Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class' return. The information below regarding returns therefore differs from the returns in other share classes.

Before making any final investment decisions, please read the prospectus, its Annual Report, and the KID of the relevant Sub-Fund here

This material is marketing communication

Monthly Newsletter Coeli European – January 2024

JANUARY PERFORMANCE

The fund’s value increased by 3.2% in January (share class I SEK), while the benchmark increased by 0.6%. Since the change of the fund’s strategy at the beginning of September this year, the fund’s value has increased by 10.1% compared to a decrease of the benchmark by 0.9%. Both measured in SEK.

* Adjusted for spin-off of Rejuveron

** Includes September 1 (strategy change to active long-only as of September 4, 2023). Please Note: On the 4th of September 2023, the strategy of the fund officially changed from a European long biased equity long/short fund to a European active long only fund. Simultaneously, the name changed from Coeli Absolute European Equity (AEE) to Coeli European.

EQUITY MARKETS / MACRO ENVIRONMENT

The fund's strong momentum continued into the new year with positive performance of 3.2%. Our benchmark rose during the same period by 0.6%, measured in SEK. In addition to continued strong performance from our reporting companies, (LVMH, Axfood, Cargotec, Wincanton, CVS Group, Diploma and 4imprint) we received a cash offer for Wincanton at a 52% premium. More on that later.

The start of the year was calm with financial market players on much-needed long leave. In the middle of the month there was a bit of turbulence, and we experienced the weakest stock market day since October. It was due to hawkish comments from the ECB's, Sandra Waller, and Christine Lagarde who refuted the market's pricing of interest rate cuts. We also noted higher than expected inflation in the UK, as well as higher than expected US PPI numbers. Investors quickly began to buy the dip, especially in high quality companies. This led, a few days later, to a new high for the S&P500, the first in 746 days. Stoxx 600 is currently about two percent away from its highest level, while European small and medium-sized companies are about 20% away.

Low expectations and attractive valuations meant that the reporting season in Europe got off to a flying start with European champions that surprised positively and where we saw strong price reactions. The ASML share rose by 15%, SAP by 7% and our own holding, LVMH, rose by a whopping 14% which was the strongest price movement since October 2008! That says a lot about how low expectations were. It was large caps that drove the indices in January with impressive Q4 reports, see picture below with data since 2006.

For better or worse, Europe is also a gamble on China's economic development. Europe benefited in January when the Chinese central bank cut reserve rate requirements for banks and signalled future policy easing. As we wrote last month, our basic analysis on China is that there is more upside than downside from current levels. There is likely some political pressure in China when they note that Chinese shares are traded at P/E ratios that are lower than the P/B ratios on the Nasdaq exchange... All the above contributed to Stoxx 50 climbing to a level that we last saw before the GFC.

Source: Bloomberg

The above picture looks depressing to say the least, but there are several opportunities with great potential in the European stock markets if you focus on companies and fundamental factors instead of how many basis points a company weighs in an index.

The image below shows a European small-cap index compared to Stoxx 50 since 2001. When Stoxx 50 has risen by 1 (!) percent, the small-cap index has risen by almost 400%.

Source: Bloomberg

Another interesting observation at the mega-cap level is that five companies in Europe are behind 50% of the rise in the broad European index since 2009. ASML, LVMH, SAP, Siemens and TotalEnergies. These five companies make up approximately 28% of EuroStoxx 50. In 2000, the five largest companies were Deutsche Telekom, Nokia, France Telekom, Shell and Siemens.

A third interesting observation is Europe's equivalent to the big tech companies in the US (Magnificent 7), which a few years ago was named the Granolas. They are GSK, Roche, ASML, Nestle, Novartis, Novo Nordisk, L'Oreal, LVMH, AstraZeneca, SAP and Sanofi. They trade at a 30% discount to the Magnificent 7, but over three years they've risen 63% compared to the Magnificent 7's 50%. Impressive! Below the valuation difference between the two groups since 2015.

Source: Goldman Sachs

Continued hawkish (and slightly confusing) comments from the ECB at the end of the month did not change the market's view of the coming collapse of the policy rate. When the year ends, the interest rate is estimated to be around 2.4%.

Source: Bloomberg

The Riksbank (Swedish Central Bank) also changed its tone sharply, which bafflingly was in line with expectations. At the end of 2023, it was communicated that another interest rate increase was not unexpected. Now, just over a month later, it was on the contrary disclosed that an interest rate cut could happen even before the summer. We understand that there is a need to have a staring contest with the market, but it is a significant problem that central banks, with far too much power over people, almost every time have to say things that few informed believe. It doesn't feel great and borderline unacceptable. A bit like reading Pravda in the 1970s when a lot of people were working on interpreting what the Soviet Union really meant, while everyone understood that what was written was not true.

The problems in the Middle East continue and the Houthi rebels' attacks on freighters in the Red Sea have forced shipping to reroute via Africa resulting in significant price increases and delays. So far, the problems are manageable, but it could become a serious financial problem for world trade.

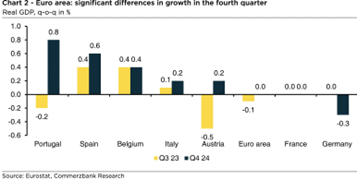

Below a number of relevant countries' GDP development for the fourth quarter of 2023. It is southern Europe that is in the lead. Sweden's growth during the fourth quarter was a modest 0.1%. US growth was an impressive 3.3%, but the economic cycle we're in is markedly different. Despite a long-standing strong US economy, ISM Manufacturing in the US has not been above 50 (expansion) since September 2022!

The European consumer has already seen improvements. In Sweden, we are lagging, among other things, due to variable interest rates and electricity prices, but Swedish consumer satisfaction between December and January showed the biggest improvement since the measurement started in 1996. Very promising!

Source: BNP Paribas

In Davos it was business as usual.

Source: X, Kochbank

In France, it was also business as usual with angry farmers blocking Paris and other big cities.

Source: X

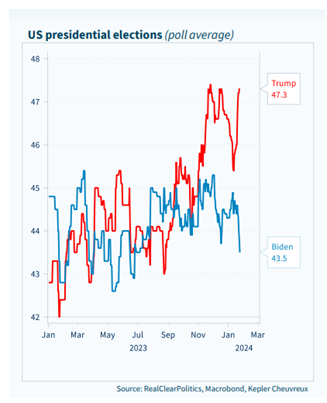

Donald Trump looks set to become the Republican nominee after a landslide victory in Iowa and an easy contest in New Hampshire. It has been 32 years since Bill Clinton was elected president. He is younger than both Donald Trump and President Joe Biden.

Source: X

PORTFOLIO COMPANIES

Wincanton

In January, we got the fantastic news that our British logistics company Wincanton had received a takeover offer. The buyer of the company is the French logistics company CEVA Logistics. The bid, announced on January 19th, landed at £4.50 per share. This corresponds to a bid premium of 52% against the closing price from the day before the bid was announced, or 82% against the volume-weighted share price from the last 12 months.

Wincanton was a contributing factor to the fund's weak result in March last year. The stock then fell by 40% after losing a major contract and we communicated afterwards that we were buying more shares as we thought the reaction was exaggerated. For a long time, we have felt that Wincanton was unfairly undervalued but after the takeover offer the share is now trading 120% higher than in March last year.

Before the offer, the company had traded at low single-digit earnings multiples while the management implemented several positive structural changes and improved the cash flow profile through a renegotiation of the company's pension debt. It also had a resilient financial development despite a very difficult economic climate where consumers' increasingly thin wallets had a negative impact on trade volumes. During the Christmas period, peak season for the business, Wincanton was even able to report organic growth, which we think is impressive given the circumstances.

In several conversations with the management team, we have argued that the company should start a share buyback program. This was finally due in 2024, but CEVA Logistics apparently shared our view of the valuation and thus had time to make their offer before the buyback program started.

Wincanton is the third logistics company in the UK to be bought by foreign stakeholders in a short time (the other two companies are DX Group and Clipper Logistics). It's probably no coincidence. On the one hand, logistics companies with Wincanton's profile have a bright future and benefit from trends in warehouse automation, outsourcing and increasing e-commerce penetration. In addition, many British companies are valued undeservedly low. Not least the companies with market values in the lower range. If the stock market does not want to reflect a company's true value, it is often a matter of time before the value is reflected in some other way - this time via a bid.

The Wincanton share was naturally the fund's top contributor during the month.

If we look at a couple of other British companies in the portfolio where we believe there is some takeover risk, we note 4imprint, the gift advertising company that has grown its profit per share by around 20% per year for eight years and trades at 10x operating profit for 2025e. (More about 4imprint below.) We also guess that there may be larger players who might want to sink their teeth into Volution, a ventilation company that should be able to grow profits by over 10% per year and is valued below 10x operating profit on our estimates for next year. Below is Wincanton's share price development since the beginning of 2023.

Source: Bloomberg

4imprint

The only real loser for the fund in the last reporting period was 4imprint. The company then released a financial update that was slightly better than the analysts' estimates, but with a slightly cautious guidance. The stock was down 12% on the day of the report because of that but we took advantage of the overreaction and doubled our position in the days that followed. In January, 4imprint disclosed another update. This time the message was much better received. When 2023 was summed up a record margin of almost 11% was recorded, leading to full-year profit estimates being exceeded by 8-9%. The stock rose 20% in January.

Biotage

The share rose by 10% in January and was thus one of the fund's best contributors. The year began with CEO, Tomas Blomquist, leaving his desk on the day and was replaced by the chairman of the board (and former CEO), Torben Jörgensen. Torben will act as interim CEO and the process of finding a new CEO is underway. We believe that the market views this positively as Torben is highly valued and is the person behind the construction of Biotage as it looks today. We also think the CEO change is positive, as Biotage enters a new phase after the acquisition of Astrea Biosciences. It also shows that the new main owner, Gamma Biosciences, has a long-term perspective and is not afraid to reshuffle the management team.

But it was probably not this that was behind the share's strong development in January, but more likely strong reports from similar companies such as German Sartorius and Swiss Lonza. In particular, the order intake caused the Sartorius share to rise 8% on the reporting day. Even their guidance was slightly better than what the market expected, and the hope is that the worst in the sector is now behind us. Biotage publishes its quarterly report on February 15th.

LVMH

Expectations were low when LVMH announced its fourth-quarter results on the evening of January 25th. The combination of a slight acceleration in Q4/Q3 organic growth (+10 percent vs +9 percent) and a positive outlook for the full year 2024 sent the stock up a whopping 13% on the day of the report, which was the largest single-day gain since October 2008 when the financial crisis was at its worst. That Europe's second largest company with a market capitalization of 390 billion euros can surprise the market with such magnitude is remarkable. Stressed investors and many sleepy analysts are probably the explanation, but the most important explanation (in our opinion) is that they ignored the valuation and focused on short-term momentum. It was absurd that one of the world's best companies before the report was valued around P/E 20x 2024e and around 18x 2025e.

A bonus for us was that we took some capital from the sale of Wincanton shares after the bid and bought more LVMH before the report. We also increased in Campari in the same way, which in turn rose by five percent on the same day, because the biggest positive surprise in the LVMH report was Wines & Spirits.

SUMMARY

Europe has had a good start to the reporting season with strong reports from well-known heavyweights. Doubtful investors with low expectations and still large amounts of capital on the sidelines have contributed positively to the development. The rise from depressed lows in October has been strong and has taken many by surprise. Large chunks of capital are prepared to enter the stock market (our assessment), which should mean that setbacks in the coming months are likely to be relatively mild.

The above, in combination with a more resilient economy and clearly falling interest rates during the year, mean that the outlook for small- and mid-caps looks better than it has for several years. Our conviction means that in this month's summary we focus on small-caps. Special thanks to Goldman Sachs who contributed significantly to this month's images.

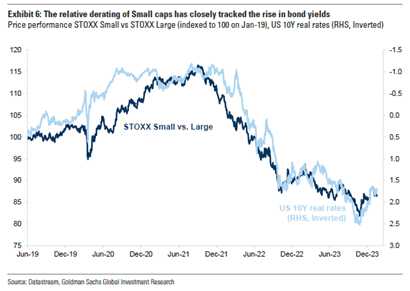

Most, including us, underestimated the power of rapidly rising interest rates on small-cap valuations. The course of the rise was record-breaking, and the magnitude was also very strong. With great probability, we are now at the highest levels for interest rates and thus also at the peak. It is the same force this time, but in the other direction and as an investor you should not miss this. The image below is as simple as it is clear. It shows the correlation between the inverted US 10-year interest rate and the price development of small companies in relation to the price development of large companies.

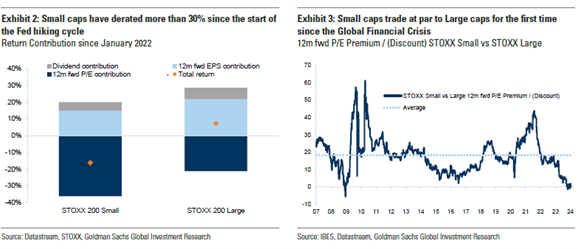

The image below shows the magnitude of declining multiples for small-caps versus large-caps (image on the left). For the first time since the financial crisis, small-caps are now valued at the same multiples as large-caps, despite stronger turnover and profit growth (image below on the right).

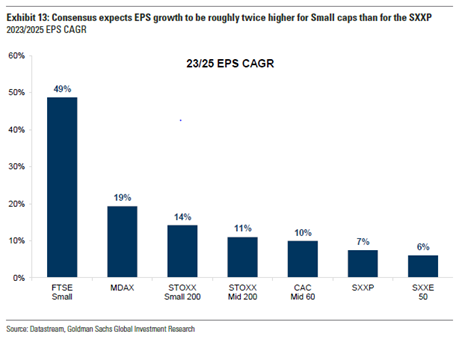

Below is expected profit growth for a number of different countries' small-cap indices. All markets' profit growth is significantly above the broad European index, which is expected to provide 7% profit growth per year in 2023/2025.

Since the lowest level in October last year, the development for small-caps has been 6% better but there is still great potential before catching up with the price development for the larger companies.

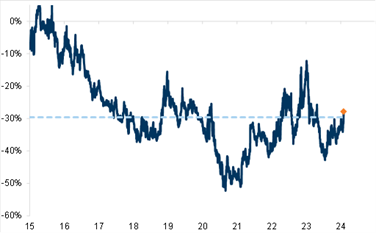

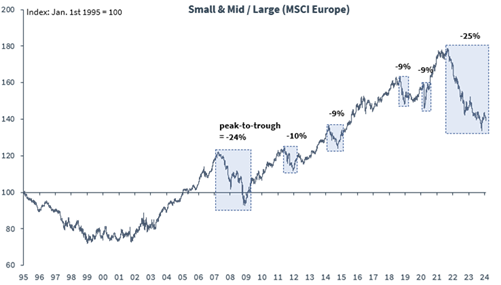

The image below illustrates the valuation gap since 1995. We would be surprised if the trading pattern this time deviates significantly from how it looked historically.

Source: Kepler Cheuvreux

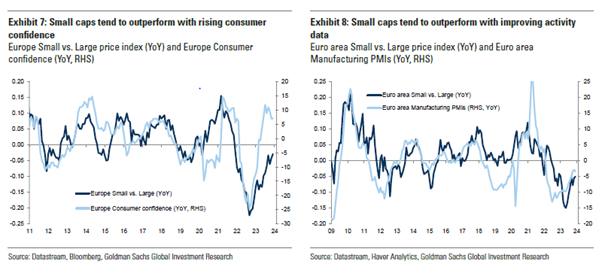

As we mentioned earlier, Europe consumer confidence is now rising. It is usually a development that favours, above all, small-caps.

After 22 months of more or less constant headwinds, stock markets trended upwards in early November. Inflows into European equity funds have been under pressure for the past two years, and this especially applies to the small-cap funds. If we are correct in our market view, it will likely reverse with more inflows and contribute positively to the development. Small-cap funds' inflows have decreased by as much as 25% since the beginning of 2022. There is no need for major improvements before it starts to show in share prices.

Despite the rise in the broad European stock market recently, the valuation remains at an average low level (white line). It is the profits that drove the rise in the market.

Source: Bloomberg

Hopefully you, as interested readers, have understood that we think you should increase your allocation to small- and mid-caps. We note that we are not alone in having a positive view as we saw several takeover bids during January. In addition to the bid for our own Wincanton, there were also bids for Byggfakta (which our sister fund European Opportunities owns) and Swedish Kindred, to name a few. We believe it could be a strong M&A year as company boards also see light at the end of the tunnel, while they are sitting on a strong balance sheet and there are many high-quality smaller companies at attractive valuations. We note that on Wall Street within fixed income, January was the most active month ever with $200 billion in new bonds.

In the short term, it is difficult to predict the development and we continue to face significant challenges geopolitically. For those statistically inclined, it may be interesting to know that the second half of February is the worst two-week period of the year (since 1928). Massive buyback programs are now rolled out again and if you, like us, have a strong view that inflation will continue to trend downward and that we will not have a deeper recession, it does not matter much in which month the interest rate cuts will come. They are coming soon, and the year is long.

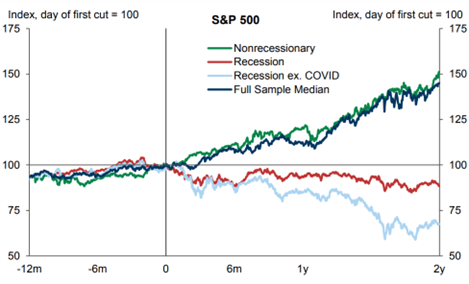

We conclude with the following slide showing the historical performance of the S&P500 after the Fed made its first rate cut (0 on the timeline). Don't read too much into the levels of the numbers, but more the direction of the different outcomes.

Source: Goldman Sachs

As always, the most important thing for the fund's development is how our companies develop. We are entering an extremely busy month and after a good start to the season, we are looking forward to future reports.

Thank you for your interest!

Mikael & Co

Malmö February 7th, 2024