Before making any final investment decisions, please read the prospectus, its Annual Report, and the PRIIP of the relevant Sub-Fund here

This material is marketing communication

An article highlighting the opportunities in expanding the electrical grid.

The energy transition is experiencing truly unique tailwinds with both the US Inflation Reduction Act and the EU Net Zero Industry Act. We are in the second phase of the renewable energy transformation, which is driven by energy security and safekeeping of supply chains as much as the fight against climate change. In our view, this second phase will be substantially larger and more significant, and it will accelerate the energy transition.

However, it will not be smooth sailing despite the incredibly favorable regulatory backdrop. Last month we talked about the rapid improvements in regulation around permitting, especially in Europe, which has been a key bottleneck. As permitting is about to become less costly and faster the next bottleneck is likely to be grid connection and transmission capacity. When we switch from an energy system that transports a mix of fossil fuels and electricity to one that increasingly transports electricity, it is understandable that the physical wiring requires upgrades. This is true for most regions in Europe and most states in the US. Before a renewable energy project is connected to the grid it requires an approval to connect. These interconnection approvals are becoming more costly and are already prohibitively expensive in some regions.

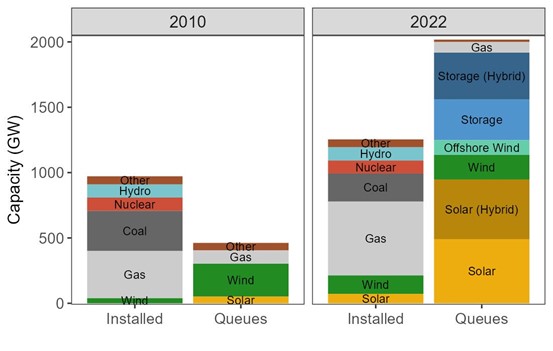

In the US, it is not only an ageing grid, but it is also a political issue as different states have different electrical systems. There are currently close to 2,000 GW of clean energy projects waiting for interconnection in the US, according to Lawrence Berkeley National Laboratory. This is approximately 50% more than the combined output of all the currently operating power plants in the country. See below.

Existing U.S. capacity (2010 and 2022) compared to interconnection queue capacity (2010 and 2022).

Source: Lawrence Berkeley National Laboratory.

The good news is that there is tremendous interest in developing renewable energy projects. The bad news is that the interconnection queue is growing faster than projects are installed. Interconnection times have already increased by 2.5x since the mid-2000s, now averaging 3 years for solar and wind projects in the US. The growth in renewable energy would have been even stronger if not for this issue.

To allow for more connections, the transmission grid requires substantial upgrades and expansion. For example, Bloomberg New Energy Finance (BNEF) estimates that USD 21tn will need to be spent to expand and reinforce the grid to reach net zero by 2050. This is a substantial investment opportunity for the fund.

During March, the FERC (Federal Energy Regulatory Commission) chairman said it is working ‘feverishly’ to advance a transmission reform, a key step in alleviating the grid connections bottleneck. This makes a lot of sense as the projects currently waiting for interconnection are alone enough to reduce US’ Green House Gas emissions in 2030 by 50% from the peak in 2007 and put the country firmly on the path to net zero by 2050. We are hopeful.

Joel Etzler

Portfolio Manager Coeli Renewable Opportunities

Vidar Kalvoy

Portfolio Manager Coeli Renewable Opportunities