Monthly Newsletter Coeli European – September 2024

This material is marketing communication.

Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class’ return. The information below regarding returns therefore differs from the returns in other share classes.

Before making any final investment decisions, please read the prospectus, its Annual Report, and the KID of the relevant Sub-Fund here.

September Performance

The fund’s value increased by 1.1% in September (share class I SEK), while the benchmark increased by 0.3%. Since the change of the fund’s strategy at the beginning of September last year, the fund’s value has increased by 25.6% compared to an increase of the benchmark by 10.3%.

Source: Coeli European

* Adjusted for spin-off of Rejuveron

** Includes September 1 (strategy change to long-only implemented September 4 2023)

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

Equity Markets / Macro Enviroment

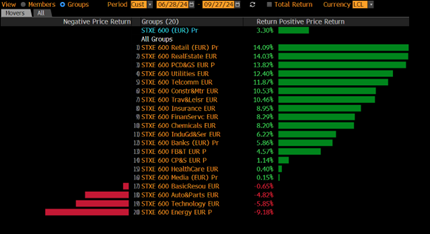

The fund rose by 1.1% in September compared to the benchmark index which rose by 0.3%. The corresponding figure for the whole year is +17.7% and +12%. The fund's best contributors were Volution, Cargotec and Lindab. The weakest contributors were Campari, Biotage and 4Imprint.

September began as usual with high volatility in the stock markets. The first week the S&P500 fell by four percent and the following week it rose by four percent. The picture was similar in Europe, albeit somewhat milder. During the second half of September, several stock markets reached new highs, and the last week saw a spectacular rally in Asia that also fuelled the Western stock markets. The party was hosted by the Communist Party of the People's Republic of China, who brought several bazookas loaded with huge stimulants in an attempt to fuel consumption in the country. The Chinese stock market rose in a few days by 27% and had its best week since 2008. Explosive to say the least and one can now read about Chinese hedge funds having severe problems with their short positions.

Source: Bloomberg

Illustrated in another image with some leading indices included, up to September 27th.

Source: UBS

It feels like a long time ago, but barely two months ago, the Nikkei had its worst trading day since 1987. It was followed by a historic rally. On the last day of September, the index fell by just under five percent. Poor Japanese market makers. Glad that one doesn’t have to determine prices on Japanese stocks.

Source: Bloomberg

The best sectors in Europe during the last week of the month were consumer products and commodities. Consumer products had their best week ever (!) where luxury companies were the leader by far and, which in turn had their best week since 2012. The fund's position in LVMH, which until the last week was under great pressure, rose by a whopping 19% in a few days (with a market capitalization of SEK 4,000 billion).

Source: Bloomberg

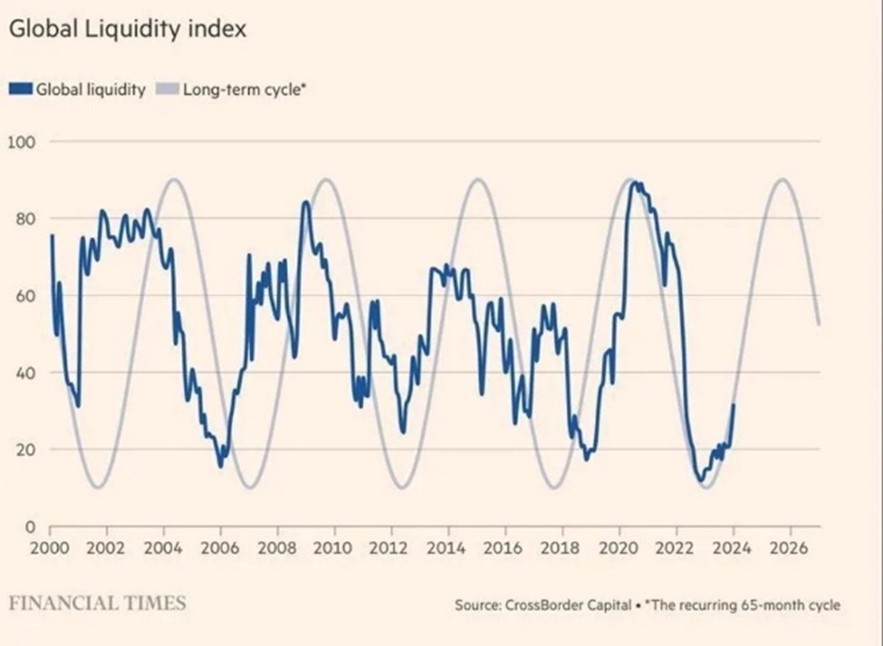

Since mid-point of the year, interest rates have dropped significantly. The US 10-year interest rate, which is a good reference rate, has since July 1 fallen from 4.46% to today's 3.75%. It's a huge movement and significant lubricant for the economy and asset prices. Below is an illustrative image showing that we probably have only begun the recovery in terms of global liquidity in the systems and that there is much more to come.

Source: Financial Times

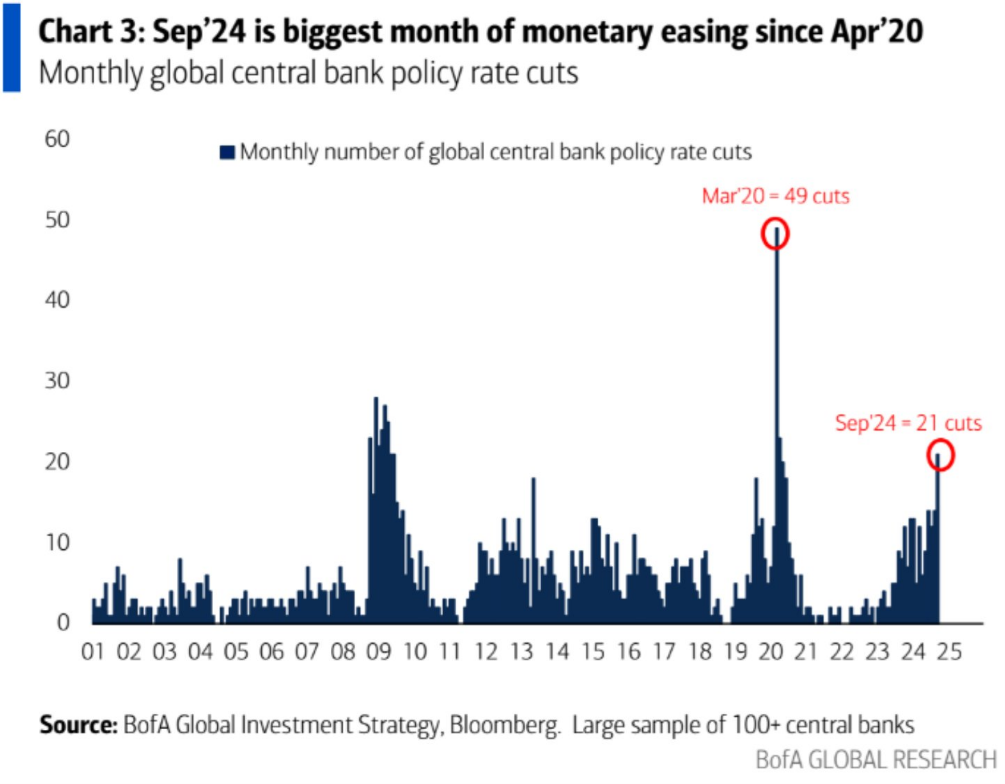

The gates have opened for the global liquidity system.

Source: BofA Global Research

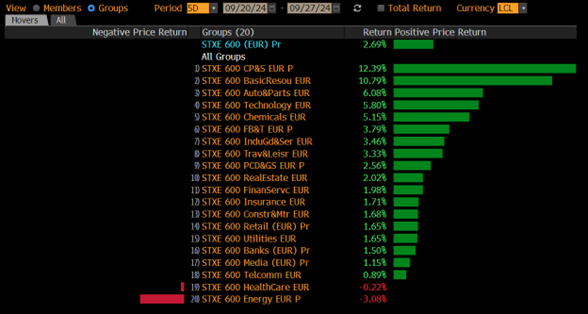

Below is sector development for the broad European index since July 1. Unsurprisingly, the winners are consumers and real estate. As you know, we have a lot of real estate exposure in the fund.

Source: Bloomberg

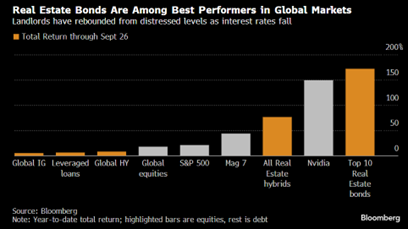

Hard-pressed real estate bonds and hybrid bonds are, so far, the world's best asset class this year.

Source: Bloomberg

The Fed's double rate cut on September 18 was a welcomed feature and, after some hesitation, was well received by the world's financial markets. Donald Trump commented on the decision by stating that the economy is "in a very bad shape". Jerome Powell said: "The US economy is in a good place and our decision today is designed to keep it there".

Source: HEDGEYE

On September 25, the Riksbank (Swedish Central Bank) lowered interest rates for the third time in a short time and laid the ground for two more interest rate cuts this year. As a new feature in the communication, it was also said that one of them could be a double lowering. Excellent and it is needed as today's real interest rate is far too high. Amid all this, the Swedish krona strengthened, and our own basic analysis is that the strengthening will continue next year when foreigners, who a year ago thought the Swedish banking system would have major problems with their real estate exposure, will come back and buy attractive Swedish assets.

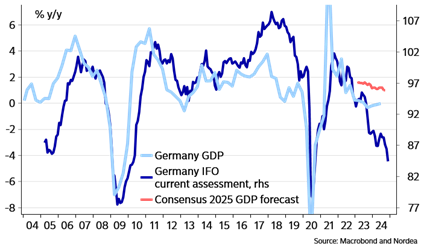

The Fed and the Riksbank are, as usual, behind a bit, but the central bank that once again appears to be completely disconnected from reality is the ECB. It would be desirable, to say the least, if they start acting on their mandate and significantly lower the policy rate. Europe is very much at a standstill and the worst is Europe's former engine, Germany. The regression below with German GDP growth in blue and German IFO as the leading indicator against expected GDP growth. This could mean that next year's growth will be significantly lower than today's expectations.

Source: Macrobond, Nordea

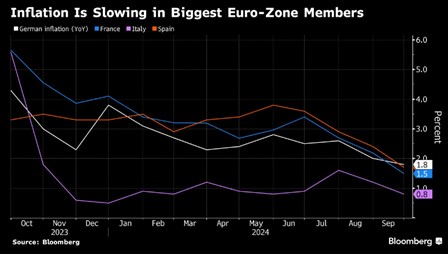

The major European countries now have inflation below two percent. What is the ECB waiting for?

Source: Bloomberg

Germany has made many serious mistakes in the last 10-15 years. In 2011 after the Fukushima accident, a hasty decision was made to shut down a fully functioning nuclear power industry and instead rely on Putin to kindly supply gas. It didn’t really work out. Instead, coal-fired power plants have increased in importance and today make up about a third of the country's electricity production! Not in vogue. Many years of doping with a weak euro in combination with a China that devoured German products made the dependence on China too great. The 2015 refugee crisis didn't help either. Volkswagen, which on Friday 27 September issued its second profit warning this year, also recently flagged that for the first time in its 87-year lifetime it may close one of its factories in Germany. A bleak sign of the times. Despite this, the German stock market has hit new annual highs on a continuous basis, but it is mainly driven by companies such as SAP (technology), Commerzbank (under the courtship of UniCredit) and Rheinmetall (defense). Smaller companies have it worse.

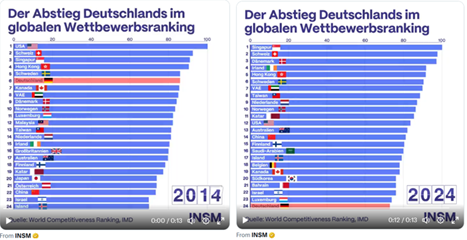

The picture below showing the collapse of Germany's global competitiveness is extremely serious. Sweden's position appears to be largely unchanged. As a parenthesis, following the sale of our last shares in Commerzbank, the fund currently has no exposure to Germany, which I believe is the first time in my time as a manager of European equities. We keep on searching as there are many fine and attractive companies in Germany, despite everything mentioned above.

Source: INSM

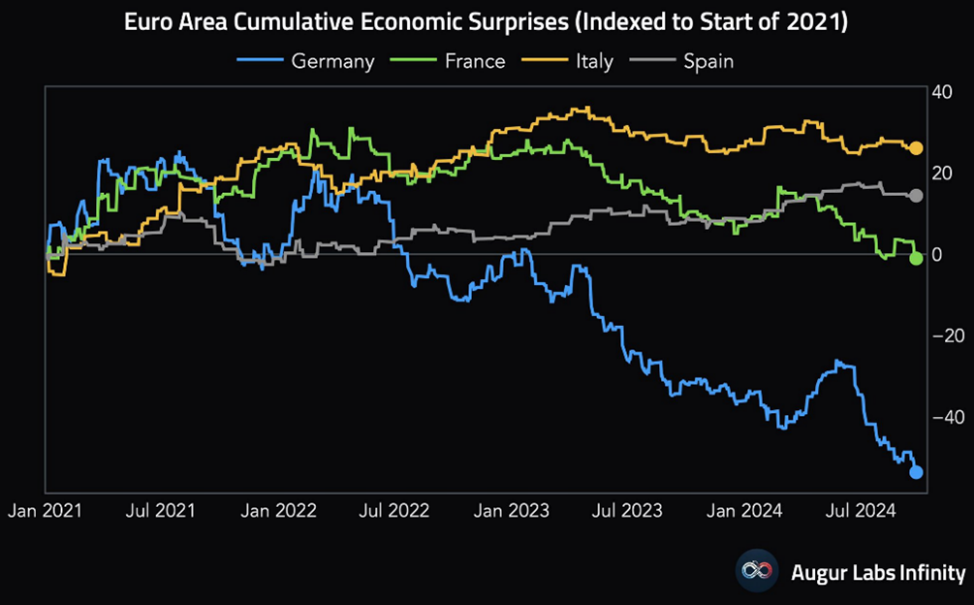

The European Economic Surprise Index. A telling picture.

Source: Augur Labs Infinity

The entire European establishment got a proper and justified kick from former ECB chief Mario Draghi, when a few weeks ago he presented his conclusion on what it would take for Europe to wake up and stop falling back behind in global competitiveness. 800 billion euros a year, or five percent of GDP, needs to be invested to be able to challenge the United States and China, which have expanded considerably since the financial crisis. Draghi also advocated for less bureaucracy and regulations that make it enormously difficult for European companies (also applies to the financial industry). The contrast between Draghi's conclusion and the opposition in Sweden, which wants to introduce a 35-hour working week, is significant. See a short summary in the clip here: https://x.com/tunguz/status/1833478861813657787

Source: Bloomberg

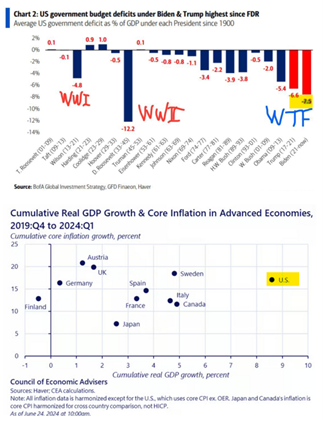

It's a bit of an elephant in the room, but America's impressive economic development over the past 15 years has also come at a price. The national debt has accelerated to extreme levels and the budget deficits under both Donald Trump and Joe Biden have been larger than ever in times of peace. The US today pays 3 billion dollars a day in interest. Regardless of who wins the election in November, neither candidate intends to balance the budget. It will either be tax cuts from Trump or increased public investment from Harris.

See the images below with first the budget deficits and then the accumulated GDP growth between 2019 Q4 – 2024 Q1. Note that Sweden stacks up well, and the next two years will cause Sweden to distance itself further to the right (our view). Also note Germany…

Källa: Haver, CEA calculations

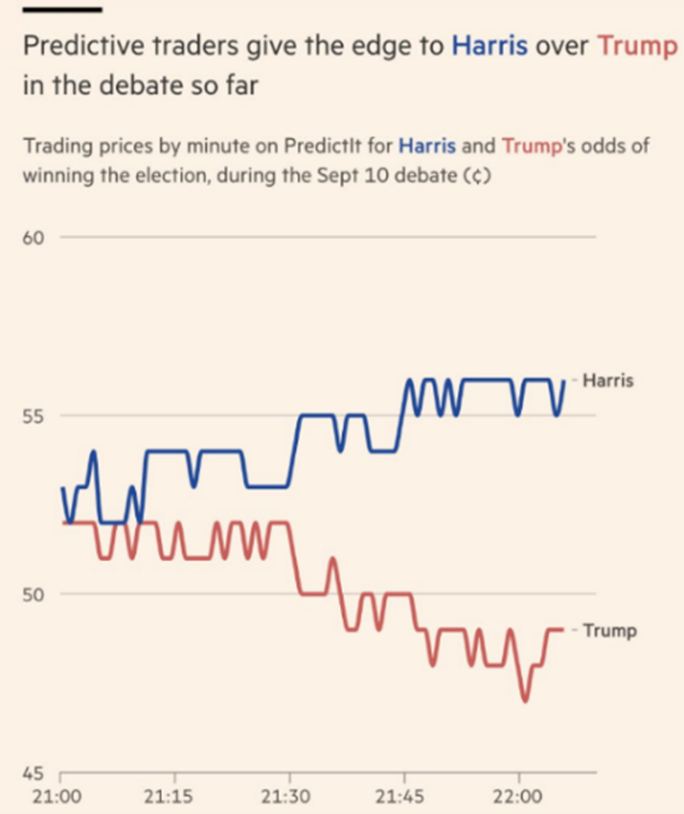

Donald Trump was unrecognizable in the debate with Vice President Harris a few weeks ago. It was a success for Harris, which can be seen in the image below, showing the odds continuously during the duel. 30 minutes into the debate, Donald Trump began accusing migrants in Springfield of eating people's dogs and cats.

Källa: Financial Times

Källa: X

https://x.com/packyM/status/1834222216214429867?t=mC9yUkHOjcwzYitADxv4iA&s=09

We memorize this version for a rainy day.

Källa: Financial Times

Portfolio Companies

September is usually a quiet month in terms of reports and company news. It gives us more time for company visits and analysis work with a focus on new ideas. During the month, we participated in a conference in Paris and met about 15 companies. Among them, we met Sacyr and Euronext, two companies that are in our portfolio today, and both of which gave a positive impression. From Paris, we also bring with us several exciting drafts for ideas that can possibly be included in the portfolio in the longer-term future.

Volution

The last time we wrote about the British ventilation company, Volution, was in July, and we wrote the following:

" With a record strong balance sheet, there is plenty of room to make acquisitions. Historically, Volution has acquired companies that, after three years on average, generate an operating profit that corresponds to approximately 18% of what was paid. Due to that yield profile, acquisitions are appreciated by the market.”

During the month, we once again saw proof that the market appreciates Volution acquisitions. In September, Australia's Fantech was acquired; by far Volution's biggest acquisition to date and the stock responded by increasing 10% on the day it was announced.

Fantech has sales of just over £90m and was acquired at a multiple of 8-9x EBITDA (which we believe equates to 9-10x EBIT). After the acquisition, Australia (and New Zealand) will account for around 30% of sales (compared to around 10% previously). We expect the acquisition to add more than 10% to earnings per share before any synergies. On our updated estimates, Volution is trading a couple of notches higher than historically, but we still think the company looks very attractively valued given its track record. Based on our numbers, the company is valued at 13x EBIT for the fiscal year 2026, which ends in July. The stock rose 9% in September and has risen 41% for the year.

Lindab

Another ventilation company that is very active on the acquisition side is, as you know, Lindab. In September, it acquired the French distributor ATIB with annual sales of approximately SEK 250 million. ATIB is the fifth acquisition for 2024 and together these companies have sales of around SEK 1.2 billion. This corresponds to around 9% of Lindab's sales in 2023. Lindab does not usually advertise what it pays for each individual acquisition, but we know that the multiples are typically low.

The Lindab share has started to get rewarded for its serial acquirer profile. The stock market can now also probably look ahead towards a 2025 when at some point we should see organic growth again. The stock rose 6% in September and has risen 42% for the year.

4imprint

One share that continues to perform weakly is 4imprint. The reason is probably that the market worries about weak economic data in the US. 4imprint is relatively cyclical and with close to 100% exposure to the American market. Our view is that this recession risk is more than well embedded in the valuation today. In addition, we have begun to see signs of brightening in the gift advertising market, where 4imprint is active. The stock fell 6% in September and has risen 9% for the year.

Campari

It has been challenging to own Campari in 2024 and hopefully that peaked in September. The turmoil began late on Friday afternoon, September 13, when the stock suddenly fell 5-6% during heavy trading. It turned out that Campari's relatively new CEO, Matteo Fantacchiotti, during a call with investors, said that the recovery in the American market was somewhat slower than expected.

Late in the evening, the company sent out a press release saying that the comments about the US market were general and not Campari-specific. On Wednesday, December 18, the CEO resigned. Later that day, Lagfin, which is the family holding company with 51% of the capital, announced that they intended to buy shares for 100 million euros in the market (just over 1% of the company) as the share price did not reflect the company's true value.

We hope and believe that the share will now begin its comeback. The company is one of Europe's fastest growing beverage companies with a unique portfolio where Aperol and Campari are the two most important products. Continued strong growth, lower raw material prices and a strong price picture mean that profit growth over the next two years is just over 35%. The P/E ratios for 2025e and 2026e are approximately 17x and 15x, respectively. As the share price fell, we increased the position, and we bought more shares even during the turbulence described above. The stock fell 9% in September and was then down 26% on the year.

Cargotec

Finnish Cargotec was one of the fund's best contributors during September without specific news. However, we noted that many Finnish engineering companies had a strong month, such as Cargotec's spin-off Kalmar where we have owned shares since 1 July. Our guess is that the valuation gap between Finnish and other Nordic industrial companies closed somewhat. The share rose 9.4% in September, and adjusted for Kalmar, the share has risen a whopping 70% this year.

SLP

During the month, SLP did exactly what we wanted, namely, to take in more capital to continue expanding in an environment where the real estate market looks better than it has for a long time. In total, the company took in SEK 1.1 billion, which will be used for further acquisitions. The loan-to-value ratio fell thanks to this from 47 to 38%. In other words, the balance sheet is strong. As the share trades at a premium to the net asset value, the net asset value per share increased by 4% at the same moment the money came in.

SLP believes that there is no shortage of interesting properties to buy. The company has a focus on slightly smaller logistics items that are too small for larger players. Therefore, competition is quite low in SLP's bidding processes. Typically, SLP would rather buy 10 smaller properties for SEK 100 million each than one large property for SEK 1 billion. We continue to like SLP and believe the stock has good prospects of doubling in the next five years. The stock fell 4.5% during September and has risen by 12% this year.

Biotage

Biotage had a weak September without any specific news. The stock fell by 5% but has risen by 40% this year.

Summary

Time flies when you're having fun and we're now rolling into the last quarter of the year. The US election in a month is the absolute highlight of the quarter and some turbulence is almost guaranteed. Before then, the last reporting season of the year starts and there has been a deluge of profit warnings in primarily cyclical consumer companies, such as VW, BMW, Mercedes, Stellantis and Husqvarna in Sweden.

From a portfolio perspective, we have made some changes in the past month. We have sold our last Commerzbank shares which we started buying in November 2022 around 8 euros and sold around 13 euros. We have also received large dividends. Unfortunately, we missed the latest uptick that occurred when the Italian bank, UniCredit, bought into Commerzbank. We have also sold our shares in the London Stock Exchange after a good performance in recent months.

Proceeds from sales have been used to increase existing holdings as well as initiate two new smaller guard positions, British Smith & Nephew and French Bureau Veritas. Smith & Nephew is a restructuring story where the company's stock in recent years has performed significantly worse than similar companies in the same industry, see five-year graph below. A new management team has implemented a push, and this summer one could see the first signs that that work is beginning to bear fruit. We monitor and follow until the next report is released.

Source: Bloomberg

Bureau Veritas is a French quality company in the testing and certification industry. They help their customers with various tests, inspections and certifications to ensure that they comply with rules, regulations, etc. Here too we have bought a smaller position pending new information in the next quarterly report.

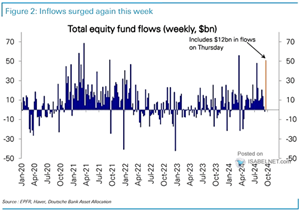

Inflows to US equity funds continue and was, last week, at near record levels. This despite a constant debate that the American economy is possibly headed for a hard landing.

Source: EPFR, Haver, Deutsche Bank Asset Allocation

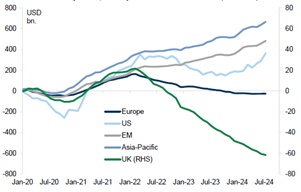

Europe has not, at all, had the same development in inflows as the USA. The picture below is through to July. Also note the line for Great Britain. With such outflows, one almost begins to wonder if there will be any capital left? It is an excellent reason to be invested as the huge outflows have created investment opportunities that are unusually good. This is also the reason why British companies have been bought up hand over fist this year. Did I hear someone mention Brexit?

Source: Goldman Sachs

Driven by attractive valuations, acquisitions in Europe continue at high pace. Several spin-offs have also been announced to highlight the hidden values that exist in the companies. Our own Cargotec is a good example of that. It is an excellent trend and the board and management feel the pressure to work more actively than before to defend their independence. In September alone, we have seen SKF and Continental announce spin-offs. BASF is also considering spinning off part of its operations. We have recently seen bids for TI Fluid and Rexel, as well as a fourth bid for Rightmove. Swatch is considering going private and LVMH founder Bernard Arnault bought 10% of Moncler a few days ago.

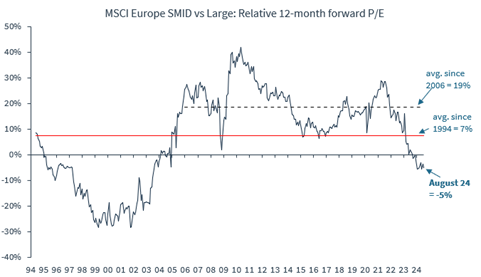

Smaller companies continue to trade at a significant discount to their historical level.

Source: Kepler Cheuvreux

Below the development for smaller companies relative to larger companies compared to the inverted real 10-year interest rate. A first observation is that smaller companies did not keep up with the latest drop in interest rates. A second observation, and more relevant, is that the real interest rate will continue to fall.

Source: Goldman Sachs

The talk of the town in recent weeks has been UniCredit, which one evening bought 4.9% of Commerzbank for 13.20 euros per share. The seller was the German state. It apparently came as a negative surprise and was not appreciated by either Commerzbank or the German state. (The fact that the German state both sells shares and then is dissatisfied with this is, in itself, quite comical.)

In a short time, UniCredit (which is considerably larger and more profitable) has built up a position of 29.9% and they obviously want to take over the bank. German trade unions have of course also expressed their displeasure. We find it strange that Chancellor, Olaf Scholz, who was previously finance minister and a member of the European banking union, spoke warmly in favor of a consolidation of the European banking sector. But when some Italian bank woos, it's not good enough. If one has not earned enough to cover one’s capital cost in the last 20 years, one should probably adopt a humbler attitude and keep calm. It is as if we, as a fund, were to perform worse than the market for 20 years and then be completely ignorant when someone else thinks they can do our job better and more efficiently.

Below is a picture of bank consolidation per country, with the five largest banks' market share in each country. Great Britain and Germany on the far right. There are 1,300 banks in Germany. The five largest banks in the US have a 36% market share.

Source: UBS

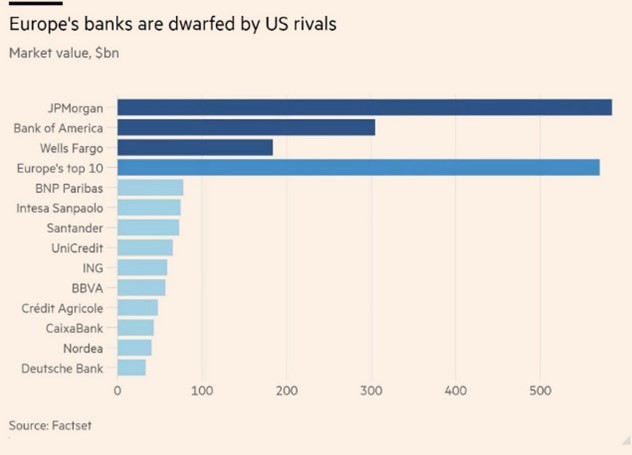

Market capitalization of the major American and European banks.

Source: Factset, Financial Times

In summary, we perceive the game plan for the coming quarters as follows:

• The famous Fed put is, with the double rate cut and given today's interest rate, back in play.

• Interest rate cuts will continue in a steadily over the next 12 months.

• Next year, consumers will begin to feel a significantly improved purchasing power driven by interest rate cuts, a defeated inflation and rising real wages. In addition, as in Sweden, significant fiscal interventions such as tax cuts starting in January 2025.

• Economic development in Europe will accelerate next year. Sweden is likely to emerge as the winner with high growth figures.

• The US economy is slowing from high levels.

• Latest US unemployment data showed a four-month low, so the economy is still holding up well.

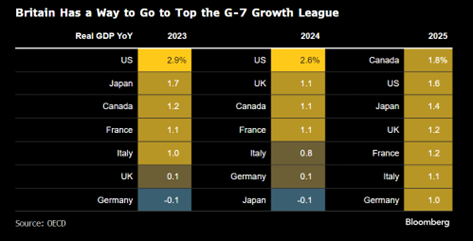

Below is the expected GDP development for some relevant countries. Sweden's GDP growth next year is expected to be around 2.6%.

Source: OECD, Bloomberg

For the European stock market, we perceive the situation as below:

• The discount on European shares relative to American is the highest ever.

• The discount for European small companies in relation to European large companies is at the highest level.

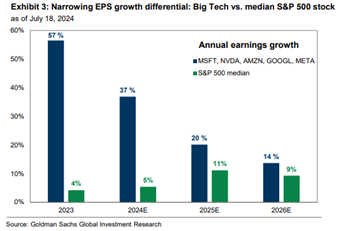

• Earnings growth for the S&P500 2025e-2026e is a cumulative 19%. P/E 2025e 19.4x.

• Profit growth for SXXP600 2025e-2026e is accumulatively 16%. P/E 2025e 13.1x.

• Earnings growth for European small caps, and as an average from several different data sources, for 2025e-2026e is about 30-35%. P/E 2025e about 10x.

• Small companies are the most interest-sensitive stocks, both on the way up and on the way down. An enormously sharp rise in interest rates in a short time, which hit small company valuations hard, is now reversing and will likely contribute to rising valuations.

• The breadth of the stock market has increased, which makes for better quality in the reversal. Since July, the equally weighted S&P500 has risen by 9%, while the Nasdaq 100 has only risen by 2%.

• The reason for this is probably that the profit growth of the large tech companies in relation to other companies is decreasing.

Source: Goldman Sachs Global Investment Research

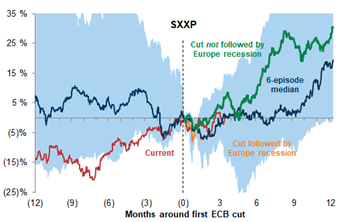

Below is the historical development of the broad European index after the ECB's first interest rate cut. We do not believe in a recession.

Source: Goldman Sachs

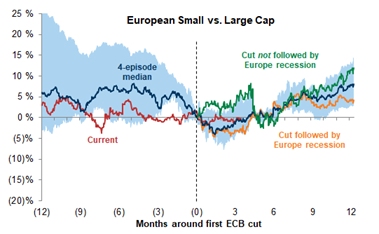

The development in Europe for smaller companies in relation to larger companies after the ECB's first interest rate cut. A few months after the first interest rate cut, smaller companies have developed stronger than larger companies.

Source: Goldman Sachs

The sum of all the above is that, excluding geopolitics, things look better than they have in many years. The election in the USA will most likely bring some extra noise and air pockets. If the Republicans lose, we hope that this time Donald Trump accepts the outcome, otherwise it could get messy for a longer period.

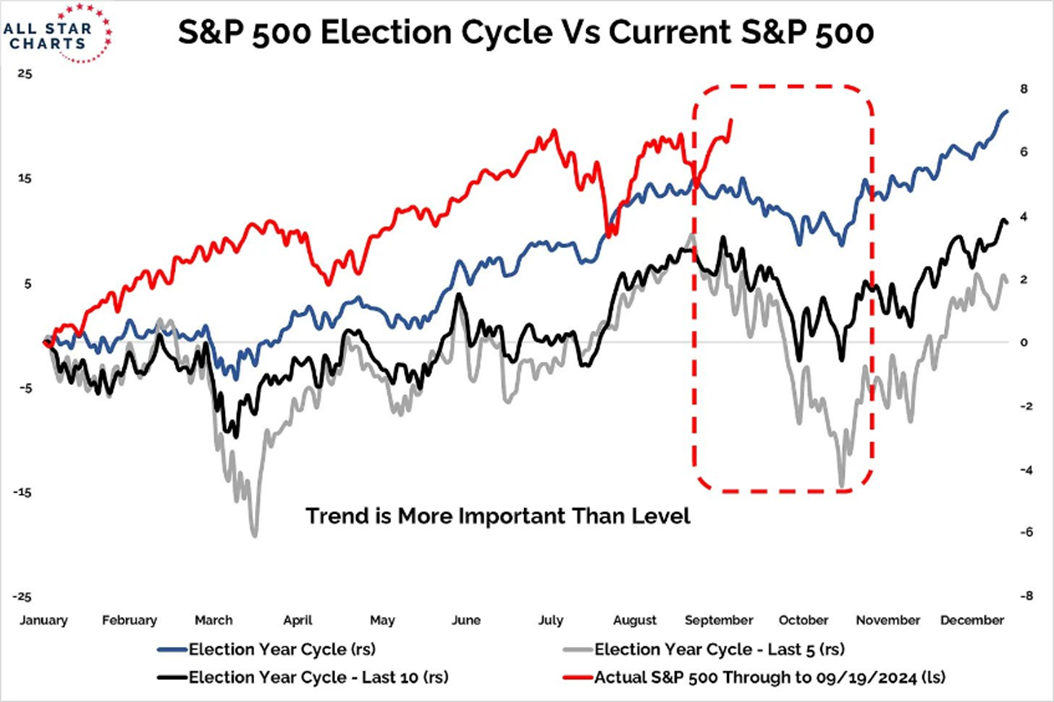

There may certainly be another reversal during October, but the underlying feeling is still strong and we believe we will reach new highs before the end of the year. Below is how it has looked historically during election years on the American stock market.

Source: Goldman Sachs

In conclusion, we look forward to the reporting season where we tend to have a high hit rate. No guarantees are promised, though. It can also be said that it was absolutely right to change the strategy just over 13 months ago. In the last 13 months, the fund has risen by 25.6% percent, while our comparison index has risen by 10.3% percent.

Many thanks for your interest!

Mikael & Team

Malmö, October 3rd 2024

IMPORTANT INFORMATION. This is a marketing communication. Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested. Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.