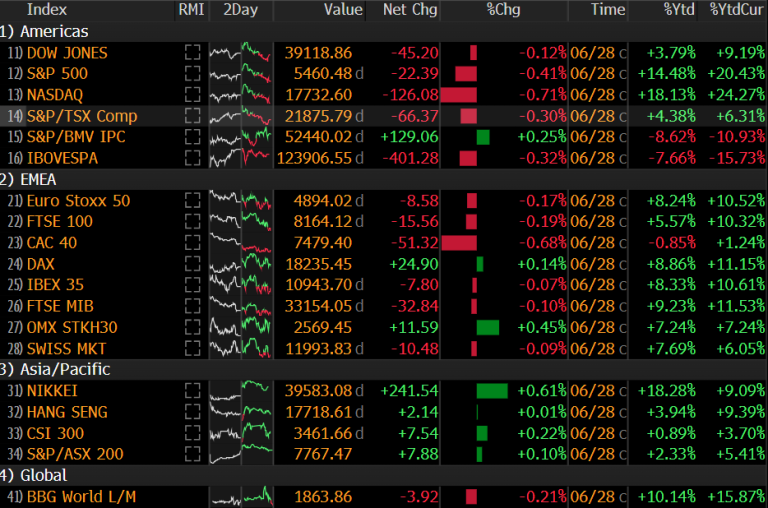

Monthly Newsletter Coeli European – June 2024

This material is marketing communication.

Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class’ return. The information below regarding returns therefore differs from the returns in other share classes.

Before making any final investment decisions, please read the prospectus, its Annual Report, and the KID of the relevant Sub-Fund here.

June Performance

The fund’s value decreased by 4.1% in June (share class I SEK), while the benchmark decreased by 3.6%. Since the change of the fund’s strategy at the beginning of September this year, the fund’s value has increased by 16.7% compared to an increase of the benchmark by 6%.

Source: Coeli European

* Adjusted for spin-off of Rejuveron

** Includes September 1 (strategy change to long-only implemented September 4 2023)

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

Equity Markets / Macro Enviroment

The big loser of the month was the French stock market, which fell by 6.4%, and in the middle of the month we experienced the worst stock market days since October last year. The fund’s three best contributors were BoneSupport, Scandic Hotels and the London Stock Exchange. The three worst were Biotage, 4imprint and Syensqo.

The reason for the negative development was the unexpected political turmoil that arose in France, when President Macron, due to his weak result in the EU elections, immediately on Sunday evening, June 9th, called for new elections. Macron’s own party got only 14.6% compared to the right-wing nationalist National Assembly which got 31.4%. It may be considered high stakes by Macron but must be set against the background that he failed to get majority in the last election, in 2022, and thus found it difficult to implement laws and reforms in the country. Rumor has it that Macron has been considering new elections for several months, but that it was put on hold due to preparations for the Paris Olympics, which are about to start. It’s starting to look brown, to say the least, in France, picture below.

Source: Le Monde

What was remarkable in June was that for only a few weeks the difference in returns between Europe and the US was massive in favor of the US, see image below for June’s returns. The weakest development was in France, and it is unusual for political developments to have such a large impact on the financial markets as it did this time. The second to last column shows developments in local currency and the last column measured in Swedish kronor.

Source: Bloomberg

The corresponding picture for the first half of the year can be seen below. European small and mid-caps rose by just over 5% and the Russell 2000 in the US rose by 1%. Also note that the Dow Jones, which contains significantly fewer technology companies than the S&P500, rose 3.8%. The OMX30 rose by 7.2%.

Source: Bloomberg

The reason European stocks came under pressure after Macron’s maneuver is that investors see a risk that party leader Marine Le Pen promises too much if she wins the election and there will be a “Liz Truss event” like in the fall of 2022. A string of unfunded tax cuts created significant turbulence for a few weeks at that time. We’re not experts in the field, but our humble view is that the most radical proposals are unlikely to pass, and a political compromise (again and hopefully) will be reached. We will know more after July 7th and Macron himself remains president until 2027.

Another issue is how France’s security policy might change with a Putin friendly in the form of Le Pen as leader of France’s largest party. Another close friend of Putin, Viktor Orbán takes over the presidency of the EU on July 1st. In the British election which takes place on July 4th, Nigel Farage and his Reform party are on the rise. It is rumored that he can get up to 15% of the vote. Last weekend, Farage said it was the West that forced Russia to attack Ukraine. And Donald Trump right now looks set to sweep the floor with President Joe Biden. Mon dieu! A sad parenthesis is that democracy is declining for the 18th year in a row and only 8% of the world’s citizens currently live in a full-fledged democracy.

In contrast to Sweden, where SD (far right party) retreated significantly, the right gained ground in many parts of Europe. The picture below gives a razor-sharp description of a divided Germany. In the old East, the right-wing populist and nationalist AfD, Alternative fur Deutschland, dominates. A personal reflection is that it feels familiar from ancient times and that is not a generally great feeling.

Source: Suddeutsche Zeitung

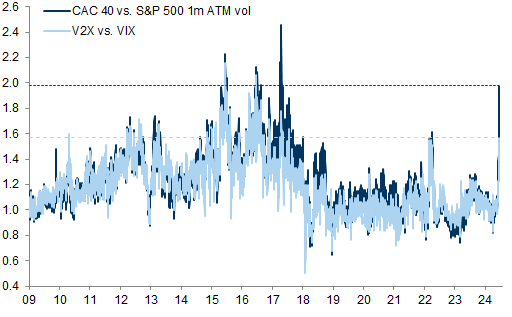

Below is a picture illustrating the European stock market volatility compared to the American one. The difference between the two markets reached almost the same levels in June as we had during the debt crisis just under 10 years ago.

Source: Goldman Sachs

Apart from a slightly unrulier market than usual in Europe, the US development in June was the calmest since 2017. The largest one-day decline for the S&P500 in June was -0.31%. According to Goldman Sachs, when measured as the “smallest worst decline” in a month, it was the fifth smallest since 1928. Ranked at number 5 out of 1146 months! US investors apparently see no risks and are riding on the AI boom.

With the exception of France, it has been quieter in the European fixed income market. After June 9, French government bond spreads have widened compared to other countries, while spreads for Italian government bonds (BTP) and the corresponding Spanish (Bonos) barely moved, which is of course very positive.

We also received positive news when US inflation was communicated on the 12th of June. For the first time since October 2023, core inflation came in lower than expected. This led to interest rates falling across the board and stock markets rising. Small caps rose upwards of 2x more than the major broad indices that day, exactly as by the book.

Source: HEDGEYE

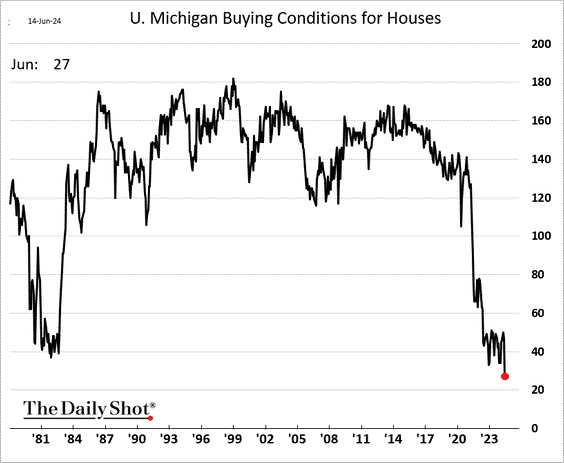

You have to give the Fed credit for cooling the conditions for American homebuyers. The worst conditions in the last 45 years, while at the same time the savings capital that was built up during the pandemic has now been consumed.

Source: The Daily Shot

Sveriges Riksbank (Swedish Central Bank), disappointed few when on June 27th it left the interest rate unchanged and paved way for three interest rate cuts this autumn compared to the previously announced two. A weak labor market and stronger krona helped, but decisive for the adjusted view is an expected lower inflation. The Riksbank believes inflation will rise 2% this year and 1.8% next year. Finance Minister, Elisabeth Svantesson, is confident of victory and believes that the fight against inflation has been won and now there will be a more expansive policy with significant investments underway. With large maintenance debts in infrastructure, it is welcome to say the least. Sweden is now gearing up and the prospects look better than for a long time, something that we don’t think the international capital has noticed yet.

Source: Consensus Economics

At the time of writing, it is hours after the first debate in the US presidential election between challenger Donald Trump and incumbent President Joe Biden. Or put another way, the choice between a criminally charged individual and a clearly demented person. These are the two people left to represent the world’s most powerful country. When they start arguing who is the best at golf you don’t know whether to laugh or cry, watch the surreal clip and say a silent prayer they have very good advisors around them: https://www.youtube.com/watch? v=Re2kZfoyo7g

Some things were better in the past: You’ll likely be in a better mood after watching the following clip of Ronald Reagan when his mental health is in question. The situation then feels far off from today’s.

Source: X

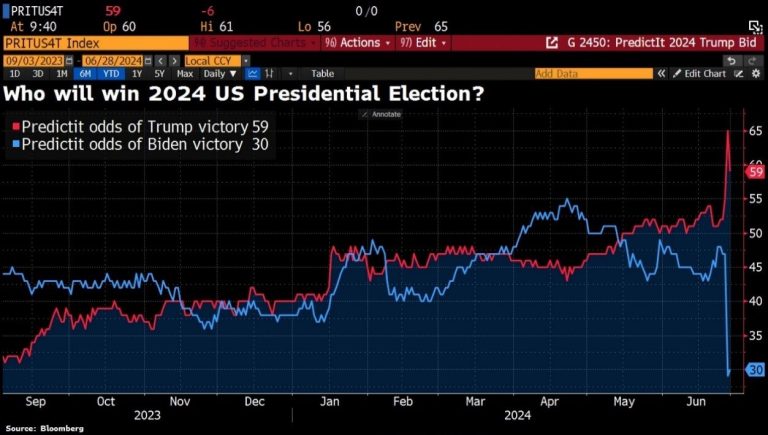

CNN reports from reliable Democratic sources that they later stated: “we have a problem”. The picture below says it all and the coming weeks will be decisive if President Biden throws in the towel and the Democrats run with a new candidate. For those who watched the sad event, it feels like a foregone conclusion.

Source: Bloomberg, Goldman Sachs

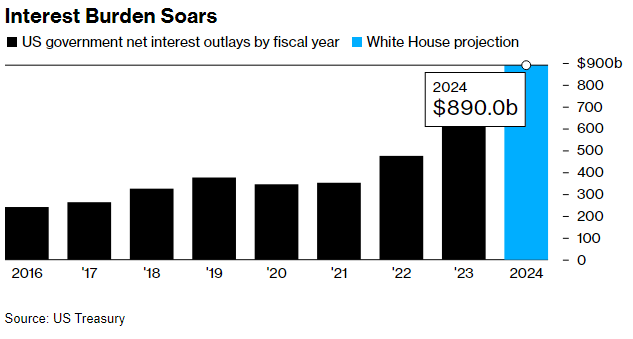

Something is likely to break. The US government’s interest payments are now up to three percent of GDP, which is even higher than during World War II. It is also more than the entire US defense budget. That, combined with Trump possibly taking over the presidency with subsequent tax cuts, means that some forecasters are counting on a severely weakened dollar next year. To be continued.

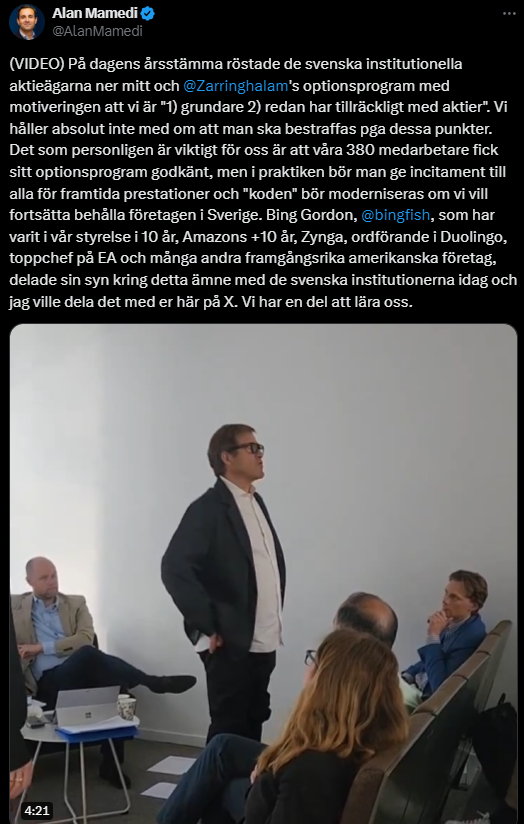

On the topic of doing the right thing. We are attaching a clip from Truecaller’s annual general meeting where new option packages were discussed. Large Swedish well-known institutions seriously thought that the two founders, Alan Mamedi and Nami Zarringhalam, should be excluded from new options since they already had so much stock. An extremely strange act that clearly has socialist features and the world’s most anxious country shows a less flattering side. It is most likely the same people who a few years ago said blindly no to investing in the defense industry. Thankfully, they were politely lectured by Bing Gordon representing Kleiner Perkins. For those of you not familiar with Kleiner Perkins, it is one of the most prestigious VC firms in Silicon Valley and they have been invested in Truecaller since 2014, so some more weight and experience behind his words.

Source: X

Finally, on June 6th, Europe widely celebrated the 80th anniversary of Operation Overlord. The brave men who gave their lives for us who came after cannot be thanked enough. It broke Hitler’s army and pushed the Russian borders to the east, which then created the Europe we all grew up in. That we now have war again is completely unimaginable and, as usual, it is a crazy man who is behind it. To all EU and NATO opponents, a trip to the American cemetery in Normandy is recommended.

Source: X

Turn up the volume!

Source: X

Portfolio Companies

Cargotec / Kalmar

There has been no significant news from our companies in June and most market participants are consolidating positions after an intense first half of the year. That, in combination with holiday times, means that company commentary from us will be sparing this time.

Cargotec recently held two capital market days where Hiab and Kalmar respectively had the opportunity to make a more in-depth presentation of their respective operations. The reason was the long-planned spin-off of Kalmar, which took place on July 1. After the transaction, the owners of Cargotec will receive the same number of shares in Kalmar as they had in Cargotec, and consequently they will then be the owners of two companies listed on the Helsinki Stock Exchange. At the time of writing, the market capitalization is approximately EUR 3 billion for Cargotec and approximately EUR 1.5 billion for Kalmar.

The old Cargotec was basically unleveraged and there will likely be a sale of MacGregor in the second half of the year. In relation to the market capitalization of EUR 3 billion, there is speculation about a purchase price of around EUR 500-700 million, or as much as EUR 8-10 per share. That overcapitalization, after any new acquisitions, we would like to see it distributed to us and other owners when that time comes.

The valuation is currently around 9x EBIT 2025e for Cargotec and around 7x EBIT for Kalmar. Those are attractive multiples given the investment return that we get. Hiab’s operating return on capital last year was just over 30 percent and it has had a sales growth of just under 8% over the past 10 years. Correspondingly for Kalmar, the last quarter was 22.5% return on capital, and it has had a sales growth of 5.4% per year for the last 10 years.

We have been invested since last summer and Cargotec’s investment thesis is a good example of situations we like. New management, new strategy, spin-off, sale of non-core operations and a valuation that was then low or during the autumn very low. A dissolution of the conglomerate structure will also reduce costs. Finally, of course, two core businesses that each have a strong history and many great opportunities in the next 5-10 years.

Biotage

Biotage was the fund’s worst contributor during June. The reason for that was likely that Sartorius, whose stock was down 12% one day in June when they were giving a presentation at an investor conference (!), talked down expectations for the next quarterly report. Sartorious, which has been a star and favorite on the German stock market in recent years, has had several disappointments in recent quarters. American Agilent was also out a month ago with soft comments, but then above all regarding the Chinese market, where Biotage currently only has a five percent exposure.

The picture below shows that in the last year Biotage has risen by 20% compared to 4% for Agilent and –35% for Sartorius. The relative excess return during the same period for Biotage is 15% relative to Agilent and 85% against Sartorius. Biotage shares fell 12% in June but have risen 22% in the first half of the year. The company reports on July 16.

Source: Bloomberg

Summary

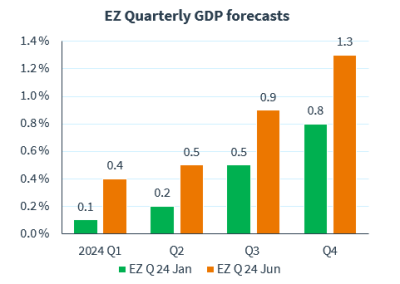

As you know, time flies when you’re having fun and another six months are now behind us. Overall, the year has developed better than expected. Economic growth in both the US and Europe has been revised upwards, which has contributed to rising earnings estimates, which in turn has driven share prices worldwide. Below are GDP expectations for the Eurozone today, compared to the beginning of the year.

Source: Consensus Economics

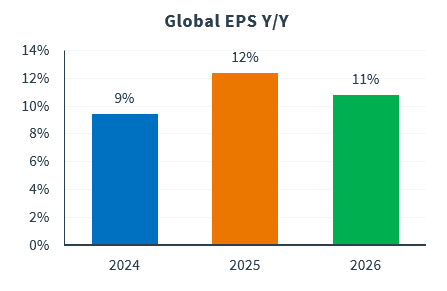

Below is the expected development in earnings per share on a global level. Growth is expected to accelerate from here.

Source: Consensus Economics

Reliable data points regarding the US stock market. 1) US stocks now make up about 70% of all the world’s stocks! 2) The rise in the American stock market has (again) been extremely concentrated in the large technology companies. 3) Nvidia, which in the first half of the year rose by almost 150%, itself accounts for almost half of the entire S&P500’s rise of 15 %! Senseless. 4) Measured in Swedish kronor, the S&P500 has risen by as much as 22% during the first six months of the year.

Source: Goldman Sachs

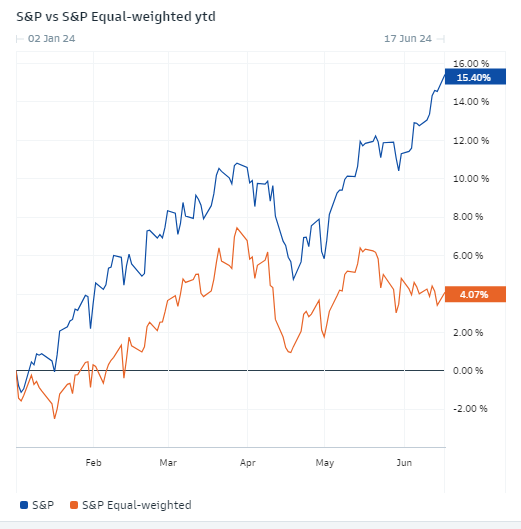

Below, the S&P500 compared to an equally weighted S&P500. The difference in yield is huge.

Source: Goldman Sachs

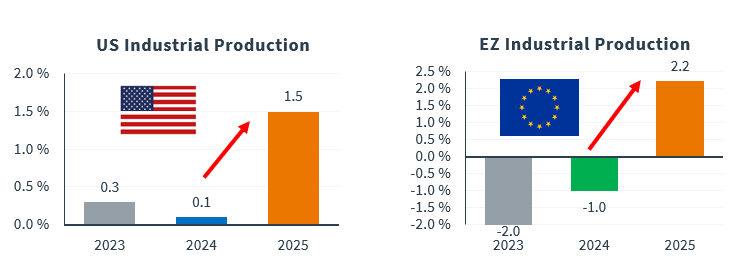

American and European industrial production is expected to accelerate substantially from current levels next year. We should see an acceleration already this autumn. Europe has about twice the delta, year over year, than the US is expected to have.

Source: Consensus Economics

The positive stock market performance this year has created optimism that we have not seen since the end of 2021.

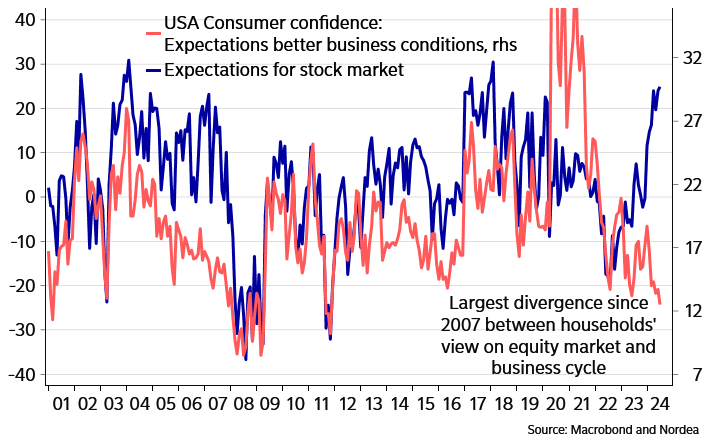

Below is an interesting picture that shows that despite a negative view of the general business climate, US investors have a positive view of the stock market. The combination of this coupled with the extremely high concentration of returns give rise to after-thought.

The optimism has led to the second largest inflows ever (2021 higher). It is primarily passive capital that increases at the expense of active capital, which in turn contributes to further increased concentration as the larger the company, the greater the weight and the more capital is pushed into new investments, regardless of valuations. A development we think is unfortunate.

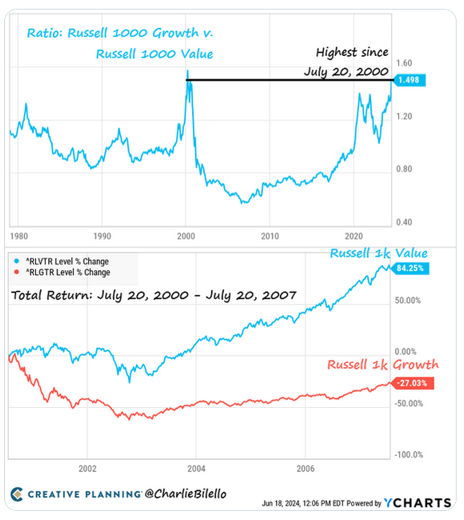

The relationship between the American growth index Russell 1000 Growth and Russell 1000 Value is now, 24 years later, back at the same level as at the beginning of the year 2000.

Source: @CharlieBilello

The development for European small and mid-caps relative to larger companies has stabilized but has a lot of catching up to do in the coming years. We think that the conditions for that are unusually good.

The extreme concentration on the US stock market has caused small companies in relation to the S&P500 to have their worst relative year ever… That says a lot, from two different perspectives and that passive capital is completely blind. As such, there is probably several good opportunities in the asset class.

Source: Bloomberg

We are now rolling into a new reporting season which will, as usual, provide answers, but also raise new questions. On an aggregate level, things tend to be better than expected on both sides of the Atlantic. Since 2010, it has only been worse than expected on two occasions, see picture below.

Source: Goldman Sachs

Trend-following strategies have in a short time reduced their exposure to European shares. The flow from there will probably continue to be weak until the British and above all the French election is over. In addition, most buyback programs are now paused ahead of the companies’ quarterly reports.

Source: Goldman Sachs

Based on data from 1928 onwards, the first two weeks of July are the two strongest of the entire year for the US stock market (which usually spills over into Europe). Nasdaq has had a positive return in July 16 years in a row… For all you number geeks, the following table is attached showing average historical returns for the S&P500.

Source: Goldman Sachs

Is the glass half empty or half full? Leaving aside the noise and volatility of recent weeks and despite significant geopolitical uncertainty, the outlook for equities as an asset class remains bright. The economies continue to show good resilience, various purchasing indices have started to rise, inflation is under control, central banks have started to lower key interest rates, consumer confidence in various parts of Europe is set to rise and buyouts on the stock exchange are becoming increasingly frequent. The conditions between different sectors and companies are unusually large, which means that it is a good stock picking environment.

Europe as a market should have the ability to rebound when the French election is over, and we know the new conditions. The market dislikes uncertainty and many shares have fallen significantly. We think company reports will generally be good and hopefully it won’t be long until the ECB makes the next interest rate cut.

As you know, we do not position ourselves for different macro scenarios, but focus on our companies, which together form a strong and diversified portfolio. Several companies have significant potential and in principle all have a strong or very strong balance sheet. July 11 kicks off our reporting season with BoneSupport and SLP. We look forward to that day.

We wish you all a relaxing July with sun and holidays.

Mikael & Co

Malmö on 8th of July 2024

IMPORTANT INFORMATION. This is a marketing communication. Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested. Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.