This material is marketing communication.

Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class’ return. The information below regarding returns therefore differs from the returns in other share classes.

Before making any final investment decisions, please read the prospectus, its Annual Report, and the KID of the relevant Sub-Fund here.

FEBRUARY PERFORMANCE

The fund’s value increased by 4.6% in February (share class I SEK), while the benchmark increased by 5.0%. Since the change of the fund’s strategy at the beginning of September 2023, the fund’s value has increased by 32.1% compared to an increase of the benchmark by 31%.

Source: Coeli European

* Adjusted for spin-off of Rejuveron

** Includes September 1 (strategy change to long-only implemented September 4 2023)

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

EQUITY MARKETS / MACRO ENVIRONMENT

The speed and power of the news flow in recent weeks have been of a rarely seen magnitude. An almost daily flow of updates from new AI solutions has caused waves of casualties and the rotation from software companies to more traditional manufacturing companies has been of historic proportions. The latest buzzword and the one applied by investors is “HALO” – Heavy Assets, Low Obsolesence. Simply put, companies that have a physical production or assets and are relatively immune to automation.

The US Supreme Court invalidated President Trump’s tariffs in February. A major defeat and we shall see how it plays out.

Moreover, we sifted through reports from our companies in a market with the highest price reactions on reporting day in many years. After catching our breadth from that, we woke up on Saturday, February 28th to witness the US and Israel having launched a full-scale attack on Iran, which killed its leader Ayatollah Ali Khamenei on the very first day. At the time of writing, the only thing that is certain is that uncertainty is growing. One can attest to that the world is moving faster than in the late 1980s when, after the lectures in Lund, I cycled home as quickly as possible to listen to P1 (BBC 1 / state radio) at 12.30 where all the stock prices on the Stockholm Stock Exchange were read out.

Despite the turbulence, the European stock markets continued to develop well and Sweden performed the strongest. OMXS30 has risen almost 12% in two months (after a relatively weak 2025) compared to Stoxx600 which, measured in SEK and over the same period, rose by 5.4%. The US continues to develop weakly, with the S&P up 0.5% this year and the Nasdaq down 2.5%. Measured in SEK, the corresponding development is -1.5% and -4.4%. Crushing.

The picture below shows the development since President Trump won in November 2024.

Source: Goldman Sachs

The fund performed well in this challenging environment to say the least and rose by 4.6% in February compared to 5.0% for the benchmark. MSCI Europe Small Cap rose by 3.5% measured in SEK (+2.3% in euros) and Carnegie Small Cap rose by 2%. S&P500 fell by 0.9% (-0.4% in euros). Despite a performance "just" in line with the market, we are satisfied given the minefield of negative outcomes that was avoided. We were unusually active in terms of adjusting positions around reports and our analysis continued to deliver, as did our companies.

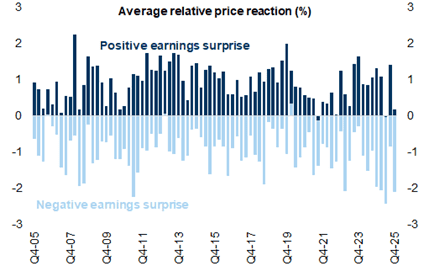

The picture below shows that there have been unusually weak price reactions this reporting season, especially for companies that have come in better than expected, something we recognize.

Source: Goldman Sachs

When the research house Citrini Research released its report “The 2028 Global Intelligence Crisis” (Link), it immediately sent shockwaves through the stock market, with sharp drops, especially for software companies around the world. The report describes a scenario of what it could look like in 2028 when AI has truly been implemented among companies. There was no news, just the author’s opinions, but it still sent great fear into the investor community. Paul Krugman compared it to Orson Welles’ radio play War of the Worlds in 1938, which created panic in the US. This time, however, there were no aliens, but the successes of AI technology and a future scenario of mass unemployment and a stock market in free fall.

Another significant piece of news announced late on Friday, February 27th, was that the Pentagon stated that they were blacklisting Anthropic, the AI company which developed Claude, restricting it from buying Nvidia chips, among other things. The reason is difference in opinions about how much the US military should be allowed to use Claude, and thus Anthropic was classified as a security risk.

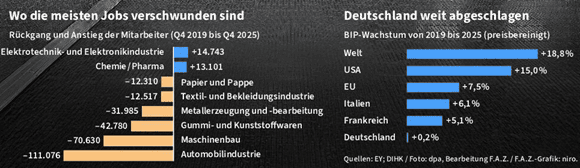

Europe's engine, Germany, has been idle for three years. Below are the developments for different industries and changes in employees. More than 100,000 employees have been forced to leave the car industry, and, on the right, you can see that Germany's GDP has been unchanged for seven years (!) while world GDP has risen by 19%.

Source: EY, DIHK

That's also why German Chancellor Merz was a bit upset recently when he gave a speech and said it's time to roll up our sleeves and shift gears. Link to X.

At the same time, in Sweden, the Left Party, the Green Party and the Social Democrats are now advocating for a shorter working week. The timing feels about as good as when the same parties changed the conditions for nuclear power just over 10 years ago and ensured that one of the world's best, cleanest and most stable energy systems was dismantled. None of the politicians involved have had to pay a political price for it.

Source: X

Moving on to more positive news as there is now clearly visible increased activity in Germany.

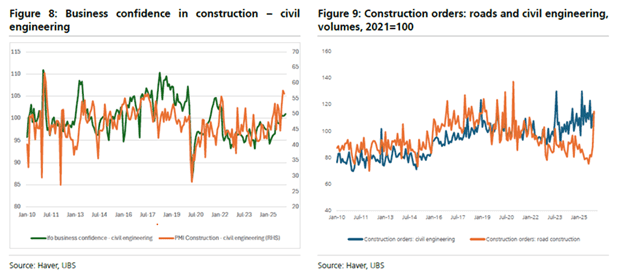

In Europe, there are also clear signs that economic activity is increasing, see construction investments below.

Source: Haver, UBS

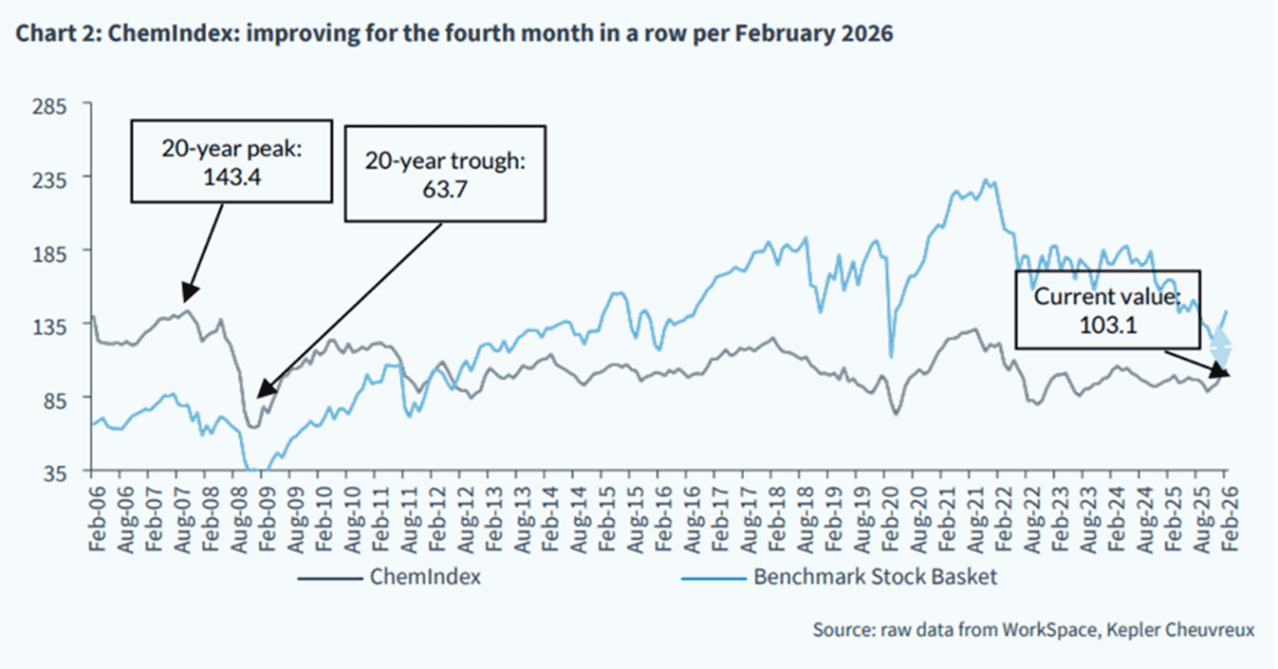

A European chemical index showed increased activity in February for the fourth consecutive month.

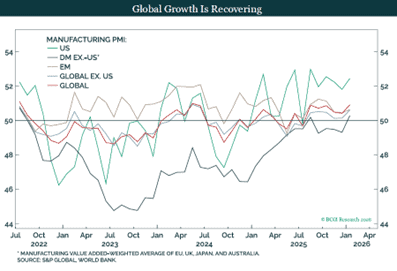

There are also clear signs of a recovery underway on a global basis.

Source: BCA Research

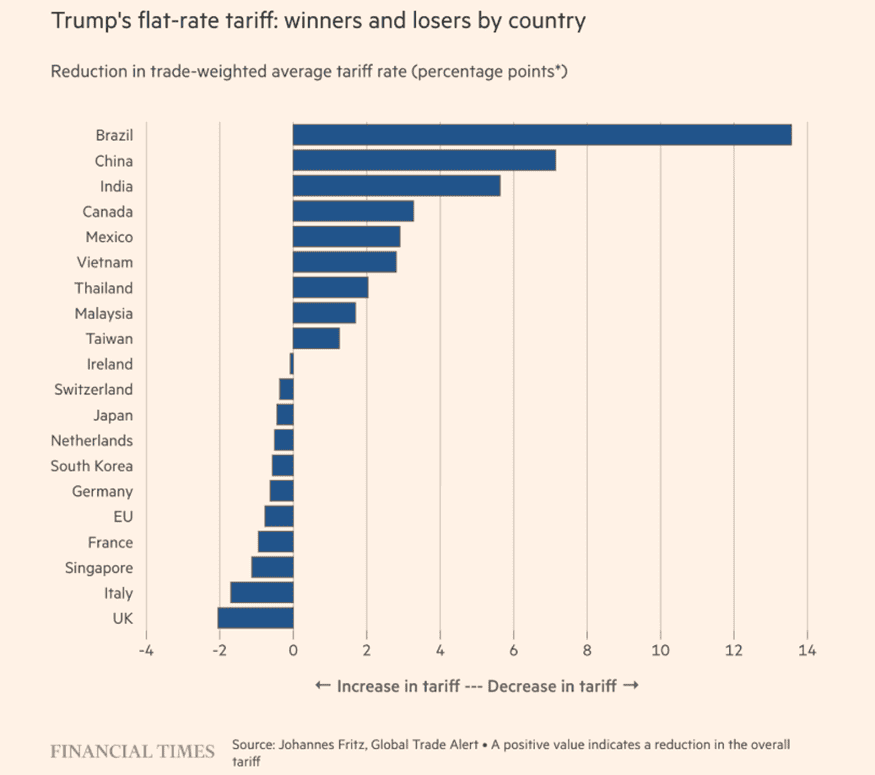

Donald Trump and his administration were dealt a major blow when the Supreme Court struck down the tariffs that were forced through last year. The court also ruled that American companies are entitled to recover $130 billion from the US government. Donald Trump and his entourage were not lenient in their criticism and a new type of tariff that can only be in effect for five months was to be imposed immediately. At first, he announced it was 10%, but the next day, probably after a bad night's sleep, the level was increased to 15%.

Below are the winners and losers of the new tariff rate. Trump's biggest opponent at the top and close ally Britain at the bottom.

Source: Financial Times

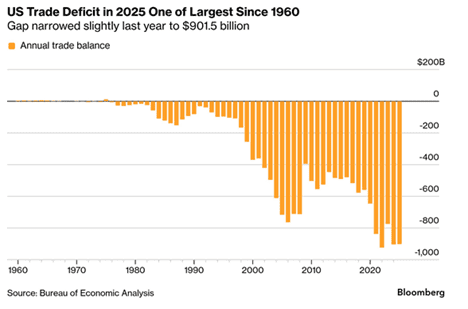

Donald Trump is now in a delicate situation where the budget and trade balance cannot reasonably be improved as the administration has communicated. The mid-term elections are near, and it will be interesting to follow the development. Funnily, the same day data was published that showed an unchanged trade deficit with the world and a record deficit with the EU, Mexico and China. In their defence, changes like this lag, but still. It is clear to most that the tariffs introduced last year have been paid by American companies and customers, not by foreign companies.

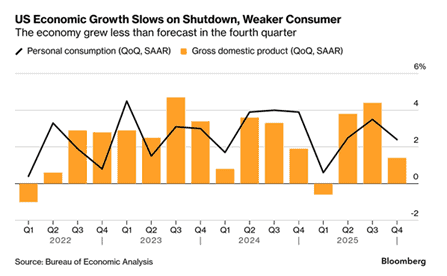

Simultaneously it was a cold shower when the US GDP data was released for the fourth quarter. Expected growth was 2.8% and it came in at 1.4%. A large part of the explanation was probably due to the shutdown of many government institutions and agencies during the period.

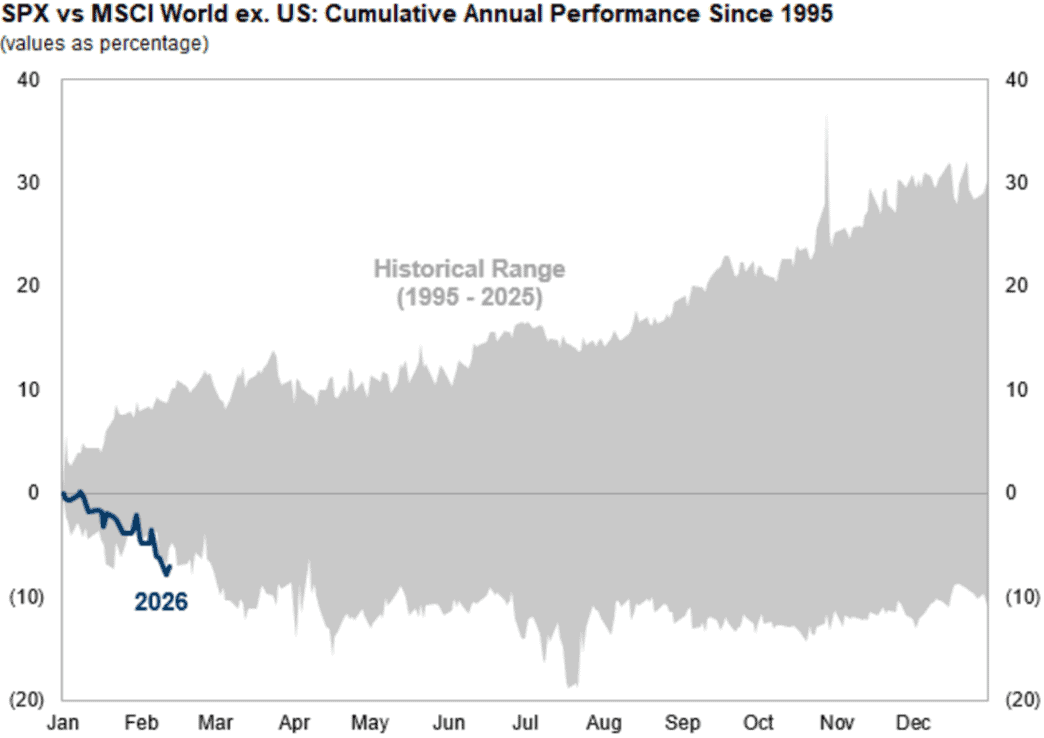

All the above has of course contributed to the US stock market having its worst start relative to the rest of the world since 1995.

Source: Goldman Sachs

PORTFOLIO COMAPNIES

A summary of the reporting season

Even though not all our companies have reported, we are leaving a good reporting period behind us. With 23 reports in hand, 17 of the companies have reported results that have been in line with expectations or better. Among the companies that surprised positively relative to expectations, we have Rational, Asmodee and FLSmidth. Lindab, Scandic Hotels Group and Konecranes are among the weaker reports.

During the year, our Swedish companies in particular have underperformed in relation to our foreign companies. Large outflows among Swedish small-cap managers have recently been reported. This is probably an explanation for many astounding price reactions among Swedish companies that, despite good results, have often seen falling share prices. Since we have an overexposure to Swedish small-caps versus our benchmark, this has contributed negatively to the performance during the beginning of the year. When things turn around, we believe there can be a quick reversal. When that happens, is of course more difficult to predict.

In a stock market where the concept of AI is on everyone's lips, we have seen the share prices of software companies, in particular, fall enormously. Other sectors with greater intangible than tangible assets have also lost a lot. Including consultants and marketing companies. Our portfolio has been relatively spared from the AI craze, and we believe that over time the stock market will begin to differentiate between winners and losers even within the sectors that are currently seen as AI losers.

Van Lanschot Kempen

The Dutch Private Banking company ended the year on a good note with better-than-expected results. Strong inflows, market share gains, good cost control, and a positive guidance for 2026 contributed to the share price rising 11% in February.

We believe that Van Lanschot is a clear takeover candidate. Last year, the major Dutch bank, ING, bought a major stake in Van Lanschot. Private Banking is often one of the banks' more attractive revenue streams, and ING probably sees value in owning the market leader in the Netherlands in full. At the same time, Van Lanschot remains family-owned and is unlikely to be sold for a pittance. If there is no takeover, we are still satisfied with owning a company that should be able to grow profits by high single digits and that has a dividend yield of around 5–6%. Combined, this provides good conditions for a good annual return.

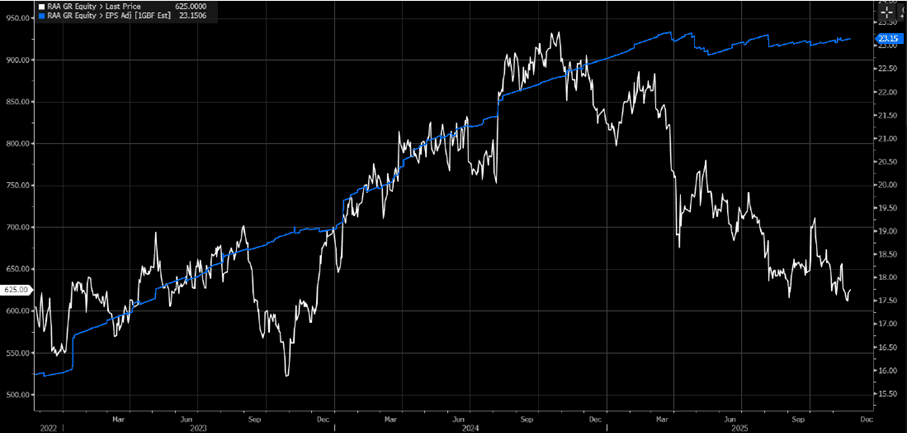

Rational

Since the end of last year, we have built up a medium-sized position in German Rational, which sells professional kitchen equipment. More specifically, it is the company's flagship products "iCombi" and "iVario", which, among other things, use steam technology to save restaurants time and money. Anyone who visits restaurants in Sweden, where Rational has a very high market share, can often glimpse Rational products in the kitchens.

This is one of Germany's more recognized public quality companies. It has a leading market position in a structurally growing market. Over the past ten years, the company has grown by 5–10% on an organic basis. Operating margins exceed 25% and the return on capital employed exceeds 50%. The company is family-owned and has basically been built entirely organically, without major acquisitions. The income statement is clean and nice without various adjustments and with minimal capitalized development costs.

The problem with this type of company is often that they are valued too high. But in 2025, the stock fell by about 20% even though profit estimates (blue line) rose during the year.

Source: Bloomberg

The market was concerned about tariff headwinds (Rational has most of its production in Germany) and lower volume growth. Currency headwinds did not help sentiment either.

After several tumultuous years due to the pandemic and Russia’s invasion of Ukraine, Rational has not recruited as many salespeople as historically. In 2025, it accelerated new recruitment. Together with the launch of the new product, iHexagon, more clarity on the tariff situation and German stimulus, we believe that volumes can start growing again.

During the month, the company released a short press release that indicated that we may be on to something: both organic growth and operating profit were better than the market expected. The share responded by rising by 13% on the same day the preliminary results were announced. The price came off its highs and closed February with a gain of 9%. We hope to return to this topic later.

Babcock

The defence stock lost about 6% in February after a rise of 15% in January and 148% in 2025. At the time of writing, unrest in Iran has just begun again and we would not be surprised if defence stocks start March with price increases. The company's restructuring is largely complete, and the share revaluation is complete. With a more reasonable valuation and a lower potential for positive earnings surprises, we have reduced our position.

Beijer Ref

During the month, Beijer Ref recovered most of January's decline, which came because of a weaker-than-expected Q4 report than expected. The share rose by around 12% in February. One theme in the share is the weak North American market, which accounts for around 23% of sales. Several US companies in the sector are now guiding for a weaker start to the year with a subsequent recovery in the second half of 2026. We are projecting that 2026 will be another year with gradually increased margins, more acquisitions and good cash flows. Hopefully, we can also expect slightly higher organic growth. The share has traded sideways since 2021 with a profit estimate curve (blue line) that has risen steadily.

Source: Bloomberg

Konecranes

After a couple of strong reports and a subsequent sharp price increase, we chose to reduce our position in Konecranes ahead of the financial statements. The Q4 report was roughly 4% worse than expected, causing the share to lose around 12% on the reporting day. We took advantage of this weakness by increasing our position sharply again. The share price ended the month with a slight increase of 1%.

We believe that despite an appreciation from low levels, the Konecranes share looks attractive. We hope that the company uses its strong balance sheet to accelerate its acquisition pace of small and medium-sized add-on acquisitions, which should cost less and be easier to integrate. In addition, we believe that the company should use its cash for buybacks and/or extra dividends. Several industry indicators point to better times ahead, which should benefit Konecranes.

Asmodee

Asmodee shares continue to lag despite good reports and rose by 4% in February, which is broadly in line with the full year's performance. The latest report in the series once again beat expectations by a wide margin. Organic growth of 26% was clearly higher than the expected 9%, and operating profit was around 23% better. We also noted that the company's free cash flow improved in line with our expectations. Management also appeared more optimistic in its outlook for the future, despite facing more difficult comparative figures going forward. This is motivated, among other things, by the fact that 2026 is Pokémon's 30th anniversary, which should contribute to another good year for Asmodee's distribution operations.

Alm. Brand

The insurance company's share has not performed well this year despite financial results that were in line with expectations. After a strong year in 2025 for the share and the sector as a whole, sentiment has turned negative: among other things, it is related to a CEO resignation that we see as undramatic, a cold, and prolonged winter and fears about the possible impact of self-driving cars on insurance premiums (which we believe is far away and if so with a very gradual impact). The company is fundamentally strong, and we believe that it can continue to gain market share in Denmark in the coming years. The share lost 6% in February and had thus lost 13% for the full year.

Continental

Continental was the best contributor of the month in February, without any direct company-specific news. During the month, most of the major tire companies, such as Michelin, Pirelli, Nokian, Goodyear and Bridgestone, reported. The weakness in their reports was mainly linked to the truck segment and the US, where Continental has relatively low exposure. The forecasts for 2026 were broadly in line with what Continental presented at the end of January. The first quarter is expected to be weak due to inventory reduction, but a gradual improvement is expected thereafter.

Both Pirelli and Michelin are trading below their historical average multiples, and in addition, Continental's tire segment is trading at an implicit discount of about 35%. Continental is simply valued too cheap. The stock rose about 8% in February.

Kalmar

Kalmar delivered a report in February that was better than consensus across the board. What the market particularly took note of was the strong order intake, which was just over 13% better than expected. The strong order intake was partly driven by several larger orders, but it is something we have seen in almost every quarter since the spin-off from Cargotec. For the full year, order intake rose by around 8%, sales by 1% and adjusted operating profit by 3%.

The company has good momentum and forward-looking indicators continue to point to expansion within Kalmar's segment. The share rose around 12% during February and has risen 18% so far in 2026.

Hiab

Hiab released a report that was slightly weaker than expected, with order intake and operating profit 4 and 3% below expectations, respectively. Sales in North America are down to critical replacement levels and demand in Europe, despite growth of 8% in 2025, remains low.

Since 2019, sales have increased by 15%, while prices have risen by almost 25% during the same period. This says something about how close to rock bottom the company is in terms of volumes. At the same time, we see that American companies operating in Hiab's end markets are stabilizing and are cautiously optimistic about 2026.

Hiab has several clear opportunities for a strong 2026: Continued leverage from increased defence spending, a recovery in the European construction market and gradually better development among American customers during the year. The company also has net cash that we expect to be put to work on value-creating acquisitions. We see approximately 30% upside in the share over the next twelve months. The stock fell 4% in February.

Bonesupport

Bonesupport's fourth-quarter sales figures were already known, but operating profit was around 15% better than expected. Growth accelerated in the fourth quarter and the company showed impressive organic growth of 36% in the quarter and 40% for the full year. Sales in the US grew by 40% in the fourth quarter and 46% for the full year, with Cerament G continuing to be the main driver.

Sales in Europe picked up in the fourth quarter with growth of 18%, a clear acceleration compared to the previous quarter. Germany continues to be weak, while the UK is improving in line with new priorities within the NHS.

What finally made the share rise on the report day (after a crazy intraday movement of 17%) was comments about customer intake in the trauma application. At the end of 2024, the company had 15 trauma centres as customers and at the end of 2025, the corresponding figure was 140. Historically, about 50% of growth has come from new customers and 50% from existing ones. Given these data points, it is clear how the company is expected to achieve its guidance of over 35% organic growth.

The most interesting thing about the 2026 sales forecast is that it does not include any major contribution from Cerament V, where news of FDA approval is expected in the first half of the year. The company will hold a capital markets day in May, where we guess it will help investors segment their end markets and describe the path forward for Cerament G in spine treatment. The stock rose just over 9% in February.

Below is the sales trend per quarter since 2017.

Source: Bonesupport, Coeli European

SLP

SLP continues to deliver and the company is running like clockwork. The management result increased by 46% compared to the previous year and was thus a few percent better than expected. Earnings per share rose by a strong 33%. Despite the strong result, the share fell on the report day.

We are fairly certain that some small-cap funds utilized the liquidity in connection with the report. We are disappointed with the price development given what the company actually delivers. The picture below shows the development in net asset value since the start of 2019 – a development that few in Europe can match.

After the latest issue, we expect SLP to utilize its full acquisition capacity. Together with completed projects, we estimate that earnings per share could increase by almost 16% in 2026, which now means that the company is trading at a P/CEPS of 16.5x for the current year. The share was unchanged in February.

Source: SLP

SUMMARY

It's starting to get a bit much now with four shocks to the system in just two months. It started with Venezuela, then came Greenland, closely followed by new tariffs and now Iran. Despite that, European stock markets have performed well so far, driven by attractive valuations, rising profits, low positioning, rising inflows and a comparatively robust political system. Apart from rising profits, the opposite is currently true in the US, and this has led to a rare underperformance compared to the rest of the world.

Mag7, which now feels more like Lag7, is contributing significantly negatively to this development due to increasing concerns about how much of the profits will be left to the owners after huge AI investments and what the expected return on the investments will be. Three years ago, 43% of the profits were transferred to shareholders compared to the expected 16% today.

Source: Datastream, Kepler Cheuvreux

The direct return for some of the major global indices. Europe is around 3.5 %.

Source: Kepler Cheuvreux

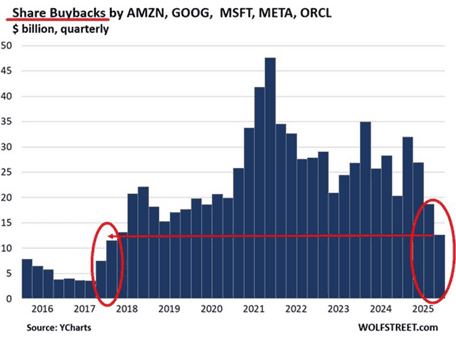

The extensive AI investments also mean that the significant buyback programs that have been underway in recent years are now expected to decrease sharply (and the companies have probably been the largest buyers of each share).

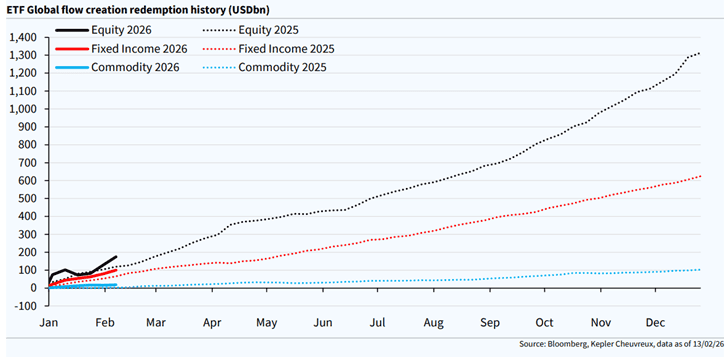

The inflow to the world's stock markets has gotten off to a good start this year.

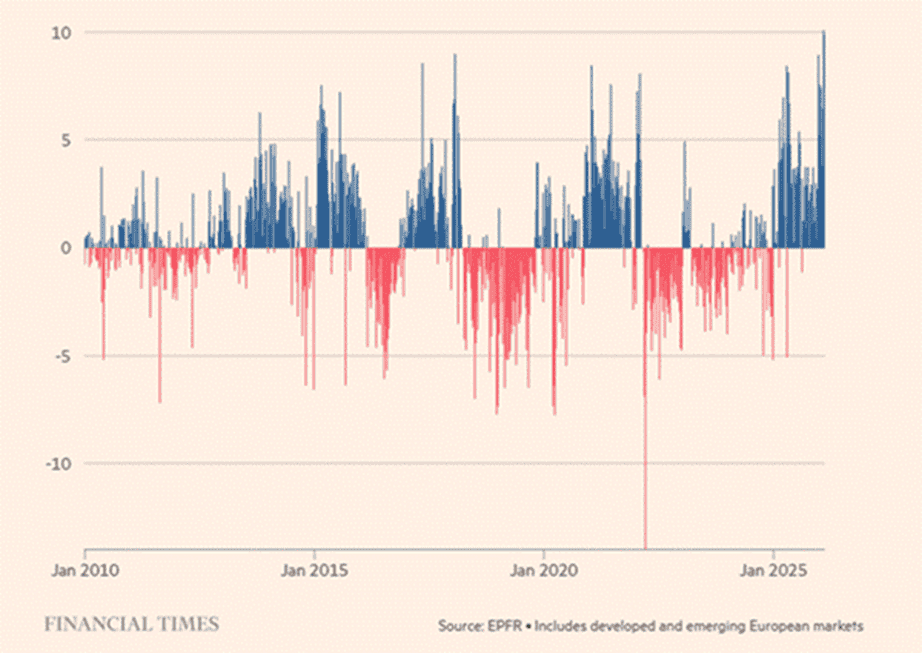

And more specifically, Europe has had and continues to have the largest inflows in probably 25 years. Below is the development since 2010.

Soruce: Financial Times

Strong inflows have helped the broad European stock indices measured in USD rise for 14 weeks in a row (!), which has never happened before.

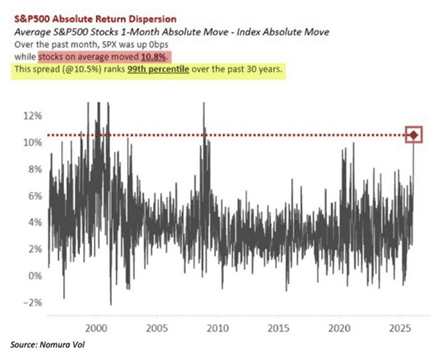

Beneath the surface, we can see that it has not been so calm. For starters, volatility at the individual stock level over the past month was in the 99th percentile measured over 30 years, beaten only by the periods during the financial crisis and the Dotcom bubble. The average stock in the S&P500 moved 10.8% while the index was unchanged. Unbelievable.

Source: Nomura Vol

Then we have the difference in development between more traditional chemical companies and technology companies.

Source: Goldman Sachs

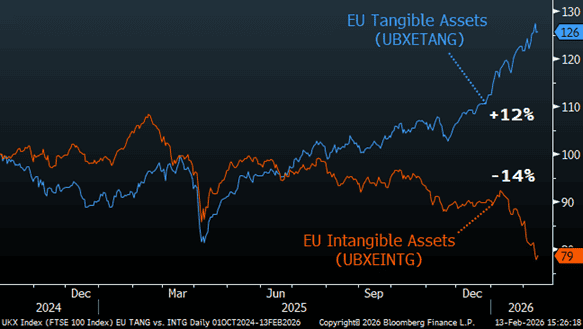

The difference in development between companies with high tangible and intangible assets.

Source: UBS

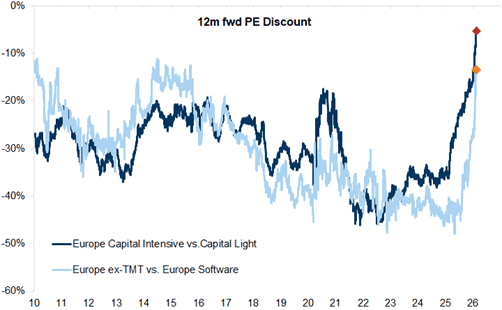

The discount for capital-intensive companies in Europe (dark blue line) relative to the broad market is almost down to zero.

Source: Goldman Sachs

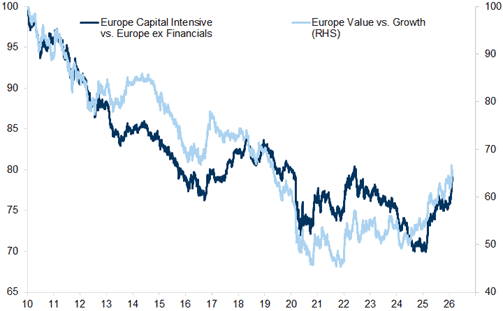

The development between capital-intensive businesses relative to the broad European index excluding banking (dark blue) and the relative return between value and growth stocks.

Source: Goldman Sachs

The fund has no software exposure.

Source: Goldman Sachs

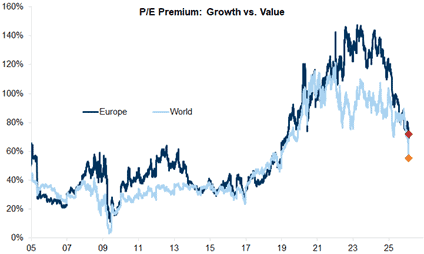

The premium for European growth companies has more than halved in a short time.

Source: Goldman Sachs

One thing that is also worth highlighting is the sharp decline in interest rates, both in the US and Europe. Below is the Swedish five-year interest rate, which has fallen significantly in a short time.

Source: Bloomberg

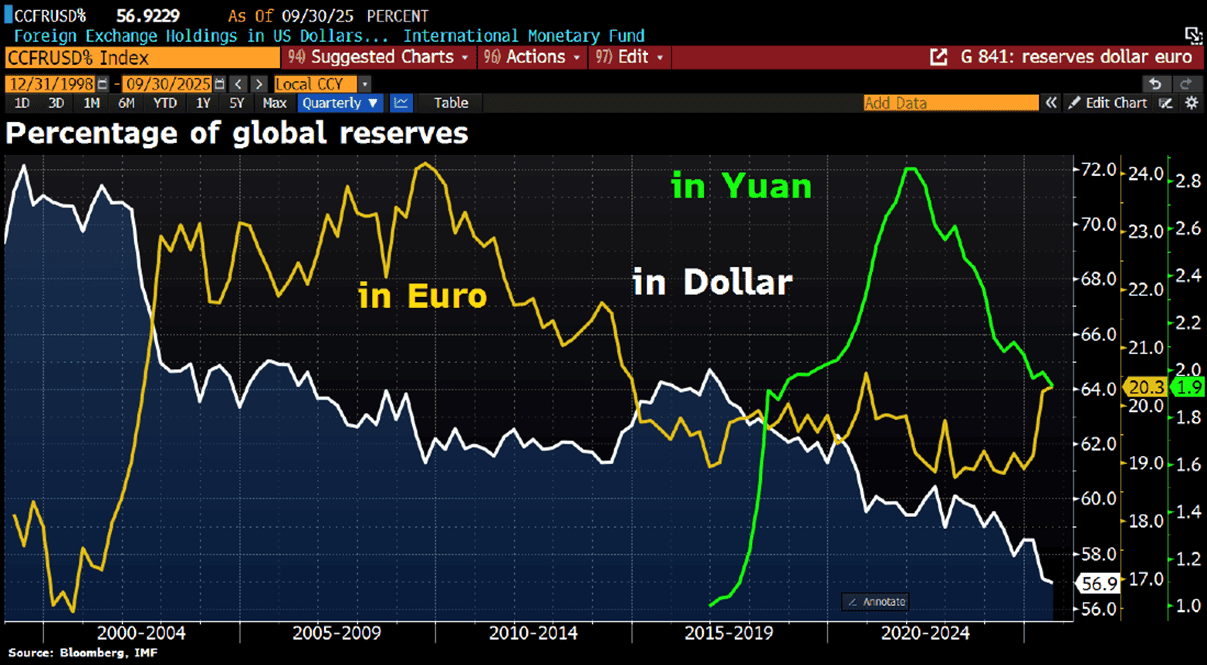

The US dollar is still on a downward slope in terms of total global foreign exchange reserves. We guess the white line correlates reasonably well with the rising US national debt. On Monday, March 2, the dollar strengthened significantly against all currencies.

The outcome of a prolonged crisis which is often the case (Ukraine, the Soviet Union in Afghanistan, the US and NATO in Afghanistan, the Iraq war, Yemen, Syria), is something to think about as US interest payments already exceed military spending and there is a generally reduced interest in allocating capital to the US. The war in Afghanistan cost the US 2.3 trillion USD. We will leave that pondering aside for now. It is much more pleasant to note the rise of the euro in the picture below.

Soruce: Bloomberg, Holger Zschaepitz

In summary, the uncertainty due to the new unrest as this is written on Sunday evening, March 1, is greater than it has been in a long time. Everything is moving quickly and the situation is changing by the hour. What determines the direction of the market from here is:

- How long will the war last?

- How long will the oil market be disrupted?

- Will the oil industry infrastructure be bombed?

- Will there be a new Iranian regime and if so, how will that look?

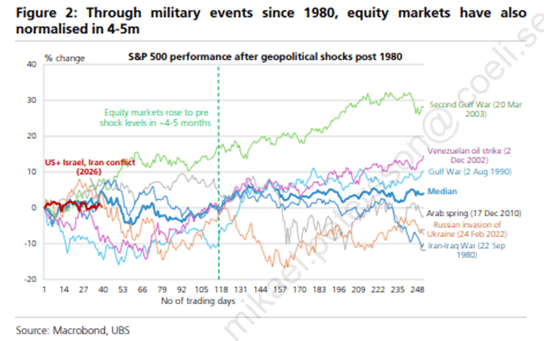

Donald Trump said that the attack could last 4-5 weeks but at the same time Israel has called up 100,000 reservists. The risks in the global economy have increased again and one can only hope that there will be some form of de-escalation in the near future. Donald Trump does not want any chaos (in the US). With a mid-term election fast approaching, the political incentives for a short conflict are very large. One can probably assume that there will be a number of unforeseen events in the coming weeks.

Historically, the market has recovered after 4-5 months after the outbreak of war. That said, this new conflict is potentially worse. On a positive note, the oil market is in unusually good balance.

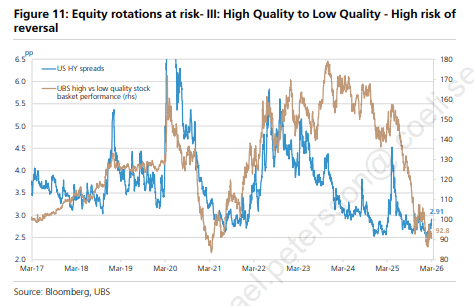

One might think that the trend from last year of quality companies underperforming lower quality companies (see beige line in the image below) should now reverse. If so, we believe it will benefit the fund's performance.

The final word is that we will wait, observe events and act gently. We have been through (too) many similar situations in the last 25–30 years. Opportunities will certainly arise in the coming days and weeks, and we are prepared. Our companies are also prepared, and they have time and time again proven to be incredibly skilled at parrying unforeseen events.

We thank you for your interest and wish you a nice first month of spring despite the events of the last few days!

Mikael & Team

Malmö, March 5th, 2026

IMPORTANT INFORMATION. This is a marketing communication. Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested. Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.