP600 rose by 3.3%, while the S&P500 fell by 1.2%, both measured in euros.

Source: Bloomberg

The fund declined by 2.7% in February compared to our benchmark, which fell by 1.3%. One factor that clearly affected the fund's return in February (in the SEK class) was the strong performance of the krona, which strengthened by just under three percent in February, making it one of the world's best-performing currencies this year. This is very pleasing, although the fund's return would have been nearly three percent better with an unchanged SEK exchange rate. A stronger krona reflects, among other things, an increasing risk appetite, which is likely to benefit the fund's performance over time.

The top contributors in February were Scandic Hotel, Bonesupport, and Euronext. The worst were Biotage, 4Imprint, and Cargotec. More about that in the portfolio companies section.

If this continues, there might very well be a trip to Copenhagen this summer! The image shows EUR/SEK over the past year.

Source: Bloomberg

As we have written about for several months, the hysteria and positioning towards American stocks have been at an absolute record level, which has also been reflected in record-high valuations. In November, we were slightly envious of the very strong performance of the American stock markets after Donald Trump won the American election, while the market moved sideways in Europe. All of this has now reversed.

With the same high speed as the new American administration is rampaging around, it has quickly become advantage Europe, where since year-end, it has had the strongest capital inflow in 25 years (!), and Europe as an aggregate has now performed stronger than the USA since Donald Trump became president. That must sting for him.

Since Christmas Eve, the SXXP600 has performed 12% stronger than the S&P500 and nearly 16% better than Nasdaq, all measured in the same currency (see image below). It is probably a coincidence, but unlike the previous term, Trump has been silent regarding the stock market. JP Morgan notes that during his previous term, he posted 156 positive comments about the stock market. So far, we are at one. The last time Europe performed stronger than the USA in such a short time was in December 2022 and before that in April 2001, so even the stock markets are offering a historic development.

Source: Bloomberg

Why did we end up here and what has happened? Until a few weeks ago, Trump's beloved tariffs were considered to drive inflation, which contributed to high American interest rates and slowed the development of the stock markets. Now the narrative has changed to tariffs being harmful to the American economy, and the latest economic data published did not help to calm investors.

American retail data published a week ago showed the weakest development in two years, consumer confidence has dropped more than in four years, and optimism among smaller companies may have reached its peak. Citibank's economic surprise index has recently shown misses in the USA while Europe surprises positively. Bitcoin, which is clearly a "Trump trade," has dropped approximately 25% in a short time.

Another asset class that is part of the "Trump trade" but has performed well is the Russian ruble, which has strengthened by about 30% this year. Well done...

Source: X

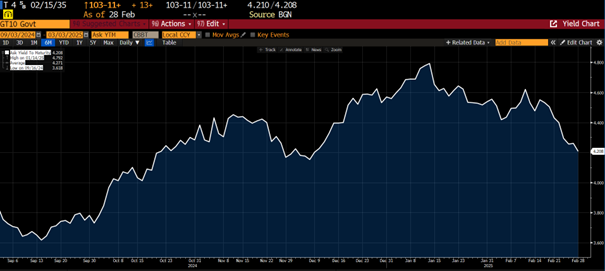

The above has also led to significant downward pressure on the American 10-year-old, clearly indicating that investors are suddenly more concerned about growth than inflation. From 4.8 to 4.2% in a month's time, see image below. One question from the writer is when (and if) Europe and especially China will finally say no thanks to American government bonds. Given everything else happening in the world, that would not be unforeseen.

Source: Bloomberg

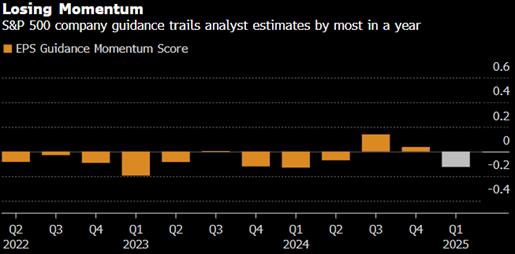

89% of respondents in Bank of America's global fund manager survey believe that American stocks are overvalued. The last time this happened was in April 2001. At the same time, as seen in the image below, the guidance from American companies has been weak during the current reporting period. The combination of the two is rarely a good combination. All this together has led to large outflows from the USA into Europe.

Source: Bloomberg

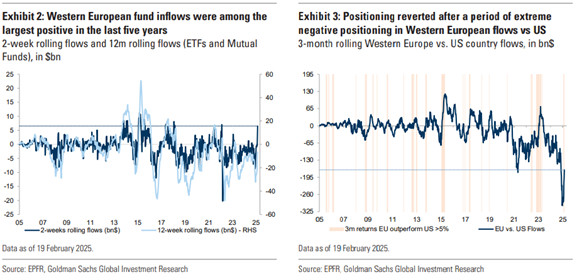

The below shoes two-week rolling inflow to Europe on the left and positioning on the right.

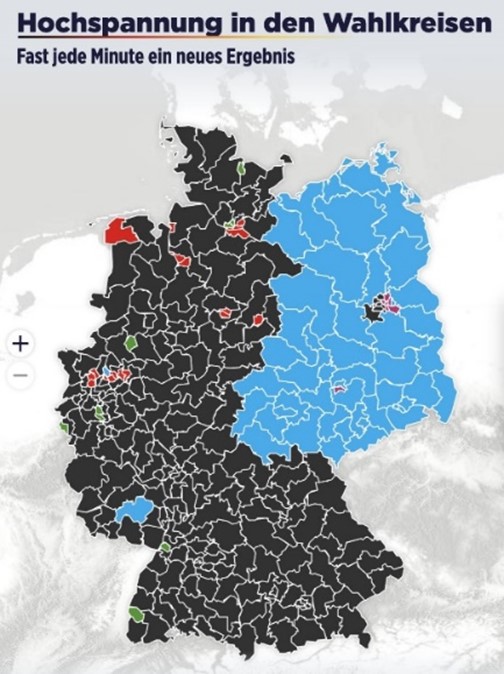

At the end of February, Germany held its election where CDU/CSU, led by Friedrich Merz, won with 28.5%, and AfD received a full 20.8%, which was twice as many votes as in the previous election. Olaf Scholz and his SPD, as expected, had a disastrous election and received a modest 16.4%. This often happens when one pursues a disastrous political policy. It was their worst election since 1890.

There was a certain relief around Europe afterwards, as it could have been worse. Elon Musk's dirty involvement and propaganda for AfD did not seem to have much effect. It is quite clear that Germany, despite the fall of the Berlin Wall in 1989, is still a divided country. AfD in blue. One can hope that Merz shows stronger leadership than Scholz, as AfD's strong development clearly shows that people are worried and afraid for the future. If that does not change, it will turn out like it has in the USA with an authoritarian leader with somewhat vague moral concepts.

Source: Holger Zschaepitz

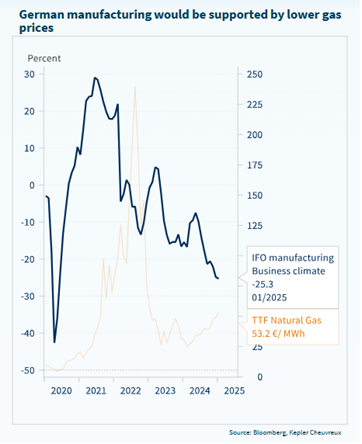

There are many of us who now hope and believe that the world's best engineering workshop will finally get some speed under its wheels. Several extremely serious mistakes have been made, not least in energy policy, but it is time to find solutions, stimulate the economy and rebound. Germany, which is Europe's largest economy with 24% of the EU's total GDP, needs to lift itself up.

The energy policy has been a disaster. Below is the activity in German industry and gas prices.

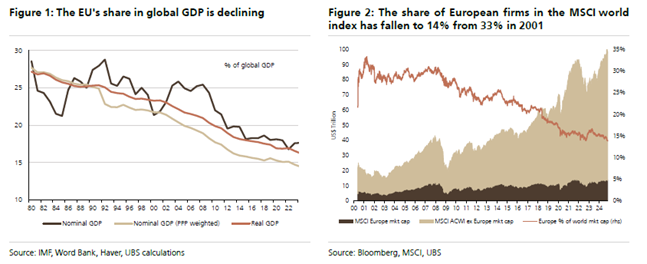

The images below show Europe's sharply declining stature in the world. It's time to roll up the sleeves now and change that! Admittedly driven by geopolitics mainly, we are currently witnessing the largest gathering of power among Europe's leaders since the war and this could be a catalyst for focus to finally be on growth, less regulation and strong leadership.

Who is surprised?

The most bizarre political video ever? "What's next for Gaza", watch the video here.

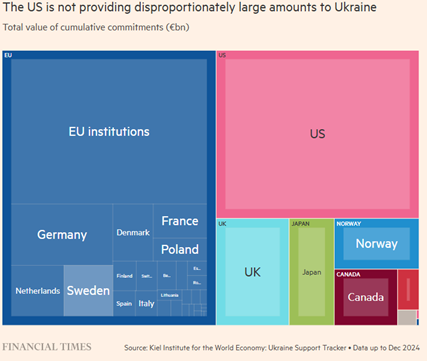

No, the US has not paid a disproportionate amount to Ukraine.

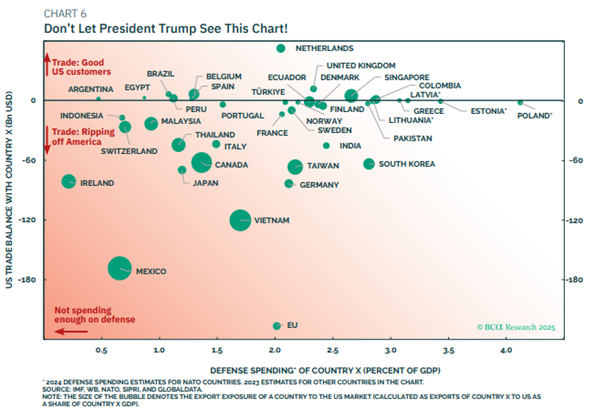

"Evil and good countries" and each country's defence expenditure.

Source: BCA Research

“Zelensky shouldn’t have started the war with Russia.”

Source: X

Portfolio companies

Euronext

The exchange operator has indulged its investors with positive reports for a long time and the report for the fourth quarter of 2024 was no exception. Operating profit (at EBITDA level) was 1–2% ahead of estimates, driven by better-than-expected revenues. The company also guided for its costs for 2025, which are expected to be slightly higher than analysts had estimated. Despite this, the stock rose, presumably due to the strong sales.

The business is currently benefiting from volatile equity markets, which typically creates larger trading volumes. From that point of view, Trump's frequent and wild outbursts are positive for Euronext. The company has been a portfolio stalwart since late summer 2023 and has risen approximately 80% since we initiated our position. In February, the share rose by 8% resulting in 12% for the whole year. Below Euronext price development since August 2023.

Sampo

We have a positive view of the future of the Nordic insurance market and against that backdrop we have owned Finnish Sampo for some time. We are currently seeing how insurance premiums continue to rise while general inflation is falling, which should be positive for Sampo. See the image below where we tried to weight insurance inflation in the Nordics based on population and compared to general inflation. Recently, the rate of increase in inflation for car repair has also fallen from high levels, which should be positive for future profitability.

Source: Coeli European

Although the market capitalization is larger than what we normally invest in, we think Sampo fits into our portfolio. The streamlining of the business in recent years has made the company more attractive because it is now a purely Nordic insurance company. The Nordic insurance market is characterized by stable and high profitability with a few large and disciplined players.

In February, Sampo released a report that was about 9% better than estimates. The stock rose 6% in February and has thus risen 7% for the full year.

Van Lanschot Kempen

We recently initiated a small position in the Dutch wealth management company Van Lanschot Kempen. The company is several hundred years old and previously had more extensive banking business. Today, the focus is instead on wealth management for wealthy private clients and foundations. The beauty of the business model is that in the long term the managed capital should rise in tandem with the stock market, which together with net inflows gives nice profit growth.

In recent years, the company has been successful in improving its customer satisfaction. The direct consequence of that is greater net inflows. Over the past five years, average inflows have been around 6% into the wealth management business. This can be compared with 1% during the previous five-year period.

Source: Coeli European

We believe that over time, Van Lanschot should be able to grow its managed capital by at least 6–7% per year, conservatively calculated. At such levels, profits should grow a bit faster than thanks to economies of scale. If you add an (ordinary) dividend that gives around 6-7% in dividend yield to that profit growth, you are on pretty good track to approximately 15% return per year (given a stable valuation multiple).

In February, Van Lanschot released a report that was slightly below expectations, mainly due to a lower-than-expected profit in Van Lanschot's investment banking division. The investment banking division is small, volatile in nature, and not highly valued by us or the market. If Van Lanschot had missed our estimates based on the main Wealth Management business, we would have been more concerned. We took advantage of the weakness that occurred on the report by buying more shares.

The share fell 4% during the month and as of the end of February had thus risen 5% for the entire year. At the time of writing, it has just been announced that the major Dutch bank, ING, has bought a large position in Van Lanschot stock. Given regulatory approval, ING will own roughly 20% of the company and the market will now consider a complete takeover. At the time of writing, the stock is up by five percent on the announcement.

Bureau Veritas

For some time now, we have held a mid-sized position in French Bureau Veritas, which offers certification, inspection and testing in a range of industries. For example, it could be helping to inspect marine platforms to ensure they meet safety requirements or calculating and reporting carbon dioxide emissions for a company's annual report. The company has had great success recently with high single-digit growth on average in recent years.

The company submitted a report in February that beat expectations by 1-2%. Despite this, the share has fallen 7% since the report. We believe that the main reasons for this are 1) that the market got used to even bigger positive surprises against expectations than what was disclosed in the fourth quarter and 2) the lack of announcements about buybacks in connection with the financial statements. Bureau Veritas also benefits from global trade and constant headlines about tariffs are not helpful from that perspective. For the year, the Bureau Veritas share has fallen by 1%.

Scandic

Scandic released a report for the fourth quarter that was about 6% better than expected in terms of operating profit. During the afternoon, Scandic also held its first capital market day in five years. The message was clear to the market: Focus is on growing the business and distribute a lot of money to shareholders. The company plans to open 10,000 new rooms over the next five years. It can be compared with the 55,000 hotel rooms you have today. They also expect "RevPar" growth (revenue per room) in the Nordics driven by increased occupancy and higher prices.

On top of that, management proposed to distribute SEK 570 million and launch a new buyback program of approximately SEK 500 million. In total, almost SEK 2 billion is expected to be distributed between December 2024 and March 2026, which is almost 11% of the market value. Scandic is traded at an FCF yield of just over 7% based on our estimates.

We continue to like Scandic, which has been one of the fund's largest holdings over the past year. The stock rose 9% on the day of the report and has risen 24% this year.

Bonesupport

Bonesupport has had a turbulent start to the year, which we wrote more about in the previous letter. In the end, the company had to come clean with its financial statements and did so with flying colors. Turnover was somewhat worse than expected, but operating profit (adjusted for positive effects from currencies and one-off costs) was around 9% better. Sales grew a whopping 48%, with the US continuing to be the driving force. Europe is also growing at a high level of 25% (adjusted for the UK which was weaker due to new priorities of the health care system there).

We also see an acceleration in growth in the second half (in absolute terms) which we believe is attributable to the launch of Cerament G for open fractures, which was approved in early 2024. However, the most important point in the report was the strong cash flow. The question marks built up by the market regarding the cash flow in recent months were set straight and the company was rewarded with a rise in the share price of 13%.

Another point to highlight is the company's phenomenal delivery time and time again – it’s like clockwork. The market keeps on questioning things from time to time, but the reports say otherwise. The stock rose 11% in February and was thus essentially unchanged for the entire year.

Kalmar

Finland's Kalmar also released its report in February. The operating profit was somewhat lower than expected, but more important was that the order intake was 19% better than expected. We believe that Kalmar is still relatively undiscovered. It is a globally leading company with a lot of things to optimize internally that we believe new CEO, Sami Niiranen, can solve with his background from Atlas/Epiroc. Another "kicker" in the case is that tow tractors in the US have been a weak segment since the pandemic: when things turn around there, there will probably be quite good momentum in the profit. The company trades at EV/EBIT 9x 2026e with an essentially debt-free balance sheet. The stock rose 5% in February and had thus risen 8% for the full year.

Vallourec

France's Vallourec had already announced its preliminary figures in January but still delivered a report that was 3% better than expected at operating profit level. The guidance for the first quarter was in line with expectations. At the same time, the company spoke very positively about the second half of the year after good order intake at the end of 2024, which was well received by the market. Vallourec is also a big relative winner on tariffs as production for the US market is 100% integrated in the US. Price expectations for Vallourec's products have risen for several months in a row, while the company may benefit from higher gas prices and expansion of natural gas. Something we haven't seen yet.

The company trades on our estimates at EV/EBIT 6x 2026e with a debt-free balance sheet. The stock rose 2% in February and has risen 14% for the full year.

SLP

SLP continues to deliver fantastic reports. This time, the management result was approximately 20% better than expected. SLP, like other real estate companies, had a slow start this year and the share fell 2% during February, despite a brilliant report. We believe that an important reason for that is that the company's CEO sold shares shortly after the report. We do not place any importance on his sale but continue to like SLP which will create more value for the owners over time. As of the end of February, the stock had risen 2% in 2025.

Biotage

Biotage is the big disappointment this year after a decline of 21% in February and 31% for the full year. From the financial report, we could see that the operating profit at the EBITDA level was 15% worse than expected, adjusted for one-time revenues. The recently acquired company, Astrea, stood out as slightly weaker, while the small molecules segment was in line with expectations.

We suspect that the company's cautious comments about Astrea's order book for 2025 were what really made the market choke on the report day. Our view is that the order book is only 15-20% of a year's sales value, which makes the comments even more odd. (It basically takes one call to fill the order book again.) Currently, Astrea is very dependent on a few large customers, and their orders tend to be large but vary greatly from quarter to quarter. Therefore, investors should not look at individual quarters. According to the company, one should expect a softer first half for Astrea.

However, we believe that now is an excellent time to buy the stock. With higher organic growth, margins, and return on capital, Biotage is now trading at a 23% discount to the sector, based on already downgraded analyst estimates.

Last week, Thermo Fisher acquired Solventum's purification and filtration business from 3M, which operates primarily in bioproduction. For this, they paid 40x EBIT (before synergies). This shows that Thermo is now competing with Sartorius, Repligen, and Danaher in bioprocessing. Astrea could probably be seen as a good complement to that portfolio. At the same time, Astrea is implicitly valued at zero according to our view of Biotage's valuation today.

We have spoken with Biotage's management, board members, and chairman to express our dissatisfaction with how poorly they have communicated to the market. It is a significant underperformance for everyone when Biotage is trading at historically low multiples, and they almost assign a negative value to Astrea, which we estimate will earn 150 million this year. Based on our estimates, the valuation is at a low EV/EBITDA of 12x for 2026.

Cargotec

Cargotec (which will soon change its name to Hiab) also released its financial statements in February. The adjusted profit was slightly better than expected, but what stood out the most was the order intake, which was about 10% better than expected. It is the first quarter since 2022 that orders are growing, and we believe there are good chances that the company will adjust its forecast during the year.

What the market took note of in the report, however, was a lower-than-expected payout from the now-sold MacGregor business leg. After adjusting the purchase price for debts in the working capital, the payout was approximately 200 million less than the market believed. The share price fell in line with that demise. Looking ahead, Cargotec is well-equipped with substantial net cash and ready to make acquisitions before a new cycle. The company trades at EV/EBIT 11x 2026e on our numbers, which is too low for a company of this quality. The stock fell 4% in February, and as of the end of February had fallen 9% for the entire year.

HBX

In February, we participated in the IPO of Spanish HBX. It is Europe's first major IPO in 2025. As one of the first technology companies to be listed in Europe in a long time, the excitement was significant. The offer was oversubscribed five times. The company is a global leader in connecting hotels and distribution channels (such as booking.com or Expedia). For this, HBX receives part of the price the end customer pays, which thus becomes HBX's income. The company has adjusted margins of over 50% and an expected profit growth of 10% in the coming years. At today's prices, we pay EV/EBITA 6.6x in 2026, which we think is very attractive.

Summary

Donald Trump has been president for only five weeks and the world, at least from a political perspective, is already in chaos. This cannot continue for another 203 weeks. The fact that Europe is now making a strong effort (which is absolutely necessary) can result in something good with an increased political and economic influence in the world.

In the rest of the world, the war in Ukraine is a much smaller issue and a stark observation was when on Friday night the 28th, after the breakdown in the White House, the American stock markets shot up and closed at daily highs. American investors don't care much about what happens outside its borders.

At the company level in the US and Europe, it is somewhat less dramatic, although certain sectors, such as the automotive industry, are working under heavy pressure and Trump's upcoming tariffs are likely to affect volumes and results. But on the other hand, these companies are valued at P/E 5-6x, so much should be discounted.

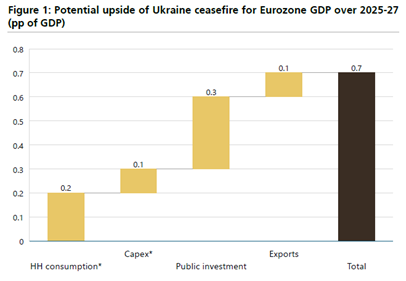

Below is an estimate from UBS on how Europe's GDP is expected to be affected in the event of a lasting ceasefire.

Source: UBS

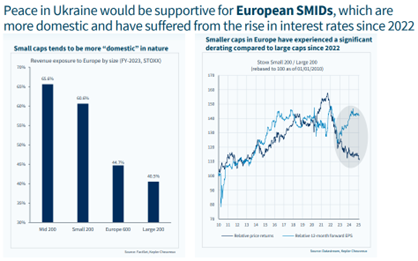

Small and medium-sized companies should benefit more than the stock market at large as they have more domestic and European exposure and have also not yet recovered from the shock of 2022 when interest rates rose sharply.

The image below illustrates well the difference in DAX (large companies) and MDAX (smaller companies) both in terms of price development on the left and exposure on the right. Since September 2022, the DAX has risen by 75%, while the MDAX has risen by a modest 15%. As much as 40% of the DAX increase comes from SAP and Siemens, which are large global companies. However, Germany's stagnation in recent years is clearly visible in MDAX development.

Source: Macrobond & Nordea

The major global investment company Abrdn has produced the analysis below which shows that UK's smaller companies have been the least popular with investors worldwide. They are currently valued at about a 25% discount to their 10-year average. The US, on the other hand, trade at a 30% premium. It is also a reason why the fund has roughly 20% exposure to SMID in Great Britain. Good companies at an attractive valuation.

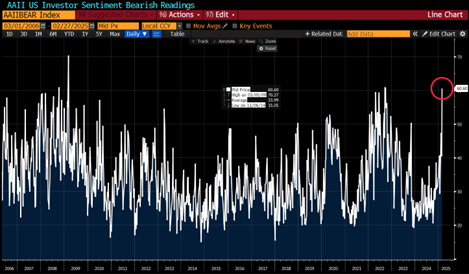

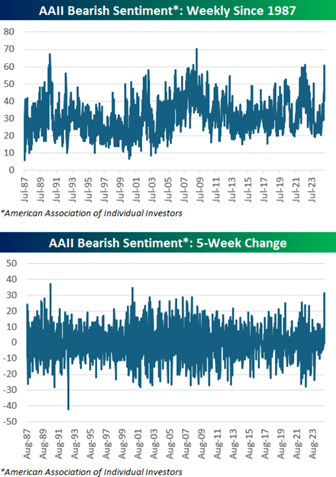

Turning to some data points regarding the world's most important stock market. On several occasions in recent months, we have referred to the euphoria among American investors that led to high valuations and concentration risk. Due to the small cracks in economic data that are now coming out, investor sentiment has changed rapidly in the US, see image below that shows bearishness among investors. Note the timeline spanning 20 years.

Source: Bloomberg

Illustrated in another way in the image below: bearish sentiment exceeded 60% last week, which has only happened five times before since the measurement period began in 1987. The five-week change is the third strongest measurement point only beaten by December 2000 and August 1990. When risk appetite and valuations are simultaneously at their maximum level, things can go downhill fast.

Source: Bespokeinvest

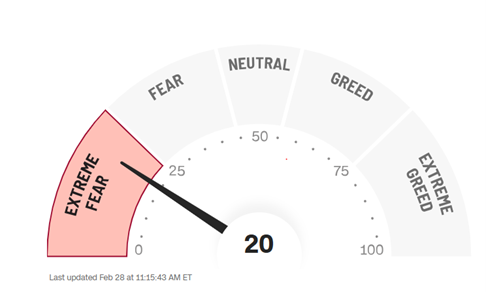

Fear & Greed index read on February 28th. This applies to the United States. In Europe, as you know, it has been significantly more positive.

Source: CNN

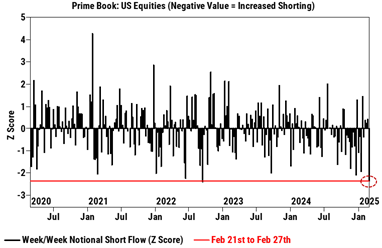

US investors shorted more aggressively in the last week of February than in the past five years.

Source: Goldman Sachs

The S&P500 is trading at a negative risk premium for the first time in 20 years. Challenging feeling to say the least.

Source: Bloomberg

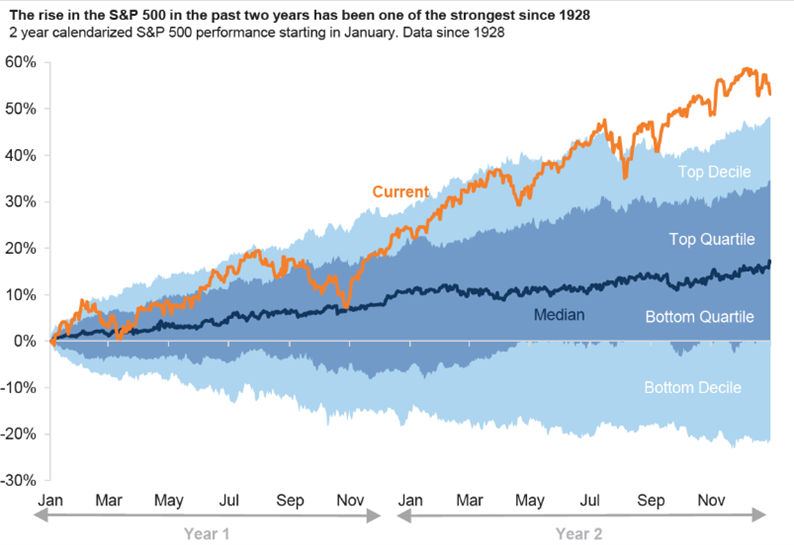

Note that the development of the S&P500 in the last two years has been stronger than at almost any time during the last 100 years.

Source: Goldman Sachs

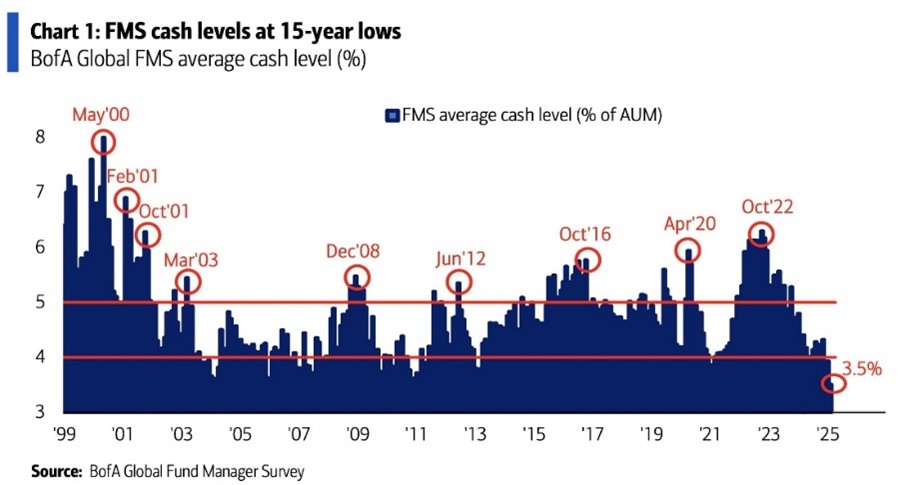

Meanwhile, global managers have the lowest level of cash since 2011.

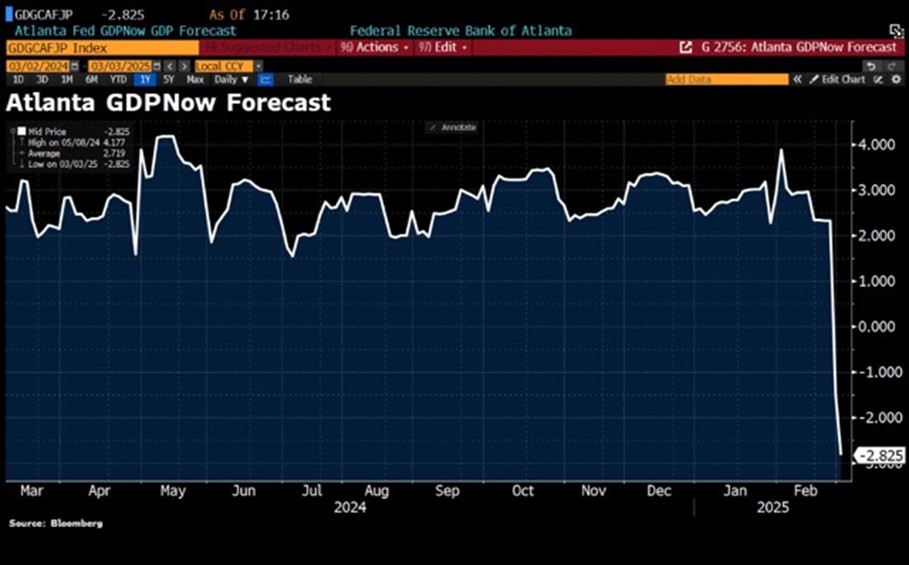

This picture came on March 3rd but is so spectacular that it had to go with the February letter. Admittedly, it is a volatile index, but it looks like something is happening down in Atlanta.

Source: Bloomberg

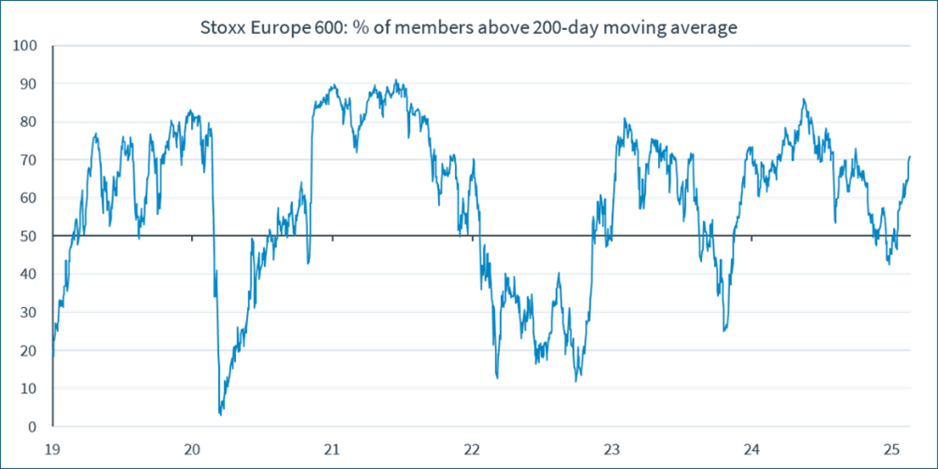

The development of the European stock markets has so far this year been significantly healthier than the American ones. Below shows the breadth of the market, which has been rising and is a good sign of quality.

Source: Kepler Cheuvreux

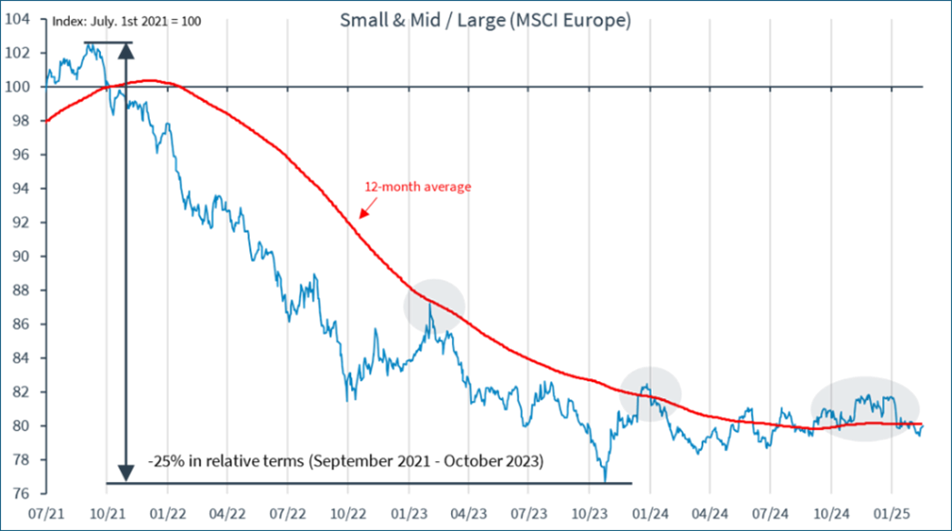

Smaller companies have traded sideways relative to larger companies over the course of a year. There is much to suggest that the smaller companies will soon break out of the trading pattern and have a stronger development. It did, however, already a year ago, show similar conditions but now it looks even better.

Källa: Kepler Cheuvreux

The record discount for European companies relative to American ones has narrowed a bit in the past month.

Source: Kepler Cheuvreux

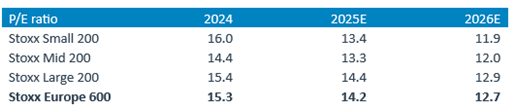

If we break out the valuation of the smaller companies in relation to the larger ones, we get the following table. An extremely attractive valuation in our view.

Source: Joakim Tabet, Kepler Cheuvreux

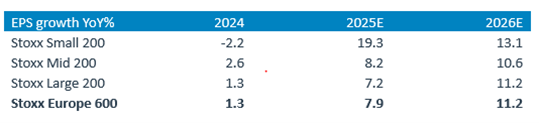

And below is expected profit growth.

Source: Joakim Tabet, Kepler Cheuvreux

Our synopsis of everything that has happened recently is that Europe will be forced to reform and stimulate its economies. It is, to say the least, much needed after a combined sleeping-beauty-like unconsciousness and a deprived-of-reality political policy that in an unimaginably short time (since the financial crisis) has driven Europe's productivity and self-confidence to the bottom.

In terms of security policy, the situation is serious, and we hope that the current situation cools down and that Russia is eventually defeated. The consensus and willingness among Europe's leaders to support Ukraine (except for Viktor Orbán of course) is after the crash in the White House last week at a new high level. Reasonably, if the will is there, Europe should be able to manage, with its muscles, a battered and greatly neglected Russia which, to put it mildly, has hardly contributed to the development of humanity.

Except for Biotage, we are satisfied with our companies' performance during February. Below we show a picture of how our companies delivered in relation to the market's expectations and how the share developed in relation to the index after the report. There are differences in measurement periods as our first company reported at the end of January and two companies as late as February 28th. But while it's not an exact science, it gives a sense of how the reporting season unfolded. So far, 12 out of 16 companies have exceeded expectations, which should be considered a pass.

Source: Coeli European

We have been busy with portfolio management and made some changes in the last month. Our small position in Corem is now liquidated and we have bought back into Commerzbank. The fund already has a stake in the Austrian bank, Bawag. We have also bought two smaller positions in German industrial companies where we continue to do analysis.

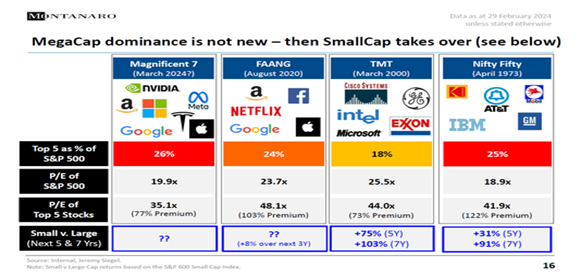

We found this picture in our drawers and which we already showed last year. Historically, when a euphoric period with strong price development comes to an end, the smaller companies have taken over the lead. It can be stated that the YTD development for Microsoft is -6%, Apple -4%, Nvidia -7%, Google -10%, Tesla -27%, Amazon -3% and Meta +14%. Now it remains to be seen whether the SMID companies can deliver according to history, but the conditions (excluding geopolitics) are exceptionally good.

Source: Montanaro

Now a new month awaits with fewer reports for the fund and more internal work in the form of analysis of existing companies as well as some new ideas.

We thank you for your interest and we will see you again in a month.

Mikael & Team

Malmö on 5 March 2025

Finally, and to the yes-saying and back-scratching journalist as well as the eagerly bleating JD Vance who questioned Zelensky's attire - below, Winston Churchill in the White House in 1942.

Source: Daniel Korski, X

IMPORTANT INFORMATION. This is a marketing communication. Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested. Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.