This material is marketing communication.

Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class’ return. The information below regarding returns therefore differs from the returns in other share classes.

Before making any final investment decisions, please read the prospectus, its Annual Report, and the KID of the relevant Sub-Fund here.

JULY PERFORMANCE

The fund's value increased by 2.3% in July (share class I SEK), while the benchmark increased by 1.5%. Since the change of the fund's strategy at the beginning of September, 2023, the fund's value has increased by 29.1% compared to an increase of the benchmark by 21.8%.

Source: Coeli European

* Adjusted for spin-off of Rejuveron

** Includes September 1 (strategy change to long-only implemented September 4 2023)

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

EQUITY MARKETS / MACRO ENVIRONMENT

July was as usual a positive month for the world's stock markets. It was a typical summer month that gradually awoke with a multitude of reports accompanied by President Trump's continued tariff play. In total, 67% of the fund's companies (measured in capital) reported in July, and it was another good result, with one exception which we will return to. The SXXP 600 rose by 0.9% in July and the S&P500 by 2.2%.

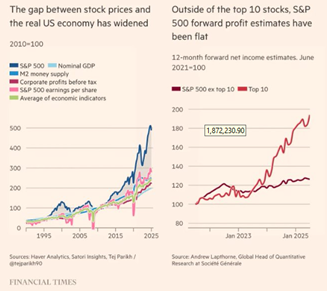

Overall, the reporting season can be summarized with very strong reports from the large US tech companies. Concentration within the S&P500 is once again at an all-time high, with, for example, Nvidia and Microsoft together having a weight of 14% in S&P500. The rise for the S&P 500 in July was therefore largely due to the development of the US tech companies.

Source: HedgeEye

The stock market is not a good reflection of the underlying economy. The dominance of the large US tech companies in the S&P 500 is incredible.

Another thing to keep in mind if you are startled by the resilience of the US stock market is that 81% of GDP comes from the service sector. In the 1940s, it was 38%. The higher the share from the service sector, the smoother the cycle. Household debt is also low. Debt/wealth capital is near record lows and 50% lower than in 2008.

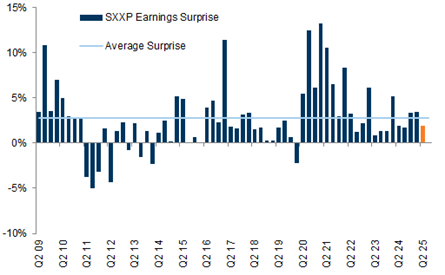

For European companies, the majority have now reported their results, and the outcome of positive surprises is below average.

Source: Goldman Sachs

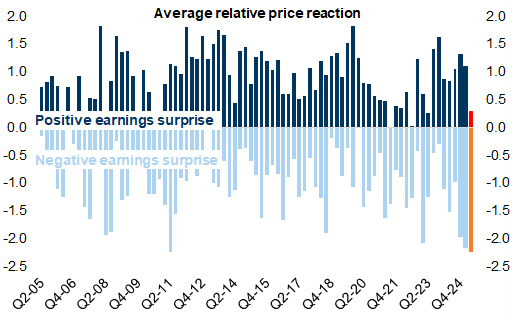

The stock market is meting out the harshest punishment in decades to companies that fall short of earnings estimates (according to Goldman Sachs). Many companies reported a weaker start and stronger end to the quarter due to all the turbulence with tariffs. Banks continue to report strong results and have not been in better shape since before the financial crisis. Construction companies are starting to become cautiously optimistic, but unfortunately Germany and Sweden are lagging most other European countries in activity.

Source: Goldman Sachs

There were intensive negotiations between the EU and the US administration to reach an agreement in early July. Reportedly, things were going well, but on Saturday, July 12, President Trump (yes, it's a one-man show) sent a letter to the EU saying he wanted 30% tariffs. The disappointment among the EU negotiators was palpable, and rightly so. Two weeks later, they agreed on tariffs equivalent to 15% for around 70% of exports from the EU to the US. American goods imported into Europe have no tariffs. Many details remain, but many of us were surprised by the one-sidedness of the agreement. It feels like the EU has bowed down to the autocrat on the other side of the Atlantic. Exports in the US account for 11% of GDP. For the UK and Germany, they are 31 and 42%, respectively.

It will be interesting to follow the development of the US economy. As this is being written, news is coming out on Bloomberg about American investment banks losing business in Europe as the turmoil from the American administration has scared away clients. Who is surprised? Euronext's colorful CEO rants a bit during his speech in connection with their quarterly report and thinks the US is increasingly starting to resemble an emerging market.

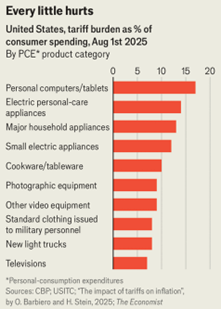

The Economist has analyzed the impact on prices of various products in the United States once all tariffs have been implemented. Even if consumers choose American products, the price may have risen because there are foreign components in the product. When prices rise, it reduces the purchasing power of the American consumer, which is unlikely to be appreciated. Of course, it also affects the production levels of non-US companies.

Source: CBP, USITC, The Economist

Below are the current tariff levels, which can of course change at any time depending on President Trump's mood. The Swiss were completely taken aback when they received word on the evening of July 31 that President Trump had decided to increase tariffs to 39%. That's the fourth highest tariff rate in the world after Syria, Laos, and Myanmar. The following day, Switzerland celebrated its national day. How is it possible to behave so badly? The Swiss newspaper Blick calls it the biggest defeat since the Battle of Marignano in 1515, when French troops defeated Swiss troops in their attempt to control parts of northern Italy.

Chinese and American delegations met in Stockholm at the end of July to try to make progress in their tariff discussions. The meeting was described as somewhat positive, and the date was moved forward to continue discussions.

Source: Fitch, White House, The Economist

An important data point that is likely related to the chaos left behind by the US administration is the jobs report that came out on Friday, August 1st, which showed significantly fewer new jobs created. It was primarily substantial downward revisions to the data from recent months that caused interest rates to fall sharply in line with falling stock prices. It seems obvious that some of the downward revisions are due to the extremely high uncertainty among companies. Companies are holding off on investment decisions, including new hires. We are hearing the same from our own companies.

The big leader's response to the report was to immediately fire the manager and those responsible for labor market statistics. “The data had been RIGGED in order to make Republicans and ME, look bad". Apart from today's high levels of tariffs, you don't have to be too well-versed in history to see the parallels with times gone by.

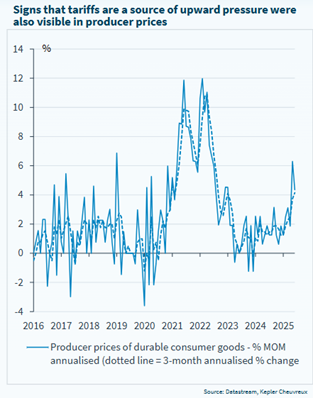

Producer prices in the US have begun to rise and tariffs have likely had some effect.

Source: Kepler Cheuvreux

The admiration for the great leader took on new expression when those closest to the administration now think that Trump should receive the Nobel Prize in Economics. https://x.com/carlbildt/status/1950997611676311880?s=12&t=0N7sZrq39DU5Tq-Zr-TWaQ

At the same time, the White House spokesperson listed all the conflicts that Trump has ended, which makes him a given winner of the Nobel Peace Prize.

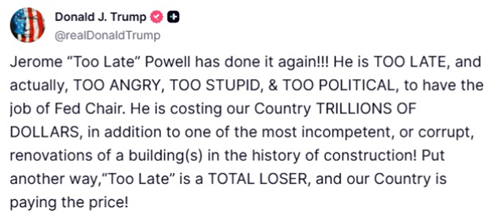

The highlight of the month with a high entertainment value was still Trump's visit to the Fed, which is undergoing an extensive renovation of their premises. A renovation that the American president thinks costs too much and reflects their economic ignorance. You must watch this clip if you haven't already. Someone wrote that it's like it was taken from The Office. https://www.youtube.com/watch?v=woaa3pEzIHM

Trump was not happy with Jerome Powell's performance afterwards and when the interest rate was not lowered this time either, the response was swift.

Source: TruthSocial

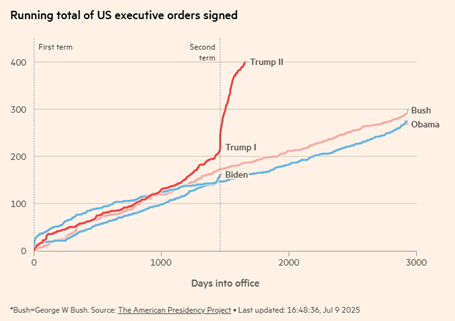

Regardless of what you think of the politics, he is, at least, productive.

Source: The American Presidency Project

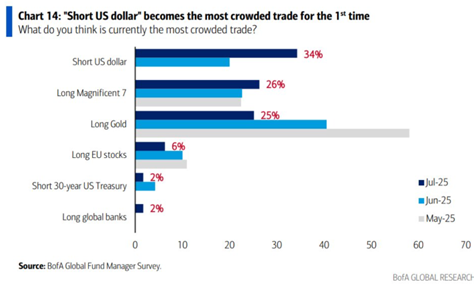

All the above has led to the latest survey of Bank of America institutional clients showing that negative positions against the US dollar is the largest crowded trade in the market. Note the increase in recent months. Long positions in gold have declined sharply in line with increased risk appetite. The level of capital invested in European equities also appears to have declined.

Soure: BofA

All the turbulence has led to the euro strengthening against the dollar by just over 10% to around 1.16. That is a significant weakening of the dollar in a short period of time, but those with good memories will remember that it is a long way from old levels.

Source: Bloomberg

As expected, the ECB kept the key interest rate unchanged after the end of its meeting in July. The economies in the eurozone have shown some resilience, but growth remains modest. Among the larger economies, Spain continues to lag with +2.8% in GDP growth. But there is reason to be optimistic. Huge infrastructure projects will start soon, Germany will come with fiscal stimulus and of course the huge investments in defense. Below is a picture from Austrian Palfinger (crane manufacturer and partly a competitor to Hiab) that sums up the situation well. Europe has not seen anything like this since after the Second World War.

Source: Palfinger

But to put things into perspective, Nvidia will soon have a market capitalization equivalent to the 50 largest companies in Europe. It's almost hard to fathom.

Source: Bloomberg

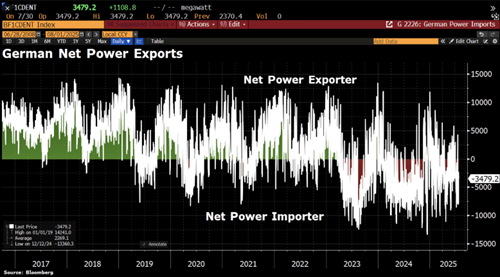

Europe's energy policy, and Germany's in particular, leaves a lot to be desired. The picture below shows how Germany has gone from being a net exporter of electricity to a net importer. Due to an unimaginably lousy electricity transfer system, the whole of southern Sweden is also feeling the effects of this, with energy prices that are often 10x higher than in northern Sweden (where they also have lower taxes than in southern Sweden). Given the sharply increasing consumption of electricity for the use of AI technology, it feels challenging to say the least for some European countries to keep up with the development. Soon we will be able to read: "We didn't see it coming".

Source: Bloomberg, Holger Zschaepitz

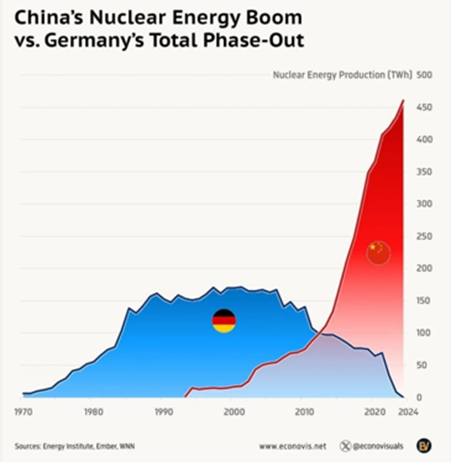

A dismal record that is hard to beat. Sweden also boasts far-reaching rankings in the field.

Source: Energy Institute, Ember, WNN

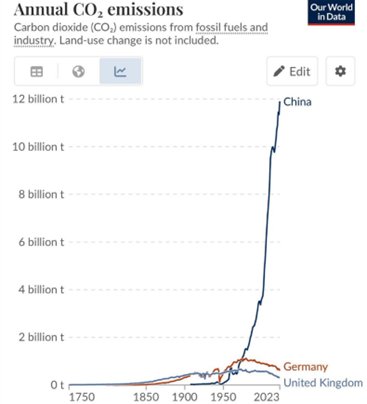

How much have Europe and its citizens had to pay in terms of lost competitiveness due to the energy policy pursued? This is not to say that China and the US are without fault, but the price for European citizens has been high.

Source: Our world in data

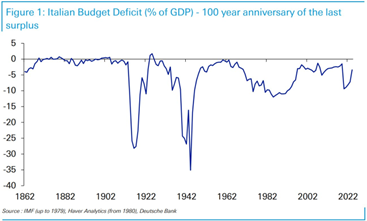

Were you at the party? This year, Italy celebrates the 100th anniversary of its last budget surplus. Despite this, Italy is now experiencing a rare political and financial stability led by Giorgia Meloni. She has been in power for just under three years, which is almost a new record. In the last 164 years, Italy has had 133 governments. The country's national debt reached a peak during the pandemic of 158% but is now down to 135%.

Source: IMF, Deutsche Bank

PORTFOLIO COMPANIES

Konecranes

Konecranes reported results that were markedly better than expected. Order intake and operating profit were around 11–12% higher than analysts' estimates. At the same time, profitability remained at an unchanged high level, despite the company previously stating that the margin in the corresponding quarter last year was unusually strong. So far, Konecranes seems to have brushed aside most of the clouds of concern that loomed in the form of tariffs and their impact on both costs and demand.

Although US tariffs are bad for Konecranes (the company has relatively little production in the country), the company does not seem to be a major relative loser given that many competitors seem to have similar value chains. In addition, the tariffs are expected to create changed logistics flows over time, which in that case should benefit demand to some extent. At the same time, European purchasing indices have risen for several months in a row and in July reached their highest level since July 2022.

Our estimates suggest that Konecranes continues to trade at single-digit EV/EBITA multiples, despite the return on capital employed, as defined by us, rising from around 17% in 2019 to more than 30% in 2025. We estimate that around 65–70% of operating profit will come from more stable aftersales revenue. The company has now performed well through several years of macroeconomic turbulence and we believe it is time for a solid share appreciation. The share rose 9% in July.

De’Longhi

The Italian manufacturer of predominantly coffee machines has had a mediocre year in terms of price (-5%). However, operations continue to perform well despite the stock market's doubts regarding tariffs and American demand. De'Longhi's report for the second quarter of 2025 was around 3% better than analysts had expected. The guidance for the full-year result was adjusted upwards. Organic growth for the first half of the year is summed up to 8%, while the operating margin has risen by around 80 basis points.

De'Longhi has a long history of good organic growth. The share is valued at analysts' estimates of EV/EBIT 8-9x for the next 12 months. These can be compared with a historical ten-year average of 12x. Evidently the share is being punished for its production exposure (exclusively Chinese and European), which, combined with an American sales share of around 20%, has scared the market. At the same time, the company's management does not seem particularly worried about the tariffs that have now been announced.

We see the stock as clearly undervalued. If the company can prove that it can handle the second half of the year without a greater impact from the tariffs than expected, the stock should get a boost. The consumer sector has had a couple of frosty years on the stock market and at some point, things should turn around. With lower interest rates and larger European wallets, there should be conditions for that to happen soon. When things do turn around, you probably want to own the best consumer stocks, and we place De’Longhi in that compartment. The stock rose by 1% in July.

Alm. Brand

As we have written about in several previous monthly letters, we have liked the Nordic insurance sector for a long time – and perhaps especially this year. Insurance premiums are now increasing at a faster rate than costs, which is a good tailwind for margins. So far this year, insurance companies have also benefited from relatively mild weather.

During the first half of the year, we have slowly shifted parts of our Sampo holding to Danish Alm. Brand. Alm. Brand is fully focused on the Danish market and will soon complete a lengthy integration process of the Danish Codan, which was acquired several years ago. The Codan acquisition was not well received by the market due to a high price tag. However, the industrial logic follows one we have seen in many other cases in the Nordic insurance market: Scale is vital for your profitability. We believe that the market will soon discern the contours of "Alm. Brand 2.0", which we believe is a clearly better company than "Alm. Brand 1.0". Not least with the help of a capital markets day this autumn.

During the month, Alm. Brand also released a nice quarterly report that was better than analysts' estimates. The growth of 11% in the private segment stood out. Of that growth, 4 percentage points came from market share gains, according to the company, which we see as a sign of strength. Overall, the report was free of major question marks in our opinion. Alm. Brand rose by 7% in July. Together with our holding in Sampo, the Nordic insurance sector constitutes just over five percent of the fund's exposure.

Lindab

The ventilation company continues to try to fend off tough end markets. The report for the second quarter was certainly in line with analysts' estimates - but these had been adjusted downwards close to the report release. The positive thing about the report was that the most valuable segment "Ventilation Systems" performed well given the conditions. At the same time, the more volatile segment, "Profile Systems", was worse than we forecasted.

Our investment thesis is mainly based around the expectation that the large investment program that CEO, Ola Ringdahl, has been implementing for many years will bear fruit as the company's volumes increase again. Margins should rise significantly on the back of that. When volumes will return is difficult to predict, but lower interest rates in Europe should certainly create the conditions for that. Perhaps the large German stimulus package can also have a positive impact from 2026. Lindab shares rose by 5% in July.

Volution

This ventilation company has been one of the fund's largest holdings for a long time. The half-year report illustrates why: Despite tough end-markets, the company's organic growth increased to more than 6% during the second part of the financial year ending in July 2025. This is an increase from around 4% in the first half of the year. The integration of the large Australian acquisition that was completed at the end of last year seems to be going very well. Earnings per share are expected to grow a little over 15%.

Volution shares rose by 13% in July and had thus risen 20% in 2025. This comes on top of a price development of 29% in 2024. Despite the good price development, we think there is plenty of upside left. The share is trading at around EV/EBITA 12x on our estimates for 2027.

Diploma

The British serial acquirer continues to impress. When the company released its third-quarter report for the financial year ending in September, it was (as usual) with a positive message. The company is now guiding for organic growth of around 10%, up from 8% previously. In addition, it announced several smaller acquisitions. Acquisitions, in particular, have been long-awaited after a period of slower development in that regard. The share rose by 10% in July. The company's valuation is starting to strain, and we have therefore reduced our position.

Hiab

Hiab continues to impress as an independent company. Adjusted operating profit was around 11% better than expected, which sent the share up almost 11% on the reporting day. The company delivered a somewhat fantastic 16.2% operating margin, despite production volumes remaining depressed. Order intake was also better than analysts expected and grew almost 9% compared to last year. Europe is the main driver. We continue to hear positive sentiments about Europe, and it finally feels like things are starting to move.

Hiab's long-term financial target is to have an operating margin of 16% by 2028, something we believe the company will reach already next year. Over time, we believe that Hiab will become a Nordic favorite that deserves a higher multiple given how well they perform. The share rose just over 16% during July.

Bonesupport

Bonesupport reported in line with expectations. The stock has been weak during the spring, and we have increased our holdings. Sales grew organically by 40%. Easter negatively impacted growth by 3–4 percentage points. In the first quarter, the stock was penalized by currency headwinds, but the market looked past this in the current quarter.

The company also mentioned that it expects an acceleration in sales growth for Cerament G in the U.S., which seems reasonable given that it has been nearly a year since the launch of Cerament G for trauma. In the fourth quarter, Cerament BVF will be launched for spinal applications, and based on our understanding, the study data looks promising. We expect to receive more information on this during the autumn. We also anticipate updates on the pathway for Cerament G to be used in spinal applications.

With the second-quarter report, an era ends with Emil Billbäck stepping down as CEO. We will miss seeing him in the spotlight but are pleased that he will remain with the company. It has been a truly phenomenal journey under his leadership. We have not yet met the incoming CEO, Torbjörn Sköld, who most recently comes from Stille, but we have heard positive things about him. The stock rose 18% in July.

Kalmar

Kalmar delivered a very strong report. Order intake was 16% above expectations, and operating profit exceeded forecasts by 5%. Unfortunately, the initial share price increase was erased after the management team flagged a weaker outlook for the U.S. in the second half of 2025 during the earnings call. Kalmar has posted very strong order intake in recent quarters, which has been reflected in the share price, up 25% this year. After having met the management, we believe they may be overly cautious.

Kalmar has received a well-deserved revaluation this year and, based on our estimates, is trading at approximately EV/EBIT 10x. The stock rose 10% in July.

Vallourec

Vallourec delivered a low-key report for the second quarter. Operating profit was in line with expectations, and the forecast for a strong second half matched analysts’ expectations. Outside the U.S., Vallourec has seen high activity and secured several large orders in the first half, reinforcing the outlook for a stronger second half. The stock rose 4% in July and is trading at approximately P/E 9x for 2026 based on our estimates.

HBX

The fund’s major disappointment in the second quarter was HBX. The third quarter came in about 5% below expectations. What the market reacted to most was the downgrade in the company’s outlook. Assuming the midpoint of the new guidance range, total transaction value and revenue were revised down by 5% and 3% respectively, while EBITDA remained unchanged. This triggered panic in the market, leading to a 20% drop in the stock during July. We have reduced our position.

Both data and peer reports pointed to strong travel activity in Europe, but unfortunately, this was not the case for HBX. In turbulent times, travelers tend to downgrade, take shorter trips, and book later. This leads to more bookings directly through hotels or OTAs (Expedia, Booking.com). HBX’s strength lies in transcontinental travel booked well in advance. Given the strong data we had going into the report, we likely wouldn’t have done anything differently, but we clearly underestimated how affected HBX would be.

SLP

SLP continues to perform well, and the second-quarter report was no exception—fully in line with expectations. Looking ahead, the interest rate environment should benefit real estate companies in general, and perhaps SLP in particular. When rate hikes began in 2022, SLP’s yield requirement rose from 5.2% to 5.9%. Since May 2024, the Riksbank (Swedish Central Bank) has made seven rate cuts, from 4% to 2%, with another expected this autumn. Despite this, SLP’s yield requirement remains at 5.9%. One reason may be that SLP itself acquires properties with yield requirements above 6%. The company is highly acquisitive and plays a significant role in the transactions used by valuation institutes. Unlike two or three years ago, SLP’s portfolio today is of significantly higher quality, which should contribute to lower yield requirements, all else being equal.

Based on current earnings capacity, SLP is valued at 18x free cash flow, which we consider relatively inexpensive given its growth prospects. If we assume a 50 basis point reduction in the yield requirement, this would generate an increase in NAV of SEK 1.5 billion, or nearly SEK 6 per share. It does not seem unreasonable for this to occur within the next 12 months, given that the reference rate (STIBOR) has moved from 4 to 2%.

Scandic Hotels Group

Scandic delivered a report that was weaker than expected. EBITDA was about 7% below forecasts, largely due to tough comparables (last year included events like Taylor Swift). Booking levels for the third quarter suggest slightly higher occupancy and pricing compared to the previous year.

The major event in connection with the report was Scandic’s announcement of its intention to acquire Dalata Hotel Group’s hotel operations from Pandox and Eiendomsspar as part of their public bid. The acquisition increases the number of rooms by 20% and establishes Scandic in Ireland and the UK. Our view is that Dalata is very well-managed and shares many similarities with Scandic, with a dominant position in Ireland. The deal is expected to contribute positively to EPS immediately after completion. We believe Dalata could add as much as 20% to earnings per share.

Scandic’s stock was unchanged for the month, and we anticipate some changes in the shareholder base as the company transitions from a “dividend stock” to a “growth stock.” Once the acquisition is consolidated, we believe the market will appreciate the EPS growth.

SUMMARY

We are pleased with the delivery from our companies during the first half of the year. The development of the fund in July was good and was driven by the quarterly reports. In addition, we have had a good balance in the portfolio in recent months. August and September tend to be weaker stock market periods with higher volatility as a large part of the world's managers are on holiday. In addition, we all now have an American administration that increases volatility and makes it rather pointless to predict the nearest development. Below the historic volatility for the past year.

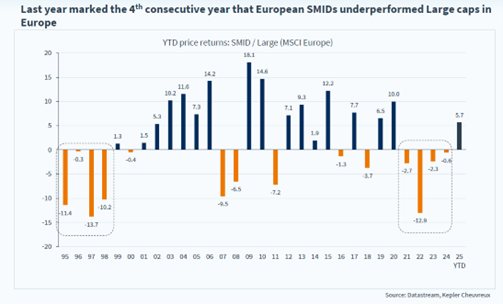

What is now clear, for the first time since 2021, is that European small companies (SMID) are in favour and showing a stronger price development than larger companies. It is a development that, all other things being equal, benefits our investment philosophy. It is also evident that a corresponding development does not exist in America, which is mainly due to the complete dominance of the large tech companies. The interest rate level in the US is also more than twice as high as in Europe.

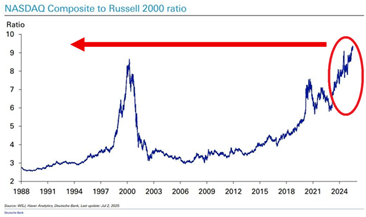

In the US, Nasdaq has never had such a strong excess return compared to smaller companies.

Source: WSJ, Haver Analytics, Deutsche Bank

An important image for understanding the stock market's development in 2025.

Source: Bloomberg

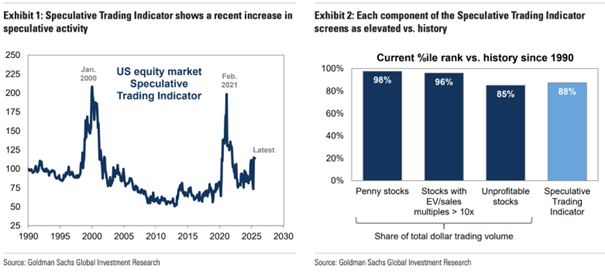

Goldman Sachs is raising a warning finger against all speculation among American retail savers. They see clear parallels from the dotcom euphoria of 1999–2000 and the meme madness of 2020–2021, and their speculative indicator is rising.

Source: Goldman Sachs

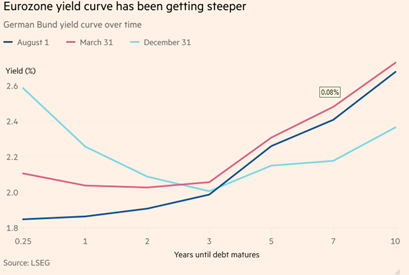

The performance of European banks has been exceptionally strong in recent years. It took the sector 15 years to recover from the 2008 financial crisis, and banks were a major contributor to many of Europe’s post-crisis challenges. However, they are now back—and in a big way. For the fifth year in a row, banking is the best sector in Europe. The ECB had its annual stress test a few days ago and for many years this was a major nervous event where the weakest were singled out, resulting in new price pressure. This time it was a non-event, and the sector continued its strong development the next day. Banks are currently operating in an ideal environment. With a rising interest rate curve in Europe and massive defense and infrastructure investments underway, banks are expected to maintain strong earnings. The fund has just over 5 percent exposure to the banking sector through Commerzbank and Bawag.

Source: LSEG

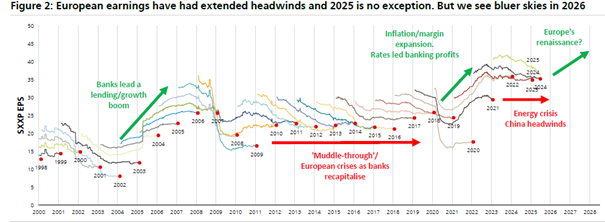

The picture shows Europe's economic profit development over the last 25 years, where the imprint from the banks left its mark. The outlook brightens in 2026.

Source: UBS

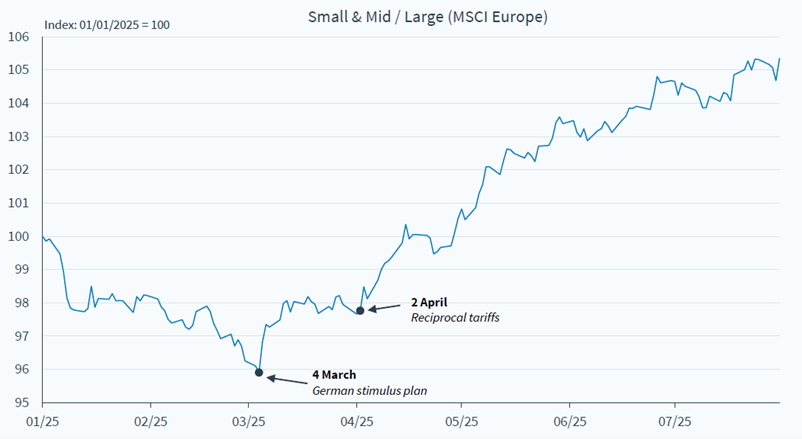

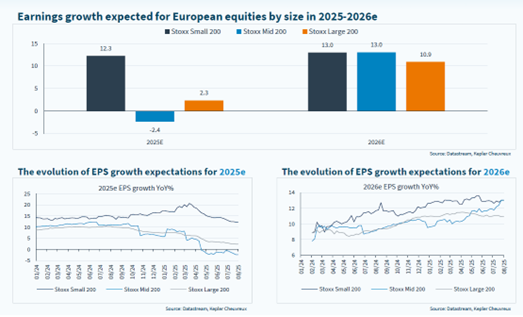

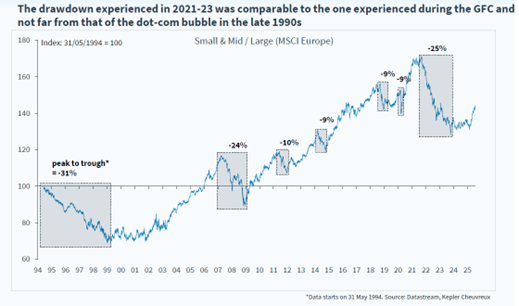

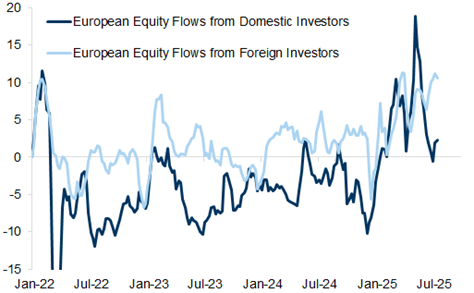

Below is a collection of excellent charts that clearly illustrate the renaissance currently underway among European small-cap companies. There are many indicators suggesting that this trend could continue for a long time. A big thank you to Joakim Tabet at Kepler Cheuvreux, who kindly prepared the charts for us during his vacation.

The first catalyst for SMID outperformance was the announcement of Germany’s defense plan in March, and the second came on April 2nd with Trump’s tariffs.

Source: Kepler Cheuvreux

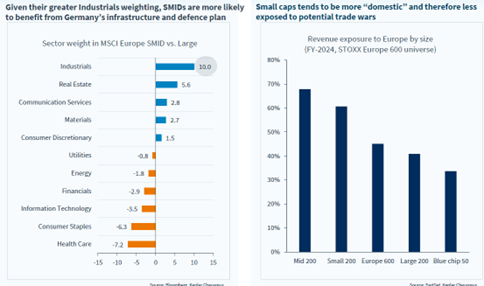

A large weight of industrials within SMID and a lower impact of tariffs contribute positively to strong performance.

Source: Kepler Cheuvreux

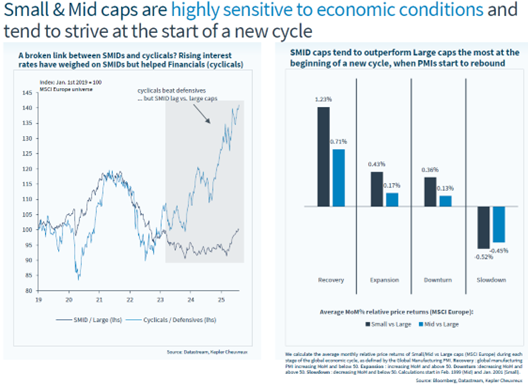

Smaller companies are more sensitive to general economic developments and tend to perform stronger than larger companies when economic activity increases.

Source: Kepler Cheuvreux

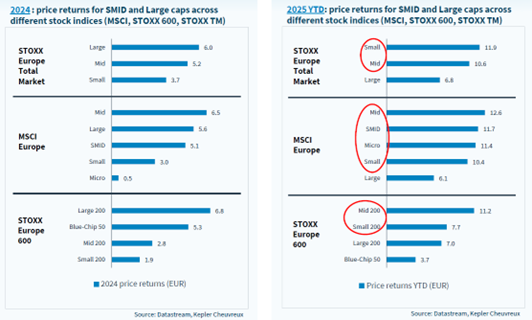

The development in 2025 is a mirror image of 2024.

Source: Kepler Cheuvreux

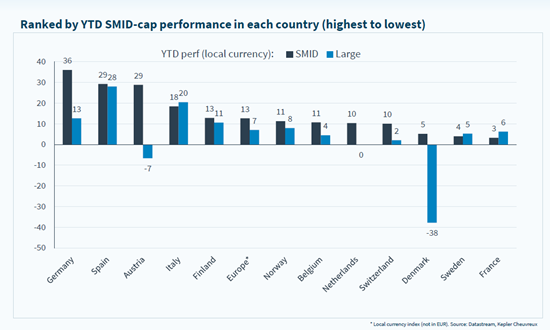

German and Spanish small-caps are at the top this year. The UK is not included here, but small-caps there have performed worse than large-caps so far this year, which also applies to Sweden. The fund has approximately 45% of its capital in these two countries.

Source: Kepler Cheuvreux

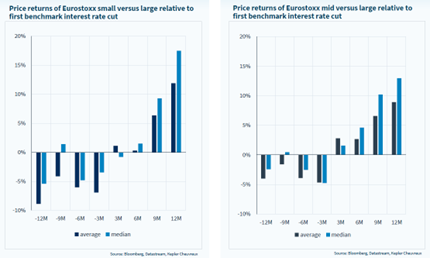

A clear picture showing the interest rate sensitivity of SMID.

Source: Kepler Cheuvreux

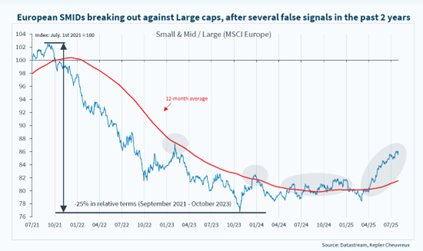

It's happening now.

Source: Kepler Cheuvreux

Those who are good at technical analysis confirm the picture.

Source: Kepler Cheuvreux

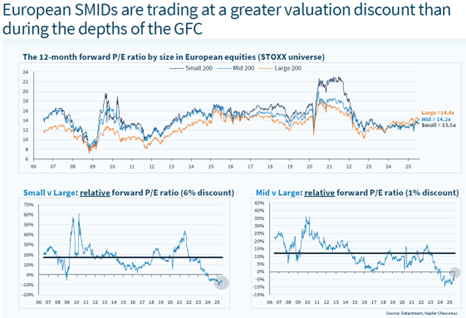

The valuation of SMIDs is at a lower relative level than during the global financial crisis, which feels strange.

Source: Kepler Cheuvreux

There's nothing wrong with growth either.

Source: Kepler Cheuvreux

We have mentioned several times that the current climate feels a bit like 2002, a period where major problems were dealt with, but which was then followed by several strong years for stock picking and SMIDs. We continue to have that feeling.

Source: Kepler Cheuvreux

Another good picture showing the development over 30 years.

Source: Kepler Cheuvreux

In summary, the outlook for European small and mid-cap companies appears unusually strong. Many investors remain underweight in this segment. As we write these final words, we also note that global hedge fund investors are preparing to “load up on Europe.” According to Goldman Sachs, Europe is expected to be the primary geographic focus for the second half of the year. We are not surprised—and they are welcome. Earnings growth in Europe and the U.S. is approximately 11% and 12%, respectively. Europe is trading at 14x earnings, while the U.S. is at 23x, and the dollar is currently not the most comfortable currency to hold.’

European investors are now returning as buyers after having sold for most of the year.

Source: Goldman Sachs

One should be prepared for some volatility ahead, primarily driven by the U.S. administration. In Europe, we now believe we understand the rules of the game (though nothing is ever certain), and we will adapt accordingly. The uncertainty that has cast a shadow over many decisions has now lifted.

In the U.S., we expect some upward pressure on inflation as prices begin to rise after the summer. If not sooner, then next year the U.S. Federal Reserve will likely have a new chair who will align closely with President Trump, push up long-term interest rates, and trigger new shockwaves through the system—then the circus will start all over again. But that’s not something we need to dwell on right now.

Thank you for your interest and have a wonderful August!

Mikael & Team

Malmö, 7th of August 2025

IMPORTANT INFORMATION. This is a marketing communication. Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested. Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.