Monthly Newsletter Coeli European – November 2024

This material is marketing communication.

Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class’ return. The information below regarding returns therefore differs from the returns in other share classes.

Before making any final investment decisions, please read the prospectus, its Annual Report, and the KID of the relevant Sub-Fund here.

November Performance

The fund’s value increased by 0.4% in November (share class I SEK), while the benchmark increased by 1.3%. Since the change of the fund’s strategy at the beginning of September last year, the fund’s value has increased by 22.1% compared to an increase of the benchmark by 11.7%.

Source: Coeli European

* Adjusted for spin-off of Rejuveron

** Includes September 1 (strategy change to long-only implemented September 4 2023)

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

Equity Markets / Macro Enviroment

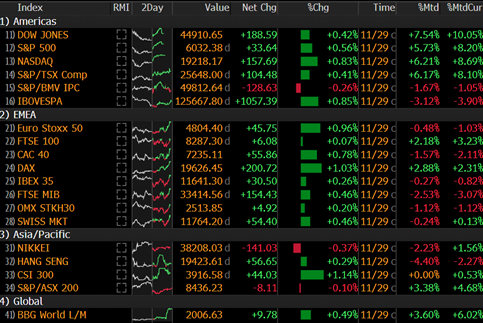

Where does one begin after everything that has happened in the last few weeks? For the world's politicians, economists and investors the starting point and epicentre is the consequences of the US election where the US president-elect is named Donald Trump. It was an historic event in many ways and one which has already left a big mark on the world's financial markets. The fund rose by 0.4% during November compared to the benchmark which rose by 1.3%. Some other reference indices show the SXXP600 +1.0% and Russell 2000 (US small caps) +10.8%. For the full year, the fund has risen by 14.4% compared to the benchmark, which has risen by 12.1%.

The image below shows November's development for several different markets. Second to the right in local currency and to the right of that measured in Swedish kronor. The conclusion is that the USA wiped the floor with Europe. November was the best month for US stocks since 1998 and 2024 looks set to be the best year compared to European stocks since the early 1980s! Nearly 10% points difference between Sweden and the USA measured in Swedish kronor, in one month!

Source: Bloomberg

During the month, we spoke with, among others, the management of our portfolio company, Diploma, which has around half of its sales in the USA. Diploma's management in the US is more optimistic than ever and we understand them. The Russell 2000 was the best performer of the major American indices in November, rising by a whopping 10.8%. By comparison, Carnegie's small company index fell by 3% measured in USD. The difference is two annual returns in four weeks, something that will go down in the financial industry's history books.

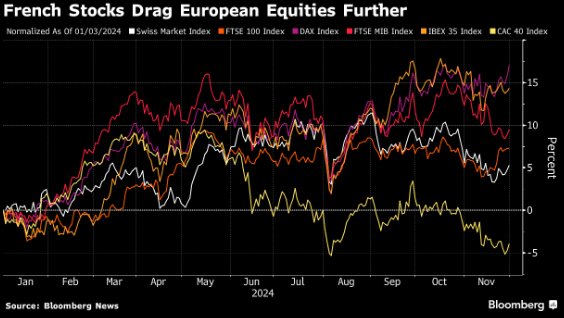

Illustrated in another way, this year's return can be seen below. Germany leads the league, and it is a bit of a paradox that when there is a political crisis in Germany, as it was in November, share prices rise as investors begin to hope for a change. During the first 11 months of the year, OMXS30 (Stockholm index) had only risen by around 5%.

Source: Bloomberg News

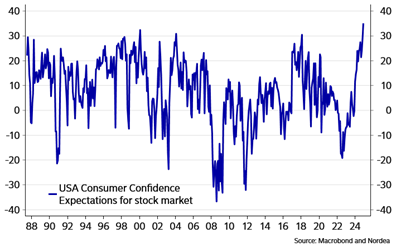

The share of the American population that believes in continued stock market gains has never been higher.

Source: Macrobond and Nordea

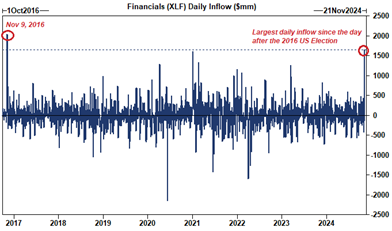

Enormous amounts of capital, especially passive, have flooded into the American stock market in a short time. The inflow the day after the election was one of the largest ever, see below for banking and finance.

Source: Goldman Sachs

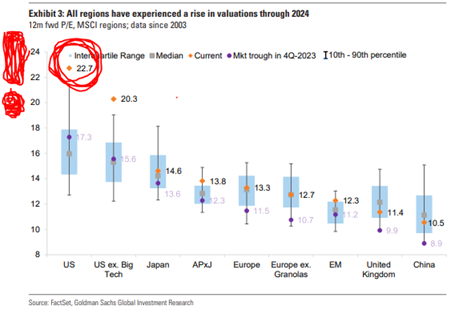

Many are overweight the US now – a clear consensus position. The euphoria is somewhat reminiscent of when Ronald Reagan became president in 1980. We note that at that time the P/E ratio was 7.5x and 9% of the population's wealth was in stocks. Today, the corresponding numbers are 23x and 41%. The enormous inflows have in a short time increased the valuation difference with the rest of the world to new high levels, see picture below.

Source: FactSet, Goldman Sachs Global Investment Research

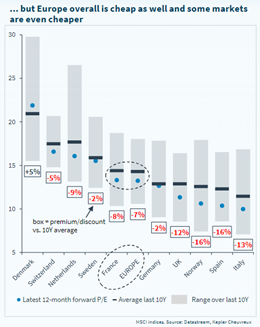

All European markets except Denmark (Novo Nordisk) are valued lower than the 10-year average.

Source: Kepler Chevreaux

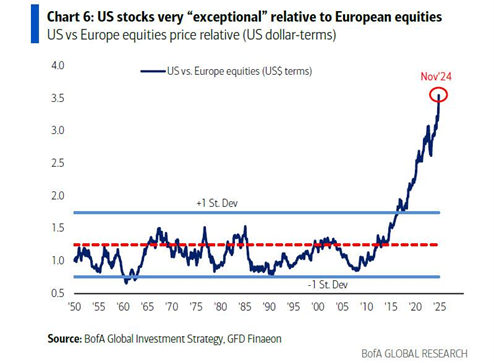

The picture below is almost too awkward to show, but we'll do it anyway. What have Europe's politicians been up to for the past 15 years?

Source: Bofa Global Investment Strategy, GFD Finaeon

Source: X

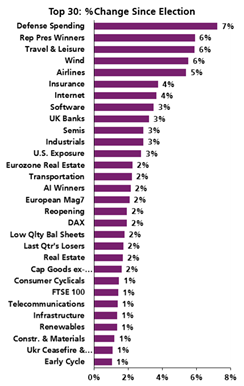

The sector in Europe that has fared best after the American election is the defense industry, not much of a riddle.

Source: UBS

In Europe, many raised their eyebrows when, due to continued political disagreement, France had to pay a higher interest rate on its government bonds than Greece. It is unprecedented. It has also left its mark on the French stock market, which has been really weak this year with -4.1% return as of the end of November.

Source: Bloomberg

Bad news about the Eurozone economy kept trickling down in November and PMI fell from 50.0 to 48.1. Those hoping for a double reduction in the interest rate in December will be disappointed. The ECB is not known for being ahead of the curve but rather driving forward on a tortuous path with the help of the rear-view mirror. Also in the UK, PMI fell in November from 51.8 to 49.9. In the US, it rose from 54.1 to 55.3.

The outlook in Sweden is better, where the confidence indicator of the manufacturing industry increased by 4.2 units to 95.8. The confidence indicator for construction activities also increased by 4.2 units to 98.4. The household confidence indicator rose for the fourteenth month in a row(!) and is slightly above the historical average. Expectations for the household and national economy in Sweden twelve months ahead are considerably more optimistic than normal. We also add here that on December 2nd we got access to the Swedish PMI figures which rose from 53.2 in October to 53.8 in November. Good!

The euro has weakened significantly against the US dollar in a short time.

Source: Bloomberg

Given that our base is Sweden, we must include this image as well, which shows the Swedish krona against the US dollar. During the fourth quarter and so far, the dollar has strengthened by 7-8%, which are huge numbers in this context. We guess that analysts will in the near term adjust their profit estimates for companies with a lot of sales in the US (and perhaps most preferably with the majority of costs in SEK).

Source: Bloomberg

The collapse of Northvolt has even got the attention of international media. We hope and believe that it will not have too much of a spillover effect.

Source: Financial Times

The price of Bitcoin has gone straight up after the US election, reaching new highs.

Source: Hedgeeye

Portfolio companies

Diploma

In November, serial acquirer Diploma filed its financial accounts for the fiscal year ending in September. For the full year, the company grew organically by 6%. Including acquisitions, the total growth was 14%. The operating margin rose to 20.9% from 19.7% the previous year. All this combined, resulted in earnings per share that rose by 15% for the full year. A major contributing factor to this year's good results was the acquisition of the distributor Peerless, which we wrote about in our March newsletter.

When some algorithm picked up in the report that “markets are still challenging”, the stock fell by almost 10%. It was a strange reaction and by the end of the week the price was largely unchanged. We sold a few blocks of stock the day before the report and bought most of it back on the day of the report. Report days are sometimes seen as liquidity events among slightly smaller companies, and then it can turn out like this. Someone must sell their position.

Source: Bloomberg

We own Diploma because they are good at allocating capital. But they are not only good at finding great companies at attractive multiples. During the year, they have also divested a few companies that they no longer consider to be part of Diploma's core business. We think that is a sign of health.

Around 50% of Diploma's sales are generated in the USA. After discussions with the company, we feel confident that Diploma will not be negatively affected by Trump becoming president in January. This is well reflected in the stock market, which seems to see the Diploma stock as a way to gain "exposure" to Trump's victory. Companies that are listed in Europe, and that had a lot of sales in the US, generally seem to have performed quite well in November.

Diploma’s share price rose by 5% in November and have risen by 25% for the full year.

4imprint

During the month, 4imprint released a financial update for the financial year ending 31st of December. The message was that it expects to reach the market's expectations regarding profit, but that revenue will come in a couple of percent lower than expected. The recovery in demand that was hoped for in the second half of the year has not really materialised, even if the company will continue to grow. In other words, it is not a disaster. For us, the most important thing is that 4imprint's profitability is maintained at a high level, because an important part of our investment thesis is that the company received structurally higher margins after the pandemic. The margin is expected to reach a level of just over 10% in 2024 and the years thereafter. This can be compared to just over 6% in 2019. The company is valued at a low 10x ebit 2025e with a significant net cash position.

The stock fell 1% in November and has risen 11% for the full year.

Euronext

In November, the exchange operator Euronext held a long-awaited capital markets day. The main message is that Euronext, after an intensive acquisition period, is now shifting its focus towards organic growth. Very briefly, they want to accelerate growth within the revenue streams that are not dependent on trading volumes, expand trading and clearing within interest rates, currencies & commodities, as well as build on the leadership they already have in stock trading.

Euronext is generally known for being cost focused, but with margins already above 60%, we think it is right to focus on growth. The company is aiming for at least 5% annual organic growth in sales and EBITDA next year, numbers that we believe will be beaten by several percentage points. The management of Euronext are known to be conservative. They prefer to err on the side of caution and then beat expectations.

The stock rose 4% in November and has risen 34% for the full year.

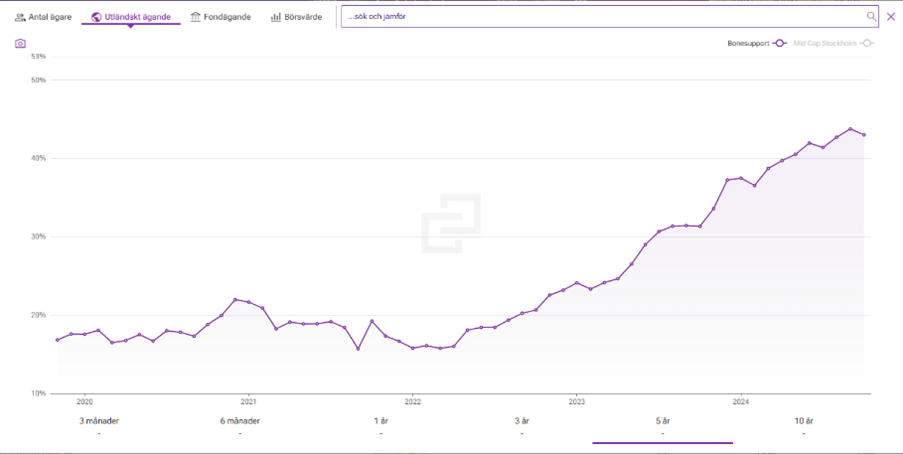

Bonesupport

Bonesupport was one of the fund's best contributors during November. It was not driven by any particular news, but we suspect that it is US investors who account for a large part of the recent buying. We are attaching a picture from Holdings of foreign ownership in the stock, which is now up to 44%. Bonesupport rose 9.4% during November and has risen by 94% this year.

Source: Holdings

SLP

During November, SLP continued to use the capital it raised in the autumn rights issue. On the last day of the month, a property with a value of SEK 306 million was acquired. That was then followed, on the first day of December, by a purchase of two more properties from Postnord (Swedish Royal Mail) in a sale and lease back deal for SEK 470 million. On a pro forma basis, the LTV is 43%, compared to the target of a maximum of 55%. SLP has a strong balance sheet and leverages it, rapidly creating shareholder value. The stock rose by 2% during November, which was 3% better than the broad real estate index. For the whole year, the share has risen just under 18%.

Kalmar

Kalmar released a strong quarterly report at the beginning of November, which was rewarded with a share price increase of a total of 13%. The company delivered better than expected on all points (order intake, sales and profit). Measured in terms of adjusted operating profit, the outcome was approximately 15% better than analysts' expectations.

Kalmar is a world leader in several segments. Internally, the focus is now on increasing profitability and organic growth. CEO, Sami Niiranen, was recruited from Epiroc and has worked for several years within the Atlas Copco/Epiroc group. We believe that this is a good recruitment as the big driver forward for increased profitability is service, something that Atlas/Epiroc have historically been good at. Kalmar is valued at a low 8x EV/EBIT on our estimates for 2026e.

Kalmar was spun off from Cargotec at mid-year and the share has since risen by 23%. The increase in November was 12%.

Cargotec

In November, the Cargotec share fell five percent after the company announced a sale of its subsidiary, MacGregor. The buyer was the private equity company Triton and the deal valued MacGregor at 480 million euros. Judging by the share price's negative reaction to the news, expectations of the acquisition price were a bit higher than what was received. In addition, Cargotec had already told the market that MacGregor was for sale, which probably did not make their negotiating position very strong.

While the MacGregor price tag was somewhat of a disappointment, even for us, there are clearly positive aspects to it all. The management has delivered exactly what was promised. Hiab, as the company will be called from the next general meeting, is a high-quality Nordic industrial company that deserves a premium valuation on the stock exchange. Hiab will also have a net cash position, which sits well as the company is looking at several acquisitions.

Although the stock lost about 5% in November, it has been strong for the full year, up 69%.

Biotage

Biotage became something of a "hot topic" in November when the company was to be excluded from the SBX index (Stockholm Benchmark Index). Nordea estimated that around 1.3 million shares would be sold due to the exclusion. This corresponds to roughly 1.6% of the shares or almost 2.1% adjusted for free float. Around the October report, there was abnormally high-volume trading when the stock was under pressure, and we believe the reweighting had something to do with this.

All of the above are of course technical factors that (probably) created a selling pressure that is not based on fundamental factors. We have used this to increase our position. We see the Biotage share as cheap at today's price levels. We value the company at approximately 15x operating profit in 2026, which we think is too low given the quality of the company. The stock retreated 5% during November and has risen by 10% for the year.

Summary

European equity investors notwithstanding, most of this letter has revolved around the US and the consequences of the outcome of the election. It is inevitable and the biggest topic of discussion in recent weeks has been the extent and timing of new duties and tariffs and how to read Donald Trump. The first "sharp" guidelines from the new administration came in the last week of November when Trump announced that he intended to introduce tariffs of 25% on all imports from Mexico and Canada and the corresponding 10% on China. Someone calculated that, in that case, in isolation it would increase US inflation by 0.9 percentage points.

Our humble take on this is that these threats, just like when it started in 2016, are negotiating tactics and one should not jump to conclusions, although new tariffs are most likely to come. A few days later, Donald Trump posted: “Just had a wonderful conversation with the new President of Mexico, Claudia Sheinbaum Pardo. She has agreed to stop migration through Mexico and into the United States effectively closing the Southern Border…It was a very productive conversation!”

Another relevant comment (we think) is that the Democrats also introduced a lot of tariffs. See the communication below which was released on May 14th this year by the White House, and which applies to tariffs against Chinese products. Steel and aluminum: from 0-7.5 to 25%. Semiconductor: from 25 to 50%. Electric cars: from 25 to 100%. The list is long and worth bearing in mind when listening to the debate. https://www.whitehouse.gov/briefing-room/statements-releases/2024/05/14/fact-sheet-president-biden-takes-action-to-protect-american-workers-and-businesses-from-chinas-unfair-trade-practices/

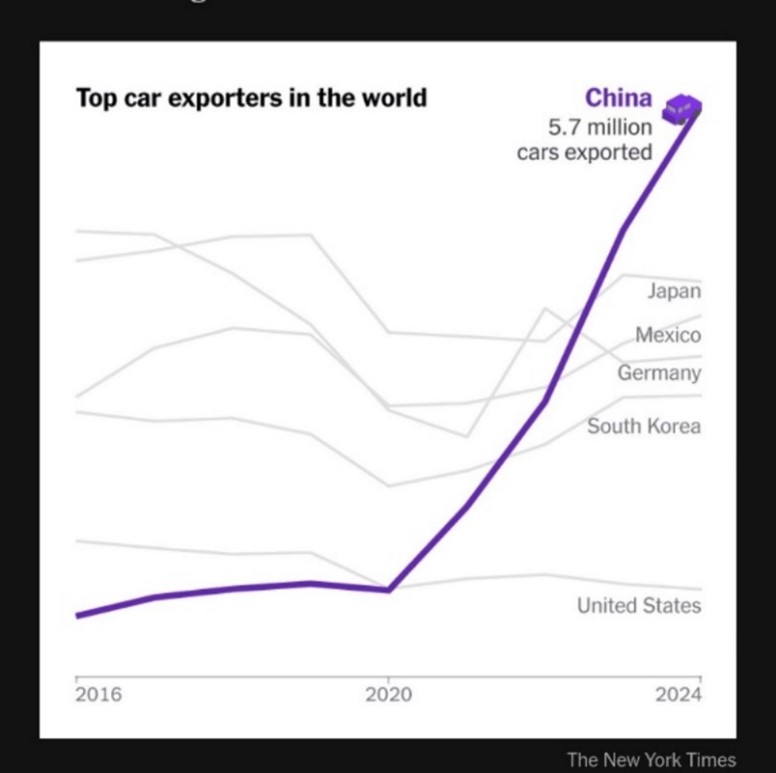

Despite the tariffs, China's total of 241 car manufacturers have managed to establish themselves well in the global car market - to say the least.

Source: The New York Times

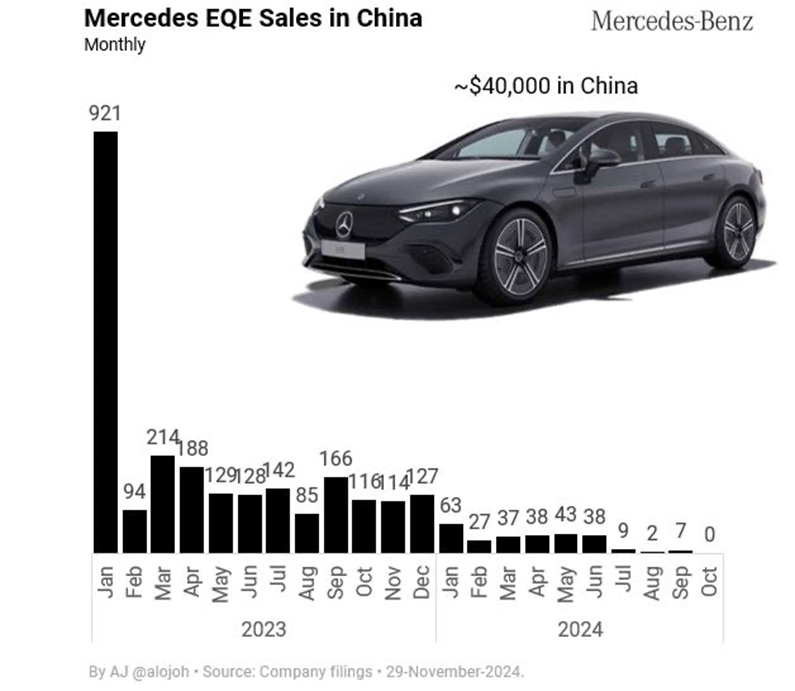

Premium German cars, on the other hand, have a tougher time in China.

Source: X, Michael A. Aouret

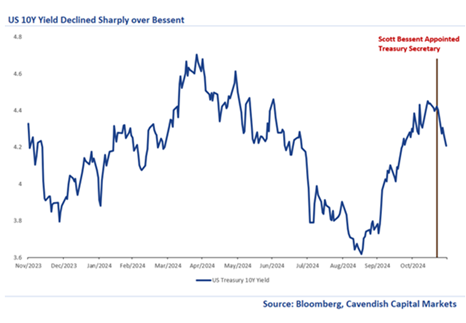

Things will move quickly from January 20 onwards when Donald Trump and his new administration are installed. Various ministers have already been nominated and among those there are some question marks. Fox News contributor Pete Hegseth is expected to become Secretary of Defense, Robert F Kennedy Jr. Secretary of Health, known as a major vaccine opponent. Pam Bondi becomes attorney general after first-time candidate Matt Gaetz withdrew amid allegations of sex with a minor, to name a few. The nomination of Scott Bessent as Treasury Secretary, a well-known hedge fund manager, was well received by the market (see developments of the US 10-year yield below). A somewhat softer tone on tariffs and also a certain focus on reducing the US budget deficit contributed positively.

Source: Bloomberg, Cavendish Capital Markets

US corporate bond spreads are now at their lowest in 26 years and even in Europe there has been a lot of progress compared to just a year ago. At this time last year, the Swedish bond market was completely frozen, but now transactions take place all the time and the interest among investors is large.

.

Source: Ice data indices, Federal Reserve, Financial Times

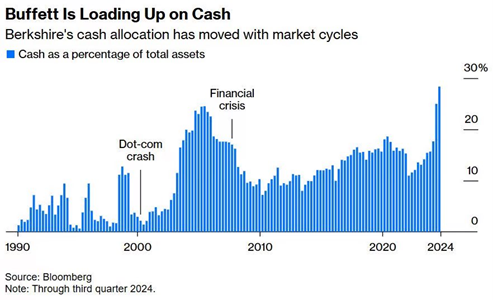

We note that Warren Buffett has a greater proportion of cash today than during the financial crisis.

Source: Bloomberg

American insider sales are at an all-time high. Historically, however, it has not been a particularly good sales indicator.

Source: Financial Times

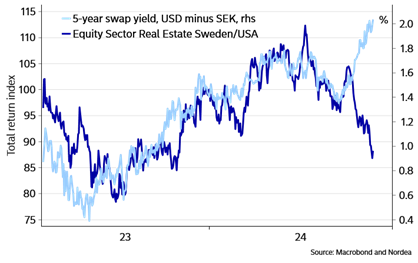

We have watched with some envy at the returns that US stocks have given in recent weeks. One of the stranger developments in the recent period (we think) has been Swedish real estate stocks which have fallen by just over 13% since the peak in early October while the Swedish two-year interest rate has fallen from around 1.8% to today's 1.6%.

In the United States and since the beginning of October, the American two-year interest rate has risen from approximately 3.6% to today's approximately 4.2%. It had no negative impact whatsoever on US real estate stocks, which rose 5.7% in November.

Study the image below. The prerequisites for Swedish real estate stocks to rebound feel unusually good and we have recently increased our real estate exposure by buying more of the logistics company SLP, which is one of the fund's larger holdings.

Source: Macrobond and Nordea

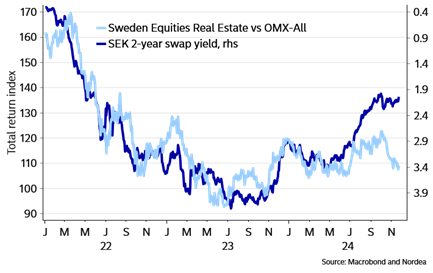

The same message illustrated in another crystal-clear way, thanks Mikael Sarwe at Nordea.

Source: Macrobond and Nordea

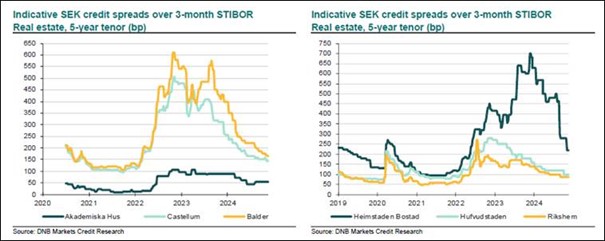

A huge change for the better in a short time has taken place in terms of credit spreads for real estate bonds. Study the curve for Balder for example. Incomprehensible.

Source: DNB Markets Credit Research

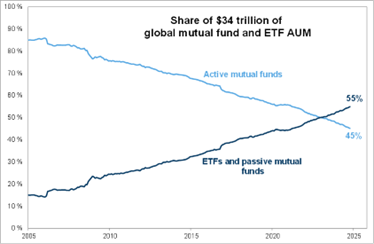

If you've read this far, you're probably wondering why you should allocate part of your portfolio to European stocks at all? The answer is that if you find any fund that over time has created excess value through active management, that takes real company risk based on fundamental factors instead of investing in a stock based on how many points the stock weighs in an index, it is highly reasonable to allocate part of the capital to such type of management.

Nowadays, most of the inflows go to passive funds and ETFs, which we deem sad. An increased inflow of passive capital leads to greater buying pressure, to a higher valuation, to an increased number of points in the index, to more passive buying and so on. The higher the company's valuation, the higher the demand from passive capital. It doesn't feel right and that's why the stock market works completely differently today compared to just 10 years ago. The advantage for people like us is that it creates opportunities that did not exist 10 years ago. Having said that, it requires a certain amount of patience.

Source: Goldman Sachs

To return to European stocks and if we allow ourselves to mention some of the fund's best performing European stocks this year, it is Bonesupport which his risen by 94%. The company has its headquarters in Lund, thus Swedish and European, but has most of its operations in the USA. Switzerland's Accelleron, which has risen 87%, has 70% of its operations outside Europe. British Diploma, which has risen by 24%, has about 50% of its turnover in the US and close to 60% of its profit. Finnish Cargotec which spun off Kalmar earlier in the year, has together risen by 76% and has 60% of its turnover outside Europe. The point of the above is that the location of a company’s headquarter is rather irrelevant.

Two things determine the performance of a stock over time; the company's ability to create value and the price you pay for the share. There are many European small and medium-sized companies that create value and where the valuation is low and that is the reason why Europe remains interesting. But today's algorithms don't pick up on what (fewer and fewer) value investors pick up on. The algorithms run on momentum, profit growth and technology. It is not something that immediately pops up among Europe's larger companies and among the smaller companies there are significantly fewer ETFs and passive capital that invest. Which investment is most attractive? Tesla at P/E 145x or VW at P/E 3x? It is not possible to answer as passive flows now largely determine price and valuation in at least the short and medium term.

On Saturday, November 30th, the Financial Times wrote that there is a sale on for European companies. In the last days of November, there were as many as four buyouts on the London Stock Exchange with a total value of £5.3 billion. Buyers were companies from Canada, Abu Dhabi, Australia and Europe. As you may remember, the fund had a takeover of British Wincanton at the beginning of the year. The trend is likely to continue unless valuations rise on their own. The pressure today on company management is significantly higher than it was before, and we note that European companies are buying back more shares this year than ever before - a positive thing.

We maintain our positive outlook for the small and medium-sized companies asset class. We also note that the Russell 2000 had a stronger development than Nasdaq during November.

• Interest rates in Europe are very likely to continue to fall, which has historically benefited small companies the most.

• Growth for the asset class SMID (small and medium-sized companies) is significantly better than for larger companies.

• The valuation difference between small and large companies is at historically high levels.

• Finally, smaller companies should fare better than larger companies in terms of duties and tariffs, as they typically have a higher proportion of domestic sales.

Source: Bloomberg

After such a sharp underperformance of Europe compared to the US, there should be good conditions for a reversal. But as we have said many times before, this fund is not a mirror image of the larger stock market but consists of a portfolio of what we think are 15-20 interesting and attractive investments, where the expectation of investors should be to get excess return in the long term in relation to the market.

At the time of writing, there are only 18 trading days left in the year. A year that, as usual, offered great drama and many interesting days. We thank you all for valuable collaboration, great input and shown interest. We are now all looking forward to a peaceful Christmas with family and friends and not least a generous Santa.

Merry Christmas & Happy New Year!

Mikael & Team

Malmö, December 5th

IMPORTANT INFORMATION. This is a marketing communication. Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested. Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.