Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class' return. The information below regarding returns therefore differs from the returns in other share classes.

Before making any final investment decisions, please read the prospectus, its Annual Report, and the KID of the relevant Sub-Fund here

This material is marketing communication

Monthly Newsletter Coeli European – March 2024

MARCH PERFORMANCE

The fund’s value increased by 9.6% in March (share class I SEK), while the benchmark increased by 7.2%. Since the change of the fund’s strategy at the beginning of September this year, the fund’s value has increased by 19.8% compared to an increase of the benchmark by 6.7%.

* Adjusted for spin-off of Rejuveron

** Includes September 1 (strategy change to long-only implemented September 4 2023)

EQUITY MARKETS / MACRO ENVIRONMENT

The fund performed strongly with a 9.6% return compared to 7.2% for the benchmark. The broad European index rose by 3.6% and the S&P500 by 3.1%, both measured in local currency. The Swedish krona weakened by 2.6% and thus contributed positively to the fund's return. Underlying momentum in the fund was strong and produced a positive return on 17 of the month's 20 trading days. All but two holdings (Carel and CVS) gave a positive return and the five main contributors were: Sacyr (+12.8%), Corem (+20.7%), Commerzbank (+19.0%), SLP (+9.3%) and Accelleron (+13.4%). Total contribution from the top five holdings was 3.2%.

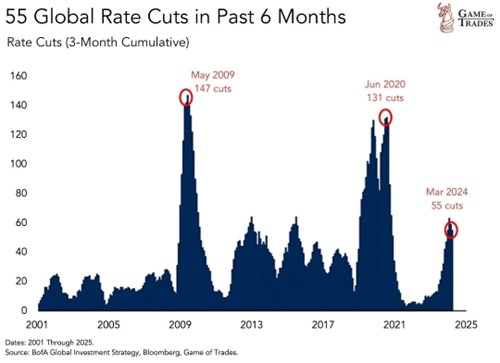

The Fed delivered a perfect message to the market on March 20th when it revised up the growth for the US economy while also communicating that there will likely be three interest rate cuts this year. Although the last two inflation data published were higher than expected, the Fed said that things are moving in the right direction. They also see a labor market that is normalising and their comments about the second half of the year were clearly dovish. Our simple view is that we believe in a first interest rate cut in June, otherwise it will be too close to the election in early November as one want to avoid criticism from the Republicans that the Fed is supporting the incumbent President, Joe Biden. The investors and economists who for two years stared blindly at the inverted yield curve and stubbornly claimed that an American recession was on the way, seem to continue to lose both relative and absolute performance. If one is to say something serious about the picture below, the famous Fed put is again in play but, this time, to a lesser extent in the stock market but significantly more in the US economy as a whole. Definitely positive.

Source: X

Back in the day, when the world was less complex, the world's central banks acted in reasonably synchronised fashion. That does not seem to apply now when there is zero interest in Japan, 4% in Europe, just over 5% in the US and 2.5% in China. Growth figures also differ, although few see the five percent GDP growth that China's state authorities are communicating.

It was not synchronised, but the Swiss central bank was the first to cut interest rates in March. The Bank of England started talking dove-like and even the Riksbank (Swedish Central Bank) surprised when they said, at the end of March, that once could see a first interest rate cut as early as May. Put simply, the above is completely in line with our view for the past six months and the portfolio is also positioned for this, which can be seen in the fund's return during the same time period.

Later this year we will likely see a new peak in the image below (our view).

Source: Goldman Sachs

So far Europe is asserting itself well in this environment. The valuation gap against the US is the highest ever, despite the fact that the performance of Europe's stock markets has been positive in 15 of the last 18 weeks. That’s the longest positive period since 2012.

Below is the return for the first quarter of 2024. The performance for European and American small- and mid-caps during the same time period was 8.2% and 4.0%, so slightly lower than for the large broad indices.

Source: UBS

Best sector in Europe so far this year is the defence industry followed by low valued banks. The second worst sector in the first quarter of the year is real estate (which, however, had a very strong finish in 2023).

Source: UBS

In addition to the valuation differential that explains part of Europe's strong start to the year a clear improvement in economic indicators has driven the development, particularly in the UK.

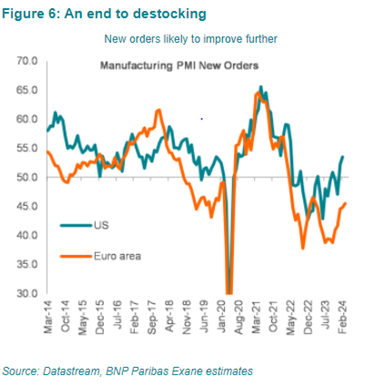

The outbreak of war in Ukraine led to a huge inventory build-up for many industries and is still disrupting growth and forecasting for many companies. Now the volumes for new orders are rising in both the US and Europe, which is a step in the right direction.

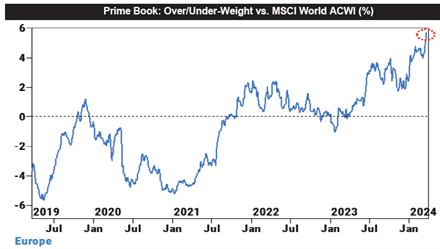

In the past month, Europe has been the most net bought region among Goldman Sachs clients. The net allocation against MSCI World was a whopping +5.8%, which was the largest deviation ever measured.

Source: Goldman Sachs

As we wrote in last month's newsletter, we were surprised that small-caps did not follow the rise during the beginning of the year given the excellent conditions. In mid-March, there was a change of scene and the share prices of smaller companies began to rise.

Measured in local currency and during the second half of March, European small-caps rose 2.3% compared to the broad index which rose 1.2%. US small-caps rose 4.6% compared to the S&P500 which rose 1.8%. Swedish small-caps rose by 5.0% compared to the OMX30 which fell by -0.4% (where large dividends weighed down).

The development follows inflows to funds with a focus on small- and mid-caps (like us). Note the bar in March which showed by far the largest inflow in the last three years.

It is also a sign of health that the breadth of the market has increased, see image below. The picture looks the same for the American market where at the time of writing Magnificent 7 has been reduced to Magnificent 5, as Apple this year has fallen by 12% and Tesla by 33%.

Source: Goldman Sachs

European inflation is soon fully under control. Below is Eurozone inflation including data from April 3 which showed 2.4% against an expected 2.5%. Are you awake ECB?

Source: Bloomberg

Simultaneously Europe's engine, Germany, continues its regress and few, if any, signs of an economic recovery are visible. The expected interest rate cut until the end of the year is currently around 0.9% and it feels obvious that the ECB will, once again, damage the economy unnecessarily. The same people who stubbornly stuck to zero interest rates are now stubbornly clinging to the current level of interest rates. Impressive.

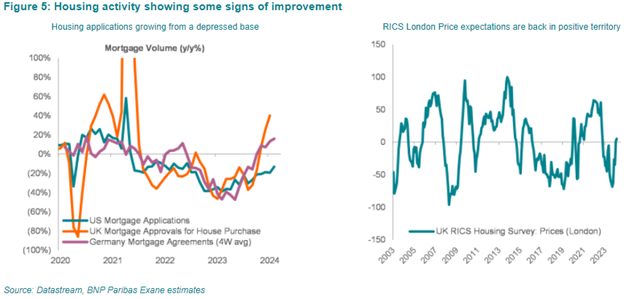

After some very challenging years for the UK economy, things now appear to be slowly turning. Fitch upgraded the outlook for the UK economy from negative to stable at the end of the month. Below is the activity in the UK property market as well as price expectations. Similar developments are now also visible in Sweden, with three consecutive months of rising prices. It will continue in the coming quarters with rising real wages and falling interest rates.

Is this the picture of the month? We'll know in a few months. China, which has been completely under the ice since the pandemic broke out, now shows the biggest increase in leading indicators since 2005!

In March, the EU was in full swing against American technology companies. First, Apple had to pay 1.84 billion euros for abusing its dominance in music streaming. It was complaints from Spotify that proved Spotify right and the EU handed out its first ever bill against Apple for this kind of overstep. Apple will appeal the ruling.

A few weeks later, it was time again when the EU started investigating Apple, Alphabet and Meta regarding options in the use of personal data. It should be obvious that if one does not pay for the product (Facebook) then one is the product and it is easy to understand that our American friends feel that EU are chasing American technology companies when they themselves are significantly behind in development. Europe has completely missed the enormous opportunities that have arisen in the last 20-25 years and no new global technology champions have been created. Incredibly sad on many levels.

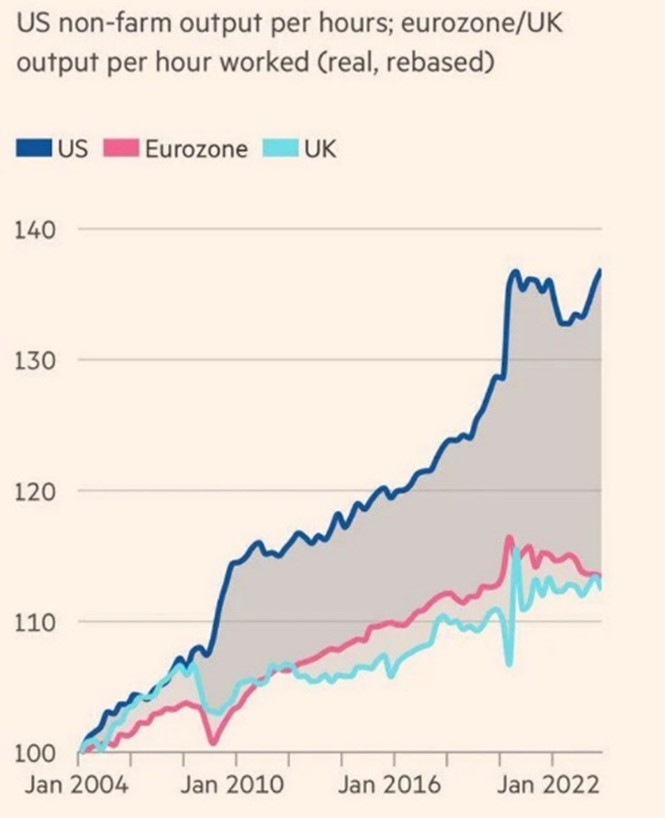

Maybe we should think about improving productivity in Europe instead of prioritising shorter working hours and higher pensions? Just a thought.

Source: Financial Times

On March 7th, Sweden finally joined NATO. Thanks! Prime Minister, Ulf Kristersson, received a standing ovation when he witnessed President Biden's annual State of the Union speech. https://twitter.com/tomsamuelsson/status/1765932713217814937 At the same time, the Social Democrats tried, in a gutsy way to say the least, to take the credit, despite the fact that for 75 years they refused to even discuss the subject.

Source: KluddNiklas

PORTFOLIO COMPANIES

Accelleron

The ABB spin-off and turbo engine seller, Accelleron, was the last of our companies to report for 2023. The full year ended with 16% organic growth in sales, with a corresponding increase in operating profit. The figures were a few percent better than the advance tips. For 2024, management is guiding for more modest growth of 0–2% organically. This is partly due to a couple of the company's markets slowing down after a couple of very strong years, and partly, we believe, because the guidance is a function of the fact that management has historically been very conservative in its outlook.

The beauty of Accelleron's business model is that around 75% of revenues is made up of recurring service revenue. After two years of unusually high one-off product sales, several years of highly profitable service revenue await. The profits are therefore predictable, which the stock market usually values highly. The predictability also makes it easy for the management to plan for their costs, which is clearly manifested in the fine operating margin of just over 24%.

When we invested in Accelleron about 1.5 years ago in conjunction with it becoming its own public company, it was precisely the predictability that we liked and it has always been a core holding since then. Since then, the company has performed above the market's expectations while profit multiples have risen by over 50%. Overall, this has seen the share price more than double since our initial investment. Even if we do not believe in an equally strong development going forward, we believe that the share will do better than the stock market. In March, the share rose by a further 13%.

Source: Bloomberg

Diploma

British serial acquirer Diploma has a high profile among many UK fund managers, which is reflected in the valuation of 17-18x EBIT on the next 12 months' expected earnings. In order for our investment calculation to add up, Diploma must succeed in carrying out value-adding acquisitions. In March, we saw just such an acquisition when management acquired Peerless Aerospace Fastener, which distributes fasteners to the aerospace industry.

- The company has historically grown by 9% organically on an annual basis and has an operating margin of 30%.

- The acquisition is carried out at a valuation of approximately 7x EBIT for the expected operating profit in 2024 (!).

- Diploma expects the acquisition to add 8 percent to earnings per share in the first year.

- The return on investment is estimated at 15% in the first year (and the figure increases in future years).

The acquisition seems almost suspiciously good. When a question on that theme was put to management in a conference call, it was mentioned that the bid for Peerless was won in competition with private equity firms, which, however, cannot offer the autonomy to Peerless's current management team that Diploma can. Diploma also has a perpetual ownership horizon, which private equity companies by nature do not have. Competitors made higher bids for Peerless than Diploma, but they were outbid in favour of the soft values that Diploma can offer.

The stock reacted extremely positively to the acquisition announcement and rose by 8% in March.

Bechtle

For some time now, we have built a mid-sized position in the IT retailer, Bechtle. There are several IT retailers in Europe (Norwegian Atea is a relevant comparison), and Bechtle is considered by many to be the best. Some of the sales come from software products, but the majority of sales come from hardware such as PCs, mobile phones and the like. Bechtle targets other companies and has a large proportion of its sales from the German-speaking parts of Europe. Over the past five years, Bechtle has grown sales by 13% per year with a high return on capital.

The company is family owned and managed by an esteemed CEO who has held his role since 2010. The company has a very long term view, which is not least reflected by the company's 2030 goals that were decided back in 2018.

An important part of the strategy is to acquire other smaller retailers at low valuations which are then allowed to be managed with continued high autonomy. In addition to Bechtle being able to acquire these companies at good valuations, there is also an industrial logic in that a larger scale Bechtle gains a better negotiating position against its suppliers such as Dell, HP, etc. Overall, we think Bechtle has many of the quality markers that a good serial acquirer should have.

In the short term, the market is worried about the economy in general, and the German economy in particular. In addition, Bechtle has a high sales exposure to German small- and mid-caps, which have it even tougher in the current climate. If you look ahead; however, there are many years of structural growth where Bechtle should be able to grow by 5-10% organically and more with the help of acquisitions. Over time, the service leg of the business should make up an increasingly large proportion of sales, which should have a positive effect on profitability.

The stock is valued at around 13x EBIT on our 2025e estimates, which is slightly below the historical average. However, our estimates do not price in more acquisitions. The valuation is not low in relation to many other retailers, but also not crazy high compared to Bechtle's historical valuation levels. We have tried to take advantage of the market's short-term fear of the economy for an investment we believe will pay off in the long term. Bechtle shares rose 3% during March. We hope to return to this topic later.

4imprint

In March, the gift advertising company released its financial results which confirmed already announced figures from a press release earlier in the year. At the same time, management expressed that the year started in line with analysts' expectations. This was enough for the stock to rise 11% in March. 4imprint is thus one of the fund's best shares this year with an increase of 38%.

Since 2012, 4imprint has grown its sales by 15% per year, compared to 4% for the market as a whole. 2023 was another year in which the company gained market share. The strategy has been the same for many years and regardless of the economy, the company will very likely continue to gain market share. With neutral working capital and low investment requirements, the return on capital employed is very high, at over 100%.

.

.

Source: Coeli European

Carel Industries

Since last year, we have owned shares in Italian Carel, which, among other things, produces and sells control solutions, humidity controllers and dehumidifiers. The company has a history of strong organic growth, is family-owned and has also started to build a good acquisition track record. With exposure to data centres, energy efficiency and industrial cooling solutions Carel has a large structural tailwind in the coming years from most of its business areas.

Around 10% of the revenue; however, comes from the heat pump industry to which Carel is a subcontractor. Although this represents a relatively small percentage of sales, the heat pump leg accounted for a large part of last year's growth. The well-documented problems that the heat pump industry is experiencing with higher interest rates, lower electricity prices and overstocked inventories will now instead affect Carel negatively in 2024. This is what the market latched onto when Carel outlined its outlook for the year to analysts in March and the stock fell by about 5%.

We foresee a couple of weaker quarters which could possibly affect the share negatively. On the other hand, the share has developed weakly during 2024, which may imply that most of the short-term concerns are already reflected in the share price. In the longer term, we are not worried about Carel, which is a fine company with good future prospects, and we believe that the stock market will value the heat pump exposure as something positive as soon as there are whispers about that market bottoming out.

Volution

In March, the British ventilation company released yet another good report that resulted in positive estimate changes from the analyst collective. The market is worried about declining sales against the backdrop of the difficult construction climate, but Volution continues to report positive organic growth. We think that the company deserves a proper valuation from today's levels, which implies about 13x next year's profit on our estimates. With the current valuation, we believe that there is a certain bid risk for the company, especially in combination with the ownership profile as there is no clear main owner.

Rugvista

As we mentioned in the previous monthly newsletter, we thought the reaction to the company's Q4 report was exaggerated. After we adjusted for a couple of one-off costs that the company itself included in its reported operating profit, the profit was pretty much in line with the advance predictions. In March, the share regained ground with a rise of 15%.

SLP

Property companies developed relatively weakly during February, but were considerably stronger during March, and SLP was no exception. Fundamentally, nothing has changed in the company. However, the share price has been under pressure from a larger seller and a less well-executed placement at the beginning of March. We took advantage of the opportunities presented and ramped up the position from low levels to the now the largest holding of the fund. The share rose 9.3% during March, but from the lowest levels where we bought a lot of shares, the share rose 17-18% and SLP thus became a strong contributor to the fund’s performance in March. The stock market is a strange market; when there is a sale on, people don't want to buy and when the prices are higher, people come back.

Bonesupport

Bonesupport continues to deliver great value to the fund. During March, two pieces of good news came in, which caused the share to rise 12 and 8% respectively during those days. The first news was a 510(k) approval for the indication interbody fusion in the spine. The application concerns Cerament BVF in the USA and the amazing part is that the approval only took 10 days (usual processing times at the FDA is 90 days). Either Bonesupport was just lucky, but more likely the data from clinical trials is so strong that there isn't much to deliberate on. Launch of the products remains at the end of 2025.

The other news was a market approval for open fractures in the US. Cerament G is the first and only combination product to be approved in the United States for this indication. However, there is one detail that we think the market has not caught on to. Typically, a 510(k) approval is granted for the indication sought, in Bonesupport's case, the shin bone. The FDA approval covers all extremities, that is, surgeons may not only use Cerament G prophylactically on the shin but in all extremities. This is of course incredibly good for the case. The replacement codes should be in place by September, allowing us to expect sales in the fourth quarter. The codes also give hospitals full reimbursement if surgeons say they use Cerament G. In other words, there are very large incentives to choose Cerament G over other off-label products that are cheaper. This means that the estimates will probably need continued upward adjustments as usage increases. Trauma and open fractures are one of the fastest growing areas in orthopaedics. With the approval, the door opens up for a larger company to acquire Bonesupport. With gross margins around 92%, Bonesupport in a larger organisation with its own sales force could generate a contribution margin of around 80-85%. At today's rate, that would mean EV/EBIT 15x for such an actor, not very expensive for a company with a completely unique product that is taking market share at breakneck speed.

Surgical Science

After having owned the share for a long time, we chose, in March, to sell our last shares in Surgical Science and reinvest the capital in a couple of other new companies. We thank CEO, Gisli Hennermark, and CFO, Anna Ahlberg, for phenomenal work during the approximate five years we have been invested.

Sacyr

Sacyr is a Spanish concession company focused on building, developing and operating private motorways. We have been invested in the company since the beginning of 2023 and since a few months ago it has been one of the largest holdings in the fund. The company has a checkered history with far-reaching deals where, among other things, it bought into the oil company Repsol. Since 2015, the business has been cleaned up and last year it was finally finished.

Today, the company has a strong balance sheet with the help of significant operating cash flows, dividends from associated companies and disposals of more peripheral assets. This, in turn, has now made it possible to invest in projects that one previously had to turn down, as one did not have enough capital to be able to participate. The beauty of this type of business is that once the investment is made, it is a safe asset that generates a predictable cash flow and requires very little incremental investment over its lifetime which can be up to 30-35 years. The company presented its Q4 results on February 29, which were solid, and the stock rose 12.% in March. Despite that rise, the stock trades at a low 10x and 9x operating profit for 2024e and 2025e, respectively.

SUMMARY

We have had a positive outlook of the stock market since mid-October when we started to argue in our monthly newsletter that the conditions for the stock market were starting to be exceptionally good, especially for small- and mid-caps. In Europe, we had basically had 22 months in a row with historically bad conditions and the state of investors was at the turning point at rock bottom. The difference in the state five months later is almost like night and day, especially in the financial markets, but great progress has also been made in the real economy.

Our reference point and view from here is that the starting point, after the 22 months mentioned above, was at a level that occurs once per decade. The easy money has been made, but the conditions from here are still unusually good and, once again, especially for small- and mid caps. Nothing has really moved the needle there, as the asset class this year lags behind the general price trend and, in terms of valuation, is at levels that rarely appear. Consequently, we are still clearly optimistic given today's conditions. In order to hopefully increase the understanding of how we think, we first give you an overview of what the major economic conditions look like and then what it means for the smaller companies.

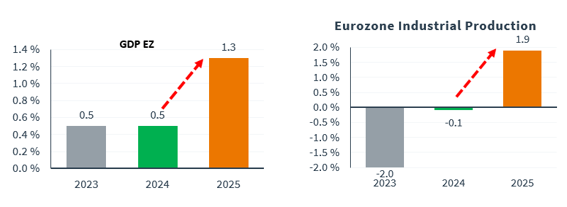

Europe is expected, after two years of a retracting economy, to accelerate starting in the second half of this year. Industrial production is an important component.

Source: Kepler Cheuvreux

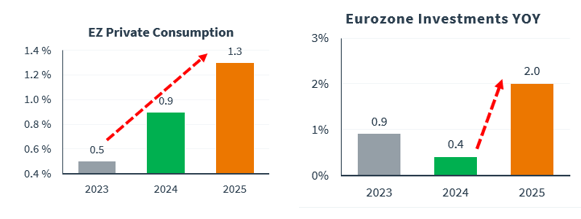

Private consumption rises in line with real wage increases and investments are also expected to rise significantly.

Source: Kepler Cheuvreux

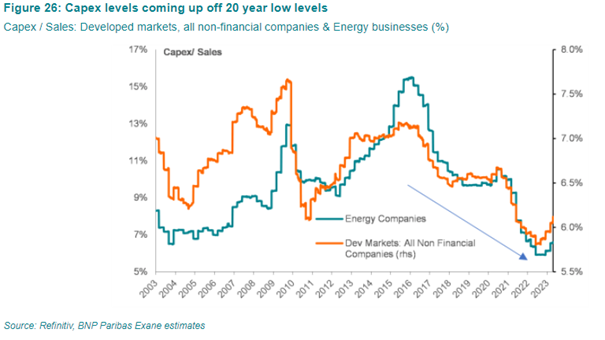

10 years of steadily declining corporate investment is now reversing.

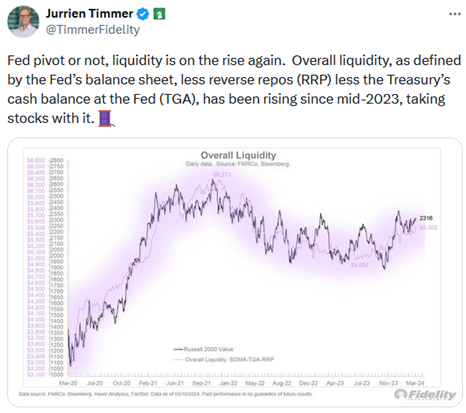

The financial conditions have eased considerably and are a major reason why risk appetite has increased in recent months.

Source: Jurrien Timmer, Fidelity

European banks, which have been more or less completely knocked out since the GFC in 2008, have since a year ago awoken with profits not seen for more than 17-18 years. The ECB is currently feeding the banks heavily where current interest rates give very strong net interest income for the banks (our own Commerzbank is a perfect example). For some of the banks' customers, it is tough, but for the economy as a whole, it is very positive that banks have finally recovered.

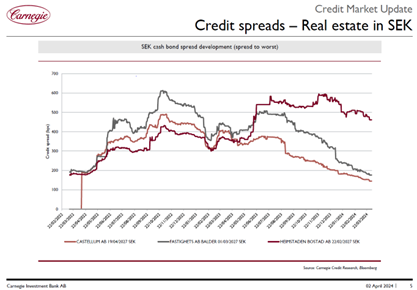

European property shares are also starting to heat up after two very challenging years. The bond market, which was completely dysfunctional, has been functional for a few months now and is a strong contributor to the fact that real estate shares have started to recover. For about a year now, the fund has had around 10% exposure in the form of SLP and Corem, where both shares rose by around 33%last year, but this year have fallen by around 1and 4%, respectively.

Below are credit spreads for Castellum, Balder and Heimstaden. In six months, Balder's mark-up has dropped from around 500 basis points to just under 200. That is extremely high and of course extremely gratifying. Worth mentioning is that inflows to bond funds have been significant in recent months. So no fear there.

Source: Carnegie

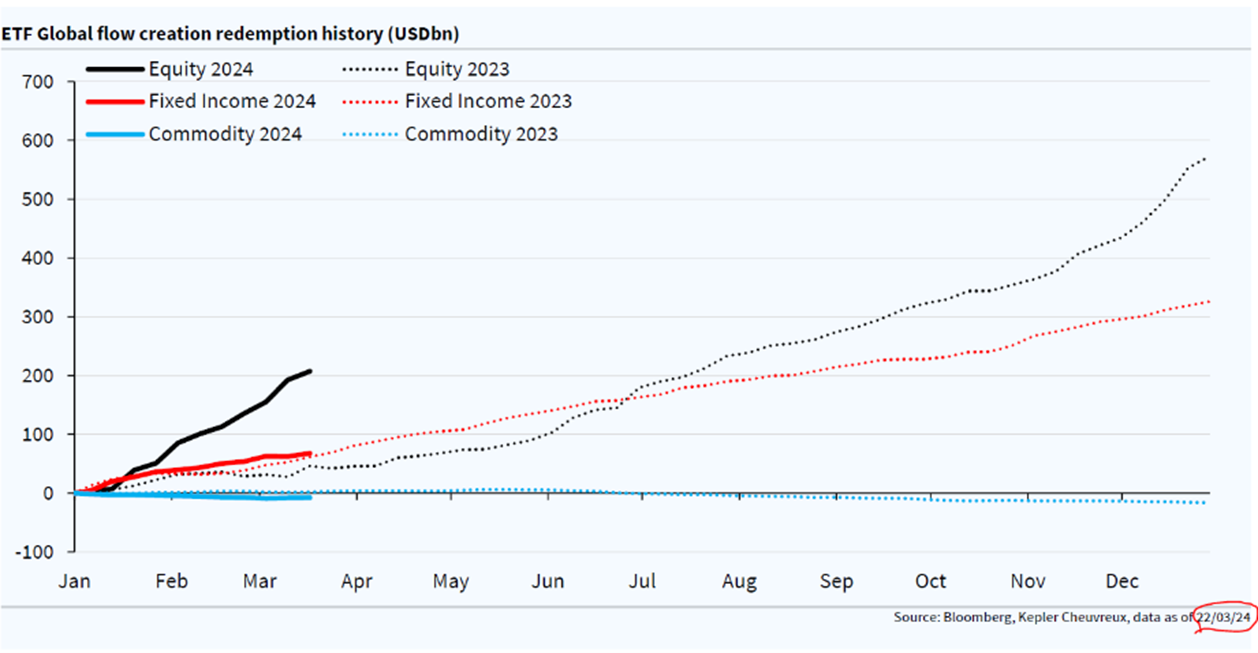

But it is equity funds that account for most of the inflows so far this year (compared to 2023).

Source: Bloomberg, Kepler Cheuvreux

The Nordics take the lead in Europe in terms of buying pressure on shares in 2024. That is one reason why we have had and continue to have an overexposure to Sweden in the fund. It has been really depressed up in the Nordics.

Source: Kepler Cheuvreux

We wrote last month that our firm opinion is that European companies have never done as much buyback of shares as now. We applaud that. The figure below shows the net demand for the US equities since 2000. Corporate buybacks are by far the biggest takers of shares and are to the highest degree contributing to a strong stock market. 5.5 trillion USD… Just under a trillion of that is expected to be bought back this year, so very high levels.

Source: Goldman Sachs

Another healthy sign is that the market for IPOs opened up in March with several major companies entering the stock market. The majority of these introductions went well with positive returns on day one. We did some work on two European introductions, but nothing was our cup of tea. We expect an accelerating number of introductions before the summer break.

Overall it all boils down to the conditions and reasons why we remain positive about smaller companies in particular.

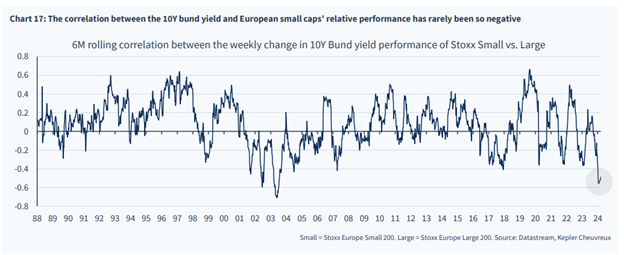

Only once before has the negative correlation between the 10-year interest rate and the relative development between small- and mid-caps been greater. It was 2003, which was also the starting point for a number of fantastically good stock picking years for, mainly, smaller companies.

Source: Kepler Cheuvreux

Smaller companies have developed significantly better than larger companies when interest rates were cut in Europe. We think the kick-off for the first reduction will take place in June (but should happen now already).

Source: Kepler Cheuvreux

Historically speaking, the development of medium-sized companies has been significantly better compared to larger companies after the first interest rate cut.

Below is a hot candidate for picture of the month. Historically, small-caps have taken over the development after a period of mega-cap dominance. Of course, we could be wrong, but for what it's worth, we ourselves are convinced that this will be the case this time as well.

Source: MONTANARO, Jeremy Siegel

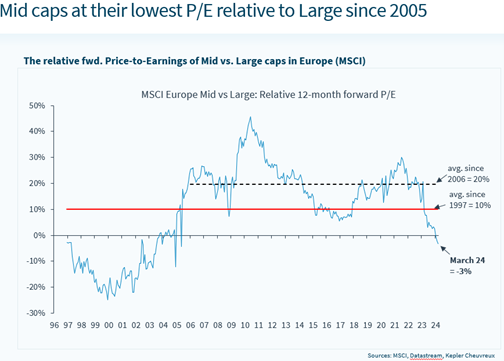

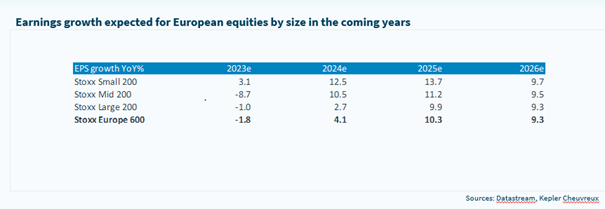

In conclusion, what does the current valuation look like for the small-caps? Thanks for asking, excellent!

Source: Kepler Cheuvreux

Source: Kepler Cheuvreux

Source: Kepler Cheuvreux, Datastream

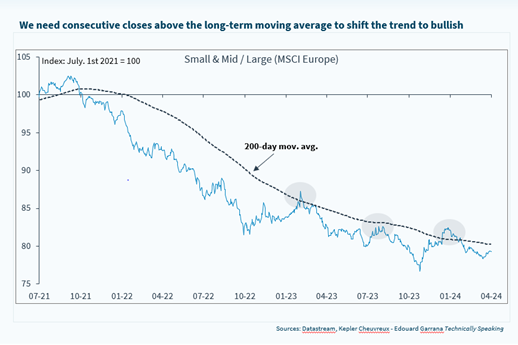

Now we hope (expect) that the asset class, SMID, will also pass some technical levels which will then likely trigger purchase programs that could make it really interesting.

Finally we are pleased to announce that we have received a significant capital increase from our largest investor, Norges Bank Investment Management, NBIM. We are of course very happy and proud of this. This underlines the strength of our portfolio management and the fund, Coeli European, is largely a reflection of the mandate we manage for NBIM.

That's all for this time and we thank you for your interest!

Mikael & Team

Malmö April 5th, 2024