Readers of our monthly reports know that the fate of the Inflation Reduction Act (IRA) is critical for renewable energy stocks. Uncertainty over its survival, especially since Trump took the lead in the polls last summer, has made some renewable energy tech segments, including solar, almost uninvestable. Now, with the Republican-controlled Congress nearing agreement on the so-called “One Big, Beautiful Bill,” which includes IRA cuts, we are approaching the risk-clearing event we have long awaited.

We were caught off guard and the fund underperformed when the first House draft was substantially better than expected for most renewable energy tax credits. Although the final bill included substantially more cuts to tax credits, we now believe uncertainty has been substantially reduced for most solar segments.

Below we briefly summarize the most important changes to tax credits relevant for solar and our portfolio. This is not a comprehensive review of all credits.

45X: Better Than Feared, Crucial for Onshoring

The Advanced Manufacturing Production Credit (45X), created by the IRA in 2022, incentivizes domestic production of clean energy components. Ironically, most new plants were built in Republican states, which may help explain why this credit survived almost unchanged with only a one year earlier phase down. This is great news for US manufacturers, especially First Solar (FSLR), our only long-term solar holding since Trump’s election. If the Senate changes anything, it will likely be to delay the phase-down again. FSLR remains the biggest IRA winner and benefits further from Trump’s tariffs on global imports, especially China, as FSLR sources most inputs domestically and avoids Chinese-made polysilicon.

PTC / ITC: Front-Loaded Demand, Medium-Term Noise

The Clean Electricity Investment Tax Credit (ITC) and Production Tax Credit (PTC) have been around in some form for decades and were both enhanced by the IRA. For example, ITC allows most clean energy projects a 30% tax credit, potentially rising to 60% with domestic content or other adders, and was originally available through at least 2032. The first House draft accelerated the phase-out to start in 2029 and end in 2031, but the adders survived. The final bill was harsher, projects must now be in service by the end of 2028 and construction commenced within 60 days of the bill’s signing. This will be tough for smaller developers, but large players like Nextera Energy (NEE) and AES, both in our portfolio, should manage, having already safe harboured projects into 2027. Moreover, there are strong signals that the Senate will moderate the phase-out. In any case, this will likely pull forward demand and trigger a construction boom over the next two years, benefiting developers and EPCs like Quanta(PWR) and Mastec (MTZ), both portfolio holdings in ‘Grid Services’.

FEOC: The Silent Killer in the Fine Print

Unfortunately, the frontloading of demand described above can be hampered by the House’s Foreign Entity of Concern (FEOC) language, which aims to block not only Chinese-owned companies from US tax credits but also any project using Chinese components, a near-impossible standard today, though it would be a major tailwind for FSLR.

However, given the US’ AI race with China and power being one of the key constraints, we expect the Senate to soften the FEOC language and phase in restrictions over several years. Nevertheless, Chinese companies will likely be squeezed out of the US market, essentially their only profitable market. We remain short Chinese solar stocks with US manufacturing exposure.

Residential Solar: Roller Coaster Off the Tracks?

Republicans have never favoured residential solar, seeing it as a subsidy for wealthy homeowners. The House initially claimed to remove this subsidy, saving about USD 77bn over 10 years, but it only cut credits for direct ownership, leaving leased solar systems still eligible for 30-40% tax credits. As leasing already accounts for over 50% of the market, we anticipated this would quickly approach nearly 100%, making the actual savings much smaller than intended. Nevertheless, as we expected the first draft to be the worst, we adjusted our positions when direct-ownership-focused companies sold off and leasing specialists rallied.

However, the House addressed this “loophole” in the final bill, explicitly making leasing systems ineligible as well, continuing the rollercoaster for residential solar stocks. Unfortunately, the text was written in haste and introduced a new error that still allows leasing to qualify for tax credits. We expect the Senate to correct this issue, and we do not expect Senate Republicans to push to retail the subsidy. If residential solar loses tax credits at year-end, expect a rush of installations followed by a 50–70% demand slump over the next years. We believe this risk is not fully priced into US-focused residential solar stocks.

Outlook: Policy Volatility, Structural Tailwinds

Regardless of the final cuts to the IRA, we see this as a clearing event for solar stocks, making the sector investable again. Moreover, the bigger picture is that this is not just about solar, it is about US energy policy in the age of AI. If the US wants to win the AI arms race, it cannot afford to slow solar deployment or remove manufacturing tax credits. We believe these realities will ultimately shape the legislative outcome.

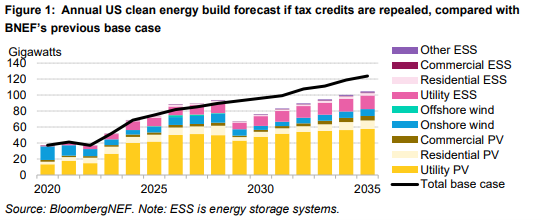

What if our assumption is incorrect and the Senate does not reverse some of the cuts outlined above? Bloomberg New Energy Finance has estimated demand for solar, wind and batteries (ESS) through 2035, based on the scenario where the House bill passes the Senate unchanged. As illustrated in the graph below, demand is expected to accelerate through 2028, followed by a sharp fall across most sub-sectors in 2029. Notably, utility-scale solar is projected to rebound relatively quickly from 2030 onwards. Furthermore, even though utility-scale solar installations are expected to dip in 2029, we expect FSLR to remain sold out as it continued to benefit from a tariff advantage over foreign-produced solar panels.

By 2029 however, the US will have a new administration that could have a very different view of the importance of renewable energy. Considering the expected strong growth in power demand and the time it takes to build alternative power like nuclear and gas power plants, we would not be surprised if new subsidies will be made available in some shape or form.

We continue to prefer utility-scale stocks, with FSLR as our largest position. We have also added a significant stake in Nextracker (NXT), the leading tracker provider for utility-scale projects, and maintain smaller positions in other utility-scale names. We remain net short residential solar companies and Chinese panel makers listed in the US, while staying long renewable developers like NEE and AES, as we see AI-driven power demand expectations increasing.

We will continue to monitor the bill’s progress in the Senate and provide updates as the situation evolves.

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Over 15 years of investment experience spanning both public markets and private equity.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Spent six years at Horizon Asset in London, a market-neutral hedge fund.

- Started working with Vidar Kalvoy in 2012.

- Five years in Private Equity at Morgan Stanley.

- Began his investment career in the technology sector at Swedbank Robur in Stockholm in 2006.

- Holds an MSc in Engineering from the Royal Institute of Technology (KTH), Stockholm.

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Has managed energy equities since 2006 and brings more than 20 years of experience in portfolio management and equity research.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Head of Energy Investments at Horizon Asset in London for nine years, a market-neutral hedge fund.

- Experience from energy investments at MKM Longboat in London and equity research in the technology sector in Frankfurt and Oslo.

- Holds an MBA from IESE in Barcelona and a Master’s in Business and Economics from the Norwegian School of Economics (NHH).

- Before entering finance, he served as a lieutenant in the Royal Norwegian Navy.

IMPORTANT INFORMATION. This is a marketing communication. Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/. Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested. Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.