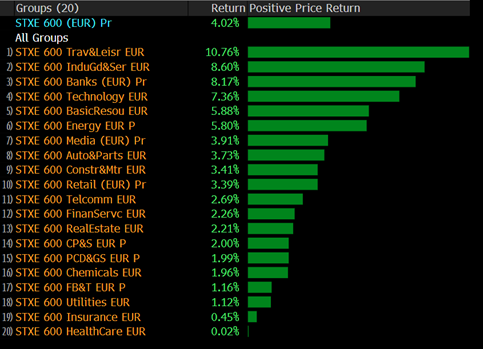

There were unusually large differences in returns between different sectors in May. Travel & Leisure was the best sector and rose by 10.8%. The fund owns two companies in that sector; Scandic, which rose by almost five percent including dividends, and Spanish HBX, which rose by a whopping 28%. HBX, which is a new company on the Spanish stock exchange and forgotten in the turbulence, presented a nice quarterly report that contributed to the rise.

Source: Bloomberg

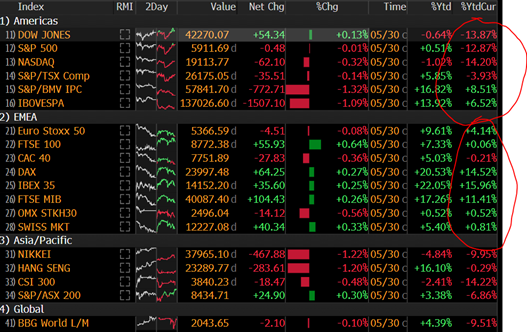

The chaos with Trump's tariffs continued even though the market reacted calmer than in April. On Friday, May 23rd, the world suddenly heard that the US would impose 50% tariffs on the EU as early as June 1st. On Sunday, after speaking with Ursula von der Leyen, Trump changed his mind and moved the date forward to July 9th. On Friday, May 30th, Trump announced that he would double tariffs on imported steel from 25 to 50% as of June 4th. The circus continues and it is extremely frivolous all around. It is inconceivable that one can communicate and pursue such bad political policy. It will be interesting to follow developments when, in the near term, American companies and consumers will, for sure, have to pay for those policy actions. The US will gradually become weaker. China and Russia are rejoicing.

Source: X

Donald Trump arranged sponsorship for a new Air Force One. The royal family of Qatar gifts the US “a very expensive plane.” Nothing surprises us anymore.

Source: X

At the end of the month, the administration suffered a major setback when the US Court of International Trade ruled that most of Trump's tariff war was illegal, and that the president had thereby exceeded his authority. The decision has of course been appealed and the tariffs remain in place for the time being. It is now a delicate situation in that the risks to the global economy and the US can now be decided in the US courts. The response was posted below on Truth Social.

Source: @realDonaldTrump

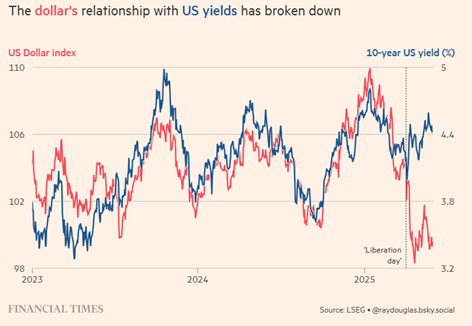

The correlation between the USD and the US 10-year yield has broken. Something seems to have happened on April 2nd……..

Source: Financial Times

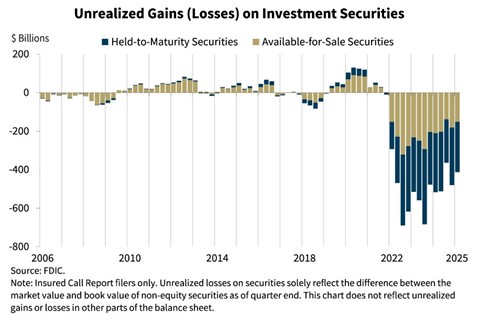

The high US interest rate has led to unrealized losses among bondholders.

Source: FDIC

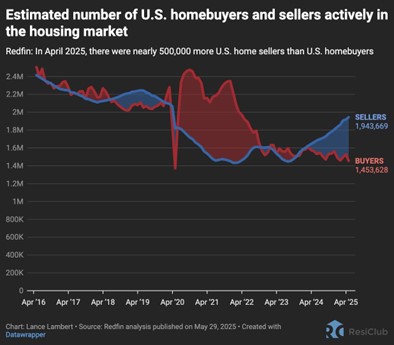

The interest rate level has also led to a strong supply of American homes. The mortgage rate in the US is now around 7%. Tariffs are unlikely to reduce inflationary pressure.

Source: Redfin analysis

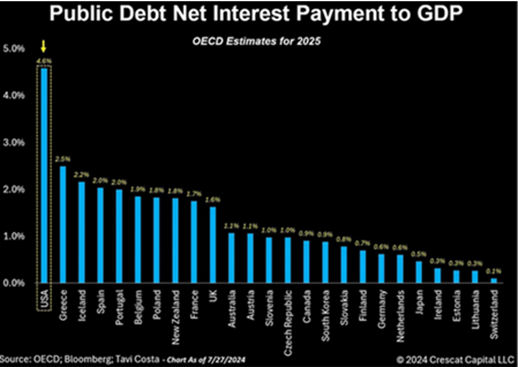

The US is now paying 5% of its GDP in interest costs. It will likely end in tears. It's unclear when, though.

Source: OECD, Bloomberg, Tavi Costa

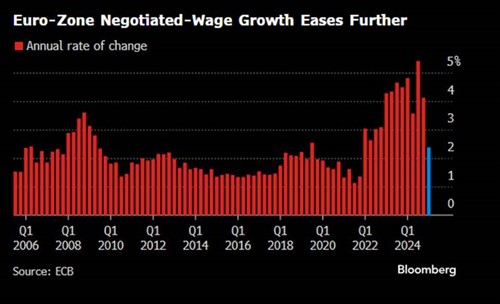

In Europe the pressure on wage hikes is decreasing, which is positive from an inflation and competition perspective.

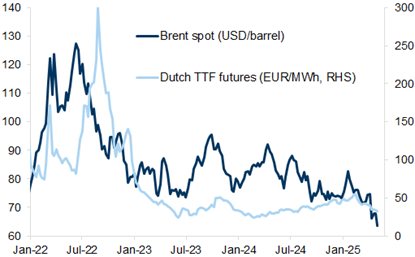

Energy costs in Europe are also moving in the right direction.

Source: Goldman Sachs

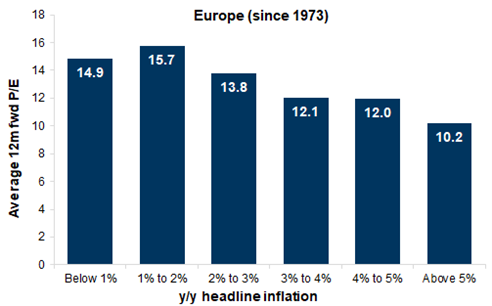

Falling inflation leads to higher valuations. The image below shows the historical P/E ratio in Europe in different inflation environments.

Source: Goldman Sachs

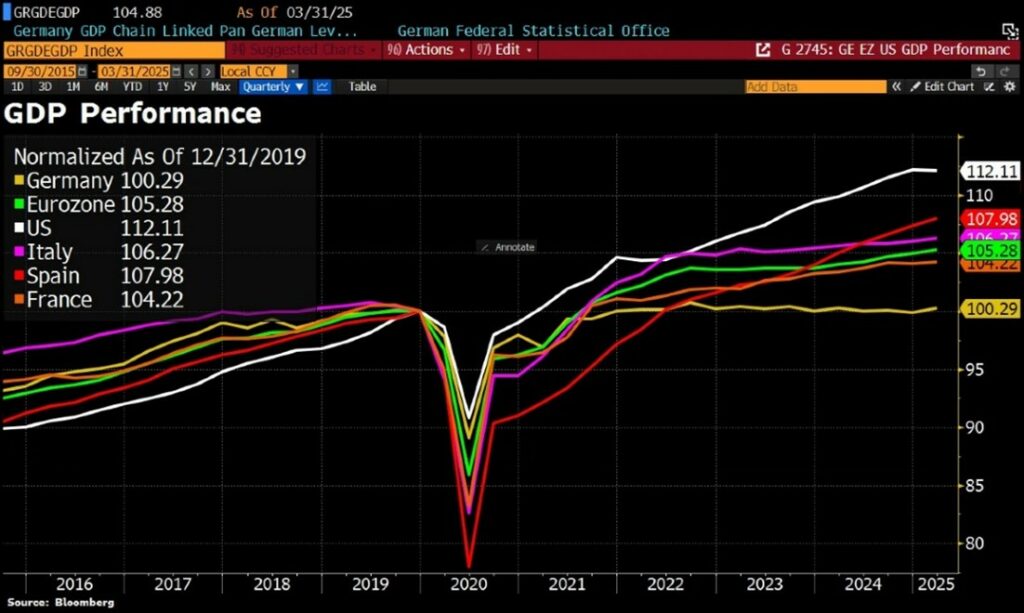

Germany, the engine of Europe, has had zero growth for several years. See the picture below where the US is clearly leading the development, partly doped by large budget deficits year after year.

Source: Bloomberg

British pension funds have agreed with the government to invest at least five percent of their assets in the UK in a bid to accelerate growth and support private companies and infrastructure projects. Good!

There is far too much capital in European bank accounts instead of in the stock market. Changes are coming with incentives for private individuals. Good and timely!

Source: Hallosafe

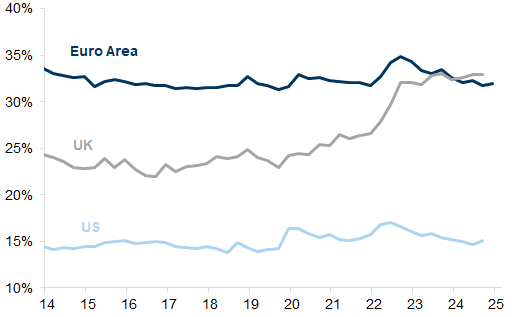

Europeans prefer cash to more risky asset allocation as is clear from the picture below showing the currency and deposits as a share of household financials assets (%).

Thanks for everything, Warren Buffett! He surprised most people at Berkshire's annual general meeting by announcing his resignation as CEO. At 94 years old and considering his contributions, it feels well deserved.

Source: Financial Times

De’Longhi’s first-quarter report may indicate that we are on to something: The company beat EBITDA expectations by 12% while reaffirming its guidance for the year. Management also gave some reassuring words regarding potential tariffs. A big difference today compared to the first “round” of tariffs from 2018 is that it is much better prepared for all eventualities. De’Longhi shares rose by 6% in May.

Lindab

Over the past few months, we have begun to see some signs of a brightening in the construction market after 2–3 difficult years. Although Lindab's ventilation segment is late in the construction cycle, and it will likely take a couple of quarters before we see a proper turnaround in operations, we believe that the share price will do well before operational development materialises. After several years of hard work with cost levels and investments in factories and machinery, the operational leverage when volumes return can be significant.

In May, Lindab's report for the first quarter was released. Operating profit beat analysts' expectations by 5–10%. The share rose by 6% during the month but has fallen by 6% for the full year.

Rotork

The British electric actuators vendor briefly reported that order intake in the first few months of the year rose by around five percent on an organic basis. At the same time, sales were slightly lower than in the previous year, partly due to a strong comparable period. Although Rotork's financial update was roughly in line with what the market had hoped for, we had hoped for slightly higher order intake.

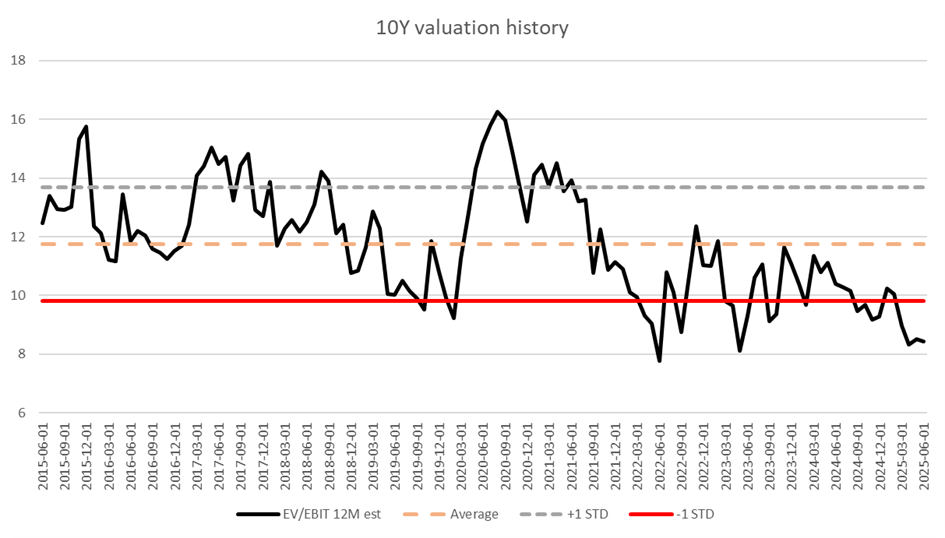

The Rotork position has not been a particularly positive contributor this year – the share price rise as of the end of May was around 0% for 2025 after a rise of 3.5% for the month. We hope and believe that Rotork can surprise on the upside when it is time for the company's half-year report. The share is valued at around 13x EBIT on the next 12 months' analyst estimate, compared with the average over the past ten years of 16-17x.

Van Lanschot Kempen

Since we wrote about private banking player Van Lanschot in our monthly newsletter for February, the share has risen by around 19%. In May, Van Lanschot released a short financial update that included, among other things, net inflows for the first quarter; during the first three months net inflows corresponded to around 12% of the year's opening assets under management, annualized. Impressive and the share rose 7% in May.

Sampo

As previously mentioned, we have believed in 2025 as a strong insurance year. The price increases from the previous year have caught up and surpassed inflation, which has given good momentum to profits. Sampo has been a good contributor to the fund's development this year with a price increase of approximately 19%. We think this is good given the low risk level in the company. Sampo's report in May was again strong with a result that was around 3% better than expected (underwriting result).

Asker Healthcare Group

In May, Asker released its first report as a listed company. The figures were roughly in line with what we want to see for the full year: organic growth between 5–7%, acquisition-related growth that at least matches the organic growth and an improved margin of a couple of tenths of a percent.

As a serial acquirer in a stable end-market, we are not surprised that the Asker share is highly valued. If Asker can build on a longer history of stable reports as a listed company, we believe that the share can be valued at the top among Nordic serial acquirers (which in turn are already valued high). At the time of writing, the share is over SEK 100 per share, which should be compared with the IPO price of SEK 70 from the end of March. We bought a lot of shares around SEK 75 per share in the stock market dip in April, and thus Asker's contribution to the fund's development has been clearly positive this year.

Asmodee

When Embracer announced its spin-off of the board game company Asmodee, we did some work on the company (the fund has a strong focus on spin-offs where we often do a lot of analytical work). At the time of the spin-off, we noted, among other things, 1) a relatively cautious guidance for the year and 2) that management had little if any incentive to “promise high” in connection with the spin-off, while 3) external indicators such as Google Trends pointed up for several important products. Overall, the risk/reward looked positive ahead of Asmodee’s report for the fourth quarter, which ended in March 2025.

In addition to the short-term play on a good report, we invested in Asmodee because we judged that the company should benefit in the long term from being an independent company. The company’s cash flows can now be reinvested in acquisitions or certain organic initiatives, which was not the case under Embracer’s ownership. When we started buying shares, we also thought the valuation looked appetizing. For these reasons, we bought a smaller position during March this year.

Indeed, the report was clearly better than expected - sales were almost 20% better than analysts' estimates and operating profit even better. This was clearly better than we had dared to guess. The share has risen by about 42% since the end of March and rose 22% during May alone. Our big mistake in this case was that we did not have a large enough position despite high conviction. We are self-critical on that point and learn for the future.

Diploma

The British serial acquirer released its report, in May, for the first half of the broken financial year ending in September. Organic growth came in at 9%, compared with expectations of 7%. Operating profit was 5% better than expected. Finally, the company's guidance for the full year was raised. Diploma appears to be relatively protected from the effects of the tariffs despite its large US exposure. The company may even be a winner; as a distributor with expertise in purchasing, Diploma could potentially gain market share in a world where purchasing logistics are becoming more difficult.

Diploma shares rose 15% on the day of the report and had risen 10% in 2025 as of the end of May.

Babcock

A new holding in the fund is the British service company Babcock. The company has a high exposure to the British defence sector in particular, which accounts for more than 70% of sales. The business model is contract-based and usually publicly procured. Babcock helps with things like technical support, system integration and training. This can involve, for example, replacing parts on combat ships, training combat pilots or carrying out routine maintenance on submarines – among many other things.

Babcock is a typical turnaround case. Babcock has historically made the mistakes that many companies with contract-based business models make – firstly, it has made many acquisitions with poor integration, and secondly, it has had incentive systems for salespeople that prioritized sales over profitability. The result of these two things has led to many years of low profitability. In addition, Babcock has struggled with pension liabilities that have significantly reduced cash flow every year.

For a couple of years now, Babcock has been governed by a new management that has slowly phased out unprofitable and bad contracts. Above all, there are completely new requirements for new contract bids; risk and profitability are the primary focus. At the same time, Babcock has implemented group-wide financial systems (the auditor has previously complained about weak financial control within the company). The worst holes from old pension sins have also been plugged, and the company's cash flow profile is therefore much better than it has been in a long time.

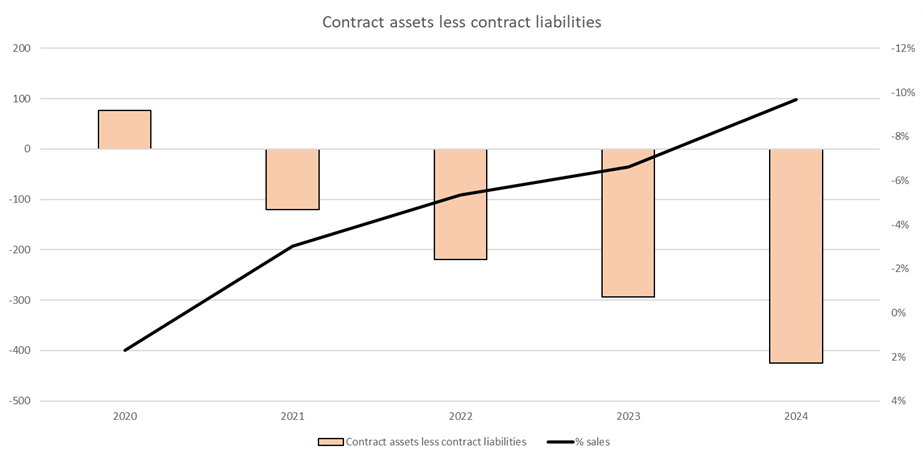

One should always be careful with contract-based business models. Especially in cases like Babcock, where contracts are often agreed over many years and where overly optimistic assumptions can lead to very negative consequences over long periods. The contract-based model also means that profits are settled based on internal budget forecasts that leave a lot of freedom for management's assumptions. For us, it has therefore been important to feel secure with the company's accounting. We note that contract liabilities (cases where Babcock has received compensation but has not yet reported these compensations in the income statement) have grown as a percentage of sales – we see this as positive and a sign that the new management is more conservative.

Our belief is that Babcock, in a more streamlined form, should be able to generate profitability of just over 8% at the operating level. Investments should be relatively small in relation to sales, which, combined with negative working capital tied up, means that Babcock should be able to generate a return on capital employed (excluding goodwill) of more than 50%. In a world where defence budgets are growing rapidly in Europe, organic growth should reach high single digits. As we see it, Babcock is well on its way to reaching these numbers.

The first phase of our investment in Babcock has been positive. Since we bought our initial shares in April, the share has risen by approximately 25% by the end of May. This is partly due to a positive financial update from the company, and partly because defence stocks continue to perform strongly in the market. Despite the price increase, we still think that the share looks attractively valued at EV/EBIT 10-11x on our estimates for 2027e. We hope to return to this at a later stage.

HBX

For a number of weeks now, the fund has had a minor position in HBX Group. HBX is a travel-focused technology company that helps hotels sell surplus rooms by distributing them through a global network of travel distributors, such as tour operators or travel agencies. The B2B model builds trust in the value chain, as they avoid direct competition for the end customer, unlike OTAs (Online Travel Agencies, such as Expedia or Booking.com). OTAs offer a wide reach but often compete directly with hotels by charging high commissions and by controlling the customer relationship. This often leads to conflicts and erodes the hotels' profitability and brand loyalty. HBX, on the other hand, is a non-competing partner that helps hotels increase their occupancy and complements the hotels' own direct bookings.

HBX filed its first report as a listed company in May. After a turbulent start to its stock market career which was fueled by Trump's tariff drama in April, the stock rose 30% during the month. The report was in line with expectations, but as we suspected, it was enough for the stock to do well after the price decline that had occurred. Projections were unusually low ahead of the report and some were probably afraid of worse results.

The company has a broken financial year, and this time reported its results for the first half of the year. Sales grew 10% to 319 million euros with an operating margin of almost 50% (before depreciation). The company reiterated its outlook for the full year. Although some customs chaos was noted in April, a normalization has already been seen in May. The weakness in the report was the operational development in the US, which was not a big surprise.

We estimate that the company can grow sales by 7% annually with an operating margin of about 50% and high cash conversion. Despite this, the company is trading at a low 9 times operating profit this year and 7.4x times 2026e.

Bonesupport

The share has been a source of sorrow for the fund this year and for the month of May. The share fell by around 20% in May without significant news. However, the number of shorted shares has increased, which likely made parts of the market nervous. We met with the company during the month and feel confident in the investment. We have also bought some shares near current levels. Based on our estimates and at today's price, the company is valued at 10x sales in 2026E and just over 30x operating profit. The corresponding figures for 2027E are around 7.5x and 21x. The company has an interesting pipeline of products to be rolled out in the coming years and sales in the trauma segment are still in their infancy.

Vallourec

Our French steel company Vallourec released its first-quarter report in May. Operating profit came in at EUR 207 million, slightly better than expected. With a strong order book, Vallourec expects the second half of the year to be better than the first, but the market is currently primarily concerned about low oil prices and investment prospects for the oil industry, especially in the US. In our opinion, this is more than reflected in today's valuation of around 7x net profit in 2025 (analyst estimate). After a major restructuring, which included a thorough clean-up of the company's balance sheet, Vallourec paid its first dividend in over 10 years in May. The dividend yield is just over 10%. The share price was unchanged in May, including the dividend.

Summary

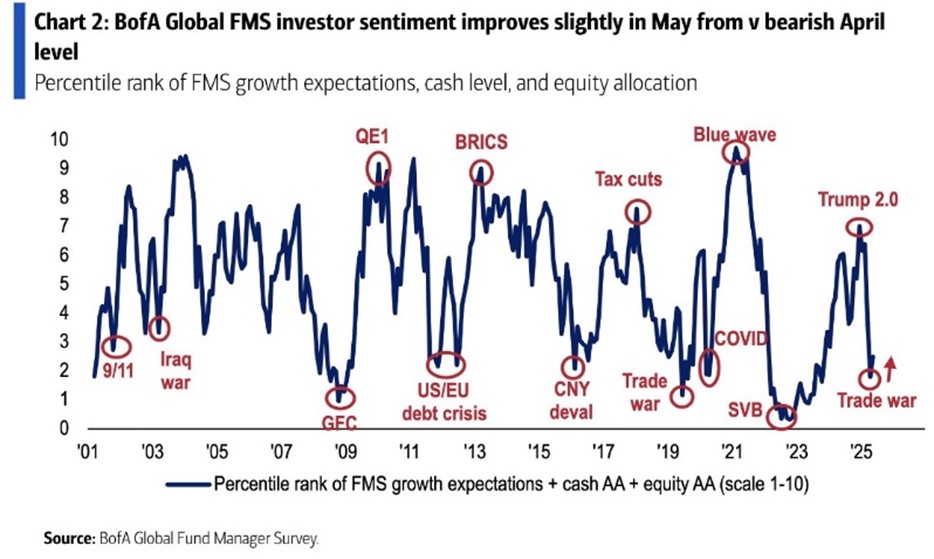

After one of the best Mays in a long time, it is clear that stock trading is not just a winter sport. The gains since the lows in April of 20-25% have been brutal (as was the decline) and the market is now close to all-time highs in the US while in some places in Europe it has hit new all-time highs. It is a rise that has been unwanted by many as the positioning towards stocks has been low, see image below, and which in turn has further driven the rise as investors have been gradually forced into the market.

We are pleased with the fund's performance during this dramatic period with few mistakes and several new large holdings that have yielded significant excess returns in a short time. Despite having had a very large cash position in Biotage (bid) since mid-April, we have performed well.

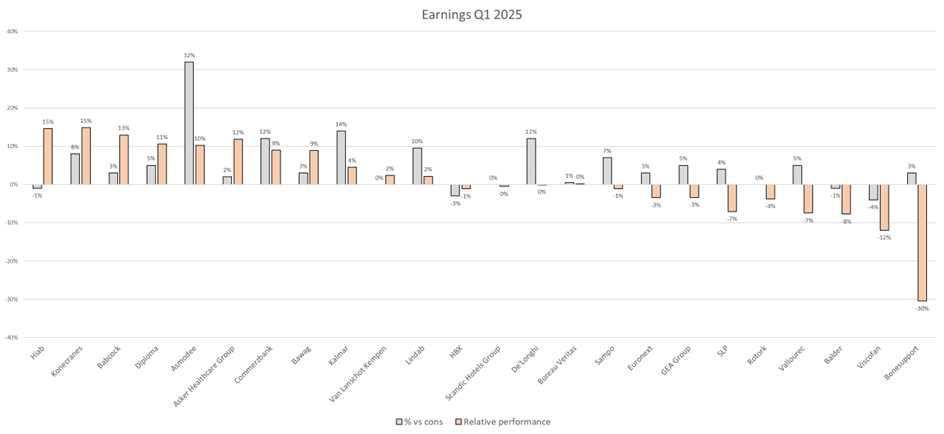

The picture below shows the outcome and the market's expectations for our companies during the recently concluded reporting season. It is not an exact science in that for some companies it is the result that we focus on while for others it may be the turnover (what we assess the market is most interested in). Additionally, for some companies it has now been 1.5 months since the reporting while for others it has been two weeks. Having said that, 20 out of 25 companies have met or exceeded the market's expectations.

Source: Coeli European

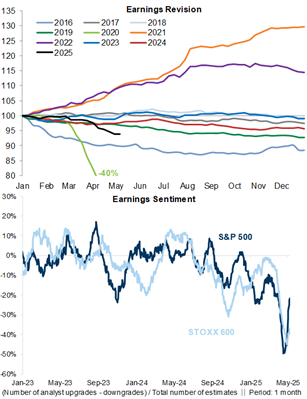

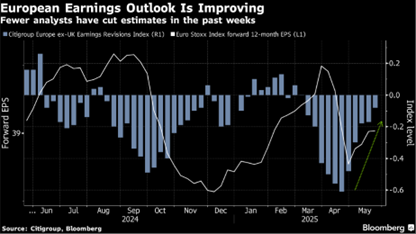

The reporting season is now completed, and the black line below shows the year's development so far with earnings expectations which have come down. The bottom image shows the number of upward revisions minus downward revisions. The US has recovered faster, and we believe this is due to an unusually strong reporting season for Mag7.

Source: Goldman Sachs

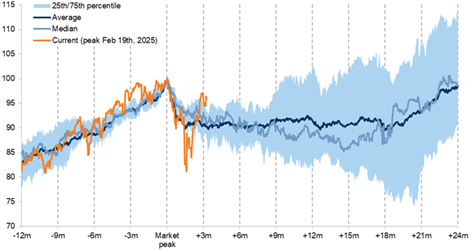

The image below shows the historical development after the market reached its peak, as well as this year's development, which is illustrated in the orange line.

Source: UBS

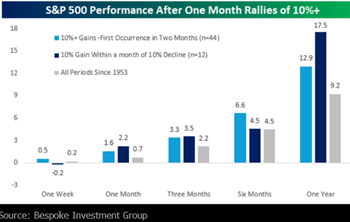

The image below shows historical development after the S&P500 rose by 10%.

Source: Bespoke Investment Group

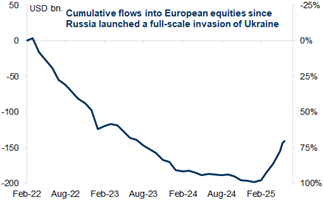

After many years of outflows from the European stock markets, this year has turned around with strong inflows.

Source: Goldman Sachs

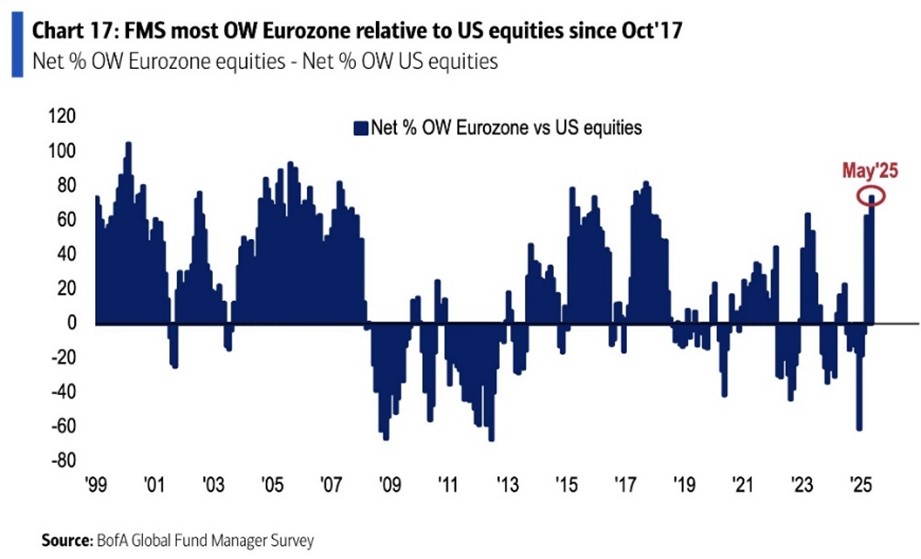

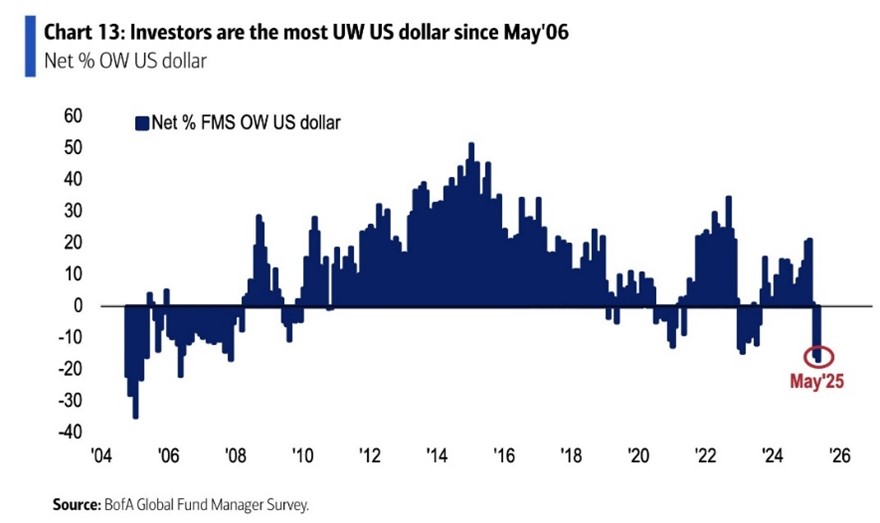

Investors have sold US stocks and the USD.

European banks are leading this year's rise for the fifth consecutive year. Since January 2022, the rise is close to 150% compared to around 40% for the big US tech companies. The fund owns Austrian Bawag and German Commerzbank in this sector.

Source: Goldman Sachs

Measured over the same period, US small caps relative to larger companies (black) and European small caps relative to larger companies (blue). European small caps have performed significantly better than US ones, likely due to significant interest rate cuts in Europe, significantly lower valuations and lower positioning.

Source: Goldman Sachs

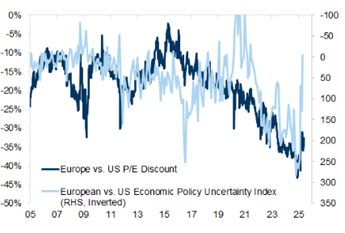

There has been some reduction in the valuation discount between European and American stocks this year. One explanation is likely to be the sharp rise in the economic uncertainty index in the United States.

Source: Goldman Sachs

8 of the top 10 stock markets in the world so far this year are European. European stocks are considered safer investments right now given all the uncertainty in the US and at the same time growth is expected to pick up in Europe. If political uncertainty is driving the shift to Europe, it will likely continue for several more years.

In conclusion, and given today's extremely uncertain political situation, it is impossible to have a strong opinion on short term market direction. We are investing our time and energy in company analysis and before summer is in full bloom we intend to have met with all our companies for an update. We are convinced that they will handle tariffs or other challenges in an excellent way.

We thank you for your interest and wish you a sunny June with school graduations, student celebrations, swimming and when it comes, the highlight of the year, Midsummer Eve! Go easy on the herring.

Mikael & Team

Malmö, 5th of June 2025

IMPORTANT INFORMATION. This is a marketing communication. Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested. Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.