This material is marketing communication.

Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class’ return. The information below regarding returns therefore differs from the returns in other share classes.

Before making any final investment decisions, please read the prospectus, its Annual Report, and the KID of the relevant Sub-Fund here.

MARCH PERFORMANCE

The fund’s value decreased by 9.5% in March (share class I SEK), while the benchmark decreased by 4.4%. Since the change of the fund’s strategy at the beginning of September 2023, the fund’s value has increased by 19.5% compared to an increase of the benchmark by 25.2%.

Source: Coeli European

* Adjusted for spin-off of Rejuveron

** Includes September 1 (strategy change to long-only implemented September 4 2023)

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

EQUITY MARKETS / MACRO ENVIRONMENT

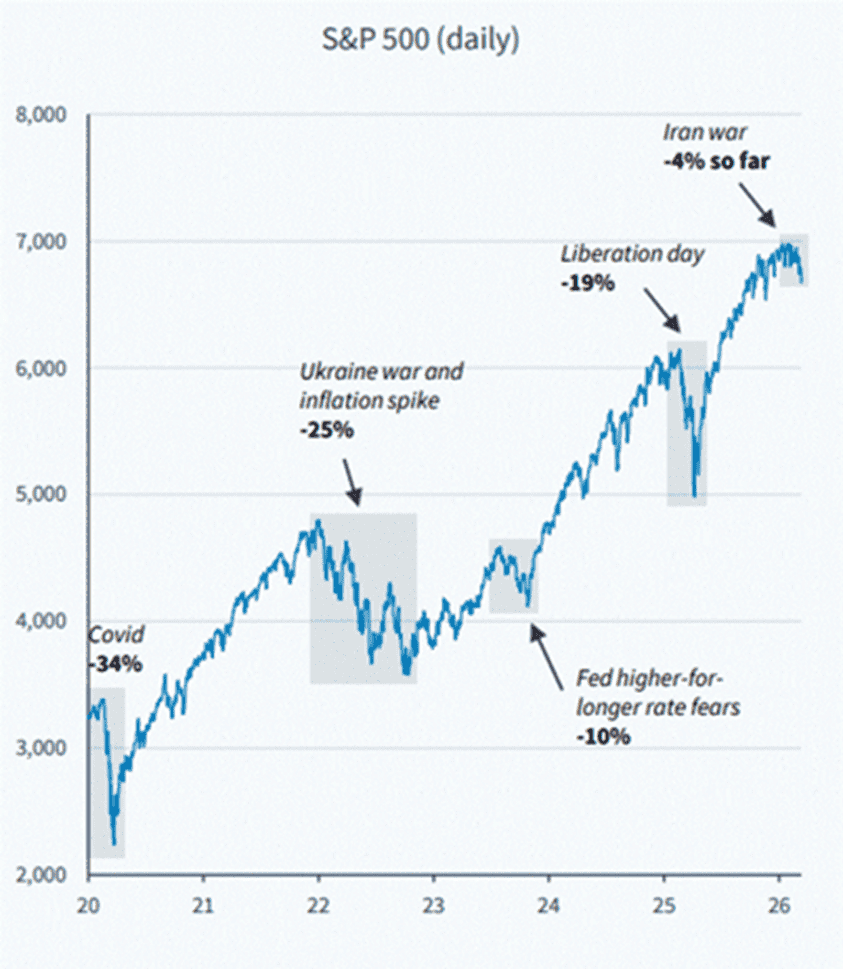

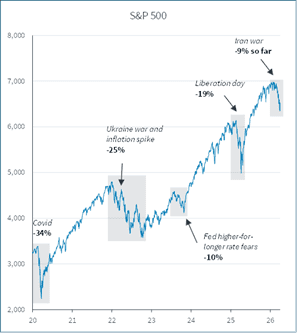

“There are decades when nothing happens, and there are weeks when decades happen.” Widely attributed to Lenin, which is a perfect description of the last few weeks. The conditions for 2026 looked good. There were hopes of a continued accelerating economy, better consumer confidence and a stock market that could slowly broaden and rise. Right now, these hopes do not look like they will be achieved. A seemingly ill-considered attack on Iran by the US and Israel led to five weeks of very weak returns on the world's stock markets, sharply rising interest rates and the largest increase in the price of oil ever in a single month.

Source: Goldman Sachs

The broad European index fell in March by 8%, OMX30 by 9.1%, and the S&P500 by 5.1% (all in local currency). The fund underperformed 9.5% percent compared to our benchmark, which lost 4.4%. The simple explanation for this was a clear underperformance in our industrial and consumer-related companies.

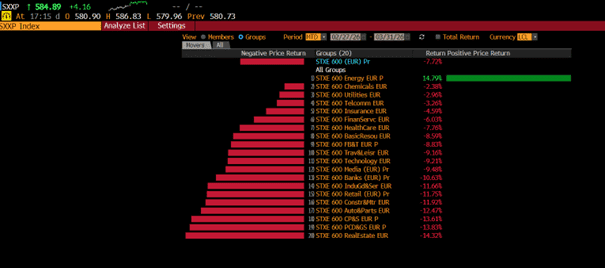

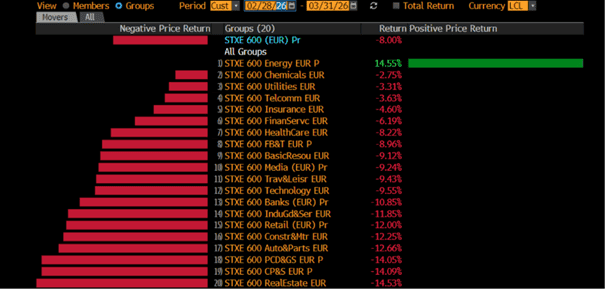

The image below shows sector returns for March. Almost a 30% difference in return during a month where Energy was at the top and Real Estate and Cyclical at the bottom.

Source: Bloomberg

The conditions that existed before February 28th and that generated a balanced return for the fund at the beginning of the year changed abruptly with the outbreak of war. We have adjusted and rebalanced the portfolio by selling our entire holdings in Kalmar and Babcock and initiated new positions in more defensive companies that we hope to return to in future monthly letters. We have also added a few names at low levels. More on that later.

The first quarter of the year summarized in a picture.

Source: Mohamed El-Erian, LinkedIn

Much could be said about the Iran war and its development, but we will keep it short as it changes by the hour. It is clear to the whole world that the attack on Iran was ill-conceived, without any thought of consequences and without a clear exit strategy. In addition, the enemy's resilience and ability to continue damaging important infrastructure despite the US's superior military firepower, which has knocked out most of the military-strategic value in Iran, have undoubtedly been underestimated. The regime remains in a new yet unclear constellation while still controlling the Strait of Hormoz. The Houthi rebels in Yemen pose the same threat at the entry point to the Red Sea. On the last day of the month, Trump commented to the Financial Times that he is nearly ready to withdraw from the war, even though the Strait of Hormoz will not be opened. He gives the impression of becoming increasingly desperate to end the war but has painted himself into a corner.

The administration is unsurprisingly going through a serious crisis of confidence at home and Trump and his colleague, Secretary of War, Hegseth (who is rumoured to be called “the secretary of war crime” in the Pentagon) have clearly demonstrated that they do not understand how dependent the US is on the outside world. Trump's boasting, aggressiveness and vulgar rudeness towards US allies have been met with a cold hand from most countries, who have also refused to provide assistance. It all feels a bit amateurish and the regime in Iran will pressure the US to make maximum concessions to stop the war. It feels a bit odd, but it is not surprising that the administration must resort to force from higher powers. Pastors pray over Trump in the Oval Office.

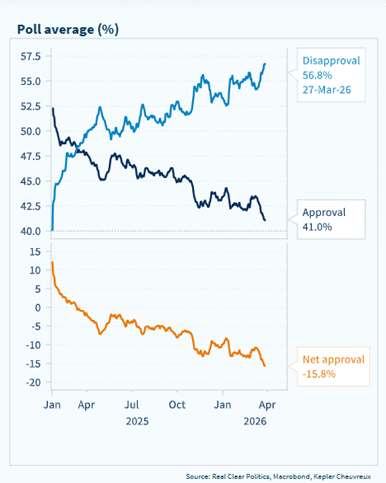

The proportion of dissatisfied voters in the US is increasing in line with the price of gasoline.

Source: Real Clear Politics, Macrobond, Kepler Cheuvreux

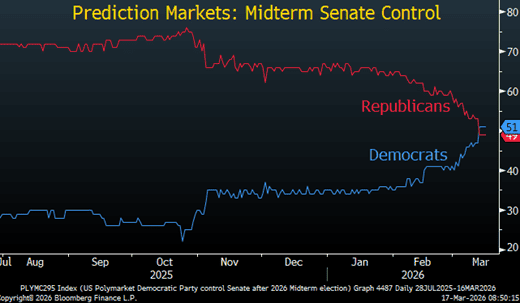

The American midterm elections will be largely shaped by developments in Iran.

Source: Bloomberg, UBS

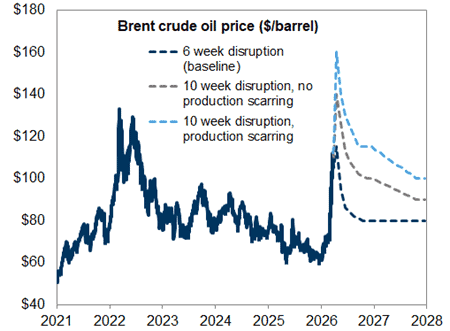

Basically, everything has revolved around the price of oil in the past month. The image below from Goldman Sachs shows their estimate of how the price of oil will develop depending on how long the strait is closed.

Source: Goldman Sachs

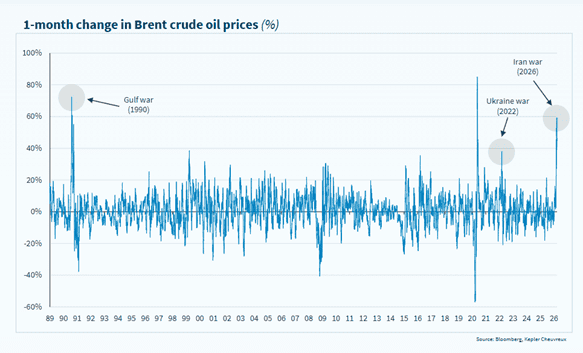

The sharp increase in oil prices will be written in history.

Source: Bloomberg, Kepler Cheuvreux

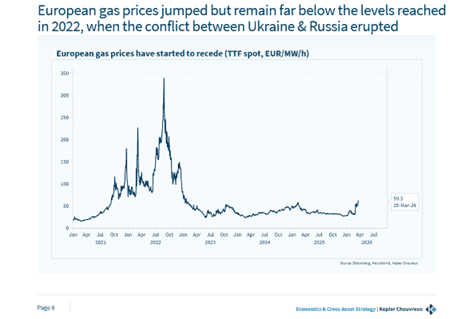

Gas prices in Europe have also risen sharply but are far from the levels of spring 2022 when Russia attacked Ukraine.

Source: Bloomberg, Macrobond, Kepler Cheuvreux

Interest rates around the world rose sharply in March. Below is the German 10-year, which quickly rose from around 2.6% to 3.1%, the highest level since the euro crisis in 2011.

Source: Bloomberg

It has been many years now since we experienced a normal, traditional stock market cycle.

Source: Kepler Cheuvreux

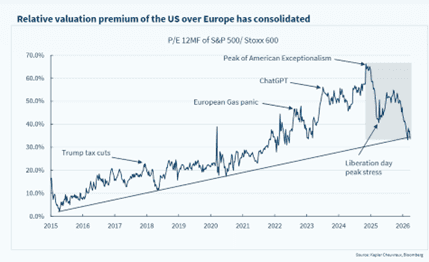

The highest level of valuation for the US relative to Europe coincided with Trump's election victory.

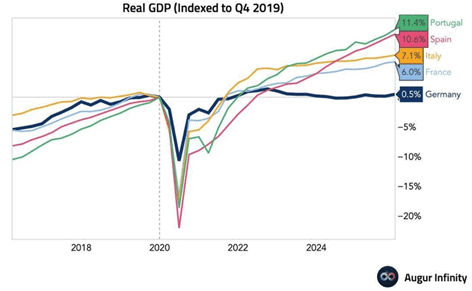

An interesting picture showing the GDP development in recent years for countries in southern Europe compared to Germany. How can Germany have been idling for almost 10 years, and yet be considered the engine of Europe?

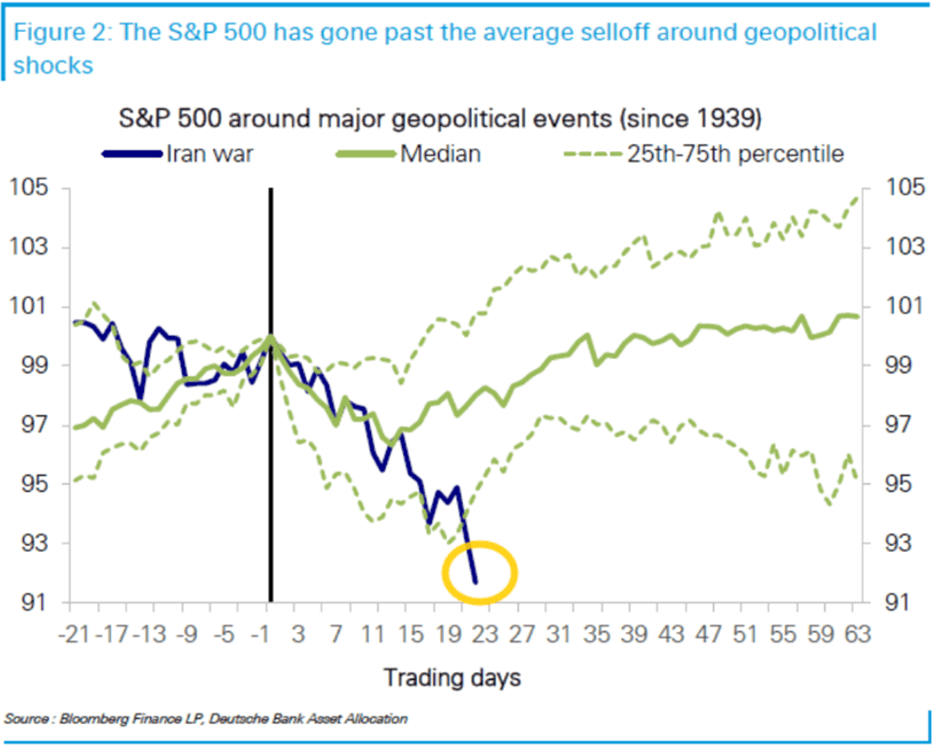

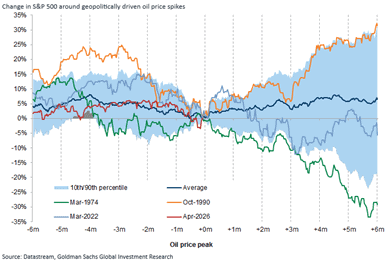

The chart below, which shows how the S&P500 has historically performed during previous geopolitical shocks since 1939, could be summarized as: worse than usual. For Europe, the declines have been even more severe, mainly due to the energy crisis that is hitting harder here. In addition, it can be noted that oil experts are significantly more concerned about the consequences than equity investors, which is something to keep in mind.

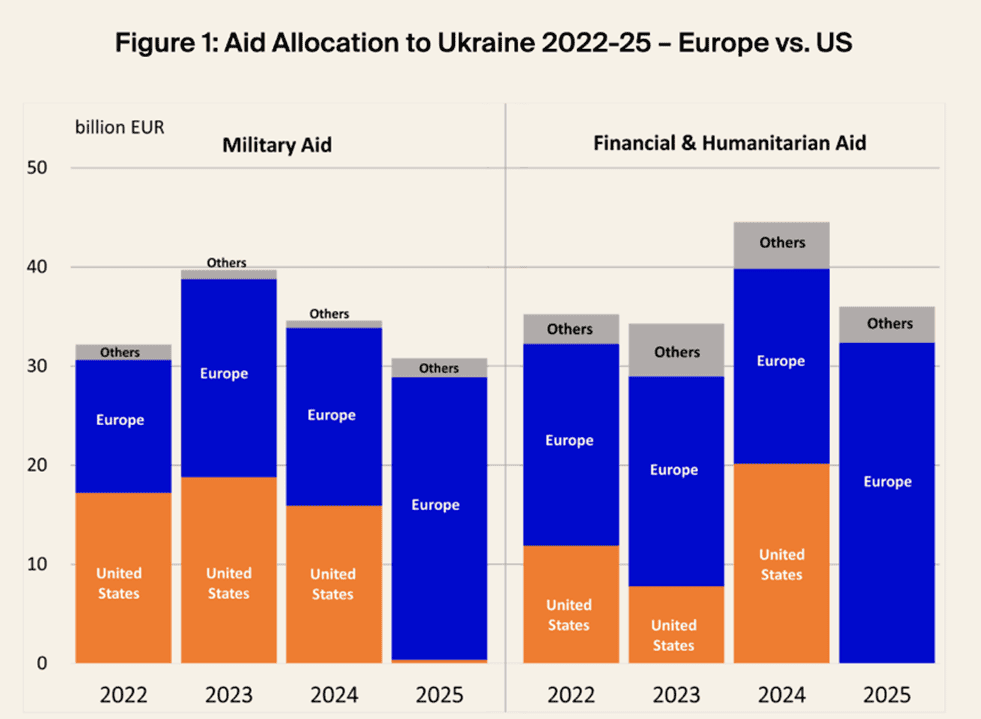

Trump has insulted most of the world's leaders in recent weeks and is now also saying that the US is considering leaving NATO. That would basically give Russia (Ukraine) and China (Taiwan) a free pass to continue their chosen path. Below are the facts for aid to Ukraine. The US has contributed zero and nothing since 2025, which is of course a gift to the rogue state Russia.

Source: Ukraine Support Tracker

Source: Bramhall’25NYDN

Have you seen Iran War – The Movie? Länk.

Below are the two latest issues of The Economist.

PORTFOLIO COMPANIES

A general note on our investments

The fund had a challenging month, primarily due to its sector allocation. Several sectors in Europe that performed poorly during the period—such as consumer-related companies, real estate, construction related businesses, and manufacturing—are areas where the fund has been relatively overweight. These sectors also tend to be more cyclical, meaning they often react more quickly and more sharply to changes in economic conditions, such as interest rates, economic outlook, and consumer confidence.

On the opposite side, we note sectors that performed significantly better during the month: energy companies, oil producers, chemical companies, and telecom operators. The fund has had only minimal exposure to these areas, which means it did not benefit from the strong performance of these more defensive or commodity driven sectors.

Source: Bloomberg

During March, several of our holdings released financial statements that were in line with expectations or better, but with cautious guidance for 2026, which contributed negatively to the fund's performance. Read more about this in the company comments below. However, we attribute most of the declines in the individual names to the fact that they are part of sectors that have been trading weakly because of the outbreak of war in Iran. If we are able to end the war in the near future, the shares should recover.

In terms of sales, our portfolio companies have a low exposure to the Middle East. However, our companies - like all others - are affected by concerns about weaker demand and higher production costs that may result from persistently higher energy prices. Whether these concerns will be realized in the long term is very difficult to predict at the time of writing. As mentioned earlier, we have reduced our exposure to certain cyclical names and increased in names where we believe the declines are excessive. We have also initiated three new positions that we hope to return to later. All of these positions contributed positively on an absolute and relative basis during the month.

De’Longhi

The coffee machine company released its full figures for 2025 in March, showing an operating profit (EBITDA) that was a couple of percent higher than estimates. However, the guidance for 2026 was interpreted as cautious. The uncertainty following the Iran war and its possible consequences on production costs and consumer demand probably means that De’Longhi’s management chooses an extra conservative stance in its comments for 2026. The company has a history of guiding cautiously at the beginning of the year and then beating estimates.

In addition to the cautious guidance, European consumer companies traded weakly in March, with a decline of about 14% (measured by the SXXP 600 consumer basket). De’Longhi shares lost 23% and are currently trading at about 32 euros per share. As of the end of December, net cash was about 5 euros per share. We estimate that the company’s golden egg, Professional Coffee, is worth at least 10 euros per share. Our estimates therefore value the remaining part, which mainly consists of coffee machines for consumers – a growing segment – at around 5-6x EBITDA. We think this appears low. At its worst in March, the company was valued, adjusted for its large cash position, at P/E 10x and 8.5x for 2026e and 2027e, respectively. We are reiterating to the company's management to make the values in the business visible, preferably through buybacks, extra dividends, a separate listing of Professional Coffee or a value-creating acquisition.

Volution

The ventilation company released another fine report that showed good organic growth in a difficult end market. Management also guided for a higher expected annual profit than the market had outlined. Despite the higher profit estimate, the share fell both on the report day and for the month (-20% in March). Ahead of the report, the share had performed well. We took the opportunity to sell ahead of the report and have since bought back shares. The share is now valued in line with its historical ten-year average, which we believe is unjustifiably low given management's strong delivery in recent years.

Rotork

The actuator company's operating profit for 2025 was better than the market expected. At the same time, the outlook was somewhat gloomier than expected. In the short term, Rotork is guiding for a weaker outlook in its energy segment, with good demand in other segments. In addition, the company has an exposure equivalent to 10% of sales to the Middle East, where sales are expected to decline until the war in Iran ends. After that, a lot of repair work should arise for Rotork in the region. Historically, the Rotork share has also correlated somewhat with the oil price - if we get a situation with persistently high oil prices, it should affect Rotork positively in the medium term. We reduced our position in the Rotork share ahead of the report and have since bought back some. For the month of March, the share lost –19%, which gives a decline of –4% for the full year.

Trigano

The RV company's sales report for the second quarter (broken fiscal year) was below expectations. Organic growth was around 5%, compared to our expectation of 9–10%. The deviation is explained by a delay in the supply chain, when a key supplier was hit by a fire, which shifted some deliveries from the second quarter to the third quarter. Adjusted for the delay, sales were in line with our expectations. The company's factories are operating at full capacity for the remainder of the year, which should contribute positively to profitability in the coming year, and likely compensate for the loss in the second quarter. Like De'Longhi, Trigano shares were affected by a general decline among consumer-related stocks in March and fell –16%. The company is now valued at EV/EBIT 5-6x, which can be compared to the ten-year average of around 8x. It is worth pointing out that the average profit growth over the past 10 years is 15% per year.

Asmodee

The board game and trading card company announced its first major acquisition as an independently listed company. The acquisition target, ATM Gaming, is a French board game company that has been strong for several years. In the coming financial year, it is expected to reach an operating margin (EBITDA) of approximately 50%. The purchase price consists of a mixture of cash and newly issued shares and includes additional purchase considerations. The financial structure is appealing, as it provides good incentives for ATM Gaming's management to maintain its commitment to the company in the coming years. If all additional purchase considerations are met, the acquisition multiple will be approximately 5x EV/EBITDA. Asmodee should also find synergies in special sales, as it can broaden its existing distribution of ATM Gaming games from Spain and Italy to other geographies.

Despite several quarters that far exceeded analysts' expectations, the Asmodee share has not been particularly well rewarded. The strong quarters have been mainly driven by Asmodee's partner channel and trading card games. The development we have seen here is not something the market dares to extrapolate (which we understand) and is the sales channel that carries the highest risk since Asmodee does not own its IP itself. However, it is a good source of cash flow generation that can finance further in the next step, and which over time should diversify Asmodee's business further.

Asmodee shares fell by 4% in March and have risen marginally for the full year.

Continental

Continental's share price performance in March was disappointing. Despite a low and attractive valuation and surprisingly stable earnings due to a high proportion of replacement tire sales, the share fell by 16% in March. At the beginning of the month, the company published its results for 2025, which were in line with the previously communicated preliminary figures. Management also gave new guidance for the full year 2026, which was in line with market expectations.

We suspect that the market's biggest concern right now is whether the announced sale of ContiTech will go through this year given the turbulence we are currently experiencing. Under current conditions, we believe there is a high probability that ContiTech will be sold in the coming months.

Late in March, an article was published on Bloomberg that named a number of different interested parties who had submitted indicative bids of around 3.5-4.0 billion euros. This is in line with our estimates and corresponds to 17.5-20.0 per Contitech share. A significant portion of the sales proceeds, which will hopefully be received during the third quarter, will be distributed to us, the owners. According to our way of looking at the valuation of Continental, you effectively get Contitech for free when you buy a share in Continental at today's levels (just over 60 euros per share).

On April 1, the company also held a “pre-close” call ahead of the first quarter, which signalled continued good activity. There is a tailwind this year from various falling raw material prices, but oil, which is an important input for tire manufacturing, is now going in the wrong direction. Historically, Continental has been adept at adjusting prices and managing rising raw material costs, and the company argues that they will succeed in doing so this time as well, albeit with a certain delay.

For the current year, Continental is trading at a very low 7x P/E 2026e, adjusted for an upcoming sale of ContiTech. By comparison, Michelin and Pirelli are valued at the equivalent of 10.5x and 12x. There is no fundamental reason for there to be any discount at all. Continental also has strong cash flow and a return on its capital well above its cost of capital.

So in summary, Continental is a large position in the fund because of 1) Approximately 50% potential to be valued in line with competitors 2) A dividend yielding approximately 4.5% in early May 3) At least 10 euros per share in extra dividend during the fall, which in that case gives a total dividend of approximately 20% this year.

SLP

SLP also had a weak performance in March. The real estate sector generally had a weak performance in Europe, with sharply rising interest rates due to inflation concerns driven by higher energy prices. However, SLP fell more than the sector without any clear explanation. Given the thin liquidity, we guess that it is outflows that have pressured the share.

During the month, SLP acquired properties for almost SEK 900 million and signed three new lease agreements. The share is now trading in line with the sector in terms of cash flow multiples, which appears remarkable given the value creation that the company has delivered in recent years. SLP was the only company on the Stockholm Stock Exchange that showed positive changes in value during the entire period 2022–2024, and we see nothing to indicate that this trend will be broken.

The newly signed lease agreements support our view of continued positive net leasing going forward. The share fell just over 11% during March and we increased our position at low levels.

SUMMARY

The fund's investment philosophy is based on fundamental analysis, "stock picking" with a concentrated portfolio and a certain layer of macro on it. When an extreme event occurred like February 28th, where absolutely no one knows what the new conditions are, of course the portfolio does not work as intended. That is why our performance has been weak in March and that is why the fund, with a palette of strong attractive companies, also developed very strongly on an absolute and relative level on March 31st and April 1st when there was talk of some kind of ceasefire.

What changes have we made during the turbulence? During the first week of the month, we were lucky that there was a large buyer in Kalmar and we were able to sell most of the position at good levels. It is a good company that we have owned for several years, but the share is less liquid and as of the end of February the increase this year was a full 20%. The second position we sold was Babcock, which rose by 148% last year and by another 15% in January. Despite a new war, defence-related shares began to develop weakly in March, and we had already started a divestment for valuation reasons. A third position that has been a strong contributor to the fund, we are in the process of selling and we will return to it.

In March, we initiated three smaller positions in new companies that we hope to return to in future monthly newsletters. In addition, we took the opportunity to buy more shares at very depressed levels in De’Longhi, Rational, Trigano, Hill & Smith, Volution, SLP, Rotork and Invisio. To illustrate the volatility at the share level, it can be mentioned that Invisio, without news one day at the end of the month, fell by a full 10% (at most, the share had fallen by 26% intramonth). Three days later, on April 1, the share was trading 16% higher. One never ceases to be surprised by short-term movements in the small-cap asset class.

The decline at the broad index level, however, has been relatively limited.

Source: Kepler Cheuvreux

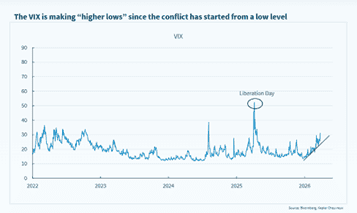

With each passing day, the damage and consequences for the world's energy market increase, which is visible in a gradually rising VIX index.

Source: Bloomberg, Kepler Cheuvreux

Historically, sharp increases in oil prices due to geopolitical shocks have only had a temporary impact on global stock prices. One thing to keep in mind this time is that the world has never been as indebted as it is now, and the possibilities for countries to support their consumers and industries are much more limited than before.

Source: Datastream, Goldman Sachs Global Investment Research

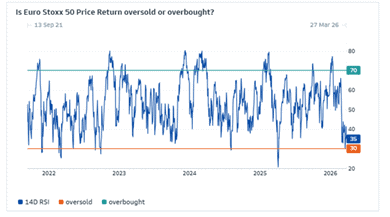

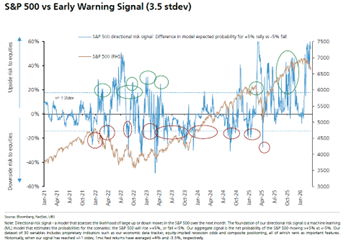

By traditional standards, the stock markets are in an oversold position, see Euro Stoxxx 50 below.

Source: Goldman Sachs

UBS shows the same thing below as their models, by traditional standards, flash green for a significant rebound. However, the uncertainty here and now is monumental.

Source: UBS

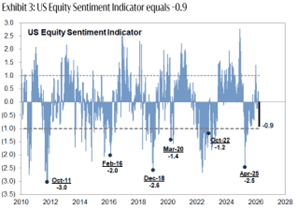

Sentiment among American investors is negative, but far from any record levels.

Source: Goldman Sachs

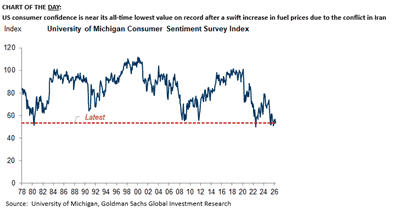

The American consumer, on the other hand, is at a record low, measured over nearly 50 years, see below. This is in stark contrast to the messages from the American administration. But it is also a strong contributing factor to Trump being elected – general dissatisfaction.

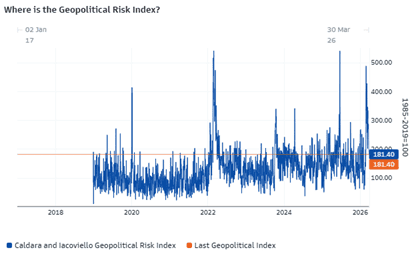

The Goldman Sachs geopolitical risk index was at about the same level as at the outbreak of war in 2022.

Source: Goldman Sachs

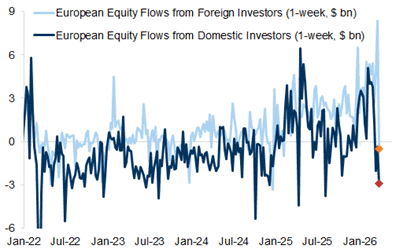

After a year of good inflows to European stock markets, it turned into large outflows in March.

Source: Goldman Sachs

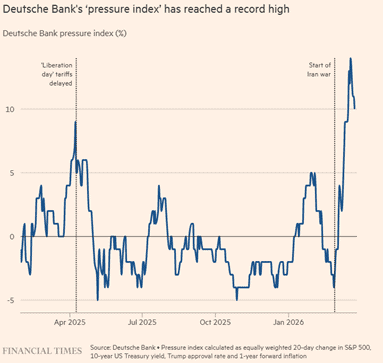

In recent weeks, the financial industry has spent a lot of time and energy trying to interpret the message of “the great leader” and when his next TACO move will come. Deutsche Bank has developed a “Pressure Index” that is intended to be a proxy and guide to when that might happen. The factors are: the population’s rating of Trump in general, inflation, the development of the S&P 500 and interest rates. The higher the level of the index, the greater the likelihood of a TACO. The index is now flashing red as all four factors are currently going completely in the wrong direction.

Source: Financial Times, Deutsche Bank

The image below shows how profit expectations in Europe have developed during the first quarter of the year for different sectors. Energy, banking and technology are at the top, while the chemical and automotive industries are at the bottom.

Source: UBS

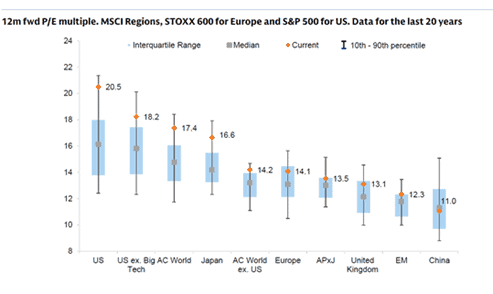

Valuations on the world's various stock markets have fallen in recent weeks but are generally still above the historical average.

Source: Goldman Sachs

The sharp decline has meant that, regardless of how the market develops in the coming weeks, CTA funds that sold shares worth USD 250 billion in March are expected to buy some back, see table below.

Source: Goldman Sachs

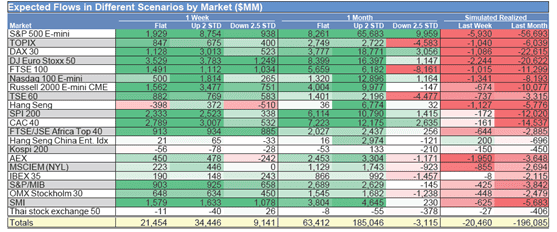

Below is UBS's latest estimate of the development of the broad European index under different scenarios (Stoxx600 closed at 583 on March 31).

Source: UBS

In summary, uncertainty is at an extremely high level, and the market is completely driven by headlines about developments in Iran. Trying to predict when and how a ceasefire will occur with rational thinking is impossible. One can try to “push a beach ball under the water” for a moment, but the harder you push, the more forcefully it pops back up to the surface, thus the recoil will be forceful if a solution comes soon. On the other hand, and diplomatically put, with an American administration whose policy development does not always show complete consistency, a delayed solution will have an exponentially negative impact on the world economy, including the American one.

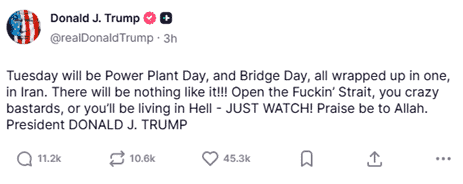

On Sunday, April 5th, Trump sent out this message that gives the impression of a person who is unbalanced. Are we watching a cognitive retardation on live broadcasts? There are now voices being raised in several quarters that the 25th Amendment must be used. An amendment to the Constitution that can be used if the president is deemed unable to perform his work and duties, but it will likely be difficult to get through.

Source: The Truth Social

The coming days and weeks will continue to be completely governed by developments in Iran. If Trump actually does what he writes above, which in that case is most likely a war crime, it will not be pleasant. The energy market will, despite persistent attempts by the US administration to portray it as something temporary, be affected both strongly and permanently. Many different industries will be affected, including the semiconductor industry. Will Trump be remembered as the person who personally crashed the AI race?

We stick to our strategy, follow developments closely and look forward to a time when our analytical capacity comes into its own and has a greater impact on the fund's development, instead of being completely governed by the macro as it is today.

Also keep an eye on the elections in Hungary on April 12th, where Viktor Orbán could be fired after 16 years in power. Vice President JD Vance will visit Hungary on April 7-8, and the timing and political context make it difficult to consider the visit as purely diplomatic and value neutral. One can, with some caution, state that the election in Hungary affects the future of the EU.

Thank you for your interest and we wish you a pleasant first month of spring.

Mikael & Team

Malmö, April 9th, 2026

IMPORTANT INFORMATION. This is a marketing communication. Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested. Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.