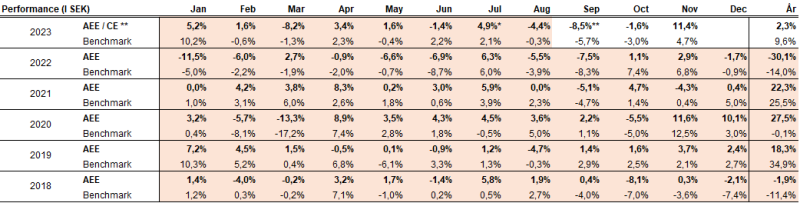

Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class' return. The information below regarding returns therefore differs from the returns in other share classes.

Before making any final investment decisions, please read the prospectus, its Annual Report, and the KID of the relevant Sub-Fund here

This material is marketing communication

Monthly Newsletter Coeli European – November 2023

NOVEMBER PERFORMANCE

The fund's value increased by 11.4% in November (share class I SEK), while the benchmark increased by 4.7%. Since the change of the fund's strategy at the beginning of September this year, the relative outperformance is +4.6%.

*Adjusted for spin-off of Rejuveron.

** AEE: Absolute European Equity, CE: Coeli European, Benchmark: MSCI Europe SMID Cap Net Total Return SEK.

Please Note: On the 4th of September 2023, the strategy of the fund officially changed from a European long biased equity long/short fund to a European active long only fund. Simultaneously, the name changed from Coeli Absolute European Equity to Coeli European. The track record highlighted in colour in the table above is that of Coeli Absolute European Equity.

EQUITY MARKETS / MACRO ENVIRONMENT

We summarised last month's newsletter with a number of bullet points, each of which indicated that the stock market could be headed for a recovery. With the November books closed, we can confirm that all indicators kicked in with full force and produced a rarely seen November rally, enthusiastically cheered on by defined falling inflation and sharply falling interest rates. That, in combination with a very cautious positioning in the market, led to some panic when capital had to be quickly put to work. As by the book, it was small and medium-sized companies that showed the strongest development, as that asset class benefits the most from falling interest rates.

The fund's strong reporting season continued in full force in November with reports from Rugvista, Diploma, Surgical Science, Sacyr, Carel, Commerzbank and Wincanton. Our portfolio rose by a whopping 11.4% in November compared to our benchmark which rose by 4.7% (both measured in SEK). It is the second strongest monthly development since November 2020 (+11.5%), and probably the best on a relative basis. We are humbly grateful that our analysis and portfolio construction produced such a strong result, and not least, that we took risks when many others did not. During the month, we exited British company, Pets at Home.

The broad European stock market rose in November by 6.5%, the S&P500 by 8.9% and the Nasdaq by 10.7%, all in local currency. The OMX30 rose by 7.6% measured in SEK and by a whopping 11.4% measured in euros, and the Stockholm Stock Exchange was thus one of the strongest stock exchanges in the Western world in November. Increased risk appetite also affected the Swedish krona, which made a remarkable comeback in November, and we will return to that later in this letter.

Developments on the world's equity markets were positive from start, but the big catalyst for the month's development was the US inflation data that was released on the 14th of November. Instead of the expected 3.3% inflation rate, the outcome was 3.2%. With a taught string and record depressed investors, a small positive deviation led to very strong gains, above all, in the small and medium-sized companies segment. The Russell 2000 rose a whopping 5.4% that day, more than double of the S&P500. Such a sharp rise for the Russell 2000 in a single day has only happened on a handful of occasions in the past 25 years.

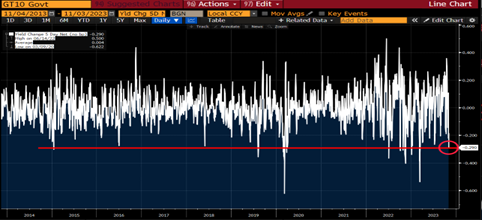

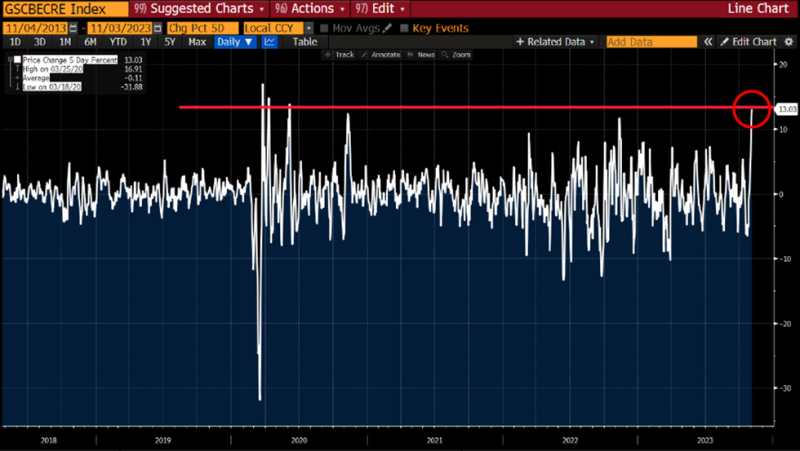

Below is five-day performance of the US 10-year bond yield. We experienced the second fastest decline since the Covid crash. High octane fuel for the stock market.

Source: Bloomberg, Goldman Sachs

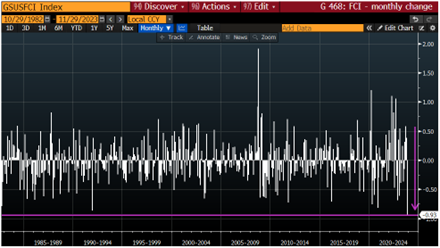

Illustrated in a different way with the picture of the month! The Goldman Sachs financial condition index improved in November with greater force than what has been recorded in the last 40 years! Unbelievable and explains both the extreme level we came from and why the recoil was so strong. Actually, the picture explains the entire development of the month of November.

Source: Bloomberg, Goldman Sachs

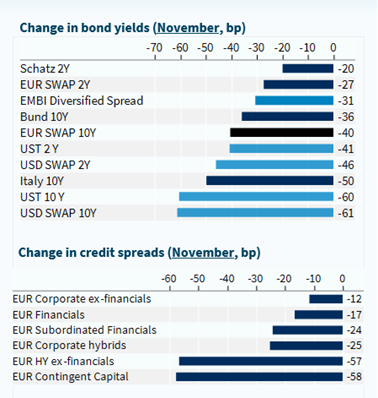

The development of various interest rates and credit spreads in November.

Source: Kepler Cheuvreux

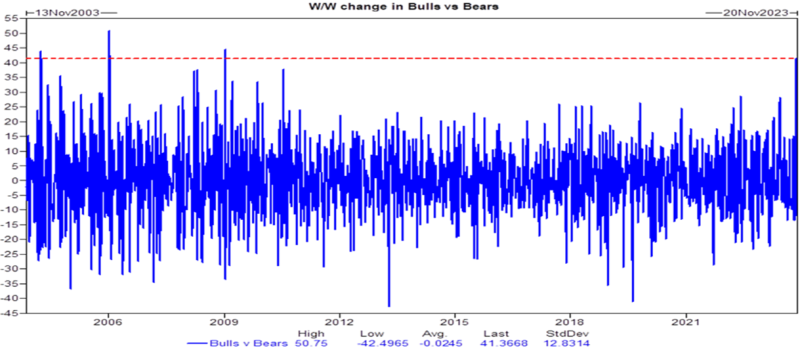

The rate cuts led to a huge shift in sentiment. The bull/bear change measured over five days was the largest since 2001 and 2008, see image below. A huge shift.

Source: Goldman Sachs

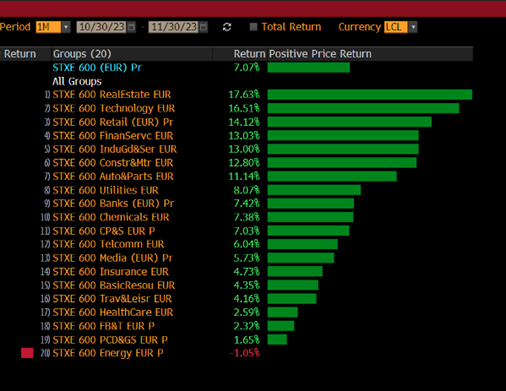

In terms of sectors, real estate was at the top, followed by technology and retail/consumer companies. The consumer is also starting to wake up with real wage increases next year, while interest rates will fall. Sweden lags behind in this development, but follows the same pattern.

Source: Bloomberg

For the second quarter in a row, German real wages are rising.

Source: Bloomberg

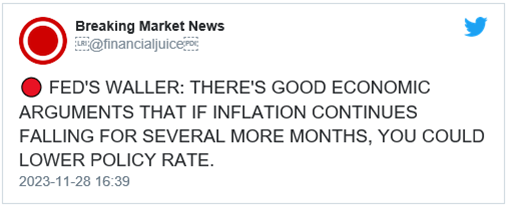

When FED minister, Christopher Waller, tweeted the following at the end of the month; the “higher for longer" theme died. Our view, for a long time, is that the central banks will cut interest rates significantly earlier than communicated, and we would not be surprised if the FED cuts the policy rate already in the first quarter of next year. The market's expectations are at mid-point of the year. The ECB will likely cut rates in early 2024.

Source: X

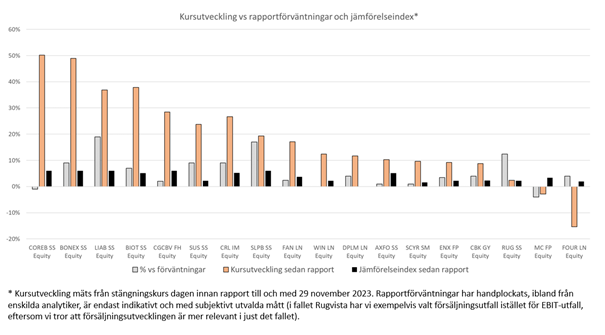

Where did all our excess returns come from in November? Below is a picture showing the price development of our various holdings since the report date (some from October) in relation to the development of our benchmark, as well as the Q3 results in relation to the market's expectations. A notable excess return from several holdings, which is the result of proprietary analysis at its best. Despite severe price pressure unrelated to the company's fundamental conditions we gradually increased in several holdings, which paid off when the rebound came.

Source: Coeli European

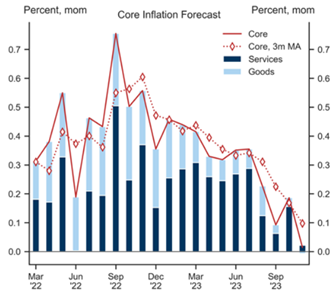

On the last day of the month we received inflation data for the euro zone, which is now trailing at 2.4% against the expected 2.7%. It is falling rapidly now, which is very pleasing, and we may well be below two percent before the end of the year. A utopia six months ago. The figure below shows that month-on-month European core inflation is now unchanged.

Source: Goldman Sachs

Risk on also applied to the Swedish krona, which in November strengthened by 3.5% against the euro and a full 6.5% against the US dollar. This despite the fact that the Riksbank (Swedish Central Bank) kept the policy rate unchanged (we applaud the Riksbank!). On the theme of risk on, we are happy to note that even Swedish small and medium-sized companies started to get into the spotlight again, after being considered pariahs for the past 23 months. Foreigners probably accounted for part of the purchases, which creates demand for Swedish kronor. Foreign ownership on the Stockholm Stock Exchange has decreased from 40% to 37%in two years. One percentage point corresponds to approximately 100 billion, which undoubtedly has a significant impact on the kronor exchange rate. On 1st of December, the krona strengthened by a further 1.2% against the euro.

The Carnegie small company index rose by 11.4% in November. Measured in USD, the rise (are you sitting down?) was a mind-boggling 18.9% and was thus, likely, the month's best asset class within the western world's stock markets. The Russell 2000 and MSCI SMID rose by 8.8 and 11.7%, respectively, measured in USD. This was of course also something that benefited the fund's development as we have approximately 35% exposure to Sweden. If you want exposure to technology and fast-growing companies, the Swedish stock exchange is superior to the rest of Europe. In addition, Swedish management and shareholder friendliness are of high quality.

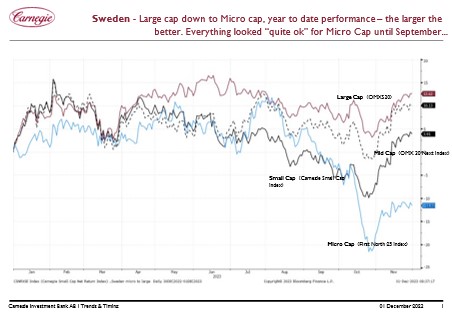

Below is the development this year on the Stockholm Stock Exchange. The bigger the company, the better, but the recoil for smaller companies has, so far, been stronger.

Source: Carnegie

On the other hand, the Swedish political landscape leaves something to be desired (expressed politically correctly so that no one is offended). Sweden ends up at the absolute bottom in terms of GDP growth this year and probably next year as well. How did we end up here? Despite this, it does not prevent us from continuing to have an overexposure to Swedish companies that have a high exposure outside of Sweden.

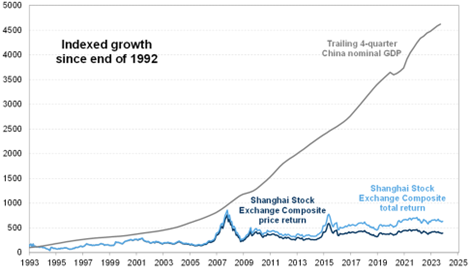

As you know, things don’t always turn out as planned. The image below shows the development of China's GDP and the Shanghai Stock Exchange since 1993. The Chinese are probably also wondering what went wrong.

Source: Goldman Sachs

There were several cheerful events in the November darkness. President Xi flew over to San Francisco and met with President Joe Biden for the first time in a year. The meeting was considered a success, from a low level. After the Chinese delegation left, Biden held a press conference where he said Xi is a dictator. It's hard not to laugh when you see Foreign Minister, Anthony Blinken’s, facial expression.

https://twitter.com/jason_howerton/status/1725254297552933177

Source: X

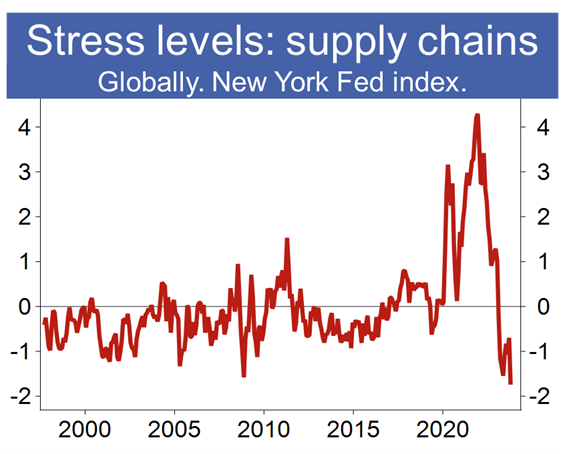

The bottleneck problems that plagued the manufacturing industry and consumers for several years are now a thing of the past. The New York Fed index records a new lowest level since statistics began to be kept in 1997. Never has the stress in the systems been measured at a lower level than now. Very positive.

Source: SEB, New York Fed

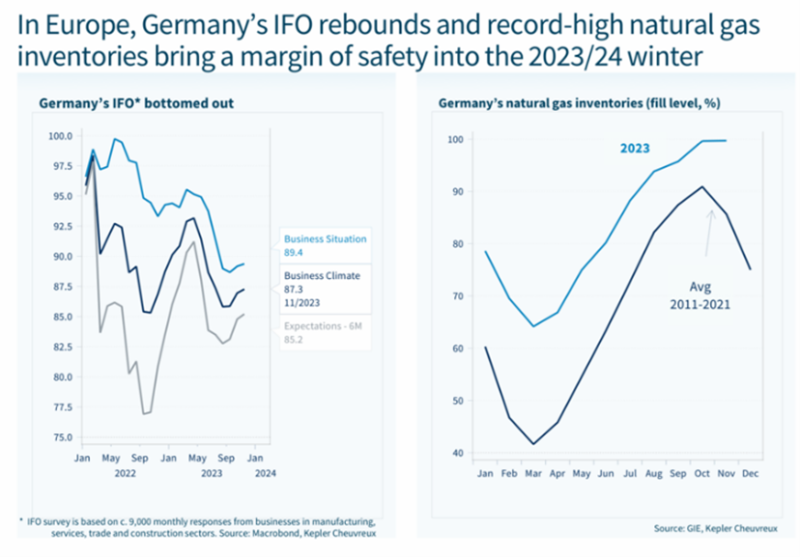

The European engine is stuttering precariously, but there has been some recovery lately. In terms of energy supply, gas supplies are well covered compared to last year.

Source: Kepler Cheuvreux

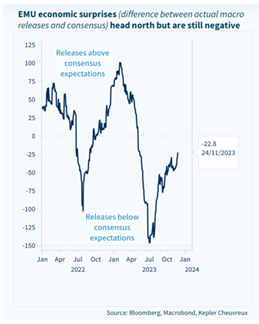

The European economy as a whole has started surprisingly positively in relation to market expectations. Still negative territory, but rapidly moving in the right direction.

Source: Bloomberg, Macrobond, Kepler Cheuvreux

In the country “Different” the union has ended up in a big fight with Tesla as it had the audacity not to join the collective agreement. Admittedly, it is not a legal requirement to have a collective agreement, but mostly to justify their own existence (personal view), they have done everything possible to oppose Tesla who led the entire world's car industry toward the electrification of the car fleets. The union has even made sure that Tesla does not get their mail handed out. Absurd to say the least. Everyone who is on strike receives 130% of their salary in compensation. It doesn't feel right, the timing is lousy for Sweden and the responsibility for the outcome rests heavily on the trade union movement.

Elon Musk came under fire after a post on X that encouraged an anti-Semitic conspiracy theory. Afterwards, he apologized and said that anti-Semitism was not his intention. Elon Musk was clear to X customers who, because of this, threatened to stop advertising on X at the end of November. The point of the video is that the odds of him giving way to the Swedish trade union movement are not playable.

https://twitter.com/greg_price11/status/1729991837958414573

Källa: X

On November 29th, one of the biggest investors passed away. Charlie Munger turned 99 and we thank him for all the knowledge he has generously shared over the years. We take the liberty of including some personal favorite quotes:

”The big money is not in the buying and the selling, but in the waiting.”

“It’s amazing how intelligent it is just to spend some time sitting. A lot of people are way too active.”

“There is only one way to the top: hard work.”

PORTFOLIO COMPANIES

Wincanton

In November, the British logistics company Wincanton released its half-yearly report for the fiscal year ending in March 2024. The figures as such were already known as the company previously released a trade update, and therefore the report release itself was not particularly dramatic. On the other hand, the management told us what they intended to do with the cash flow freed up by the fact that the company no longer has to pay off a large pension debt, which has swallowed around 35% of the company's free cash flow in recent years (we wrote about Wincanton and the pension debt in our monthly newsletter for September).

Wincanton plans to make a series of organic investments with short payback periods, some as short as three years. The investments will mainly be made in the automation and robotization of warehouse work, which is still largely carried out manually. In addition to this, Wincanton has launched a buyback program of shares, something we strongly desired and communicated. As far as we know, this has not happened in the company's history before, which says something about what management thinks of the company's low valuation. The stock rose 15% in November.

Diploma

Since August, we have built up a position in the British acquisition company Diploma. We have monitored the company for long, which in our opinion is one of the finer acquisition companies in Europe but we have always found the valuation to be difficult to justify. After a weaker price development in 2022 and a 2023 that developed sideways, we thought we were in a good position to buy the stock.

Diploma is a value-added distributor of products that on the surface are quite boring: it can be about cables, screws and nuts, reagents, cylinders and more. The beauty in this is the business model. Diploma's products tend to be cheap for the customer, but have a critical function in their workflow. Typically, the products are consumables (and not capital goods), which the customers use on an ongoing basis in their business - this dampens the cyclical sensitivity. The impression is that Diploma is in a good negotiating position in terms of price because it is often complicated/unjustified for customers to change suppliers.

The acquisition strategy is based on buying smaller distributors with high gross margins, which often indicate high service levels and good pricing power. Most of the acquisitions are of a minor nature and are bought at low multiples (around 5-7x EBIT), which gives a short payback period on invested capital. The acquired companies continue to be managed in a decentralized manner, while Diploma likes to take advantage of low-hanging opportunities for sales and profitability synergies.

Since 2007, the company's earnings per share have increased by approximately 15% per year. Diploma's full-year report covering the financial year ending in September was released during the month and was a continuation of the beaten path. Unlike many other companies, a strong and positive outlook for 2024 was also communicated. Feel free to study the numbers in the table below, impressive to say the least. The stock rose 18% in November.

Source: Diploma plc

Euronext

Another new holding in the fund is Euronext, which owns and operates several European exchanges, including Paris, Amsterdam and Milan. Traditionally, Euronext's revenue has largely come from equity trading. It is a revenue stream that is undervalued in the market because it is volatile and unpredictable. Since 2018, however, the share of income from equity trading has fallen from 34% to today's approximately 18%. Revenues that are not directly related to volumes, such as data and clearing services, today make up almost 60% of total revenues.

The change in the revenue mix should, all things being equal, in our opinion, have led to a positive revaluation of the share. When we started buying shares in August, the reality was the opposite; Looking at the forward-looking P/E ratio, the stock was valued at around its lowest levels since its IPO in the mid-1990s. After a good Q3 report, the stock rose 16% during November. On our estimates, the stock still trades at a P/E ratio of 12-13x for 2024. We think that is too low for a company that is increasing the proportion of predictable revenues and that has a near-monopolistic position in certain markets.

Carel

This year we have gradually built up a position in Italian Carel, which produces and sells control solutions, humidity controllers and dehumidifiers. Like many of the Italian companies we look at, Carel is family-owned, located in northern Italy, and has a fine history of high organic growth with a good return on capital employed. The organic growth is supplemented by one or a few acquisitions per year. During November, the company released a report that beat expectations, and the stock rose 22% during the month.

Surgical Science

Surgical Science stock had fallen sharply ahead of its Q3 report. We saw a bit of a beach ball effect when the report was then released. EBIT expectations were beaten by around 9%, which was met with relief by the market. The report and a positive market contributed to the share rising 35% in November.

Rugvista

After six quarters of negative organic growth, Rugvista reported organic growth of 14% in its Q3 report. The company has been working for a long time on a new launch of its website, which is intended, among other things, to improve the conversion rate (the proportion of customers who visit the website and who also place an order). We are starting to see the results of this in the numbers now and expect further improvements on this point in the coming quarters.

We continue to like Rugvista as the fund's play on e-commerce. The products have unusually high gross margins for their sector (around 62-63%) and profits are valued low. Perhaps there could be a change in the valuation when the market takes note of the internal improvements Rugvista has made over the past year. With any luck, maybe lower inflation figures can start to give some courage to consumers too? Regardless of the economic climate, Rugvista has a lot of power steering. We also note from several quarters that the structural migration from brick-and-mortar to e-commerce may be on the way back after a gap year in 2022, which was affected by the reopening of society after the pandemic.

The stock rose 14% in November.

4imprint

The clear loser of the reporting period was 4imprint. Not because their reported numbers were worse than expected - on the contrary, they raised the 2023 profitability guidance by around 4% - but the management was cautious in their statements regarding the future. 4imprint's products often form part of the customers' marketing budgets, and when the macro economy begins to falter, it is often a rope that many companies tighten. Historically, there has been a climate where 4imprint has taken large market shares, which benefits the company in the long term. The share fell -15% in November.

Cargotec

We described last month's valuation of Finnish Cargotec as almost unbelievable. In November, the stock became one of the fund's best contributors. Not much has happened other than that MacGregor, Cargotec's business segment which is in the middle of a turn around, received two large orders during the month. Kalmar also got a new CEO as part of preparing the company for a separate listing. The stock rose 24% in November.

Bonesupport

Bonesupport was once again a strong contributor to the fund's results. At the end of the month, the company held a capital market day that showcased Bonesupport's future visions. One area that was touched on at the Capital Markets Day was the number of clinical studies done on Cerament G. Cerament is the product backed by the most clinical studies on the market in its niche. The company continues to add more studies on an ongoing basis and 2022 was no exception.

As we previously speculated, the company will apply for approval for the indication spinal fusion. This adds a potential market of an additional 750,000 procedures annually in the United States. This doubles the potential market from today's approximately 770,000 procedures. An interesting thing is that the company has already noted that their first product, Cerament BVF, is used in spine fusion already today by some doctors, despite the fact that the company does not have a marketing permission.

Bonesupport also upgraded its sales target for 2024. Sales have really strong momentum and we believe it will continue into 2025. Europe still has a huge healthcare debt in terms of defaulted surgeries after the pandemic. At the same time, the company enters the spinal fusion market. In addition, the penetration of existing markets with existing products continues. After 2026, one can probably expect growth from new geographies such as France and Japan but also Cerament G/V for spinal fusion in the USA.

Regarding profitability, the company said that it is possible to roughly double the sales of the existing organization, but that it will not be shy to invest more to capture opportunities when they arise. The incremental margin in Q3 was 42%, which we believe is closer to the long-term margin Bonesupport will have.

The company is in the process of building the platform we previously wrote about and expected. Given how Bonesupport has taken market shares historically, we believe that the company is moving towards a bright future in new indications. After all, bones heal in the same way regardless of where in the body the bone is.

Corem

Real estate had a strong month. The Swedish real estate index rose by almost 19% during November, driven by interest rates around the world coming down sharply. Apart from that, Corem sold properties in Copenhagen for SEK 3.9 billion, which were part of the letter of intent from October. This is clearly positive as the properties in Copenhagen are low-yielding and those where expensive financing can be covered after the sale. The stock rose 23% in November.

SLP

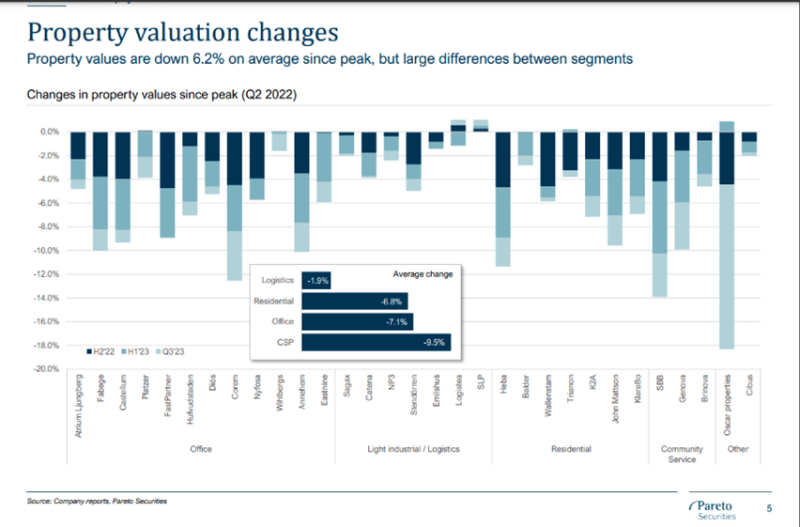

SLP also had a strong month. The major event during the month was that the company made a directed issue to a number of Swedish and international investors. The transaction was made at approximately 15% premium to the net asset value. On a single transaction, it can thus be said that SLP creates value by adding cash, which is valued 15% higher inside the company than outside. The money is to be used to buy properties in a state where there are likely to be some stressed sellers with strained balance sheets. We guess that SLP can basically pick and choose among items that stressed sellers want to get rid of. We are convinced that the capital will be put to use within a few months. Below is a picture showing how Swedish real estate companies' valuations have changed since Q2 2022. Note SLP's increase in value. Impressive in this climate.

Source:Pareto Securities

SUMMARY

After three record gloomy autumn months, we experienced a strong recoil in November. The rally started when the S&P500 hit a 100-day low, which was then followed by seven straight days of positive returns. It has only happened once before in the last 40 years and that was on March 20th, 2003 (a date that marked the end of the bear market at the time). Compared to the level from the end of July, the broad European index recovered 74% of the autumn's decline. The corresponding figures for MSCI SMID and S&P500 were 66 and 95%, respectively.

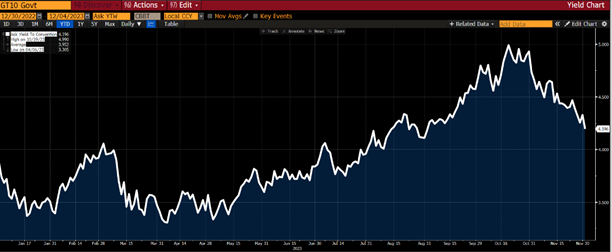

Simplistically, you can say that a rising interest rate lowered the stock market after the summer and that was also what caused the rise in November when it fell. Below is the development of the most important reference interest rate this year, the American 10-year old government bond, which also rapidly continued downwards on December 1st.

Source: Bloomberg

The European property sector has been under pressure for almost two years. Last year, the European real estate index fell by 40%, and as of November 30th, has risen by 2.9% this year. Since the lowest level in October, the index has risen by 24% and on December 1st by a further 2.3%. The country that has undoubtedly been the most affected among real estate investors has been Sweden. The corresponding figure for the Swedish real estate sector was –44% in 2022, as of November 30th unchanged this year, since the lowest level in October up by 25% and on December 1st up by 1%.

Performance for the sector was explosive in November, with Goldman Sachs' basket of shorted real estate stocks up 13% in a week, the biggest one-week gain since Q2 2020. What was even more interesting, we think, is that in the single strongest day for European real estate stocks the four stocks with the biggest increase were all Swedish! That says a lot about how badly the Swedish real estate sector has been shorted and underinvested. Our holding in Corem rose by 18% that day.

Source: Bloomberg, Goldman Sachs

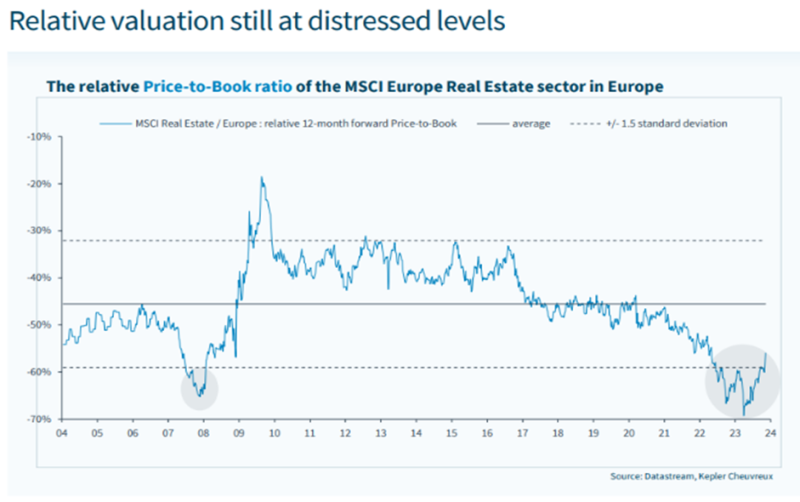

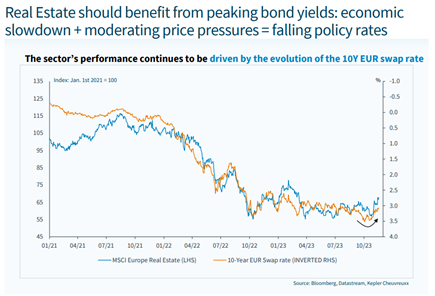

The relative valuation of the real estate sector is still at low levels.

Source: Datastream, Kepler Cheuvreux

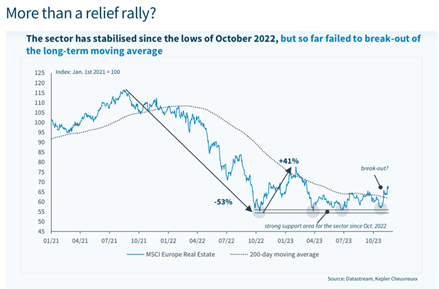

Will we see a breakout from previous trading patterns this time around? We think it is likely.

Source: Datastream, Kepler Cheuvreux

Our overall view of continued falling inflation and thus also interest rates will provide further fuel to a hard-hit real estate sector. Arguably, the sector should be among the winners in 2024.

Source: Bloomberg, Datastream, Kepler Cheuvreux

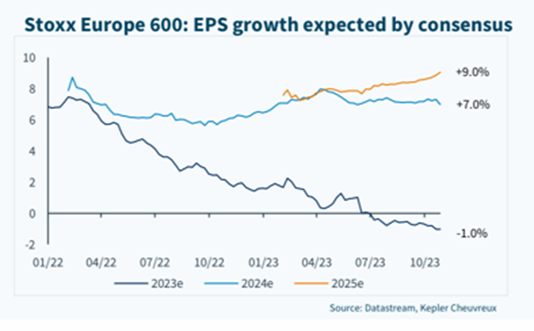

For the entire European stock market, the profit estimate looks like below. Profit expectations for the current year have gradually fallen. Profit growth for 2024e and 2025e is estimated at 7 and 9%.

Source: Datastream, Kepler Cheuvreux

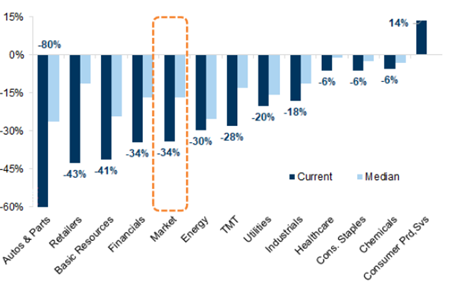

The valuation difference between Europe and the US is still at record high levels. The difference per sector is illustrated below.

Source: Goldman Sachs

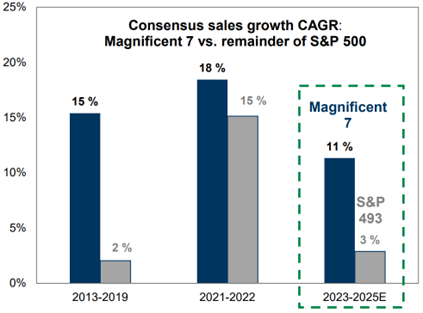

A telling picture that explains the difference between the big technology companies and other companies.

Source: Goldman Sachs

An image that shows in an exemplary way how far the FED has come in the fight against inflation. It shows inflation minus the FED's key interest rate and a lot of pain lies behind the development in the curve, but so far the American economy has fared much better than expected.

Source: Goldman Sachs, Bloomberg

We don't know much about Bitcoin and with a decline of 64% in 2022, it was hardly the uncorrelated asset that many thought. If the development within bitcoin says something about the general risk appetite (unclear to us), we note that the rise this year right now is around 140%. Five years of development below.

Source: Bloomberg

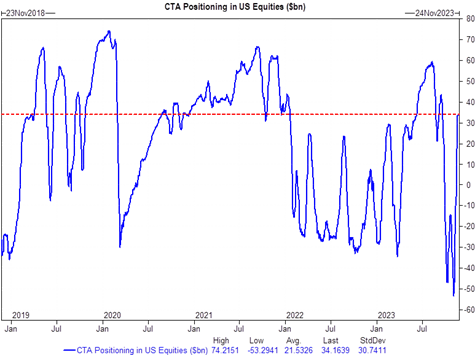

CTAs had a low exposure when the rally started a month ago. After massive purchases in recent weeks, around $235 billion, they now have a neutral exposure.

Source: Goldman Sachs

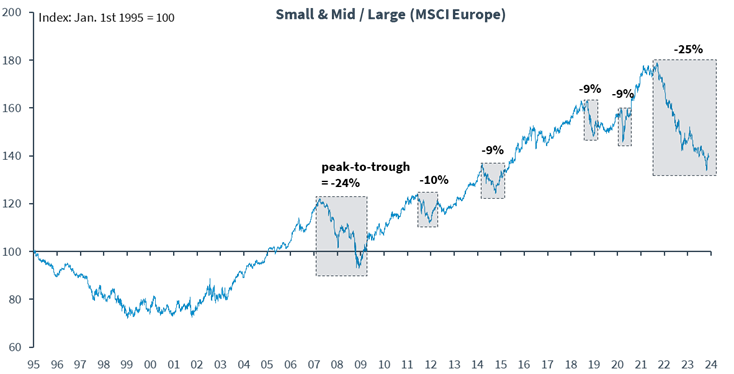

Below one of our favorite pictures. The absolute bottom level for smaller companies' share price development in relation to large companies has passed for this time (we think). Despite a strong development on a relative basis, there is a long way to go before the underperformance of the past two years has been recovered.

Source: Kepler Cheuvreux

We end this month's letter with the same picture as last time. It was a rare and great opportunity to buy shares last month and we're thankful we shamelessly took it. We believe that December will also provide a positive return, albeit not at the same levels as in November, and thus another equity year has gone down in the history books.

Source: Goldman Sachs

Despite major geopolitical challenges, the conditions ahead of 2024 look significantly better than they have been in the past two years. Now the economies will settle and the debate between whether there will be a hard or soft landing continues. Interest rates will fall back and as usual it will not be a smooth development, but we will experience both positive and negative surprises. Once the new conditions have been calibrated, we hope and believe that we will enter a more normal existence, where micro means more than macro. A development that benefits our business.

I would like to take this opportunity to thank my team for a very strong contribution during the year. Circumstances have been challenging at times, but the precision of the craftsmanship has been high. Of course, we also thank the people behind our companies. Even there, the circumstances have been challenging and you have all made a phenomenal contribution in your respective businesses!

Finally, we of course thank you, our investors, who are a prerequisite for us to be able to conduct our business.

Merry Christmas and a Happy New Year!

Mikael & Team

Malmö, December 5th 2023.