This material is marketing communication.

Note that the information below describes the share class (I USD), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class return. The information below regarding returns therefore differs from the returns in other share classes.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

1) Share Class IUS, other share classes after the fund manager commentary.

FUND MANAGER COMMENTARY

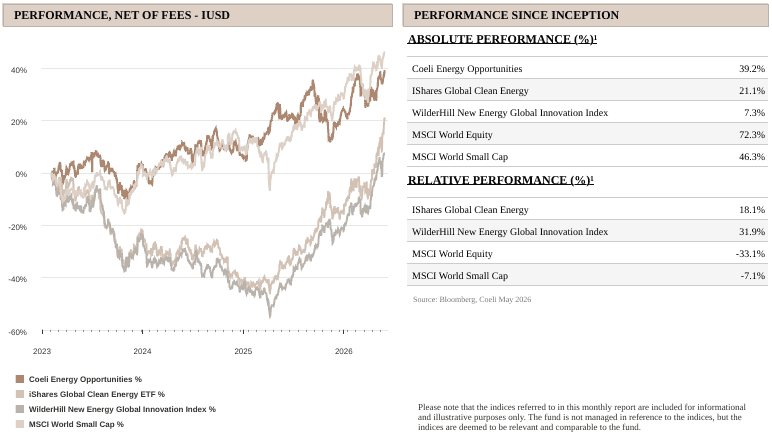

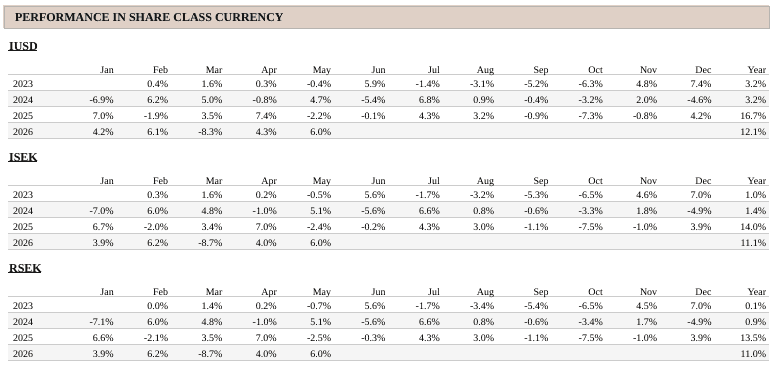

The Coeli Energy Opportunities fund gained 6.0% net of fees and expenses in May (I USD share class). Year-to-date, the fund is up 12.1% and has returned 39.2% since inception in February 2023.

In May, the fund underperformed its most comparable indices, the Wilderhill New Energy Global Index (NEX) and the iShares Global Clean Energy (ICLN) by 1.5% and 7.5%, respectively. Year to date, the fund has lagged NEX by 26% and ICLN by 31%, while since inception it remains ahead by 32% and 17%, respectively.

May largely extended the broad market trends seen in April, with conflicting headlines around the Iran war and the reopening of the Strait of Hormuz overshadowed by optimism around AI investment and a very strong earnings season. While we remain positive on the long‑term productivity gains from AI, equity markets are starting to feel somewhat bubbly. We elaborate on this in the thematic section below, “It is starting to feel bubbly”.

As in April, most of the fund’s positive contribution came from AI‑related themes, particularly “Diversified Energy”, which contributed 5.4% to NAV. The lion’s share was driven by Micron (MU), with additional gains from a couple of former bitcoin miners. “Solar” added 1.5% to NAV, as gains in Nextpower (NXT) and First Solar (FSLR) more than offset losses on short positions in inverter companies attempting to reinvent themselves as AI data‑centre providers and attracting risk‑hungry retail investors.

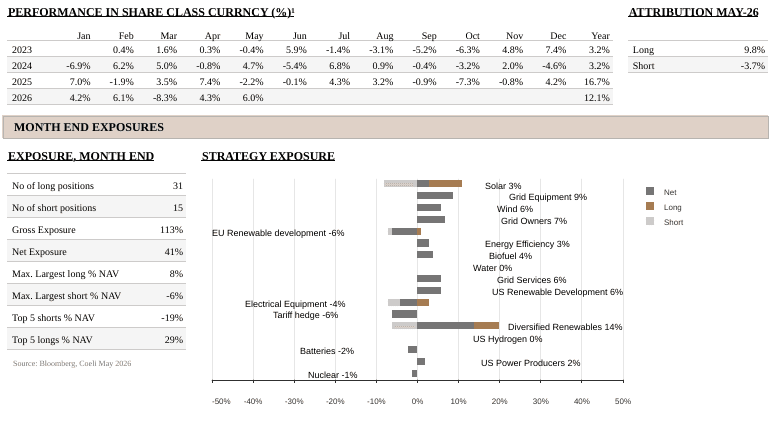

Overall, long positions contributed 9.8% in May, while shorts detracted 3.7%, as we continued to reduce exposure to “concept” stocks with large retail followings. At month‑end, net and gross exposure stood at 40% and 114%, respectively. We discuss the rationale for the large reduction in gross exposure in more detail in the thematic section below.

MARKET COMMENT – STRONG EARNINGS SUPPORT THE RALLY

The S&P 500 rose 5.1% in May, setting 11 new all‑time highs. The unrelenting rally was again led by large technology stocks, with the Nasdaq 100 up 10.5%. The S&P 500 Equal Weight Index and the Russell 2000 small‑cap index gained 2.5% and 4.3%, respectively, reflecting a strong first‑quarter earnings season and upgrades to full‑year earnings estimates. Even the Euro Stoxx 600 rose 1.9% in May, despite signs of a deteriorating macro backdrop in Europe from higher energy costs.

As we discussed in last month’s report, we are in the midst of a once‑in‑a‑generation capex cycle that is effectively supporting the US macro picture and driving robust earnings growth. Despite higher energy prices from the Iran war pushing up inflation, US GDP growth estimates are now 20–30% higher than at the beginning of the year. Similarly, S&P 500 full‑year aggregate earnings are expected to grow by around 25% this year, roughly twice the pace expected at the start of the year. On that basis, one could argue that the market is not meaningfully more stretched than it was at the start of the year. However, given that most of the earnings uplift comes from a relatively small group of companies in the TMT sector, we believe the clouds on the horizon we wrote about last month are only getting denser.

IT IS STARTING TO FEEL BUBBLY

There are moments in markets when the tone shifts from scepticism to optimism and then on to exuberance. Investors stop asking what can go wrong and start asking how far it can go. We are not necessarily at the end of that process, but we are clearly well into the optimism phase.

The AI trade is the dominant force in global equity markets. Concerns around oil prices, inflation, higher interest rates, larger government deficits and geopolitics have only increased in recent months, but for now they are overshadowed by the AI investment boom. The market has chosen to focus on growth over risk, optimism over doubt and the future over the present.

There are plenty of signs that sentiment has become stretched. AI-related stocks have seen extraordinary moves over very short periods. ARM, the chip designer, and DELL, the computer manufacturer, both rose around 100% in less than ten trading days in May. Intel (INTC) has almost tripled in the last two months, while Sanddisk (SNDK) is up more than 600% year to date. Marvell Technology (MVRL), a semiconductor company, is up more than 250% year to date and added 32% in a single day after Nvidia’s CEO Jensen Huang suggested it could soon join the “trillion-dollar club”. In normal markets, moves like these would look almost absurd.

The point is not that every move is irrational. We have partly benefited from these same dynamics in some of our long positions, but in all the cases we can comfortably justify the fundamental rational. We bought Micron (MU) in September last year, and the stock is now up roughly 700% in about eight months. We also owned Bloom Energy (BE) from around USD 18-20 per share to USD 165-170, a move that took place in less than a year. Since then, Bloom has risen further to around USD 300 per share, equivalent to roughly 1,200% since the start of 2025.

These were not random moves in random companies. Micron has benefited from being one of three key suppliers of DRAM and HBM memory, crucial for further data centre build out. The incremental buyer of memory chips is no longer price-sensitive PC manufacturers, but rather price insensitive hyperscalers. We believe the current memory cycle will last longer than any memory cycle in the past.

Bloom has won some massive contracts and so far, executed well. It sits at the centre of the “behind-the-meter” power debate, where speed of deployment, grid constraints and the need for reliable on-site power have become increasingly important. These are exactly the kinds of bottlenecks we have written about for a long time, for instance in October 2025 – “Bring Your Own Power – How the Data Center is Rewiring the Grid”.

However, there is a difference between a fundamentally attractive set-up and a valuation that leaves no room for disappointment. We still own Micron, although recently trimmed the position, as the stock has rerated from about 4x to 10x 2027 P/E despite extraordinary earnings upgrades. We sold Bloom as the valuation became increasingly difficult to justify, and it has only become more demanding since. That does not mean the underlying thesis is wrong. It simply means that price eventually matters, even when the underlying opportunity is very strong.

There is no doubt that AI demand is real. Hyperscaler capex is real. The need for compute, memory, networking, power, cooling and grid infrastructure is real. However, bubbles rarely form around things that are completely fake. They usually form around something important, where the underlying thesis is right, but where expectations, positioning and price action eventually run ahead of what can reasonably be delivered.

That is the environment we are increasingly trying to navigate. It is not that some companies simply look fundamentally expensive, that is almost always true somewhere. The more important issue is that price action is disconnecting from fundamentals and is becoming increasingly dominated by momentum, retail activity, options flows and the fear of missing out.

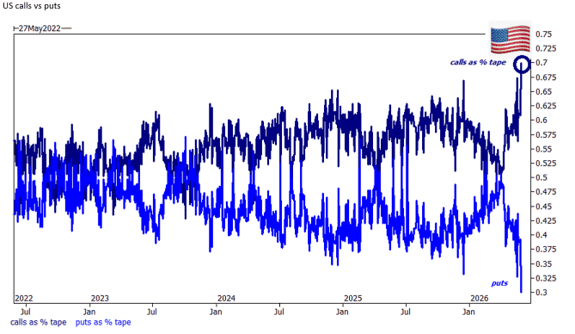

When everyone wants calls, risk management matters

Source: Goldman Sachs

This chart on US calls versus puts captures the mood quite well. Call activity has risen sharply as a share of total option activity, while put demand has collapsed. In plain English, investors are increasingly positioned for upside, not protection.

This matters. In normal markets, overvaluation is a reason to be short. However, in markets like this, overvaluation can become a reason why a stock goes up even more, because the higher it goes, the more attention it attracts from retail flows and momentum-oriented capital. “Pigs really can fly” for a while in this type of environment. Over the recent quarters, we have suffered from this dynamic in some short positions that we would argue have no, or only tangential, exposure to AI data centres or power. While we remain confident in our fundamental analysis and valuation work, the positions became impossible to hold as they caught the eye of retail investors hunting momentum stocks.

The current market environment is simply treacherous and that is why we reduced gross exposure during the month, on both the long and the short side. This is not a signal that we are less convinced about our long-term themes, nor that we no longer see attractive shorts. It is rather a recognition that the volatility of outcomes has increased and that near-term risk-reward has deteriorated. Put differently, when upside volatility becomes this extreme, the risk of being fundamentally right but tactically too early rises materially.

Importantly, we have not stepped away from the market. We remain invested in the areas where we believe the structural opportunity is strongest. What we have done is to reduce some of the most volatile positions on both sides of the book. On the long side, that means trimming names where expectations and price action had moved very quickly. On the short side, it means reducing exposure to companies where the fundamental case may still be valid, but where the near-term risk of retail-driven upside volatility had become too high.

We believe this gives us a better risk profile. It reduces the probability that short-term volatility dominates the portfolio, while still leaving us with meaningful exposure to the themes we believe in. It also provides us with more flexibility to be aggressive when this dynamic eventually fades. Retail-driven momentum, call buying and speculative positioning can dominate for periods, but they do not repeal gravity. Eventually, companies still need to deliver earnings, returns on capital and cash flow that justify their valuations. The challenge is timing since being “right” too early in a market like this can be very expensive, and in practice, indistinguishable from being wrong.

FUND PERFORMANCE - POWERING AI DOMINATING PERFORMANCE

May was a solid month for the fund, although only half of the themes made a positive contribution. While returns were again driven by AI‑related themes, one noticeable difference from previous months was the bifurcation in performance among some of our favourite powering-AI names. While certain AI stocks continued to rally, many of the winners from recent months fell in May despite strong momentum in the overall theme. We were fortunate to have significantly reduced gross exposure as these stocks sold off.

As in April, the best‑performing theme was “Diversified Energy”, contributing 5.4% to NAV. The main contributor was Micron (MU), but former bitcoin miners Terawulf (WULF) and HUT 8 (HUT) also did well. However, the share price of our largest position at the beginning of the month, Siemens Energy (ENR), fell almost 10% during May as Mitsubishi Heavy Industries (MHI) announced a further 50% increase in gas turbine capacity by 2030. Fortunately, the negative contribution to NAV was limited as we reduced the position by about 30% before the sell‑off accelerated into month‑end. ENR is still up 36% year to date and has risen by around 1,300% since early 2024, equivalent to roughly 200% annualised. We still like ENR and, while we see the MHI capacity increase as marginal negative, we do not believe it is enough to tip the overall supply-demand balance at this stage. The valuation remains supported by a strong order backlog and earnings growth, and we expect to rebuild the position on further weakness.

Similarly, the share price of Mastec (MTZ), our second‑largest position at the beginning of the month, fell only 4% in May but ended the month almost 14% below its intra‑month peak on no significant news. As we cut the position by almost half close to the peak, its contribution to NAV and to the “Grid Services” theme was positive in May. MTZ is still up 74% this year and more than 400% since early 2024. We continue to like the company and will look to rebuild the position on further weakness.

The “Electrical Equipment” theme was the second‑best performer, contributing 1.7% to NAV. The theme used to be skewed heavily short as a hedge to the other grid‑related themes, but after the recent de‑grossing, exposure is now broadly neutral. The best performer on the long side was Forgent Power (FPS), a manufacturer of electrical distribution equipment. We like the stock because, unlike most competitors, it still has ample spare capacity to service strong demand from data centres. The share price has doubled since its listing only four months ago.

The third‑best performing theme was “Solar”, adding 1.5% to NAV in May. The two main contributors were Nextpower (NXT) and First Solar (FSLR). NXT gained 32% in May following yet another “beat and raise” quarterly result and, a week later, the announcement of its entry into the battery‑storage market. Although still early days, this confirms NXT’s ambition to be a one‑stop shop for developers.

FSLR rose as much as 52% in May after lagging the rest of the solar space at the beginning of the year. The stock has been held back by constant delays to the decision on Section 232 tariffs on polysilicon, which have been expected “next month” for more than six months. The Commerce Department filed its investigation at the end of March, which means that President Trump’s legal “drop‑dead” date falls 90 days later, at the end of this month. However, once bitten, twice shy: the President has many other priorities, and we would not be surprised to see further delays before a decision is made. We have reduced our position in FSLR after the strong rally.

The gains from NXT and FSLR were partly offset by short positions in solar-inverter companies that rallied after announcing plans to enter the market for solid-state transformer (SST) for data centres. In effect, the market has already priced in these companies as future market leaders in what is already a crowded field dominated by some of the world’s leading electrical- equipment manufacturers, including Delta Electronics (2308 TT), Hitachi Energy (6501 JT), Siemens Energy (ENR), GE Vernova (GEV), Schneider Electric (SU), ABB (ABBN), Eaton (ETN), and Mitsubish (MHI), to name a few. While the opportunity is clearly large and attractive, in more normal market environment an announcement about pilot projects and the prospect of revenues several years out would typical trigger curiosity and due diligence, not a doubling of the share price.

Despite de‑grossing the book in May and running with a lower‑than‑normal net exposure, we remain structurally long the power and infrastructure enablers of AI, energy security and energy transition. At the same time, while we have significantly reduced shorts in the most speculative names, we continue to hedge the portfolio through selective shorts in the weaker parts of the energy‑transition and AI ecosystem. Our focus remains on businesses with tangible assets, strong order books and clear pricing power, balanced by a smaller but active hedge book designed to protect the portfolio if the current AI euphoria eventually gives way to a more discriminating market for capital. In other words, we are staying true to our core themes, but with a sharper emphasis on risk management in an increasingly momentum‑driven market.

Thank you for your continued trust and confidence. We look forward to updating you again next month.

Sincerely

Vidar Kalvoy & Joel Etzler

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Over 15 years of investment experience spanning both public markets and private equity.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Spent six years at Horizon Asset in London, a market-neutral hedge fund.

- Started working with Vidar Kalvoy in 2012.

- Five years in Private Equity at Morgan Stanley.

- Began his investment career in the technology sector at Swedbank Robur in Stockholm in 2006.

- Holds an MSc in Engineering from the Royal Institute of Technology (KTH), Stockholm.

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Has managed energy equities since 2006 and brings more than 20 years of experience in portfolio management and equity research.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Head of Energy Investments at Horizon Asset in London for nine years, a market-neutral hedge fund.

- Experience from energy investments at MKM Longboat in London and equity research in the technology sector in Frankfurt and Oslo.

- Holds an MBA from IESE in Barcelona and a Master’s in Business and Economics from the Norwegian School of Economics (NHH).

- Before entering finance, he served as a lieutenant in the Royal Norwegian Navy.

IMPORTANT INFORMATION. This is a marketing communication.

Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.