Monthly Newsletter Coeli European – March 2025

This material is marketing communication.

Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class’ return. The information below regarding returns therefore differs from the returns in other share classes.

Before making any final investment decisions, please read the prospectus, its Annual Report, and the KID of the relevant Sub-Fund here.

March Performance

The fund’s value decreased by 8.8% in March (share class I SEK), while the benchmark decreased by 5.4%. Since the change of the fund’s strategy at the beginning of September, 2023, the fund’s value has increased by 8.8% compared to an increase of the benchmark by 7.5%.

Source: Coeli European

* Adjusted for spin-off of Rejuveron

** Includes September 1 (strategy change to long-only implemented September 4 2023)

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

Equity Markets / Macro Enviroment

The shambles of the American administration continue to have a major negative impact on the world's financial markets. In addition to making near enemies of the democratic world, breaking up long-standing and established partnerships, and speaking highly of Russia, it also has a very clear negative effect on the American economy. Admittedly, it is a defined goal to bring down American inflation expectations and thus the dollar and interest rates, but it is a very high stakes game. Combine this with the less intelligent comments after the Signal leak. Is the boys' club on top of things?

Source: Kluddniklas

The broad European index fell by 4.2% in March (-6.7% in SEK). The S&P500 fell by -5.8% (-11.7% in SEK), Nasdaq by -7.7% (-13.6% in SEK). MSCI Small Cap fell by -5.9% in SEK and the Carnegie Small Cap index by -8.0%. The worst month in a very long time and this is largely due to the chaos that the new administration left behind practically every day.

The fund also had a weak performance with -8.8% in return compared to -5.4% for our benchmark. On an absolute basis, the krona appreciation accounted for -2.8% and for the first quarter the corresponding contribution is -5.2%. The best contributors in March were Euronext, Volution and Sampo. The worst contributors (except for the krona) were 4imprint, Bonesupport and Diploma.

The Swedish krona has had a very strong development in a short time and can be seen as a derivative on Europe who is waking up after many years of non-existent growth. At the same time, Sweden has a low national debt of only about 32% of GDP. Below the EUR/SEK development over the last four years.

Source: Bloomberg

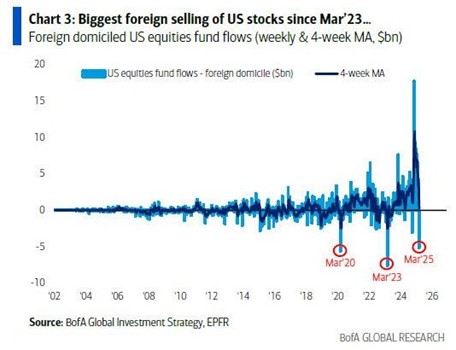

Having walked on water for the last 15 years, the US economy is now showing clear signs of slowing down. This, combined with a euphoric state of investor sentiment at the end of last year, high valuations and to some extent a new anti-American attitude from foreign investors, has led to large capital outflows from the US stock market, see image below. The outflows from international capital are at the same level as during the Covid crash and the US banking crisis in March 2023.

Source: BofA Global Investment Strategy, EPFR

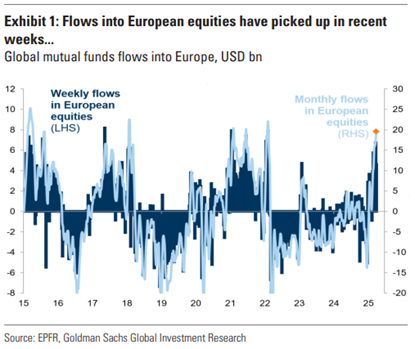

Concurrently, inflows to European stock markets have increased significantly this year.

Source: EPFR, Goldman Sachs Investment Research

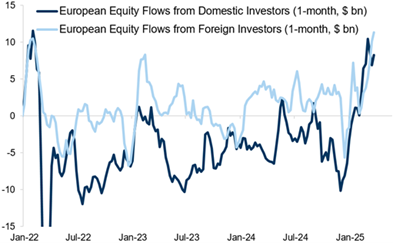

The split between capital flows from domestic and international investors into European stock markets has gone from clearly negative to clearly positive in a short time.

Source: Goldman Sachs

Signs of weakness in the American economy are also clearly visible in profit expectations, which have been adjusted down significantly more in the United States than in Europe in recent months.

The well-being of the important American consumer has also fallen sharply in recent months and is now down to historically low levels.

Source: Bloomberg

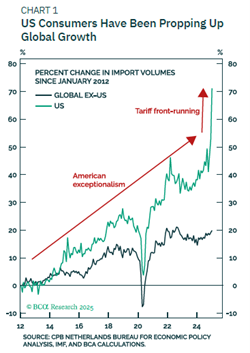

More than 80% (!) of GDP growth in the US, since 2020, has come from the private consumer. A private consumer who now suddenly seems to be feeling worse. The picture below shows the unprecedented strong development of American consumers. It looks like they have been front-running the tariffs that are now delivered blow by blow. President Trump's genius play to use tariffs to build up the US economy feels, to put it politely, flimsy. At the same time, they are in the process of reducing their large budget deficit by, in a brutal way, reducing public spending which in turn, in some miraculous way, should result in increased growth.

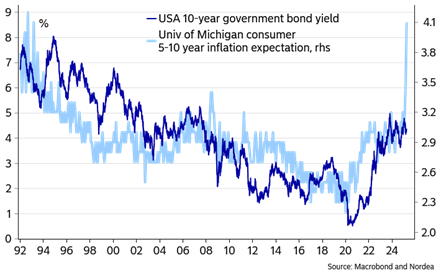

On Friday, March 28, US consumer inflation expectations exploded to their highest level in over 30 years. It feels a bit challenging to bring down the US government's interest costs if there is any truth to the picture below. Maybe the administration knows something we don't?

Source: Macrobond and Nordea

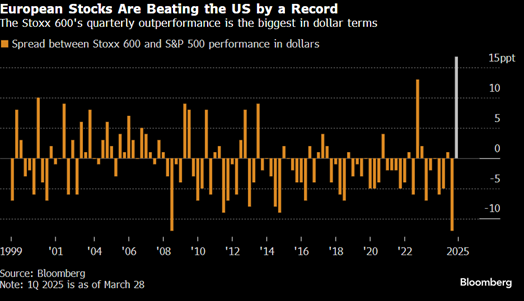

All this combined has led to the SXXP600 (Europe) crushing the S&P500 (USA) with a 17% excess return in the first quarter. A record high difference measured since 1999.

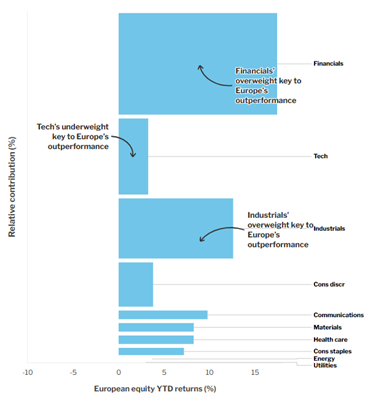

To understand where Europe's outperformance comes from this year, see the chart below. For the fifth year in a row, banks are in the lead. The fact that technology stocks have a low weight in Europe benefits Europe now that this asset class has generally had such weak performance.

Source: Wellington Management, Refinitiv

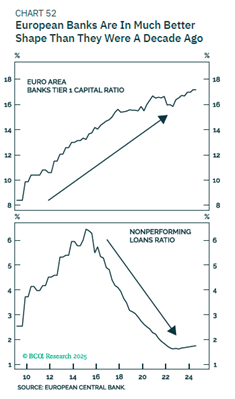

The picture below explains much of the strong performance of European banks in recent years. In addition, they come from extremely low valuation levels. Moreover, and as a point of reference, it should be said that Swedish banks have not experienced such a strong price development, but they have also been in significantly better shape.

Source: EUROPEAN CENTRAL BANK

European banks have beaten Mag7 by a wide margin since the beginning of 2022, see the sensational picture below. The fund invested in Commerzbank in November 2022 and (wrongly) sold the position last autumn. Since the beginning of 2025, we have invested in Austrian Bawag and have again taken a smaller position in Commerzbank.

Source: Goldman Sachs

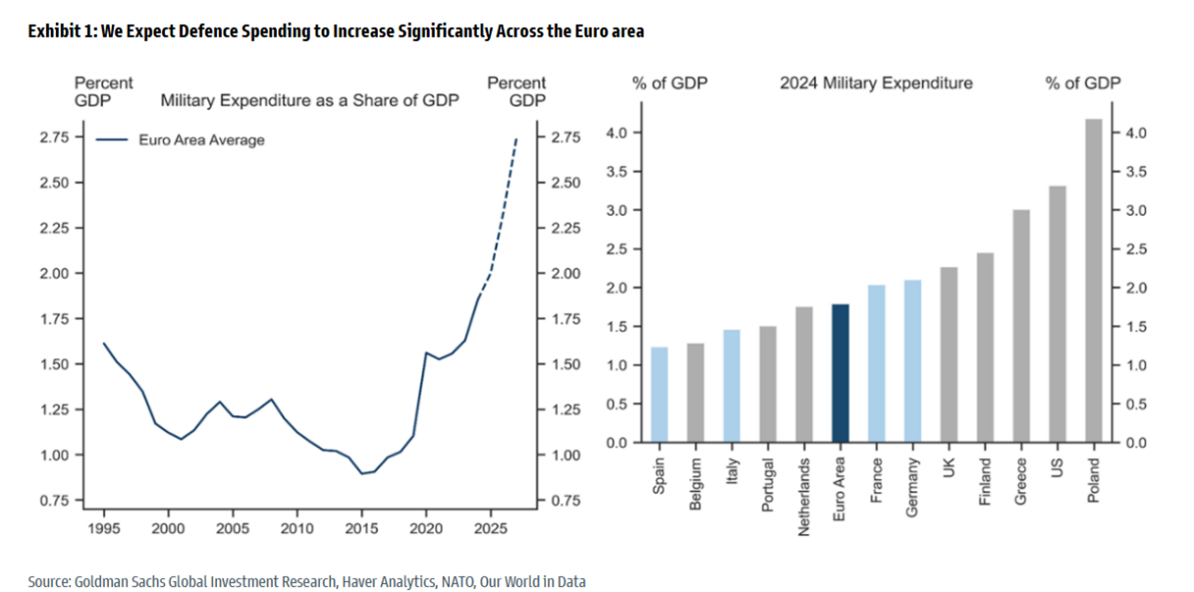

The big theme in Europe during March was otherwise the enormous defence investments announced after Vice President Vance's speech at the Munich Security Conference. It is understandable that the US wants Europe to take its own and greater responsibility for its security and what is happening now is an enormous acceleration that will trickle down to various parts of the European economy. The way the US communicates, however, is deplorable, attacking countries like Denmark and Canada in a macabre way.

The fund does not own any "war stocks", but companies like Cargotec/Hiab and Traton (new position) will certainly benefit from the development through increasing sales.

Source: Goldman Sachs

In addition to defence investments at EU level, the new German leadership also announced an infrastructure program of 500bn euros over the next 10 years. This gave the German stock market additional fuel. It is great to see that Germany, after three years of zero growth, is now acting and doing so with force and determination. This will benefit the whole of Europe.

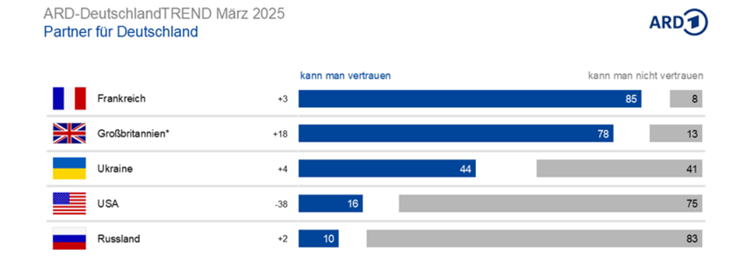

German radio recently conducted a survey among its listeners about which countries can be trusted. The US barely beaten by Russia and see the difference compared to the last survey. Well done….

Source: ARD Deutschland

It is not just defence and infrastructure investments that are supposed to lead Europe forward. There is also strong pressure to reduce the number of regulations and thus make it easier for companies to conduct their business. The idea is that this will increase profits and growth. It is also the highest priority now within the EU to work toward increased equity investments from private individuals, pension and insurance companies. Sweden is a pioneer, and the EU is looking at the solutions available in Sweden with the ISK account (ISA) which is said to be underway throughout Europe. Sweden has the highest proportion of savings in equities and the lowest in bank savings compared to the rest of Europe, and the EU wants to emulate that. Positive!

Smaller companies in Europe have significantly greater opportunities to attract venture capital from Sweden compared to other European countries.

Finally, we note that Vice President JD Vance and his wife flew to Greenland on March 28 for a three-hour stay at the American military base. There, he accused Denmark of doing a bad job in Greenland and that the United States could have done better. The next day, President Trump commented that he wants to annex Greenland. He believes it is a “good possibility” that the United States can do it without using military force, but “he won’t take any options off the table.” Absolutely crazy.

Source: X

Portfolio Companies

Volution

We have become accustomed to Volution, a British serial acquirer in ventilation, spoiling us with good reports. In March it was time again. For the first half of the year ending in January, sales and results were better than analysts had expected. Organic growth over the past six months was around 4%. This should be compared with just over 2 % for the first four months, which implies organic growth at the end of the period that was well above the 4% for the first half of the year.

The large acquisition of Australian Fantech, which we wrote about in previous monthly letters, has started well. Volution's management notes that the profitability of Fantech is at least one percentage point higher than previously thought.

We continue to be impressed by Volution, which constantly manages to outperform analysts. This despite weak end-markets. If a company performs like this in a weak end-market, think about what will happen when the new construction and renovation market picks up again. Then there should be a real boost to organic growth.

Volution shares rose 13% on the reporting date. In March, the share rose by five percent overall and was thus down 4% for the full year.

Rotork

A relatively new acquaintance in the fund is British Rotork, a leader in electronic actuators. Typical end-markets are in the energy sector, power and water infrastructure, and several other industries. The products help, among other things, to secure against leaks in various types of pipes. In the energy sector, the products can also help reduce methane gas emissions. (We wrote more about Rotork in our January letter.)

In March, Rotork released its full-year report for the financial year ending in December 2024. Sales for the full year increased by 8% – about the same as operating profit. The market focused particularly on order intake, which had a strong second half of the year, with an extra strong finish. During the first half of the year, order intake was unchanged. During the third quarter, order intake increased by about 8%, and for the fourth quarter, we estimate that order intake increased by between 15 and 20%.

We also note that the company's gross margin strengthened by a couple of percent. This is largely due to the company's service business growing faster than the group as a whole. Rotork's service business has been neglected historically and a central part of our investment thesis is that it will grow larger as a share of the sales mix, thereby contributing to better profitability in the future. This comes on top of the already strong profitability – the EBIT margin was 23.6% in 2024.

Rotork operates with a net cash position. It is of course nice to have strong balance sheets, but in this case, we think it is far too conservative. It was therefore good to see Rotork taking steps towards better capital allocation. Rotork announced a new buyback program, a higher dividend, and a slightly larger acquisition. We hope Rotork continues this path, and we believe that we will see more buyback programs during the year, provided that no further large acquisitions are made.

Our estimates place the share at around EV/EBIT 11/10x for 2026/2027e. We think that is too cheap for a company of such quality. The share rose 7% on the report day but still ended March with a decline of 4% – one of the many reactions after the reports that have puzzled us this year. For the full year, the share was unchanged as of the end of March.

4imprint

We have had some concerns about 4imprint this year because the company's products are predominantly sourced from China, while essentially 100% of sales take place in the US. This has a double negative effect on margins on the one hand (due to increased tariffs) and on demand on the other hand (due to high uncertainty in the US business climate right now). For this reason, we had reduced our position in the stock ahead of the report release in March.

Although the results for 2024 were slightly better than expected the outlook for 2025 was more uncertain. Sales fell slightly in the opening months of 2025.

As is well known, the stock market dislikes uncertainty, and the stock fell by a whopping 29% in March. This followed a January month when the stock rose 24% and where we sold a significant part of our position. In retrospect, we should have sold more than we did then. For the full year, the stock has fallen by 24%. The stock is currently trading at record low multiples from the time we have been following the company (6–7 years). The multiples are single digits for this company that has historically delivered more than 10% growth per year with rising margins and a return on capital employed exceeding 100%.

De’Longhi

For some time, we have been looking for a high-quality consumer stock. We believe we may have found the right one in Italian De’Longhi. The company is best known for its coffee machines, but also sells other consumer-related products such as blenders under brands such as Braun and Nutribullet. Our outline indicates that De’Longhi should be able to grow by around five percent per year, while margins should gradually improve from today’s 16% (EBITDA level).

De’Longhi is family-owned and has for a long time operated with a very conservative balance sheet. Per our calculations, the net cash in 2024 amounted to EUR 468 million, which can be compared with a market capitalization of just over EUR 4.6 billion. We are starting to hear some comments/indications that the balance sheet is being revalued as the family is probably quite frustrated with the low multiple at which the company is traded. Our estimates point to EV/EBIT multiples of around 8 – 7x for the coming years. We believe that De'Longhi may announce a slightly larger buyback program during the year after giving themselves a mandate to do so during their last annual general meeting.

In the near term, the market is worried about tariffs. Around 17–19% of De’Longhi’s turnover is generated in the US. However, we believe that the tariff rate is well discounted in today’s exchange rate. At the same time, we are seeing inflation in Europe falling, which, all other things being equal, should mean that consumers have more purchasing power. Europe is De’Longhi’s largest market. If we see that the European consumer wakes up again, it is of course good for De’Longhi.

We have a smaller position in De’Longhi, which fell by 10% in March.

Asker Healthcare

In March, we participated in the IPO of Asker Healthcare, a serial acquirer of distributors in the healthcare segment. We were not the only ones to be attracted by the company. From what we understand, the offer was oversubscribed by 15 times. We did a lot of work on the company before the listing, and we received a relatively good allocation. We hope to return to this topic later.

Bonesupport

Bonesupport was one of the worst contributors to the fund during March. After a brilliant report that sent the share up 13% in February, the share price has struggled. The company, like other medical technology companies, has had a tough time in March. One reason for this may be currency fluctuations. The majority of Bonesupport's sales are in US dollars and, as is well known, the dollar has fallen significantly against most currencies. All other things being equal, currency movements will reduce sales estimates by 5% and operating profit by 10%. The share fell by a full 24% during March and we have added to our position at the lowest levels. We feel confident about the company's operational development and, as we wrote in our previous monthly letter, delivery has been impeccable.

Scandic Hotels Group

We suspect that the Scandic share has been hit by profit-taking after a big rise. At the same time, several airlines in the US issued profit warnings due to poor domestic travel. We have also received some other signs from consumer companies that the American consumer is not feeling quite right. This should not affect Scandic as international guests account for around 5% of all booked rooms, which means that the exposure to America is even smaller. Scandic is trading at a free cash flow yield of 8% this year, which we think is too cheap for the largest hotel chain in the Nordics.

SLP

SLP's share price, like the broad property index, fell in March. SLP fell just over 7% compared to 10% for the broad index. Late in March, SLP announced that CEO, Tommy Åstrand, was stepping down from his position and would instead be appointed to the board. We find this a bit disappointing as we believe he has done a good job and is appreciated by the market. At the same time, the most important thing for us is that Peter Strand (former CEO and now transaction manager) remains operationally active. We remain confident in our investment as we believe the company will continue to grow at the same pace as before.

Konecranes / Hiab (Cargotec) / Kalmar

At the end of March, we were in Helsinki to visit Konecranes, Hiab (formerly Cargotec) and Kalmar. The message was clear, Europe is showing clear signs of recovery - even before Germany's huge infrastructure and defense investment. Hiab has noticed a clear increase in activity in their defence segment (which we estimate to be around 7% of sales). Lead times seem to be getting shorter and shorter while demand is increasing.

While the picture in Europe looks better, the uncertainty with tariffs lies like a wet blanket over the US market. We believe that this will ease as soon as the world finds out the rules of the game. As it stands today, these are changing daily. There is a need to continue investing but companies are waiting until the guidelines are clear.

In the slightly longer term, there may also be a positive demand effect of tariffs, although it is difficult to quantify. Tariffs create changed value chains which in turn mean that factories are moved. This in turn results in increased demand for the type of products that these Finnish industrial companies offer.

Summary

The beginning of the year has been unusually complex and difficult to navigate. That said, we are of course not satisfied with the fund's performance this year. What is even more frustrating is that our companies have fared well in the recent reporting season. 18 out of 22 of our companies have exceeded market expectations. So, what contributed to the fund's underperformance during the beginning of the year?

Biotage and Bonesupport have had a weak start to the year for various reasons.

The real estate sector has been under great pressure.

The fund does not own any “war stocks”.

The fund’s country exposure has been unfavorable, as indices in Germany and Italy (where we have low exposure) have had the strongest development, while the UK and Sweden (where we have high exposure) have had the worst development.

We are disappointed with the development in Biotage, but the fact that the company is now valued at less than USD 750 million in market capitalization minus cash is, in our opinion, an extreme mispricing. We are confident that this will be corrected during the year, albeit with a somewhat back-heavy development as the first quarter is unlikely to offer any major highlights.

Bonesupport has continued to deliver strong figures, but due to being a large historical winner and USD sensitive, investors have sold the stock and bought companies with greater economic sensitivity (our view). We also took large profits when we reduced our holding by approximately a third in January. We are convinced that the company will continue to deliver strong results during the year.

The real estate sector has been weak for six months now, even though most things are going in the right direction for the sector. Valuations are, no matter how you measure them, at unusually attractive levels. The fund's largest position is currently SLP, which has fallen by 5% this year (compared to the Swedish real estate sector, which has fallen by 9.8%, and the European real estate sector, which has fallen by -6.8% in SEK). We have a very strong conviction that SLP, with relatively low risk, will generate great value for the fund for several years to come.

In retrospect, we should have allocated capital to defence stocks earlier, but now it feels inflated. Investors have poured capital into defence stocks and care less about (in our opinion) valuations. There is a risk at current price levels that this will backfire. We own other types of companies with significantly lower valuations, but which benefit from Europe's increased investments. German Traton or Finnish Cargotec/Hiab are good examples.

We invest bottom up, i.e., we invest in companies that are interesting for various reasons. We very rarely invest top down, i.e., where we have a theme and based on that we screen for companies. At the beginning of the year, the fund had zero exposure to Germany and approximately 50% exposure to the UK and Sweden. With the major changes that took place and following our analysis, we invested in three German companies in February, where Traton and GEA were new to the fund while Commerzbank was an old acquaintance.

The German SDAX (smaller companies) has risen by 11.1% this year while the FTSE250 has fallen by 5.6 and the Carnegie Small Cap Index has fallen by 3.1%, both measured in local currency. It is very unusual to have such a large spread between countries and in just three months. With our positive fundamental view of European small and mid-cap companies, we have reason to believe that this will even out in the coming quarters as British and Swedish companies start to increase in value.

On an absolute basis, the Swedish krona has negatively affected the fund's performance by 5.2% this year (SEK class). However, it has not affected the relative return.

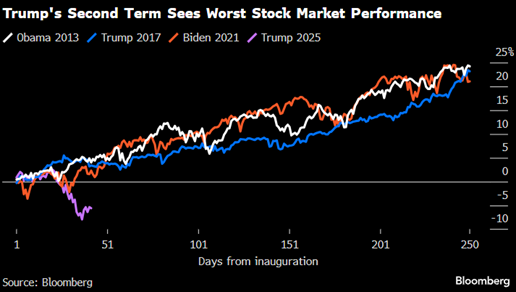

The market is so far not impressed with President Trump.

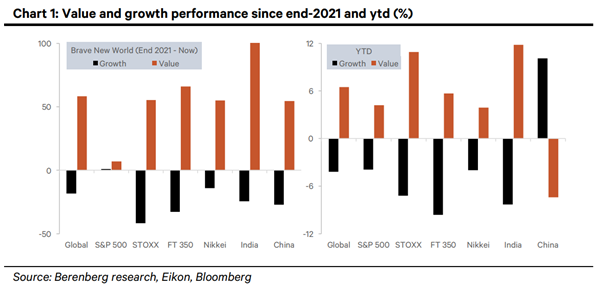

Globally, value stocks have performed significantly better than growth stocks this year. The exception is China, where Deepseek has significantly changed the global AI map.

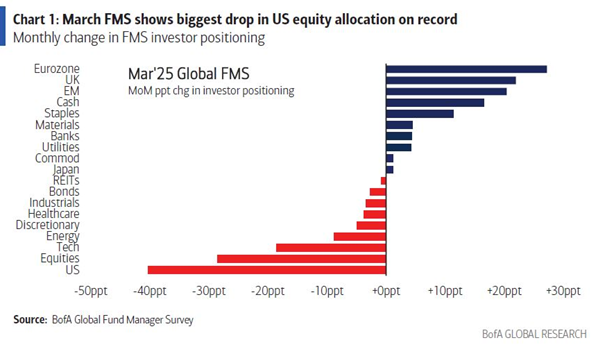

March recorded the largest monthly decrease ever in exposure to US stocks (Bank of America).

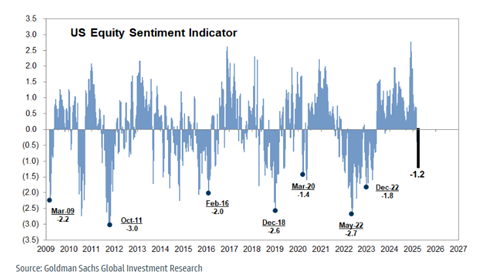

From optimist to pessimist in a short time, Goldman Sachs sentiment indicator.

Source: Goldman Sachs

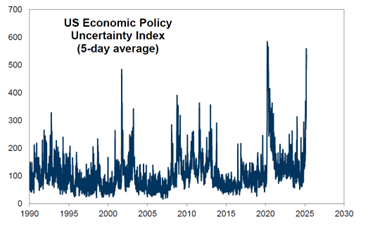

It is not difficult to understand that the stock market mood has turned downward when the political uncertainty index reaches new heights. Now it is at the same level as during the Covid crash.

Source: Goldman Sachs

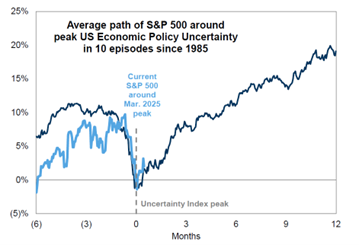

If historical performance is a good indicator of future returns, then periods of high political uncertainty are a good time to buy stocks.

Source: Goldman Sachs

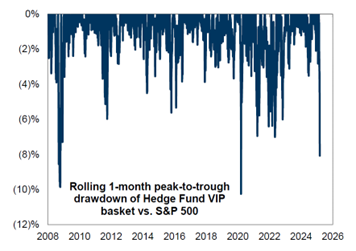

Another strong contrarian indicator is the Goldman Sachs Hedge Fund VIP Stock Index. When favorite stocks are as depressed as they are now, it's usually a good time to start buying these stocks again.

Source: Goldman Sachs

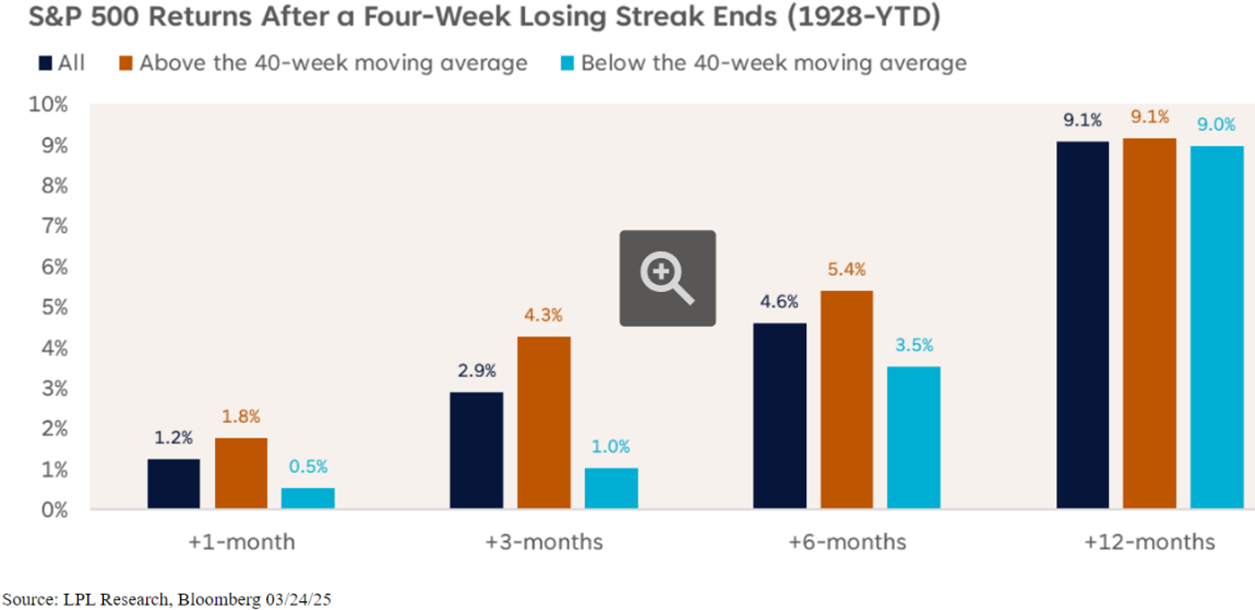

Below is a picture with statistics from 1928 showing the development after four weeks of decline for the S&P500. In the last nine weeks this year, the S&P500 has fallen in seven.

The question most people are asking themselves right now is whether the US economy, after 15 years of uninterrupted growth except for two quarters in 2020, is heading into a recession.

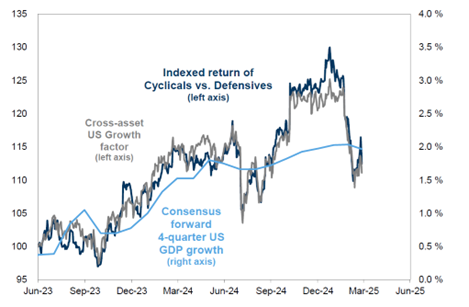

The image below shows the relative performance of cyclical vs. defensive companies (blue), and a factor index that includes several components including currency and interest rates. When plotted against the cyclical/defensive performance, the correlation is almost perfect. The light blue line shows estimates of US GDP for the fourth quarter of this year. All three curves indicate that GDP growth is currently around 1.5–2.0%. We note that Goldman Sachs just increased the risk of a US recession to 35% (from 20%).

Source: Goldman Sachs

If the Philly Fed picture below is reasonably accurate and history repeats itself, GDP will fall significantly within a month or so. We believe the risk of that is relatively high given everything that is happening. We are also getting some signals from some of our companies that activity has decreased in the US in recent weeks. The coming months will be interesting.

Source: Macrobond and Nordea

The euro has strengthened significantly against the dollar. A few months ago, experts thought the euro would go to parity with the dollar, and now they're talking about 1.20. It's swinging!

Source: Bloomberg

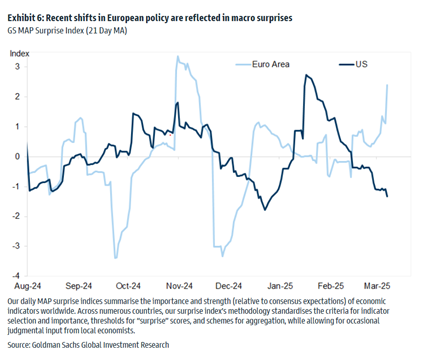

Developments in Europe have led to several positive macro surprises, while the opposite is true in the US.

Source: Goldman Sachs Investment Research

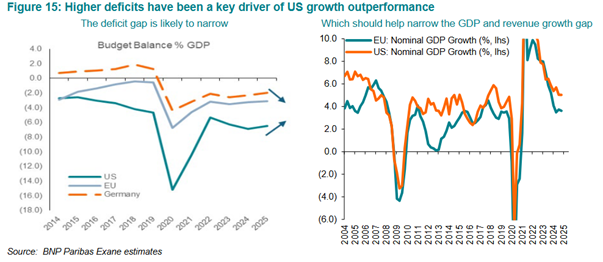

We have long wondered what developments in Europe would have looked like if they had chosen to have the same large budget deficits as in the US. We will never know, but it is indicating, with all desired clarity, that deficits in the US are expected to decrease under the new administration, while they are likely to increase in Europe due to all the new investments that have just been announced. All other things being equal, growth in Europe will therefore accelerate while it will probably decrease somewhat in the US.

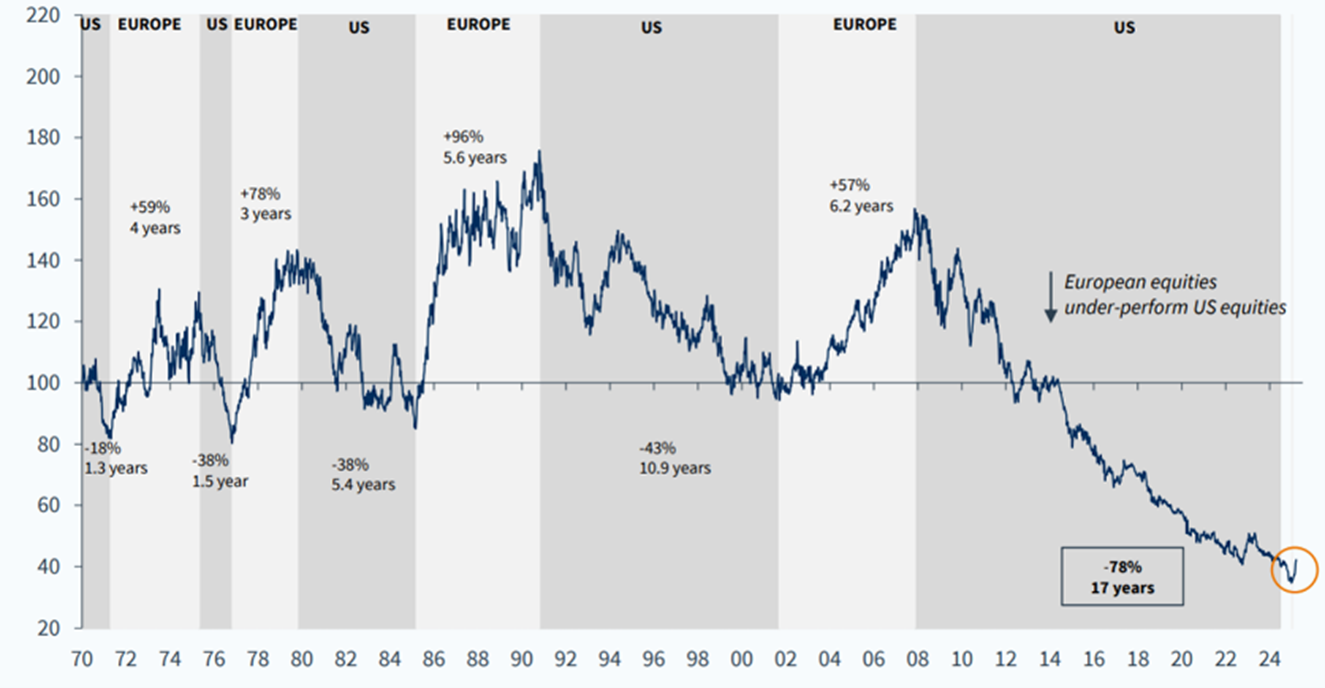

The image below shows the development between European and American stocks since 1970. The strong start of the year for Europe is barely noticeable.

Source: Goldman Sachs

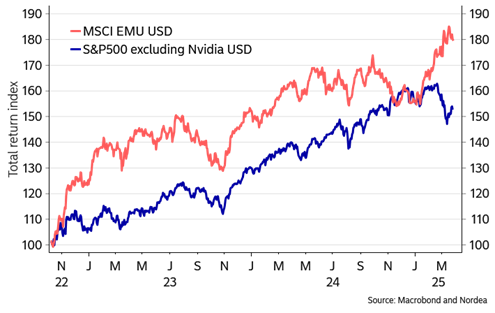

We enlisted the help of Nordea to create the image below showing the performance of the broad European index in relation to the “S&P499” which excludes Nvidia. Since the uptrend started in November 2022 and measured in the same currency, Europe has performed significantly better. Remarkable!

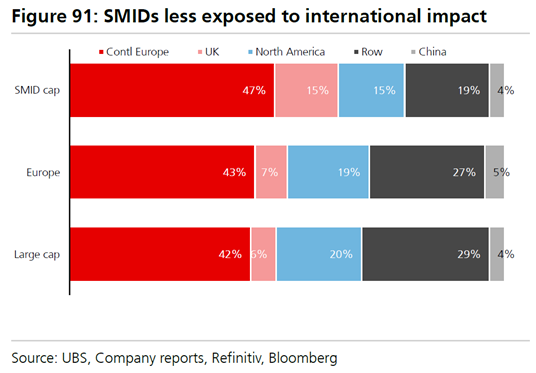

Smaller companies generally have a lower exposure to duties and tariffs, which is of course a positive, see image below.

Compared to three months ago, the valuation gap between Europe and the US has narrowed.

Source: Goldman Sachs

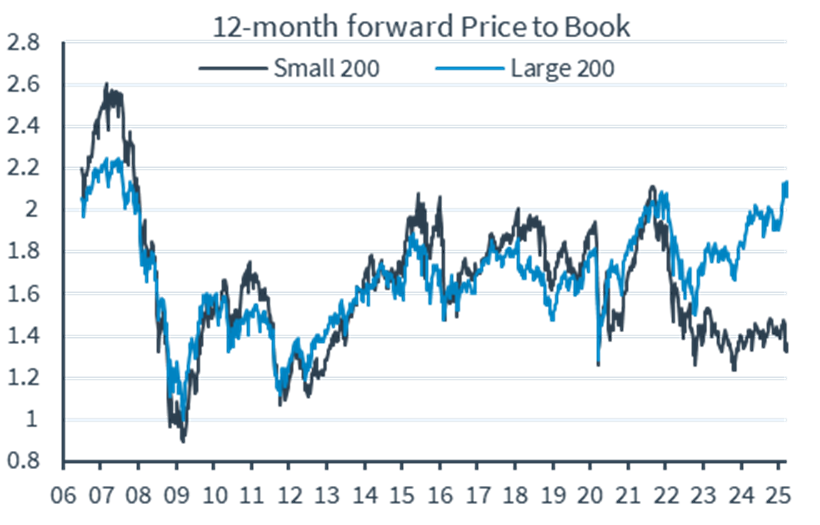

Valuations for European smaller companies relative to larger companies remain good. Below is the difference in P/B.

Source: Kepler Cheuvreux

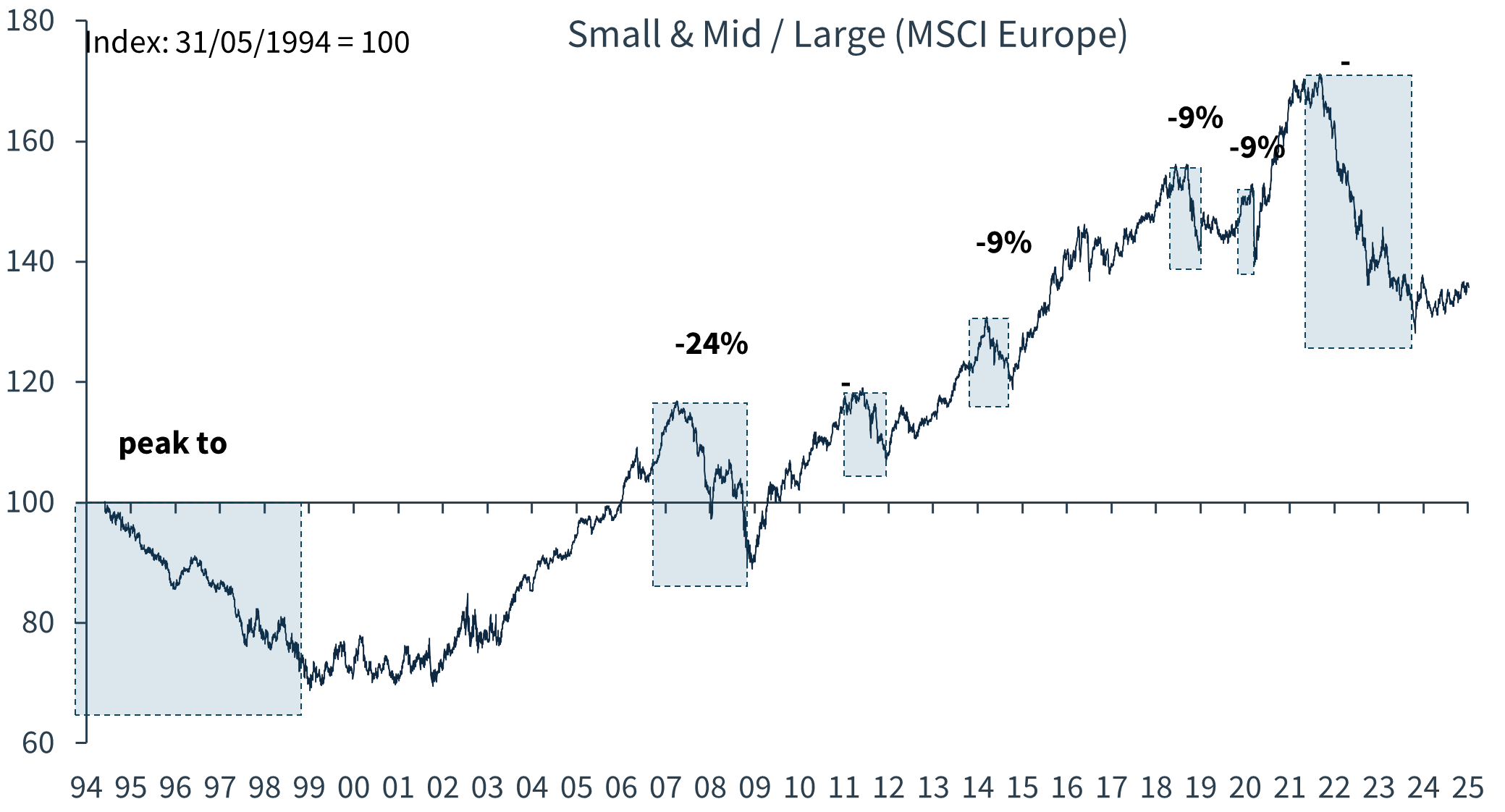

The European SMID companies have performed somewhat better than the large companies in recent months.

Source: Kepler Cheuvreux

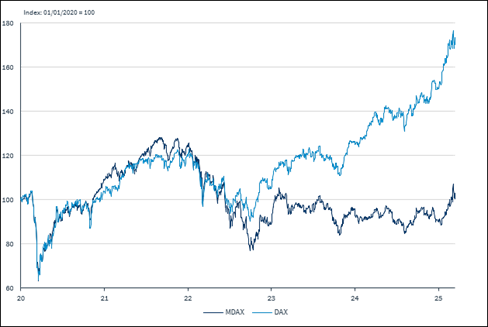

The image below shows the difference between the German large-cap index DAX (light blue) and the index for smaller companies, SDAX. If political uncertainty decreases in the future and the tariffs and their effects begin to materialise, there should be good conditions for the smaller companies to start developing stronger relative to larger companies. Valuation is lower and growth is higher.

Source: Kepler Cheuvreux

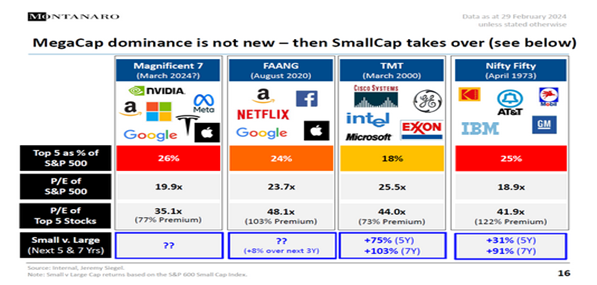

The picture below shows that when mega cap dominance has ended on previous occasions in history, small cap companies have taken over and had a strong development. Mag7 has undoubtedly broken its long dominance so now it remains to be seen whether history repeats itself for the smaller companies.

Source: MONTANARO

In summary, the developments in Europe in recent weeks are enormous and will be in the history books forever. BNP Paribas has estimated the magnitude of the German investment package (1000 billion euros). Converted, the package would correspond to the Marshall Plan after World War II and the investments for the reunification of West and East Germany in 1990 - combined!

In addition, there are likely to be positive effects from reduced regulations in Europe and an expansionary fiscal policy that will have significant effects on the German and European economy.

If there is a ceasefire in Ukraine, European energy prices will likely fall, which would in that case provide additional fuel for growth.

In addition to the above, the EU will invest a total of 800 billion euros in defence in the coming years, which in isolation is estimated to give Europe's total GDP an extra contribution of +0.5% per year for many years. It feels inevitable that Europe's growth will kick-start.

China remains a dormant joker, with the Chinese population's bank savings increasing by 10% per year while consumption remains modest. No major changes are needed to have major spillover effects on Europe's economies. That said, we have been waiting for this for several years.

Finally, and in the short term, there is a major problem that clouds the picture, and that is how the introduction of new US tariffs on April 2 will affect different countries and industries, and how Europe will respond to these. However, once the worst of the turbulence has subsided and the market begins to absorb the consequences, there should be very good conditions for interest in Europe as an asset class to persist. As much has happened in recent weeks in Europe as it has in many years, and there is no going back. We have a new world order, and the investments must be made to ensure our security and independence.

We thank you for your interest and wish you a pleasant first month of spring.

Mikael & Team

Malmö April 3, 2025

IMPORTANT INFORMATION. This is a marketing communication. Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested. Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.