Monthly Newsletter Coeli European – July 2024

This material is marketing communication.

Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class’ return. The information below regarding returns therefore differs from the returns in other share classes.

Before making any final investment decisions, please read the prospectus, its Annual Report, and the KID of the relevant Sub-Fund here.

July Performance

The fund’s value increased by 8.5% in July (share class I SEK), while the benchmark increased by 5.3%. Since the change of the fund’s strategy at the beginning of September this year, the fund’s value has increased by 26.6% compared to an increase of the benchmark by 11.6%.

Source: Coeli European

* Adjusted for spin-off of Rejuveron

** Includes September 1 (strategy change to long-only implemented September 4 2023)

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

Equity Markets / Macro Enviroment

The fund rose by 8.5% compared to the benchmark which rose by 5.3%. The biggest driver of the fund's return was strong reports from our portfolio companies, but an increased interest in small and mid-caps also had a positive effect. The Swedish krona fell by 1.9% in July against the euro, which also had a positive impact (SEK share class). The fund's top three contributors were British Volution, Biotage and Swiss Accelleron. The weakest contributors, but with minor numbers, were LVMH, Scandic and German Bechtle.

Since the end of June until the beginning of August, we have experienced a tsunami of political and economic events:

- President Joe Biden's disastrous debate against Donald Trump which led to Vice President Kamala Harris now being the Democrats' new presidential candidate.

- The assassination attempt on Donald Trump.

- The election in France which offered great drama and ended with no party taking a majority, with all that that implies.

- Britain got a new government in the form of Labour, after the Conservatives historically made a very weak election.

- US inflation fell more than expected in June, leading to extremely strong sector rotation.

- We witnessed new levels of misery in the Middle East after various attacks from both sides.

- The Bank of Japan raised interest rates for the second time in 17 years, which, to put it mildly, was not well received.

- The Bank of England cut the key interest rate for the first time since the Covid outbreak in early 2020.

- The Fed kept interest rates unchanged but flagged for a cut in September.

- The first two days of August saw weak economic data from the US which contributed to a very weak start to the month, more on that later.

- All the above was topped with a slew of company reports which, among other things, revealed that China's economic problems are bigger than most people anticipated.

In this environment, the fund returned 8.5%, which can be compared with other relevant indices (measured in SEK) such as OMXS30 +1.6%, Stoxx 600 +3.3%, S&P500 +2.2%, Nasdaq +0.3% and the Russell 2000 a whopping +11.3%.

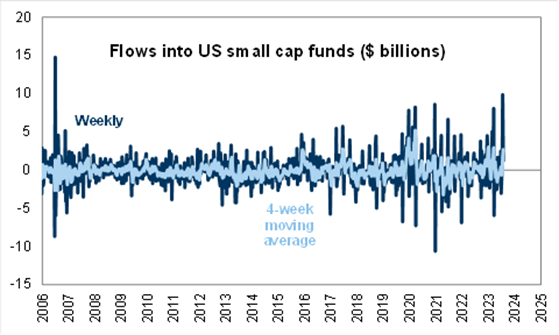

What triggered the strong rotation into, above all, US small caps was lower than expected inflation for June. Smaller companies typically have weaker balance sheets and benefit more from interest rate cuts than large companies. In addition, and more importantly, the extremely high concentration of capital deployed to large technology companies, while very low concentration in small companies, led, in the US, to the strongest sector rotation from the S&P500 to the Russell 2000 since February 2000.

Inflows into US small cap funds have increased during the summer.

Source: Goldman Sachs

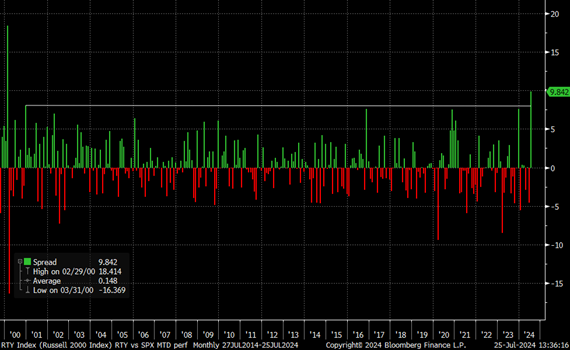

Inflows which in turn drove up share prices. The image below shows the difference in returns between the Russell 2000 and the S&P500 since 2000. Not since then has the small-cap index had such a strong excess return, +9.8 percent in July, compared to the broad index.

Source: Goldman Sachs

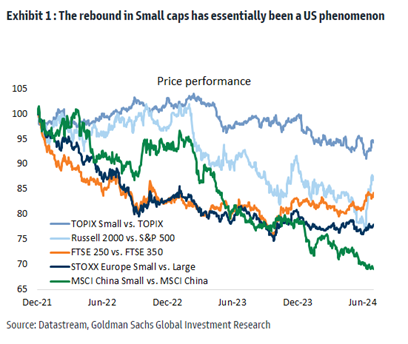

The strong rotation in the US into small caps was not as dominant elsewhere, see picture below, but the extreme concentration risk is very much an American phenomenon. Until a week ago, MAG7 (excl. Tesla) accounted for 60% of the year’s return in the S&P 500. The volatility that existed in the market in July was almost non-existent for our fund, which simply benefited from the turbulence that arose.

Source: Datastream, Goldman Sachs Global Investment Research

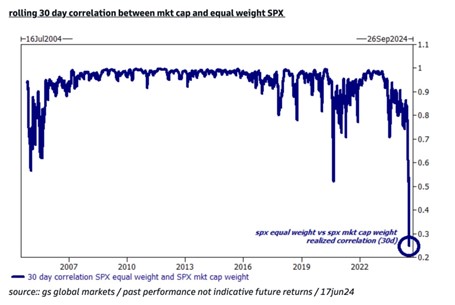

The image below enhances the understanding of the turbulence we are currently experiencing. The correlation between the regular S&P500 and the equally weighted S&P500. The large technology companies have lived in a world of their own and when high expectations are not fully satisfied, investors must adjust their expected return on the companies’ AI investments. When such a large proportion of the market has such high exposure to the same companies, things go downhill fast.

Source: GS Global Markets

Nvidia. Until recently, it has been the world’s largest company measured by market capitalization, but the last few weeks have seen extremely high volatility. There is something wrong when a $3 trillion company is traded like a mediocre micro-cap company. On August 28th, their quarterly report will be released.

Source: Bloomberg

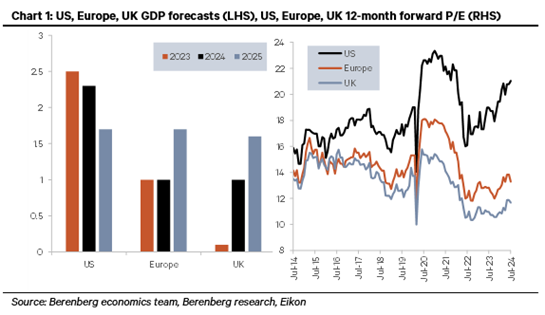

The fund’s exposure to the low valued British market was also a positive factor in July as the FTSE 100 was a stable market with a +2.5% return. FTSE Small Cap rose by 3.9% and takeovers of British companies continue with, for example, Carlsberg making a bid for Britvic. The fund’s exposure to the UK is approximately 22%. The UK economy is also starting to improve from low levels. See image below with GDP forecasts on the left and P/E ratios on the right.

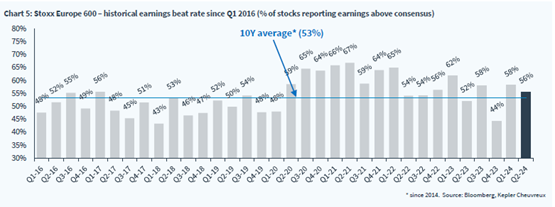

When just over half of the European companies have reported, it can be concluded that things have somewhat improved - 56% of the reports have surprised positively in terms of results.

Source: Bloomberg, Kepler Chevreux

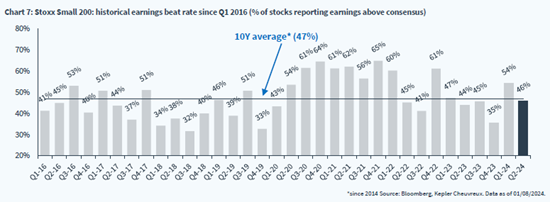

For the smaller companies, however, it has been a little weaker than expected.

Source: Bloomberg, Kepler Chevreux

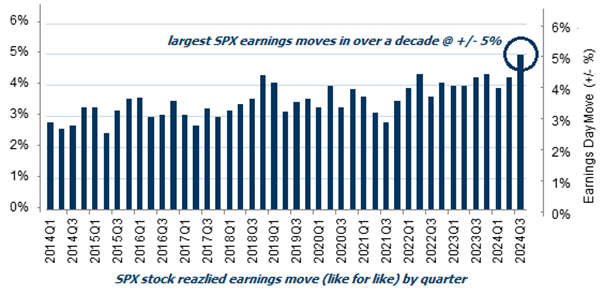

At stock level, the reporting season has produced the biggest earnings moves in 10 years in US stock prices.

Source: Goldman Sachs

What stood out during the reporting season is China's economic situation, which is worse than feared. It has affected luxury companies such as LVMH, but also auto stocks have had significant headwinds recently. What has surprised positively in Europe are construction related companies, which in many cases believe that they have reached the bottom and are now seeing rising order books in several places. The fund's two holdings, Lindab and Volution, rose by 17 and 21% respectively in July.

The image below depicts how European companies with significant China exposure performed 7% worse than the Stoxx600 in July.

Source: UBS, Bloomberg

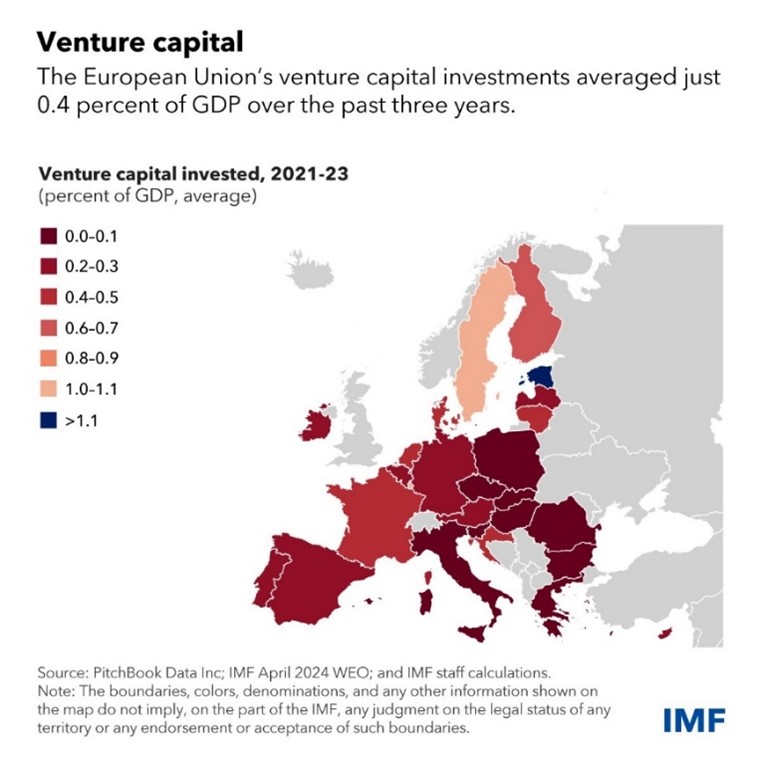

Sweden stands out in Europe in terms of venture capital investments in relation to GDP. On a global basis, Israel comes first followed by the United States. Sweden ends up here in fifth place.

Source: IMF

Donald Trump had a guardian angel when a deranged 20-year-old tried to assassinate him on July 15, see clip here. https://x.com/EndWokeness/status/1813314243434856885

He was coolly to say the least, both when it happened, but also in the days afterwards when he continued as if nothing had happened. He also managed to launch a limited edition of new trainers called Fight. However, no one has been more cool-headed than Ronald Reagan: https://www.youtube.com/watch?v=5UowNDaxRqU

After President Joe Biden threw in the towel, it is no longer as clear that Donald Trump will win the election this fall. At the end of the month, Trump made a criticized appearance at the convention of black journalists of the United States, where he, among other things, questioned the identity of Vice President Harris and claimed that she "happened to be black" a few years ago because it benefited her politically.

Source: X

Source: HEDGEYE

Portfolio Companies

After an uneventful June, the reports rolled in during July and offered all the more news. Overall, the reporting period so far has been clearly positive for the fund's holdings.

Volution

The British ventilation company released, during the month, an update for the financial year ending July. Despite a construction industry that is under serious pressure, Volution is expected to grow by 7%, of which 1% organically. The operating margin is expected to land at around 22%, which is the highest figure since 2015 when we look back at the numbers in our model. All in all, this leads to earnings per share growing by around 7% compared to the previous year.

In a context when many other HVAC companies (heating, ventilation, air conditioning) are on their knees due to low levels of new construction, uncertainties regarding energy subsidies mainly in Germany and high interest rates that have eroded consumers' opportunities to renovate, we think this is a very good result.

During the year, Volution has particularly benefited from its exposure to the UK. It is the market where the company most clearly benefits from increased regulations that place demands on the energy efficiency of buildings.

For the coming financial year, we anticipate continued strong growth in the UK, while Volution's European markets should return to growth. With a record strong balance sheet, there is plenty of room to make acquisitions. Historically, Volution has acquired companies that, after three years on average, generate an operating profit that corresponds to approximately 18% of what was paid. Due to that yield profile, acquisitions are appreciated by the market.

The Volution share rose by 21% in July and has thus risen 26% for the full year.

Lindab

Lindab's report for the second quarter of 2024 beat the pre-estimates by about 6% at operating level. After six quarters of negative organic growth, we are starting to see a glimpse of light in the tunnel. CEO, Ola Ringdahl, believes in gradual improvement of volumes during the second half of the year. Within the important ventilation segment, the company hopes that 2025 will mark the start of several years of positive organic growth.

As Lindab's long-term investment program in machines, factories and capacity is now coming to an end, there is a large unused production capacity within the company. During the conference call in connection with the report, it was mentioned that the company can increase its production volume by 20–30% without significantly increasing its costs. With gross margins already at high levels by Lindab's standards – despite a weak market with low volumes – there should therefore be significant operational leverage when volumes turn around.

In addition to this, the company will continue to acquire companies at a high pace. Today we regard Lindab as a serial acquirer. If we have managed to count correctly, we amount to 22 acquisitions since 2021, which together add up to approximately SEK 3.7 billion in sales. The acquisitions are made exclusively within the ventilation segment, which on a rolling basis account for around 75% of sales. In 2018, the same figure was 62%. The ventilation segment is less cyclical, has more stable margins and has higher structural growth than Lindab's other segment, Profile Systems. All other things being equal, the ventilation business thus deserves a higher valuation than Profile Systems.

The acquisition strategy also has other advantages. Even though Lindab is managed decentralized with a lot of freedom and responsibility at the subsidiaries, there are low-hanging cost synergies in the purchase of steel. The company is one of Europe's largest steel buyers and therefore has a favourable negotiating position against steel companies, which the smaller companies that Lindab acquires do not always have. In some cases, there are also sales synergies. The acquisitions are typically made at attractive multiples, which then improve as synergies are realized.

The Lindab share rose by 17% in July and has now risen by 33% in 2024. Since the bottom in October last year, the stock has risen close to 100%. Although the company's valuation has risen, we believe there is upside in the estimates for 2025 and 2026 if volumes return. The analysts also do not price in more acquisitions, which will most likely come.

Accelleron

The former ABB spin-off has been one of the fund's best holdings since we invested in the company in the autumn of 2022. The company, which manufactures turbo engines for the energy sector and the marine industry, is currently benefiting from a very strong business cycle in the marine sector. (Many public companies with some activity connected to the marine sector are currently doing very well: Finnish Wärtsilä, Konecranes, Cargotec and Kalmar are a few names. A couple of others are French Bureau Veritas and British Clarkson.) Shipping companies globally have order books that stretch into 2027, which provides good visibility.

In July, the company released a reverse profit warning. Growth of 9–12% is now expected in constant currencies. The previous guidance was 4–6%. In addition, it is believed that the operating margin will land at around 25%, compared to the previous expectation of 24.5%. This led to analysts needing to raise their estimates for the full year. Off the top of my head, this is the third time Accelleron has raised its guidance since listing in 2022.

The Accelleron share rose by 24% during the month. For the full year, Accelleron has risen by as much as 66%. Last year, the stock rose by 37%. The rise in earnings multiples for this quality company is well justified. At the time of writing, the stock is valued at around 17x EBIT on our 2025 estimates. That is by no means low and should be compared to the single-digit multiples we saw at the time of our post-spin-off investment in 2022, when index funds and other funds were throwing out Accelleron shares. We do not expect any further appreciation going forward and expect a return that is more in line with profit growth and collected dividends.

Below you can see the price development since our investment in the autumn of 2022. In addition, the share has a beta of only 0.75!

Source: Bloomberg

Bechtle

We have a minor position in German Bechtle, which is active in the IT sector and sells hardware, software and related services. The business is similar to Swedish Dustin or Norwegian Atea.

Bechtle's financial history is very good with several years of double-digit profit growth. This year, however, deviates from the trend: For the first time since 2009, Bechtle had to adjust its profit forecast downwards. Instead of 5-10% growth, they now believe in unchanged sales and profits in 2024. The main reason for this is continued weak demand from the primary customer group: small and medium-sized companies in Germany. At the same time, Bechtle is big in the public sector, which is currently doing better than other customer groups. In July, it was announced that it had won a major contract with Germany's federal authorities with a total contract value of up to 770 million euros.

The downward revision of the guidance was expected by the market, as several European competitors reported similar developments, and when the news came the stock fell by only 0.5%. Our best guess is that the company's growth and profitability will normalize by next year. If it does, the valuation right now looks very attractive. The stock fell 7% in July and has fallen 10% in 2024.

Euronext

Euronext, which owns several European exchanges, delivered another good report in July. The result was a few percent better than the analysts had expected. In total, earnings per share grew by approximately 19% in the most recent quarter, largely thanks to good volumes in equity, currency, energy and options trading. On top of that, Euronext's revenue, which is independent of volumes, continues to grow at a good pace. Over time, the more stable and predictable revenues will grow as a share of the revenue mix, which, other things being equal, should lead to an appreciation of the stock.

The Euronext share rose by 8% in July, and for the whole year has increased by 19%. We think that is more than acceptable for what we consider to be somewhat of a low-risk investment (although, of course, black swans can appear everywhere).

CVS Group

We continue to have a small position in the veterinary company CVS Group. The stock is currently under pressure from the CMA (British Competition and Markets Authority) investigating the veterinary sector, which has undergone a major consolidation in recent years and where prices to end consumers have risen significantly since the Covid-era. We believe that the fears surrounding the outcome of the investigation are exaggerated. We have rarely had reason to complain about the company's operational development, but in July, CVS provided an update that was actually on the weaker side. Despite that, the share price rose on the report, presumably because expectations are so low and the stock is trading at a P/E of 10-11x 2025e, which is very low.

The CVS share rose by 13% in July, and for the whole year has fallen by 32%.

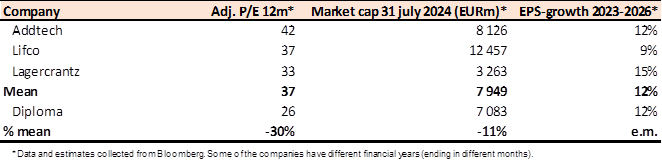

Diploma

The British serial acquirer released, in July, an update for its third quarter ending in June. This time too, the result looked good. For the full year, Diploma expects growth of 16% (of which 6% organic growth) and 15% growth in earnings per share, with 90% cash conversion. The stock is valued high but justified. If you compare Diploma with many Swedish serial acquirers, it looks almost cheap. In July the share rose 7%, and for the whole year it has risen 24%.

Source: Coeli European

Biotage

Following cautious comments from a couple of industry peers during the beginning of the summer, it was Biotage's turn to follow suit with its quarterly report for the second quarter. This is a typical example where direct comparisons with other companies can be very dangerous. Biotage came out with a report that was about 8% better than consensus. Much of this was driven by the subsidiary Astrea, which increased its sales by 70%. The organic sales increase was a whopping 9% - and the company is yet to see tailwinds from the sector, which should come soon.

Later in the month, other companies such as Danaher, Thermo Fisher and Repligen came out with positive comments, which improved sentiment. After a period of inventory corrections, major pharmaceutical companies now appear to be placing orders in line with normal levels. The activity of smaller customers is also increasing. Worth noting is that the chromatography and protein segments perform strongly at Repligen. These are two of Astrea's main areas. Overall, most companies in the sector have concerns about China. Fortunately, China only accounts for about 5% of Biotage's business.

During the month there was a rumor that KKR was exploring alternatives for its stake in Biotage, which amounts to nearly 17% of the shares. According to the article, Biotage has been gauging interest from potential buyers separately from KKR. KKR still has lock-up until May 2025 but is free to sell in the event of a takeover. From what we understand, there have historically been a number of interested parties for Biotage. It is not particularly strange as there are not very many lab tool companies like Biotage globally.

Biotage shares rose 23% during July and by the end of the month had risen by 50% for the full year.

Bonesupport

Bonesupport continues to surprise on the upside. In the second quarterly report, sales were around 9% better than expected. The big difference to analysts' estimates was that Cerament BVF in the US grew by a whopping 13%. We, like the market (and certainly the company), have expected a certain cannibalization of BVF after the launch of Cerament G, which is similar to BVF products except for that it contains antibiotics. Now it sounds like Cerament G is increasing the penetration of Cerament BVF. That phenomenon is probably due to the fact that BVF products are cheaper and can be used for simpler procedures that do not require locally releasing antibiotics.

In connection with the report, the forecast for the full year was also raised. The expectation is now that sales will grow more than 50% in 2024 (previously 40%). It has been six quarters since Bonesupport made a profit for the first time and now it has generated an operating profit of SEK 114 million on a rolling basis. With high gross margins and fixed costs that grow at a slower pace than sales, the operational leverage in the company is very high.

Few seem to have noticed that Johnson & Johnson in its latest report talked about increased competition within its trauma division. It is not entirely impossible that Johnson & Johnson has noticed the approval of Cerament G. Bonesupport received approval for Cerament G for open fractures (trauma) in March of this year. For those doctors who used Cerament G for bone infections, there are now no obstacles to using it for trauma patients. Because the product is so much better than the competitors', we believe that Cerament G is used for trauma cases at a relatively large scale already thanks to the approval. However, Bonesupport has not started marketing the product yet. That will happen in connection with a large conference this autumn.

Acquisition activity among the major medical technology companies has been very slow over the past two years. But this year, the activity has picked up, which is visible in all companies. Stryker has made several acquisitions and in July alone they made two. The Cerament G product is likely to fit well into several of these product portfolios. Although Bonesupport is many, many times smaller than these, the company's sales in absolute figures are actually growing more than players such as Johnson & Johnson, Stryker, and Zimmer Biomet (isolated for orthobiologics).

These giants already have a global sales network. If we toy with the idea of Bonesupport being acquired by one of these, they will get the fastest growing product with 85-90% contribution margin (95% gross margin and some support functions). This would mean that such a company pays 16-17x operating profit in 2025. That is a low multiple for a company of Bonesupport's nature. Having said that, this is of course a simplified exercise, and we never invest in companies because we hope for a bid.

The stock rose by 15% in July and has risen by 60% in 2024. Last year, the stock rose 134% and was the best stock on the Stockholm Stock Exchange.

SLP

It is almost redundant to receive reports from SLP on a quarterly basis. The business is ticking like a Swiss watch and the second quarter was no exception. The report came in just above expectations and the stock was rewarded with a rise of 4% on the day of the report. The management result increased by 26%, mainly driven by continued property acquisitions. It is incredibly pleasant to own a company with good management who has found a small niche that they are very good at.

The balance sheet is strong, and the company is on a stable financial footing. There is secured bank financing and available liquidity of approximately SEK 1.4 billion for continued acquisitions and investments. After a period with increased yield requirements due to higher interest rates, we now see that these have started to level off. If future interest rate cuts go ahead as planned, we will soon see a tailwind from this which directly translates into increased valuation.

The stock rose by 13% in July and has thus risen by 17% in 2024.

Scandic

Scandic delivered a report with results that were slightly better than expectations. Despite that, the share fell by around 6% on the day of the report, probably because the Scandic share price had risen significantly before the report. The third quarter has begun in line with last year but with slightly higher prices. We think it's a great time to look at Scandic now. Based on our somewhat conservative estimates, the share is valued at 8-9x net profit. This with a net cash at the end of the year.

Scandic has negative working capital, which means that the multiple you pay for the free cash flow is lower than the profit multiple (as long as the company grows). So far this year, the company has redeemed SEK 540 million of its convertible loan early. In October, the remaining part will be released and then the company can set a new agenda for its capital allocation. Given the strong cash flow and the low valuation, we believe that Scandic will launch a buyback program. There will probably also be a capital markets day with updated financial goals.

The stock rose 1% in July and has risen 40% this year.

Corem

During July, Corem delivered a good report for the second quarter and the stock rose on the day of the report. Corem continues to deliver positive net lettings, which will help the relatively high vacancy rate going forward. The net asset value amounts to just over SEK 17, which is a discount of 45% compared to the share price at the time of writing. As previously stated, the rise in the yield requirement is leveling off and we should see reductions fairly soon.

During the month, Corem made a directed share issue that brought in just over one billion kronor. The reason was to proactively strengthen Corem's balance sheet and to resolve the company's expensive hybrid loans. The hybrid loan has cost Corem SEK 160 million annually and, other things being equal, will increase the cash flow by 15%. We thought it was very positive that the company is strengthening its balance sheet and therefore we participated in the issue. Subsequently, Corem looks stronger than ever.

The stock rose by 9% in July. For the full year, the share has fallen by -10%.

SUMMARY

The market in July was bifurcated, with trading on the one hand usually characterized by the calm of summer, but on the other hand containing an unusually large number of dramatic events and changes that for short periods led to dramatic and volatile sector rotation. Given the drama that unfolded in the first few days of August, we include some data points below from those days and our reflections.

In recent weeks hedge funds have disclosed a historically sharp reduction in their gross exposure, when they suddenly realized that they owned the wrong stocks (American technology companies). A lot of capital had been allocated to winners, which quickly turned into losers. In addition, several crowded short positions began to rise sharply as short sellers began to cover their positions. The rest of the market was also caught out, as too many investors held the same holdings. That led to the Russell 2000's outperformance over the S&P 500 in July being the strongest in 25 years.

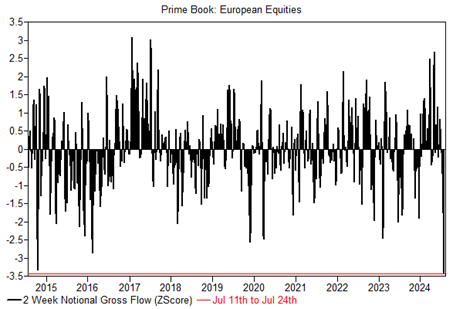

Similar patterns have also been seen in Europe, although less extreme than in the US. The image below shows hedge fund sales of European stocks, which since the end of June have been the strongest since 2015. The catalyst for this was probably the political turmoil in France.

Source: Goldman Sachs

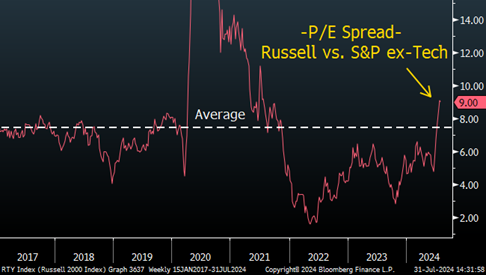

The P/E ratio premium for U.S. small caps compared to the S&P500 excluding technology soared in July after soft inflation data raised hopes for more rate cuts. The Russell 2000 is probably the index that is most sensitive to how the FED acts. The premium to the S&P500 at the end of July was higher than usual, which is unusual unless the economy is in an early recovery. During the beginning of August, we believe that the premium dropped by a unit.

In order for small companies to continue to develop well from here, in addition to expected interest rate cuts, good economic development is also required. As mentioned earlier, it was above all US small caps that had a strong development in July and this is mainly due to the fact that the US had the highest expected economic growth, as well as higher expectations for interest rate cuts.

Source: UBS

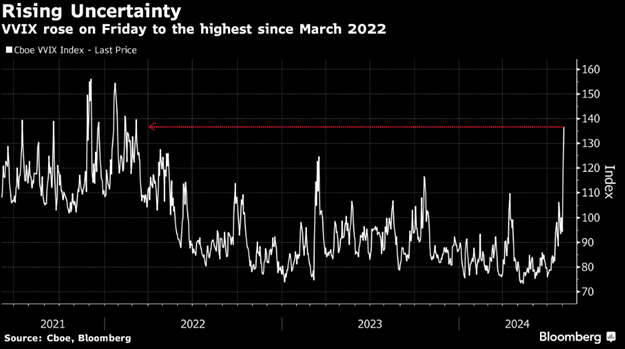

The starting position the market was in when the rotation started was also extreme, to the extent that it had been more than 1.5 years since we last had a five percent correction in the US stock market. It is the fifth longest period measured in the last 20 years. See image below of the VVIX index showing expected volatility on the VIX index which includes Friday, August 2nd.

Source: Bloomberg

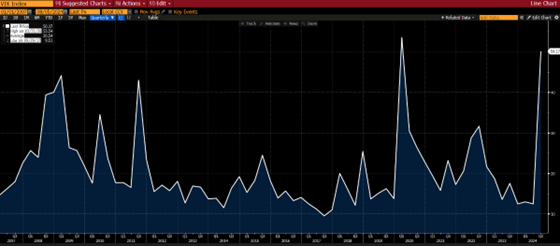

As someone pointed out on X: According to the VIX index, the three worst periods in the market have been the GFC in 2008, the Covid crash in 2020 and when the Bank of Japan raised its policy rate by 25 basis points this year. That’s one way to look at it. At the time of writing, it feels a bit hysterical. Below is the development of the VIX index since 2007.

Source: Bloomberg

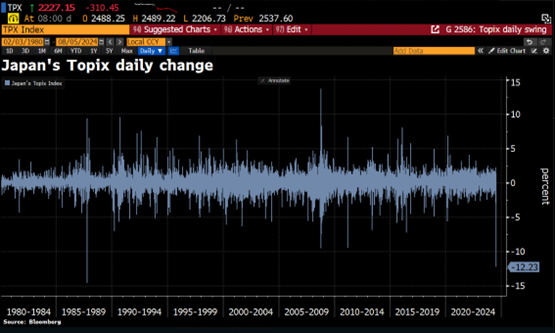

On Monday, August 5, the Nikkei index fell by 12.2%, which was the largest single-day decline since 1987. The day before, the index had fallen by 5.8%. On Tuesday, August 6, the Nikkei rose by 9.2%, which was the strongest rise since October 2008. Not exactly dead-on target. It would have been priceless to be a fly on the wall inside the Bank of Japan now. In any case, it can be noted that their interest rate increase of 25 basis points did not go down well. Borrowing costs are now in positive territory…

Source: Bloomberg, Holger Zschaepitz

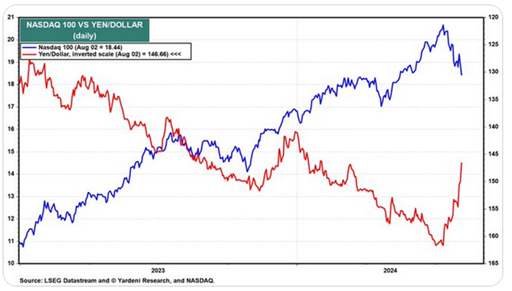

Below is the image of the month showing the development of the US dollar relative to the Japanese yen. The dollar has fallen by almost 20% in a few weeks, and the collapse came in connection with the Japanese interest rate hike last week. Investors have borrowed the yen that cost nothing and bought American shares, a so-called carry trade. When the positions are to be reversed, and also at the same time, there will be enormous pressure on currencies and the stock market. Safe to say that large losses have probably occurred here.

Source: Bloomberg

The image below shows the development of the Nasdaq 100 in blue, and JPY/USD inverted. Wondering if they will meet soon?

Source: LSEG Datastream, Yardeni Research

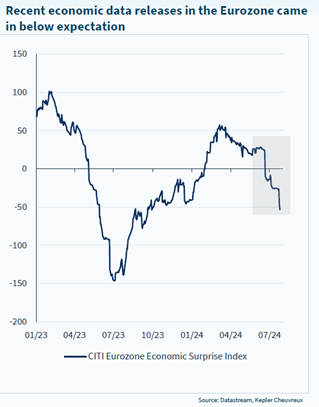

Europe has also reported weaker economic signals over the summer.

Source: Datastream, Kepler Cheuvreux

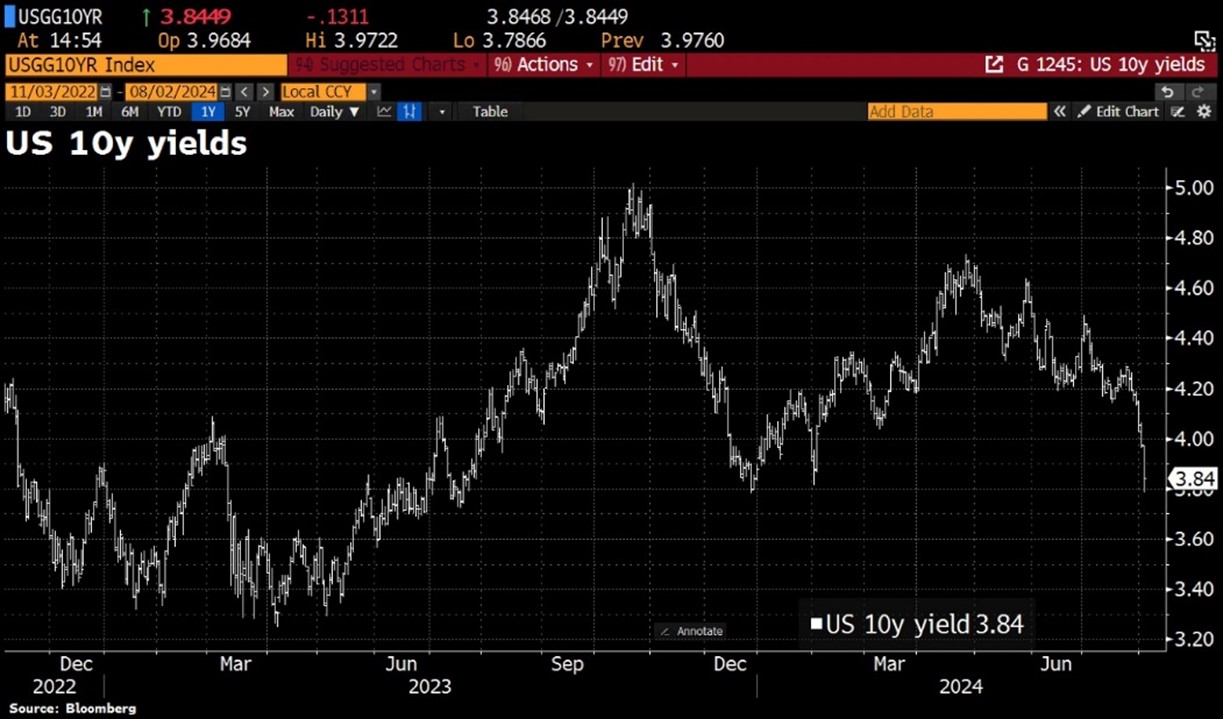

The US 10-year yield has dropped like a stone in recent weeks as a result of everything we mentioned above. Suddenly there is now speculation about a double lowering by the FED in September. As we have written many times before, we believe that there is a real risk that the central banks will once again be too late to react to changes in the underlying economy.

Source: Bloomberg

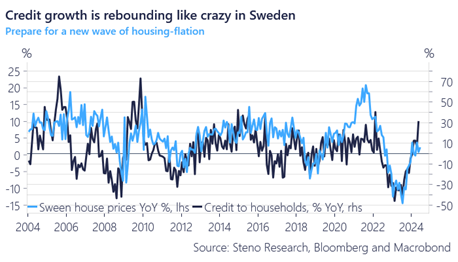

Falling interest rates drive consumption and we are now seeing substantial growth in the demand for credit in Sweden. The below graph shows house prices in relation to demand for credit.

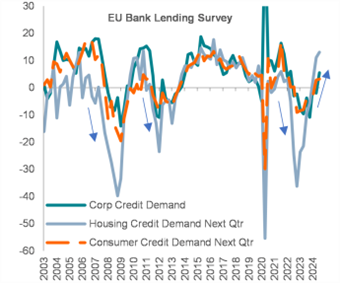

We also see signs of increased economic activity in Europe.

Source: BNP Paribas

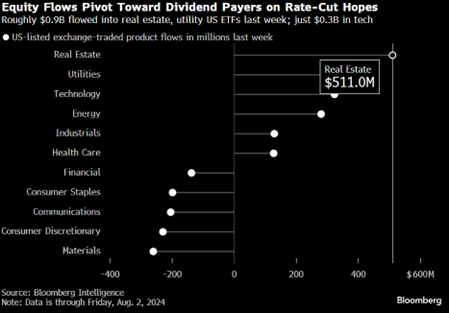

When markets were under pressure last week, the biggest inflows were into real estate funds. The reading below is as of August 2nd.

Source: Bloomberg Intelligence

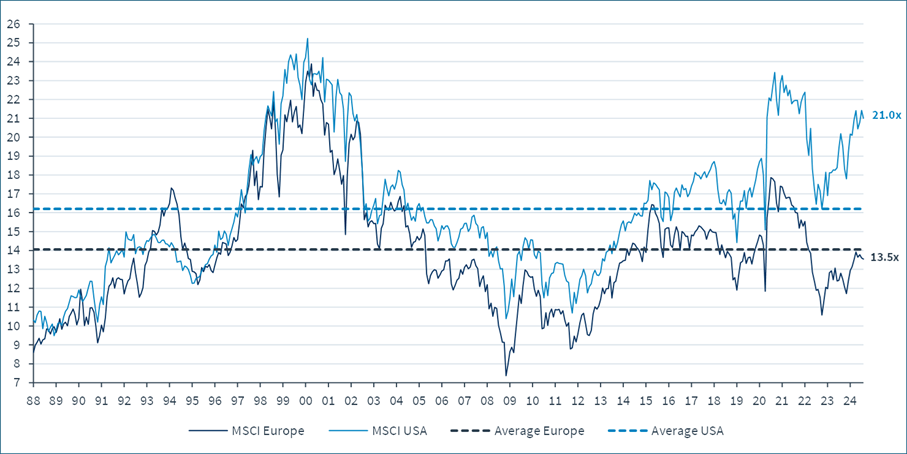

A snapshot of US and European market as of August 2nd. Both stick out, but in different directions.

Source: Kepler Cheuvreux

In summary, we feel that things went downhill very quickly and conclusions that there will be a hard landing in the economy feel very gloomy. There are many things that are starting to change for the better, even if geopolitically right now it looks unusually dark. A major war in the Middle East is the risk we are most concerned about right now.

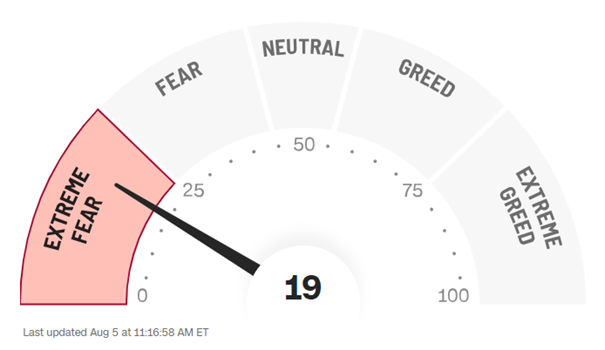

On Wednesday, July 31, a lot of stocks were traded at the highest levels and three days later the panic is in full swing. Not very logical. When CNN's Fear and Greed indicator is down to current levels (extreme fear), it is usually an opportune time to increase exposure. As far as we understand, the biggest selling pressure has come from quant funds and over-leveraged individuals and a smaller part from other institutional capital.

Source: CNN Business

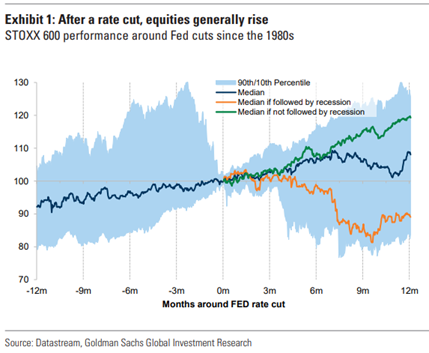

As you know, the stock market has historically developed well after interest rate cuts assuming the economy does not enter a recession, which not our main scenario. Over the weekend, Goldman Sachs increased the probability of a US recession from 15% to 25%. It feels reasonable and balanced and should not prevent an equity investment today (we think). After all, there is always a certain probability of a recession and 25% is still low.

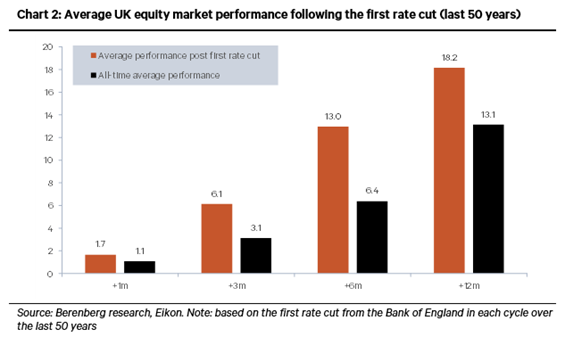

Illustrated differently, but for the UK market only.

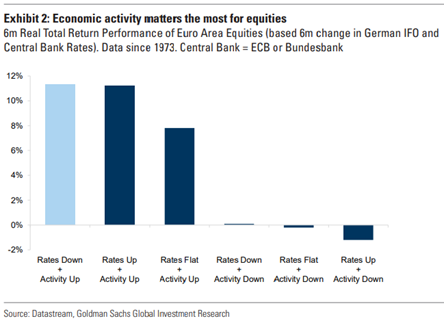

"It's the economy stupid". Below is the historical 6-month development during various economic scenarios. For Europe, our main scenario is the bar on the far left.

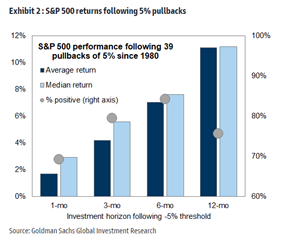

The last picture shows how the S&P500 historically has developed after a 5% decline in the market. It's a pretty clear pattern but remember it's not a linear progression.

We have now basically completed all our company reports and it has been a strong season for us. This means that our position in the current turbulence is good, while we have a modest exposure to purely cyclical companies. We sold our position in Stellantis (cars) in July before the sharp decline in the share price that came after a weak report.

Our property exposure is still around 10%, with Balder also included since some time ago (apart from SLP and Corem). It is a sector that has good prospects of having a strong return during the remainder of the year fueled by upcoming interest rate cuts.

Our belief is that we have a balanced portfolio that works well in both up and down scenarios. Finally, in recent days we have taken advantage of extreme price movements and increased exposure to a few different positions while reducing our position in Commerzbank after a strong development.

We wish you all a nice August and thank you for your interest.

Mikael & Co

Malmö on 13th of August 2024

IMPORTANT INFORMATION. This is a marketing communication. Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested. Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.