This material is marketing communication.

Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class’ return. The information below regarding returns therefore differs from the returns in other share classes.

Before making any final investment decisions, please read the prospectus, its Annual Report, and the KID of the relevant Sub-Fund here.

APRIL PERFORMANCE

The fund’s value increased by 7.6% in April (share class I SEK), while the benchmark increased by 4.6%. Since the change of the fund’s strategy at the beginning of September 2023, the fund’s value has increased by 28.6% compared to an increase of the benchmark by 31.0%.

Source: Coeli European

* Adjusted for spin-off of Rejuveron

** Includes September 1 (strategy change to long-only implemented September 4 2023)

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

EQUITY MARKETS / MACRO ENVIRONMENT

The bounce back from March lows was strong, and the first half of April showed gains of unprecedented strength. When the proclaimed negotiations between the US and Iran then failed to take place, an unusually long period of decline began. On the last trading day of the month, after eight consecutive negative days, the market turned around. The last time the Stockholm Stock Exchange fell for nine days in a row was in 2011, so if anyone hasn't noticed, we are living in unusual times.

The fund delivered a strong return in April, rising by 7.6%, compared to 4.6% for its benchmark. The broad European index rose by 3.7%, the S&P 500 by 7.5% and the Nasdaq, which had its best month since April 2020, rose by a whopping 12.5% – all figures measured in SEK.

The drivers for the fund's return were broad and overall, we benefitted from continued strong reports from our companies. The fund's three strongest contributors in April were Finland's Hiab, Britain's Hill & Smith and Austria's Bawag. More on this later in the letter.

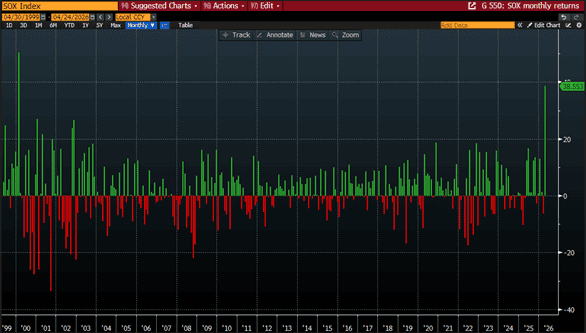

The best performers in April were companies with exposure to chip manufacturing. The US SOX index, with an RSI of 50% above its 200-day moving average and rising for 18 consecutive days, had its strongest month since February 2000…

Source: Bloomberg

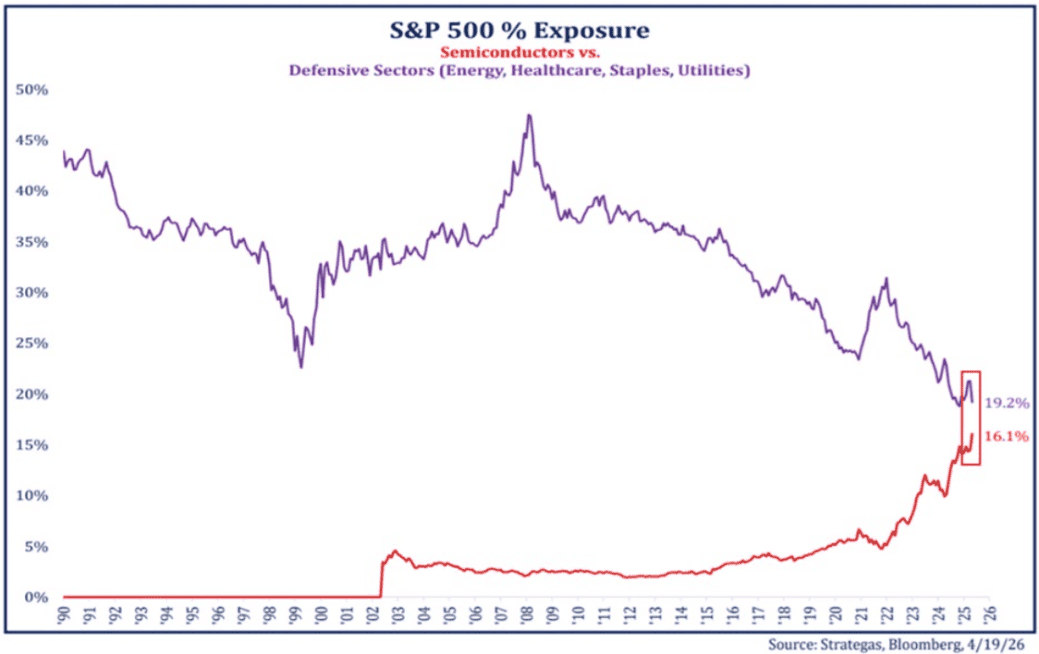

Below is a fascinating picture that illustrates the weight of the chip sector relative to defensive sectors since 1990. The development has been almost parabolic in recent years, and the chip sector now weighs almost as heavily as the total weight of the defensive sectors.

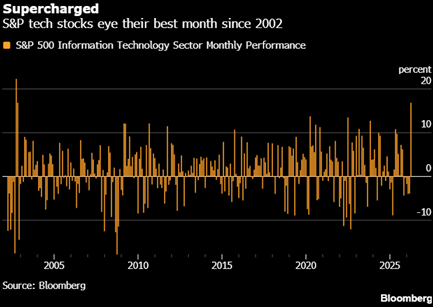

The technology sector within the S&P 500 had its strongest month since 2002.

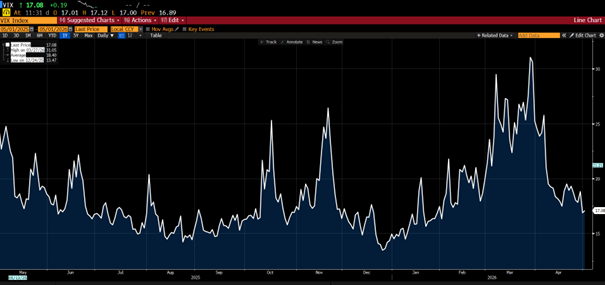

The stock market in April continued to move in line with the headlines from the US administration – one more staggering than the other. Compared to the drama of March, however, the movements and volatility were significantly lower. The market (and Iran’s leadership) now seems to view the threats differently, as clearly illustrated by the VIX index below. Given all the uncertainty in the world, one may be surprised by the level of the index below.

Source: Bloomberg

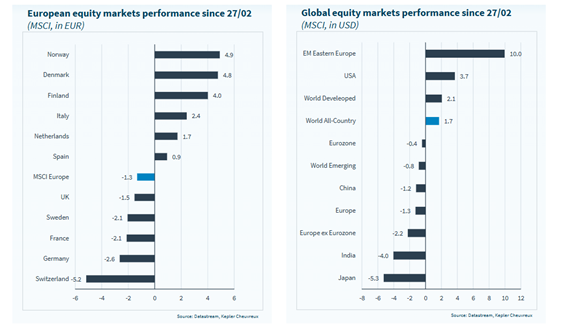

Since the outbreak of war on February 28th, Norway, unsurprisingly thanks to its energy stocks, has developed the strongest, while Eastern Europe is leading the global development.

The effect of the blockade of the Strait of Hormuz is clearly visible in the world's oil reserves. This is illustrated in the image below on the left, while the image on the right shows the year's oil flow through the strait.

Source: Goldman Sachs

A bit humour when Iranian state television posted the following on X where Mr. Bean is transformed into JD Vance. “None of the Iranian delegation has arrived or even flown to Islamabad for negotiations with the US at the moment”.

Source: X

The strong rally in April surprised many investors, and the pain trade took hold. Many were sitting on high cash levels after risk reduction in March, and the rally accelerated amidst thin liquidity. Hopes of a ceasefire and an opening of the Strait of Hormuz were the defining catalysts. Micro beat macro again – strong reports and rising profit expectations further contributed to the rally.

Source: NickAnderson@3-31-26, X

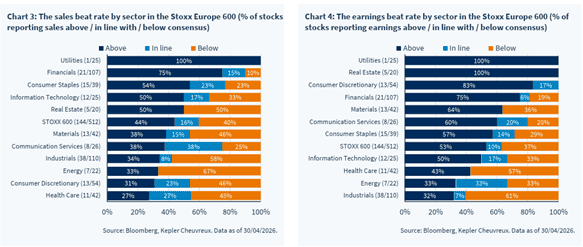

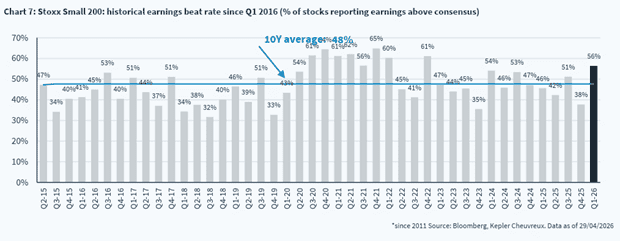

The image below shows which sectors in the broad European index have surprised positively with sales growth during the first quarter and, on the right, the corresponding figures for earnings.

European small caps had an unusually strong first quarter, see image below. The index for European SMID companies performed one percentage point better in April than the STOXX Europe 600. For the first four months of the year, the excess return over the STOXX Europe 600 amounts to two percentage points – a strong start to the year.

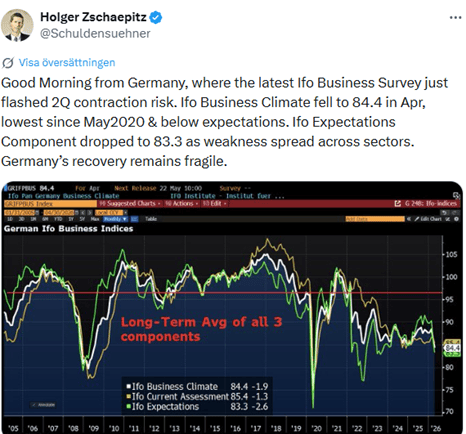

Europe's so-called engine is stalling precariously – despite promises of gigantic stimulus packages that still don't seem to have left the drawing board. How much longer? As true friends of Germany, we say: shift into a higher gear. Preferably two.

Source: HolgerZschaepitz, Bloomberg

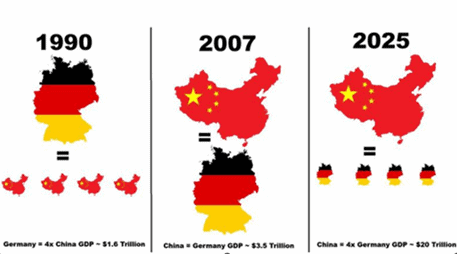

Developments are, as we know, rapid. In 1990, Germany's GDP exceeded China's by about a factor of four. Today, the roles are more or less reversed. The growth rate is explicit.

Source: X

It was with palpable relief – and in many cases pure joy – that the majority of Europe received the news that Viktor Orbán had finally lost power after years of authoritarian development. Péter Magyar’s landslide victory was not just an election victory, but a long-awaited crossroads. The celebration was not long in coming when Politician Zsolt Hegedüs broke out into spontaneous dancing in front of cheering crowds. https://www.youtube.com/watch?v=la75WSR6i1I

The criticism became too much even for the great leader and after a few hours the below post was removed. Trump explained it by saying that he thought he was being portrayed as a doctor. The Pope also criticized the post, which in turn received a lecture from Vice President JD Vance. Secretary of War, Hegseth, quoted the Bible text Ezekiel 25:17 – he thought. Instead, it was a quote from Pulp Fiction where Samuel L. Jackson's wonderful character Jules had his own homemade Bible quotes. It is impossible to come up with a fictional script like the one above. https://www.instagram.com/reel/DXM6w_3yn6L/

Source: Truth Social

Here is to lighten up the mood a bit before we delve into our companies: https://x.com/irmilitarymedia/status/2045855084848840831?s=43&t=l0N4mo6ka3H_LQq-7oz1LA

PORTFOLIO COMPANIES

Plejd

Since last year, the fund has had a minor position in the lighting company Plejd. The company is a favourite stock among many retail investors and has many years of strong operational development behind it. In terms of 12 rolling months, sales have now exceeded one billion kronor, which can be compared to sales that were essentially non-existent ten years ago. The strong development has also been reflected in the share price, which at the time of writing stands at 1,043 kronor, compared to just over 9 kronor at around this time in 2016.

Plejd's products are based on bluetooth technology that simplifies the installation process for electricians. The company is particularly keen on the relationship with electricians. We believe that customer support is excellent. Among Plejd's first products, which are now several years old, the prices have not yet been increased. Plejd's focus is therefore to keep electricians satisfied so that they can then buy Plejd's products from wholesalers such as Ahlsell or Solar. Plejd's products also provide some extra functionality for the end-customer, such as remote control of the lighting via an app, but this is not the main attraction for electricians.

CEO Babak is a co-founder and has taken the company to where it is today. He has a couple of well-known and, in our opinion, talented owners on the equity owners list alongside him. The business model has been built methodically. Over time, the company has gradually expanded into new product categories and has subsequently launched more products within each category. In addition to this, the company has progressively entered new regions. Today, in addition to Sweden, it is big in Norway. Next in line is the Netherlands, where the market has been cultivated for some time and not least the large local wholesalers who need to agree to take on Plejd's range for sales to really take off.

Our thesis for the share ahead of the year was very simple: After a very strong 2025 with just over 40% sales growth, many analysts (for good reason) lowered their percentage growth assumptions for 2026. However, the estimates available at the beginning of the year implied that growth in absolute terms would decline, which we saw as too conservative. The first quarter of 2026 offered 39% growth – certainly partly helped by wholesale inventory building – but even without this, our picture is clearly above expectations. Profitability followed suit and the reported operating profit was nearly 50% better (!) than expectations for the quarter.

The stock responded well to the Q1 report and had risen by 43% this year by the end of April. Although the valuation has risen in a short time, we believe there is more to be gained – the multiples will fall quickly if our estimates are correct. There is likely to be continued growth potential in the existing product portfolio, while the company is in the process of launching new products. In addition, there are further steps to be taken in the geographical expansion. Plejd is valued at approximately EV/EBIT 23x and 17x for 2027e and 2028e, according to our estimates.

Virbac

At the beginning of the year, we built a medium-sized position in the French animal health company Virbac, which develops and produces various forms of medicine for pets and farm animals. The family-owned company has long grown organically with high single-digit numbers. In recent years, however, the share price has moved sideways despite continuously rising profit revisions. The start of the year has been good, with organic sales growth exceeding expectations. We hope to return to this.

Beijer Ref

The Beijer Ref report delivered an operating profit that was in line with expectations, even though organic growth was a few percentage points lower than expected. Developments in the US were better than we had thought – a region that has been a cloud of worry in the market for a long time. At the same time, the European market was weaker than we had outlined beforehand. The reaction to the report was strong and the Beijer Ref share fell 6% on the report day and ended the month essentially unchanged towards the end of March after an initial strong rise in April. We took the opportunity to increase our position slightly at low levels.

Alm. Brand

The Danish insurance company managed to both raise its guidance for the full year and then issue a profit warning on the same day. The backdrop is that on the morning of April 28, Alm. Brand released its Q1 report for 2026, which was significantly better than expected (mainly due to one-off reasons such as lower weather-related cases than expected). At lunchtime on the same day, a decision was made by the Danish Supreme Court, which, in short, means that a 5% limit for the degree of lost earning capacity required to receive compensation, is sufficient. This is lower than the 15% limit previously applied by all insurance companies in Denmark that are active in the workers' compensation market.

Shortly after the court's decision was announced, Alm. Brand released a press release about an expected one-off cost equivalent to 700 million Danish kronor (approximately 3% of market cap) because of the new rules. This provision was lower than we had predicted. We note that Alm. Brand's provision is lower than the Danish insurance company Tryg, despite a slightly higher market share. There is probably some uncertainty in the assumptions required to make these provisions. Although there is still some uncertainty about the situation, we believe that Alm. Brand's valuation is now unjustifiably low in relation to other Nordic insurance companies, and we took the opportunity to increase our position. Alm. Brand is valued at around P/E 12x and 11x for 2027e and 2028e, respectively.

The share fell 6% in April.

Konecrances

After last year's strong price increase and revaluation, we had significantly reduced our Konecranes position ahead of the Q1 report. This turned out to be the right move as the report was disappointing on all fronts; order intake 2% off, forecasted sales and operating profit respectively 10% and 14% worse than expected. At the same time, most of the deviation seems to be due to a certain shift in order deliveries, which can fluctuate a lot on a quarterly basis. The fact that the order book and inventory rose by 6% and 11% respectively compared to Q4 2025 speaks for itself. We took the opportunity to buy back many of the shares we had previously sold at higher levels. The share is valued at around EV/EBIT 10x for 2027e and 2028e. Konecranes shares ended the month unchanged.

Bonesupport

Bonesupport delivered a report that was broadly in line with expectations. Sales came in slightly lower than expected, mainly due to currency headwinds. However, the most important value driver, Cerament G in the US, exceeded expectations and growth accelerated in the first quarter, possibly at the expense of weaker sales of Cerament BVF in the US, which is a trade-off we are happy to accept.

If the company can maintain this quarterly development for Cerament G, the full-year financial target of 35% growth should be within reach. At the same time, we see potential for further acceleration during the year as more trauma centres start using the product. Unlike the treatment of bone infections, trauma requires a longer follow-up period, around 12 months. During the previous year, the number of trauma centres that have used the product at least once increased from 15 to 140. We estimate that some of these will be fully operational towards the end of the year, which in that case is likely to contribute to increased sequential growth.

The stock performed strongly ahead of the report but has since been weaker, despite around one million shares being repurchased by short sellers in recent weeks. The stock rose 13% in April.

SLP

SLP offered perhaps its best report ever, with a management profit that was just over 8% higher than expected. However, the share was rewarded more sparingly, with an increase of just over 3%.

The management continues to carry out value-creating acquisitions and property development. For this, it is only paying about 14 times the current earning capacity for the year. The property sector is far from popular right now and the sector has fallen almost 9% so far this year. SLP rose about 5% in April and has developed in line with the sector this year, which appears unjustified.

Hiab

Hiab has, together with Plejd, been the big shout outs of the reporting season so far. In recent months, we have gradually increased our exposure and entered the report with a significant position. The outcome confirmed our thesis: order intake improved both on an annual basis and sequentially and exceeded expectations by around 5%. The adjusted operating profit also came in stronger than expected.

We believe that the company is approaching a clear inflection point, where order intake is starting to accelerate again. At the same time, Hiab is entering a period with significantly simpler comparative figures, which suggests strong profit growth going forward. We also note that management is now talking more about the opportunities for value-creating acquisitions. There should be good potential for this with a net cash position approaching EUR 300 million.

In addition, the picture is strengthened by several positive signals from nearby companies. Several truck manufacturers have raised their forecasts, and the distribution chain in the US is reporting a clear improvement in demand after a stronger-than-expected quarter. Even its closest competitor Palfinger has expressed a very positive market view, with extensive infrastructure investments expected to benefit the sector in the coming years.

Despite this, the share has only risen about 10% in two years and is trading at around 10 times next year's operating profit - a level that appears low for a company of Hiab's quality. The share did rise about 25% in April, but we still see significant upside over a 1–2 year horizon.

Bawag

One of the fund's largest positions is in the Austrian bank Bawag. It is an exceptionally well-run bank with a management team that has proven adept at controlling costs, executing value-adding acquisitions and driving profitability. The cost/income ratio is a record low of 33%, contributing to a return on capital employed of a whopping 28%.

In mid-April, Bawag confirmed a bid for the Irish bank PTSB Group, equivalent to approximately EUR 1.6 billion (Bawag's market capitalization is approximately EUR 11 billion). With one of the strongest balance sheets in the sector, the acquisition is financed entirely with its own surplus capital, which has been rapidly built up despite generous dividends and buybacks. The acquisition is expected to contribute over 20%to earnings per share, compared to buybacks that yield just under half that.

After a recently announced dividend of 4.5%, the stock is trading at approximately P/E 12x, 9x, and 8x for the years 2026–2028, respectively. The stock rose, including the dividend, by 16% in April and is up 21% so far this year.

SUMMARY

We are pleased with the development in April, where a combination of strong contributions from our companies and few mistakes in our analysis and positioning resulted in a strong return.

In addition, it can be noted that April 8 was probably the strongest day, both relatively and absolutely, since the strategy was changed almost three years ago. The excess return on that day amounted to a whopping 2.4 percentage points.

With a US administration that is difficult to predict, and with economic and political tensions everywhere you turn, one needs to be particularly humble and flexible in thought.

Our work as stock pickers is about allocating capital in this volatile environment to companies that have good prospects of, over time, benefiting from the prevailing environment and strengthening further. These are companies with strong pricing power, solid balance sheets and a management that works in the interests of shareholders to create value – and, this is absolutely crucial for excess return, where the price we pay is significantly lower than what we think it is worth.

What we do not do is try to predict the market's short-term movements to adjust exposure and thereby capture extra beta in the performance.

That said, here is a selection of images that highlight the latest developments in various ways.

Source: Goldman Sachs

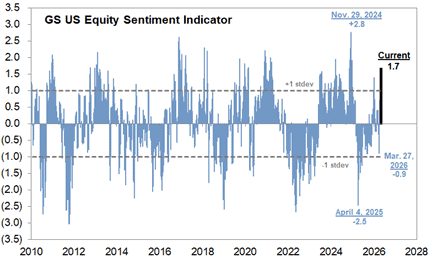

Our view of what has driven the recent risk appetite and thus the stock market is as follows:

- A belief that the US and Iran will reach an agreement and that the Strait of Hormuz will reopen.

- Rising profit estimates.

- The exceptionally rapid development in AI.

- FOMO – investors had far too much cash when the turnaround came.

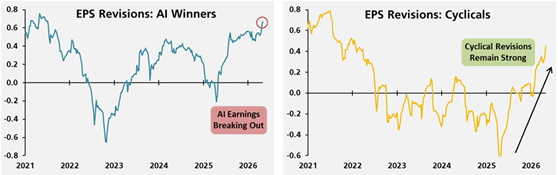

Below is the expected profit development for US AI and cyclical companies. For European companies, the development is similar, albeit on a smaller magnitude.

Source: UBS, Factset

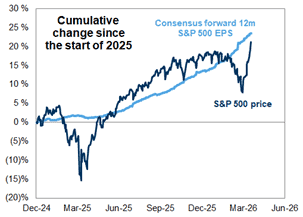

The cumulative earnings trend for the S&P 500.

Source: Goldman Sachs

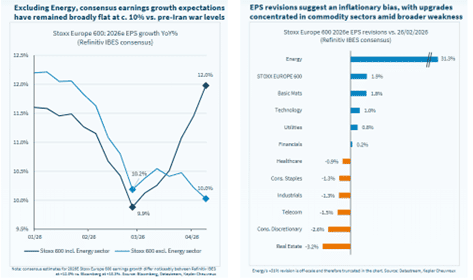

Earnings expectations in the broad European index, excluding energy, are largely unchanged so far this year. Real estate is the weakest sector, weighed down by rising interest rates.

Source: Kepler Cheuvreux

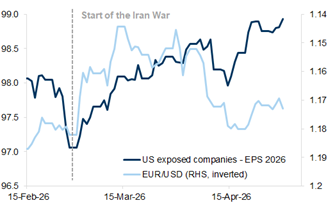

The weakened US dollar has contributed to upwardly revised profit expectations for European companies with large exposure to the US.

Source: Goldman Sachs

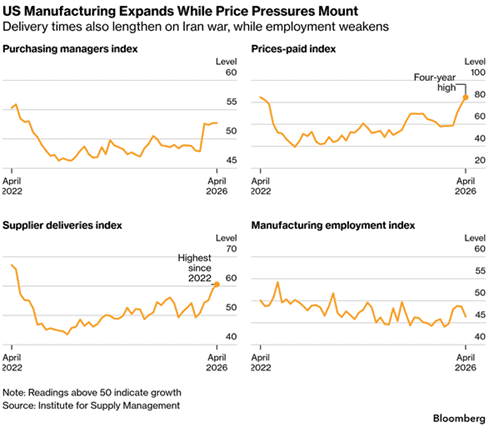

Prices are rising in the US at the same time as delivery times are increasing. This points to an economy that is continuing to grow, but also to tariffs gradually starting to have an impact on the economy.

German consumers are starting to lose hope, again.

Source: X, Bloomberg

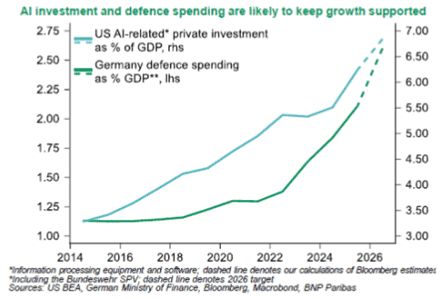

AI investments in the US and European defense investments are a strong driver of economic growth.

But the economic surprise index is losing momentum in the US, Europe and the emerging markets segment.

Source: Bloomberg, Kepler Cheuvreux

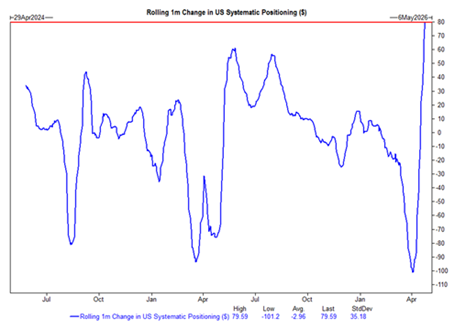

As we mentioned in last month's newsletter, large CTAs had thrown out stocks in March and, according to Goldman Sachs' forecasts, they would buy some back in April, regardless of market conditions. This resulted in an unusually strong inflow into the market ($80 billion) and contributed to the April rally.

Source: Goldman Sachs

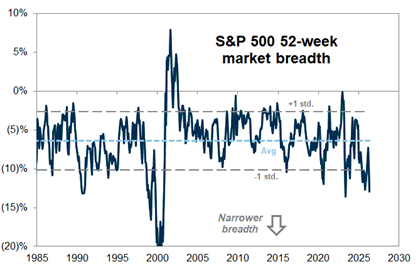

The upturn in the US has been narrow, meaning that a few companies have driven the performance. A strong upturn combined with high concentration has historically increased the risk of a market rebound.

Source: Goldman Sachs

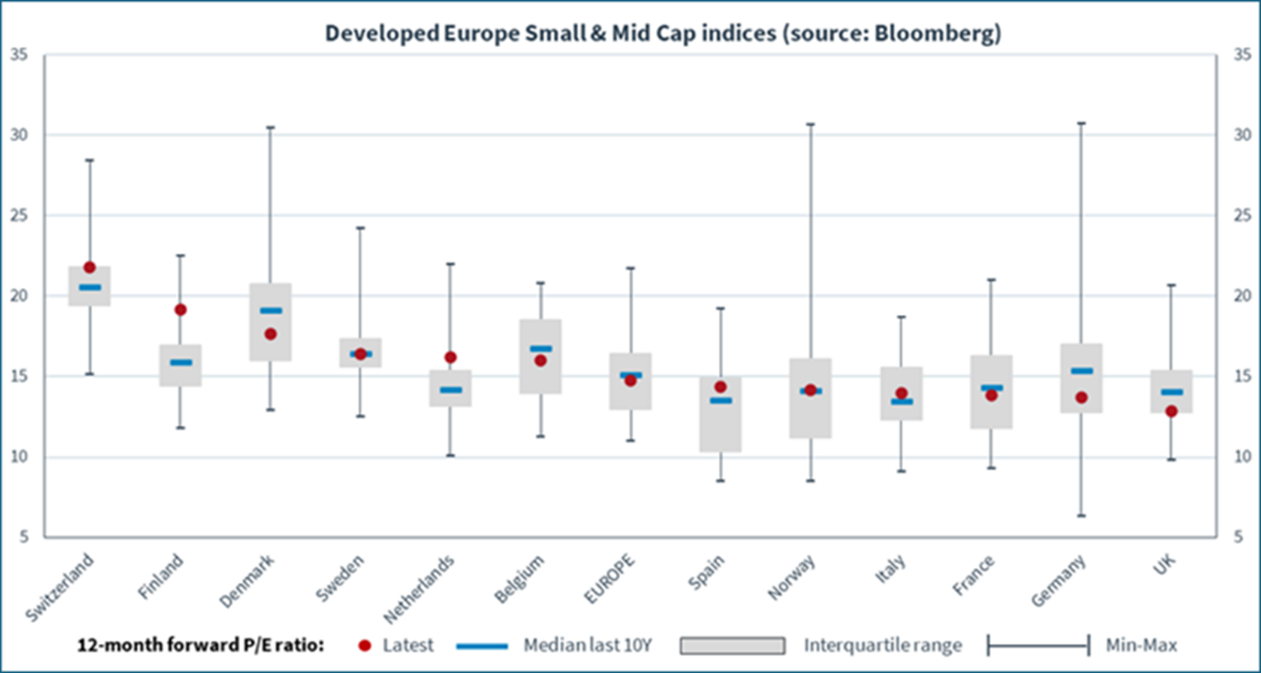

Unlike the US stock market, valuation levels for European small caps are fully in line with their 10-year average. However, at country level there are clear differences; Germany and the UK are trading well below their historical averages, while Switzerland is above.

Source: Kepler Cheuvreux

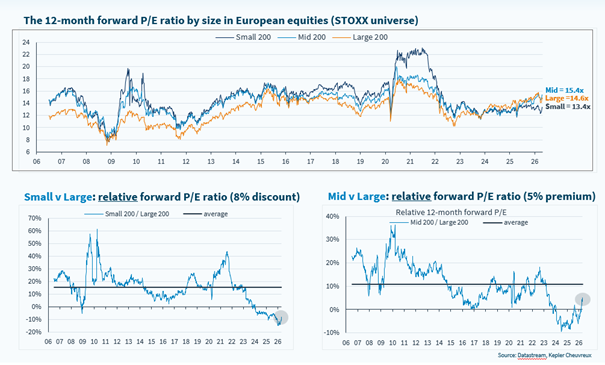

The historically high discount for European SMID companies compared to large companies has started to decrease but is still above its historical average.

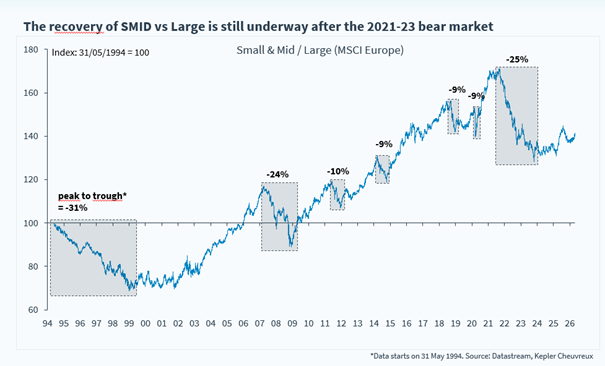

The recovery has begun.

Overall, developments in the world's financial markets continue to be dominated by the conflict in the Middle East, and above all, about the fact that the Strait of Hormuz is effectively closed. For every week that it remains closed, economic development is increasingly affected, as it takes longer and longer to restart systems and processes.

It is difficult to assess, with any great precision, when the conflict may end. At the same time, the mid-term elections are approaching, and it is reasonable to assume that Trump is increasingly influenced by growing domestic political pressure. At the time of writing, the price of petrol in the US is around USD 4.30 per gallon (USD 3 before the war). In California, the price is closer to USD 6, which is on par with Swedish levels. This is probably not sustainable over time from a political perspective.

We continue to spend our time analyzing new companies and monitoring existing positions. The reporting season has started strongly and resulted in several clear and strong price reactions, with Plejd and Hiab standing out with increases of 35 and 25% respectively in April.

Thank you for your interest and we wish you a pleasant first month of spring.

Mikael & Team

Malmö, May 6th, 2026

IMPORTANT INFORMATION. This is a marketing communication. Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested. Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.