This material is marketing communication.

Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class’ return. The information below regarding returns therefore differs from the returns in other share classes.

Before making any final investment decisions, please read the prospectus, its Annual Report, and the KID of the relevant Sub-Fund here.

NOVEMBER PERFORMANCE

The fund’s value increased by 0.2% in November (share class I SEK), while the benchmark increased by 0.1%. Since the change of the fund’s strategy at the beginning of September 2023, the fund’s value has increased by 26.4% compared to an increase of the benchmark by 22.7%.

Source: Coeli European

* Adjusted for spin-off of Rejuveron

** Includes September 1 (strategy change to long-only implemented September 4 2023)

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

EQUITY MARKETS / MACRO ENVIRONMENT

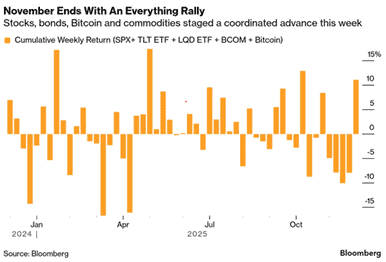

Like October, November did not follow historical patterns. A fear of US interest rates not being cut in December, combined with investors starting to question future profits and valuations for AI companies, created significant downward pressure on global stock markets during the first three weeks of the month. Nasdaq fell by 8% intra-month compared to the broad European index which fell by 3% intra-month. The last week saw a rebound that offered gains for most asset classes, see image below.

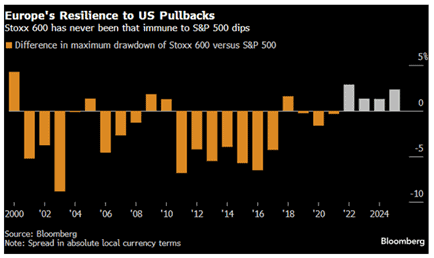

The adage that European stock markets fall more than their American counterparts when things get turbulent is no longer true. See the image below showing the development over the past 25 years. We suspect that the extreme concentration of highly valued tech companies in the US is the likely reason for this.

By the end of the month, SXXP600 had risen 0.8%, MSCI European SMID was unchanged, S&P500 +0.1% and Nasdaq -1.6%, all measured in local currency. The fund rose 0.2%, which was 0.1% better than our benchmark. By far the best contributors were Italian De’Longhi and French Trigano, which rose 16 and 19% respectively after strong reports. The weakest contributors were Danish FLSmidth and Bonesupport.

During the year, we have been both surprised and amazed by the price development of De’ Longhi and Trigano, which despite good reports and low, or very low, valuations have failed to generate any interest from investors. Now that has changed and both shares are good examples of the fact that there is significant value out there and that it pays to be patient when you have strong convictions in your analysis. We take the liberty of quoting Warren Buffet with absolutely no similes or claims:

Source: X

All reporting periods have been good during the year, but the one that just ended was the best. Out of a total of 25 companies, only three missed expectations. Given that, we are disappointed that the fund only returned about half a percentage point better than the benchmark during October-November, but we believe that the reports will also contribute positively during coming months.

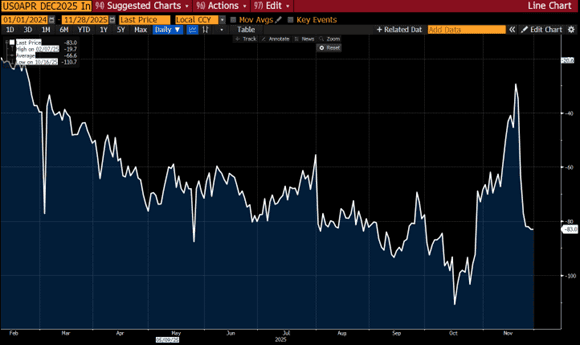

The fear of a failed US interest rate cut is well illustrated in the picture below. Well into November, there was less than a 30% probability of a cut, but some soft comments from the Fed meant that we quickly got back to more than an 80% probability and the stock market got back on its feet.

Source: Bloomberg

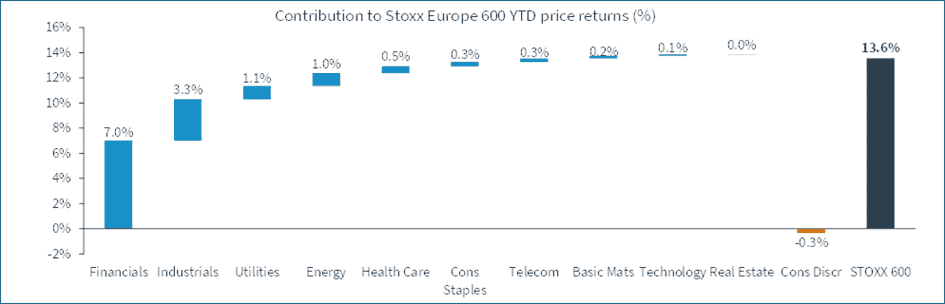

After 11 months, the broad European index has risen by 13.6%. Banking and industrials account for about 75% of the rise, with defence stocks in the industrial sector being the clear winners this year.

Source: Kepler Cheuvreux

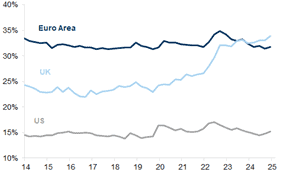

35% of the wealth of the population in the eurozone and the UK is in tired bank accounts compared to around 15% in the US. The difference in stock culture is probably even greater. American private investors now have a record high allocation to the stock market, have higher leverage than before and we also note that interest in ETFs with leverage is now at a record level. Maybe it's too much?

Source: Goldman Sachs

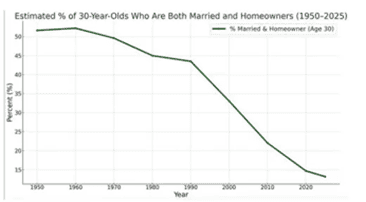

It seems that one has to take more risk if one is going to afford a house and family in the US. It is not surprising that major political forces are in motion when you study the below depressing picture with history since 1950. The same source states that it now costs an average of USD 26,000 per year to insure a family of four.

Source: Talk About Houses

The whole world (almost) held its breath when Nvidia reported and there was nothing to complain about at all, quite the opposite. It was a fantastic report. The market learned that there is a huge winner in AI, but nothing about how Nvidia's customers will make money in the future.

Source: X

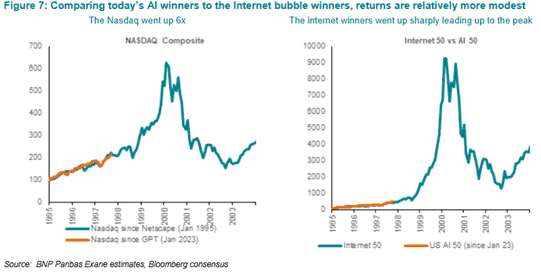

The AI euphoria has a long way to go if it is to reach the same bubble levels as during the internet hysteria in the late 1990s, like 18x more.

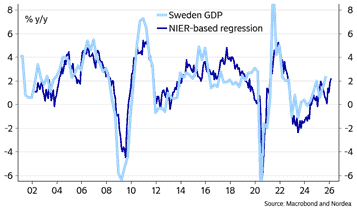

If Sweden is a precursor of an economic recovery in Europe, we have reason to be optimistic. GDP growth for the third quarter was better than expected at 2.6% and optimism is starting to spread with falling interest rates, lower taxes, inflation under control and rising wages. Nordea's combined GDP indicator continues to rise. Positive!

Source: Macrobond and Nordea

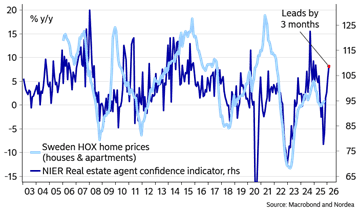

Real estate agents see a clear turnaround, which indicates rising housing prices and thus, in the long run, rising consumption.

Source: Macrobond and Nordea

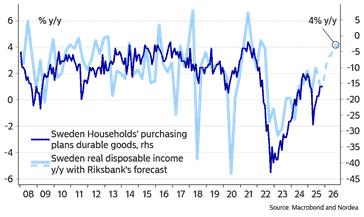

Sharply rising disposable incomes will also fuel consumption.

Source: Macrobond and Nordea

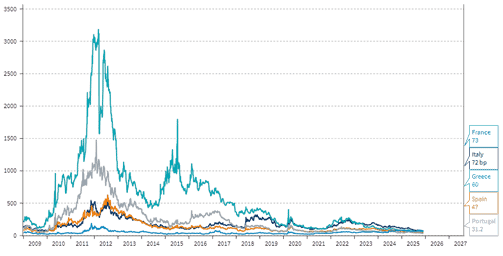

10–15 years ago, the rather rude epithet “PIGS” was coined for Portugal, Italy, Greece and Spain. All of them were in the hands of lenders and had to pay with high spreads against the German 10-year yield because of their poor government finances. The development since then for the above-mentioned countries has been exceptionally good, see picture below.

Source: Kepler Cheuvreux

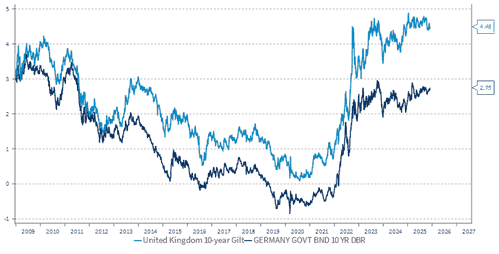

The opposite applies to countries like France and the UK where the challenges are currently significant. We did have a new epithet in store, but our self-preservation and compliance department strongly advised against it. Moreover, we are great friends of France and the UK! Below is the UK spread against the German 10-year yield.

Source: Kepler Cheuvreux

PORTFOLIO COMPANIES

Trigano

The Paris-listed motorhome manufacturer released a report during the month that was appreciated by the market. The company's operating margin for the financial year ending in August landed at 9.2%, compared to the guidance of "around 9%", while cash flow landed at EUR 564m against the guidance of EUR 500m.

Overall, Trigano has managed the year very well given the widespread problems that the industry has been faced with, where overstocked inventories at distributors have had to be reduced, which in turn has led to motorhome manufacturers not receiving sufficient coverage for their fixed costs when they have reduced production. While production has fallen, end-customer demand has been relatively strong despite low consumer confidence: new registrations in Germany and France increased by 1 and 10% respectively during the past "motorhome season" (September-August). Anyone interested can read more about our investment thesis in our monthly newsletter for September.

The outlook for the coming year looks positive. Trigano will gradually increase the production rate again, which is expected to contribute positively to profitability. The order books are well-filled after the recent motorhome fairs held every year in Europe in late summer and early autumn, and Trigano expects a clear improvement in business during the year. The market liked Trigano’s message and the share rose 19% in November. The share has risen approximately 26% since we initiated our position in June 2025.

De’Longhi

The coffee machine manufacturer released a very positive Q3 report during the month. Organic growth was 11–12%, while expectations were around 6–8%. Operating profit (EBITDA level) was around 7% better than expected. As a result of the strong results, De’Longhi also chose to raise its outlook for the year. The share reacted by rising by 14% on the report day and ended November with a price increase of 16%.

The De’Longhi share has now risen in line with the index since our investment at the beginning of the year. This despite the company raising its outlook twice and consistently delivering growth that has been higher than expectations. The market has mainly been concerned about headwinds in the form of US tariffs and low consumer confidence, but so far De’Longhi has navigated that well. Notwithstanding, the important Q4 quarter remains, which in a normal year accounts for around 40% of annual profit and essentially all of the free cash flow.

The company is still valued at low multiples. Our estimates put the stock trading at a P/E of 13-14x for next year, and the company will have a large net cash position of approximately EUR 625 million (11% of market capitalization) at the end of 2025. We believe that a potential value driver could be a potential spin-off of the company’s Professional Coffee division, which sells coffee machines for commercial use under the La Marzocco and Eversys brands. The Professional Coffee division grew by 40% in the most recent quarter and has operating margins at an EBITDA level of 20-25%. Management has flirted with the idea of spinning off the division, which we believe would highlight the values in De’Longhi.

Asmodee

The board and card game company also delivered a report that exceeded expectations. Organic growth came in at 23%, compared to the expected 17–18%, while the company's adjusted EBITDA result was 9% better than expected. At the same time, free cash flow was somewhat weak, especially attributable to inventory buildup ahead of the company's peak season in November and December. The sales mix was good, with good growth in self-published games. We see this as reassuring since it was a weaker point in the previous report.

The share responded by falling by 4% on report day, which we found difficult to comprehend. Some have highlighted the management's cautious appearance in CEO words (where they "warned" of more difficult comparative figures in the future) and during conference calls. However, so far, looking at their stock market record they have evidently chosen to be conservative in their statements and then overdeliver on expectations.

We like the long-term story for Asmodee: with a distributor network that is unique in Europe, you have good insights into which games sell better than others. This should provide good conditions for making the right acquisitions, at low multiples, where you can later refine the companies and improve profitability for Asmodee when moving from a low distributor margin to a higher publisher margin. After the years under Embracer's ownership, one had limited opportunities to reinvest free cash flow in acquisitions. That should change now that they are independent.

Asmodee shares fell by 5% in November.

FLSmidth

For some time now, we have had a minor position in Danish FLSmidth, which has undergone a major transformation in recent years to become a pure supplier of mining equipment with a focus on highly profitable service revenues. FLSmidth's report for the third quarter was slightly worse than expected in terms of order intake (6% lower), sales (5% lower) and adjusted operating profit (2% lower – but with a better margin than expected). The company partly explained the result as timing effects in the service segment. On the positive side, we find strong order intake in the service business and improved cash flows.

The report was followed up in the same month by the company's CEO, Mikko Keto, who had been instrumental in the company's transformation, announcing his resignation in favor of the CEO position in the Swiss company SIG Group. That is another company that is in clear need of a transformation (the SIG Group share has essentially halved this year). We do not believe that Mikko Keto is the right person to lead FLSmidth in its next phase, where it needs to prove to the stock market that it can also grow order intake. So, we actually view the change in the CEO position as positive. That said, he has been appreciated by the stock market. The sentiment was not improved by the fact that the company chose to cancel its capital markets day planned for March 2026 after his resignation, and that Mikko Keto also sold shares (according to his own statement for tax reasons).

FLSmidth shares fell by 19% during the month and were the fund's worst contributor. We have chosen to maintain our position as we believe there is a clear chance of appreciation if the company manages to show better order intake in 2026, while at the same time we want to see better free cash flows and clear steps towards lower tax rates in the coming years (FLSmidth's effective tax rate is significantly higher than in comparable companies). We have also noted some bid speculation (with emphasis on speculation) around the company, although it is never an important part of our investment theses.

Hill & Smith

Since September, we have had a minor position in London-listed Hill & Smith, a serial acquirer in the infrastructure segment. Hill & Smith focuses on finding companies with dominant market positions in relatively small product niches. The company's operating profit has grown by around 11% per year 2015–2024 (CAGR) and the share is currently valued a notch below its historical average. Around 75% of revenue comes from the US market. Over the past year, a new CEO has joined the company, who seems to be strengthening the focus on gradually moving the company portfolio towards more fast-growing, non-cyclical end markets.

During the month, Hill & Smith provided an update for the four months ending last October. Organic growth accelerated from the first half of the year (from 2% to 3%) with a strong development in the US, while the UK business has had a difficult time this year. In conjunction with the financial update, the appointment of Nick Anderson as Chairman of the Board was also announced. Anderson is a highly regarded former CEO of the British industrial company Spirax. We believe he can accelerate the acquisition activity at Hill & Smith, which has previously been a fine but somewhat sleepy company.

Hill & Smith shares rose five percent in November. We hope to return to this topic in the future.

Rotork

Like Hill & Smith, Rotork released an update for the four months ending in October. Order intake rose, as in the first half of the year, by 6% organically. All segments showed growth, and the outlook remains good. Rotork also announced a £50 million share buyback program. We continue to view Rotork positively, which has now delivered on its goal of accelerating growth for several years. Rotork shares rose 4% on the reporting date but nevertheless ended November with a decline of 2%.

Babcock

Babcock delivered another strong report during the month. Organic growth for the first half of the year came in at 7%, against expectations of around 4%. Operating profit (adjusted EBIT) was 7% better than expected. The outlook remains good, and management seems to believe in many more procurements/contracts won.

Despite this good news, the share fell by 7% during the month. The price development is attributable to the general decline in shares with defence exposure. In comparison, a basket of European defence stocks fell by 13% during the month, measured in pounds. The development of defence stocks in Europe, which in many cases are (unreasonably) highly valued, has been triggered by the fact that the market seems to be discounting peace in Ukraine as increasingly likely.

We believe that Babcock's valuation remains attractive despite the strong price increase since our initial investment in the spring. When peace finally comes to Ukraine, it will not stop increased defence spending (perhaps quite the opposite), and since its transformation under the current management team, Babcock is a much better company than before. Those interested can read more about Babcock in our monthly newsletter from May 2025.

SLP

SLP continued to deliver positive transactions. This time through a sale-and-leaseback deal with DSV where the properties were valued at SEK 1.1 billion with a rental value of SEK 78 million. The portfolio is fully leased with an average contract of 7.5 years, and the structure is European triple net, which means that SLP has essentially no operating costs. We estimate the yield to be 7%, compared with SLP's own required yield of 5.9%. The properties are slightly older than the company's average portfolio, and we therefore expect a slightly higher required yield on these properties. We estimate that the deal will create around SEK 200 million in value for the owners within a short period of time, which corresponds to approximately SEK 0.75 per share. It is difficult not to be impressed by this type of acquisition, and that is why SLP is one of the fund's larger positions.

At the same time, we see how the yield requirements on good logistics properties in Denmark are expected to fall by around 30 basis points already by the end of the year. If a similar movement were to occur on the Swedish side of the strait, SLP's property value would increase by up to SEK 1 billion, corresponding to approximately SEK 3.5 per share. The share fell just over 1% in November.

SUMMARY

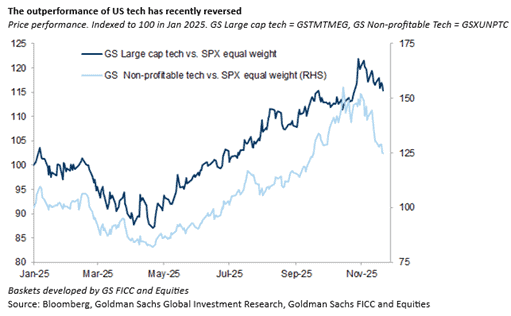

The front pages are overflowing with information about how to protect your money against the AI fever, which is usually an excellent contraindication. The picture below shows how US tech stocks have performed weaker than the broader market recently. However, measured over the entire year, tech stocks are clear winners.

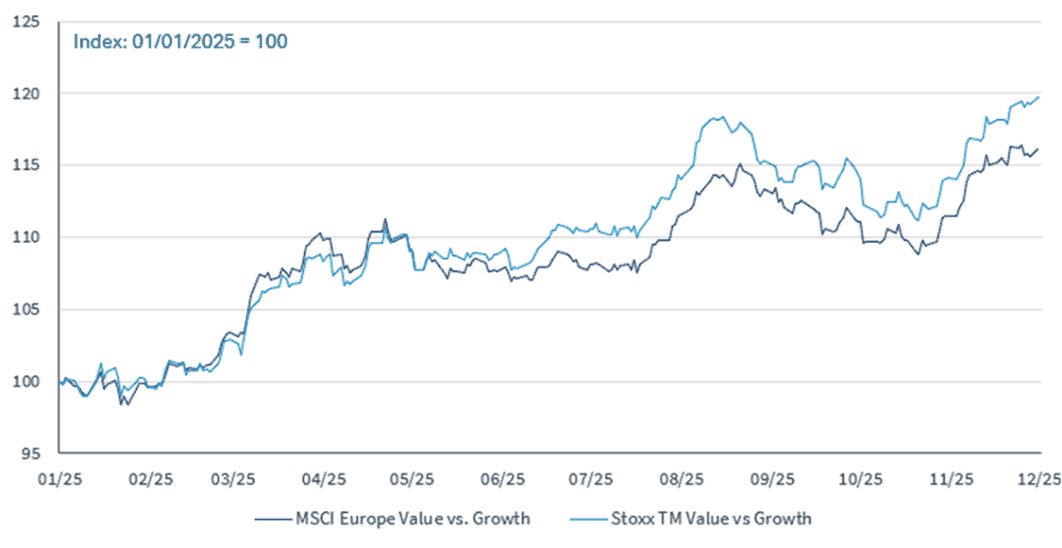

In contrast to the US, value stocks have performed significantly stronger than growth stocks in Europe, with banks as the clear sector winner.

Source: Kepler Cheuvreux

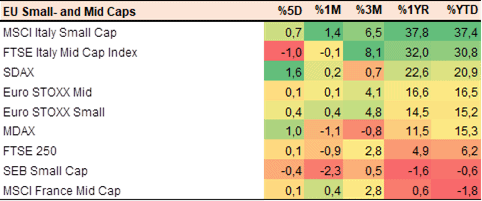

To further complicate the picture, European small caps, which are some of Europe's growth companies, have performed 20% better than American small caps (measured in the same currency) in the past year. The biggest explanation is likely the enormous interest in the largest tech companies, which in turn has driven concentration to unprecedented levels.

Source: Bloomberg

One more level down, we can see that the spread in returns between different countries in Europe has been enormous. All measured in local currency. The SEK has strengthened by 4.5% against the euro and a full 10% against the pound.

Source: Coeli European

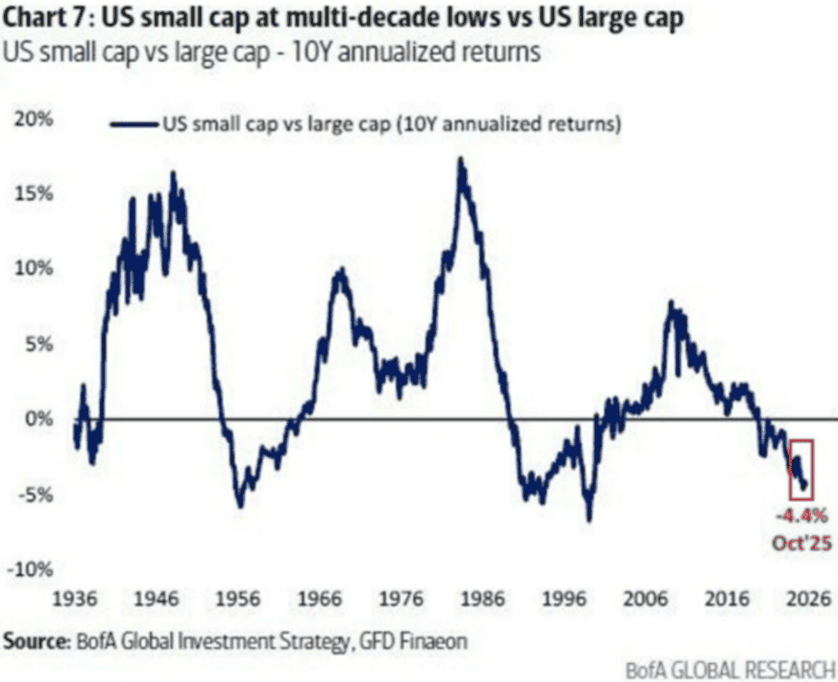

The return for American small-cap stocks compared to large-cap stocks is at its lowest level in decades, see image below with data from 1936.

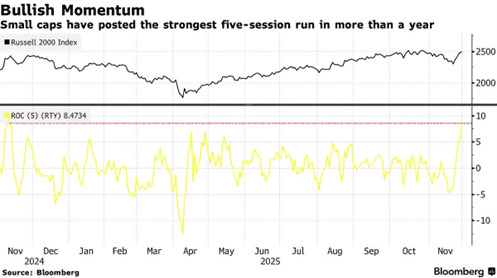

At the time of writing, US small-cap stocks suddenly had their strongest day in over a year. A turnaround or a temporary setback?

Source: Bloomberg

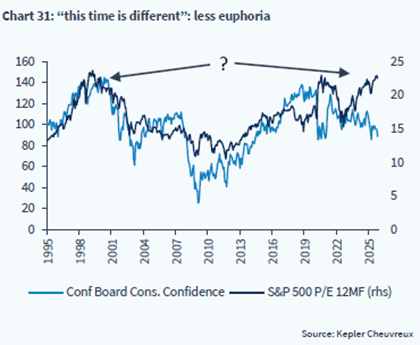

Corks were popping around the turn of the millennium and the valuation of the S&P500 was at an all-time high. After 25 years, we have now reached the same levels. A big difference compared to 25 years ago is that corks are not popping when consumer confidence is at low levels. The stock market and the real economy are not the same.

Source: Kepler Cheuvreux

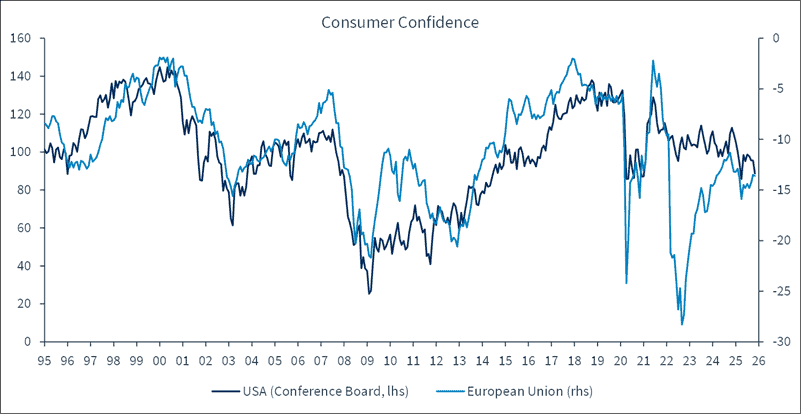

In Europe, consumer confidence crashed almost four years ago when Russia attacked Ukraine. Thankfully, the rebound has been strong, and things should get even better next year.

Source: Kepler Cheuvreux

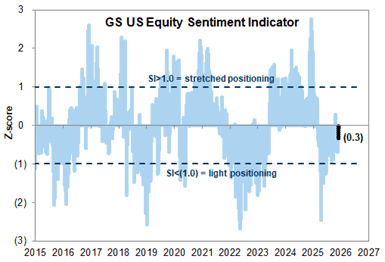

Investors are cautiously positioned and are probably breathing a sigh of relief after an unusually eventful year. Positive! The picture is updated as of November 28th.

Source: Goldman Sachs

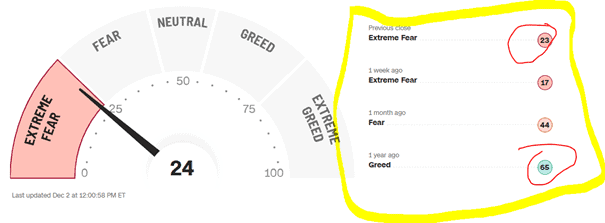

Even though it is December, investors are unusually risk-averse, which is also a positive. A possible US interest rate cut on December 10th will likely change that.

Source: CNN

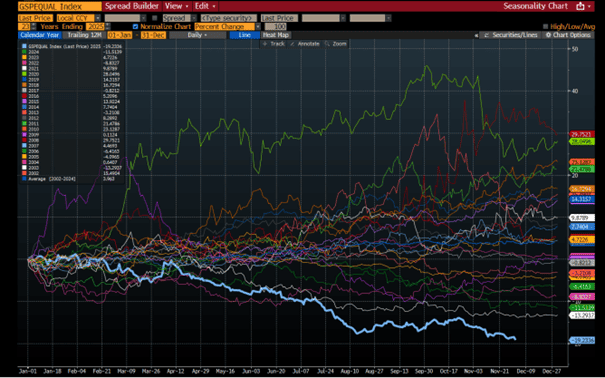

A very clear trend this year is the weak price performance of quality companies compared to companies that are of lower quality (cyclical, lower ROCE and profit growth). Goldman Sachs has a basket of European quality stocks and measured since 2002, it has never before developed so weakly relative to low-quality companies. This year is represented by the light blue line at the bottom of the picture.

Source: Bloomberg

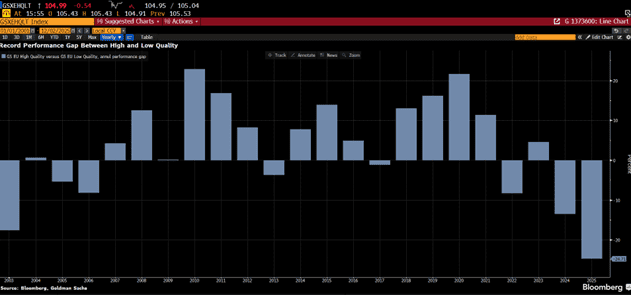

Shown another way with the difference in performance between high and low quality:

Source: Bloomberg

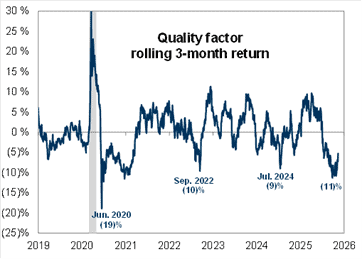

The weak development for quality companies began in the spring, but in recent weeks it has improved somewhat. There should be good conditions for next year to be significantly better for quality companies. If so, it would have a significant positive impact on the fund's development as we have a clear quality bias.

Source: Goldman Sachs

We are soon leaving behind another year that has been eventful to say the least. December usually results in a positive return, but nothing is for certain. Not much is likely to happen before the US interest rate decision on December 10th.

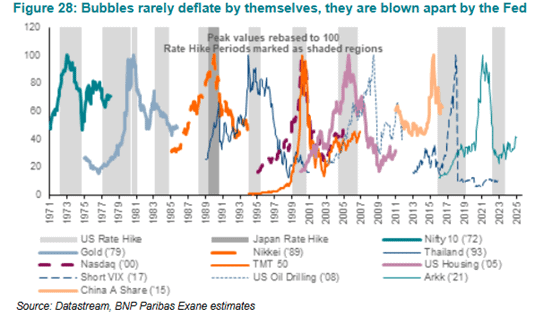

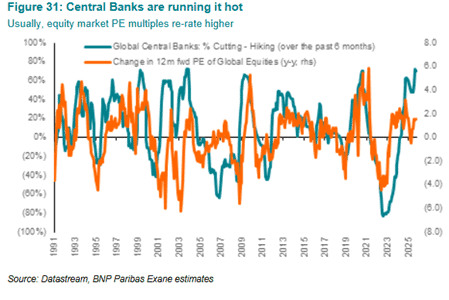

Whether we are in an AI bubble or not remains to be seen. What is more certain, however, is that it is rarely the bubbles themselves that create a decline in the market, but rather the US Federal Reserve, see image below.

The good news is that we now have a high probability of the Fed announcing further interest rate cuts next year, and this is the same for most of the world's central banks. 80% of them are in the process of lowering their key interest rates, which bodes well for demand for riskier assets such as stocks.

Despite French political turbulence, a slow German recovery and a war on European soil, the European stock market has overall had a good year. As economies now slowly begin to accelerate, as is happening in Sweden for example, demand for European stocks should be able to remain at least at current levels. Not least, diversification among global investors should be able to contribute positively as Europe remains underweight in many portfolios. When it comes to small and mid-cap companies, the underweight is even greater.

We thank you for your interest and wish you all a very Merry Christmas and a Happy New Year!

Mikael & Team

Malmö, December 4th, 2025

Source: HEDGEYE

IMPORTANT INFORMATION. This is a marketing communication. Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested. Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.