This material is marketing communication.

Note that the information below describes the share class (I USD), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class return. The information below regarding returns therefore differs from the returns in other share classes.

![]()

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

1) Share Class I USD

FUND MANAGER COMMENTARY

The Coeli Renewable Opportunities fund launched on the 6 th of February and by the end of the month it had generated a profit of 0.4% net of fees and expenses. See performance and relative performance in the table above.

INTRODUCTION – NEW FUND LAUNCH

This is the first monthly report for our new fund, Coeli Renewables Opportunities. The fund will ride the great wave of investments into renewable energy and decarbonization over the next decades. We believe some new giants in energy and clean technology are on the rise. However, the aim is not only to pick the winners of the energy transition, but also to create alpha by shorting companies that will fail. When governments throw vast amounts of money at a problem a lot of competition is created. Our expectation is that companies that lack sustainable competitive advantages or those that are drawn to the sector only to capitalize on the generous subsidies will struggle to be profitable.

The launch has gone well although we have added risk at a slower phase than expected as we felt the market was extended after the strong rally in January. Please see our fund performance part for more details.

MARKET COMMENT – ECONOMY IS STRONGER THAN EXPECTED

Since the launch on Feb 6 th to the end of February, the S&P 500 and the Nasdaq fell about 4%. Although this partly reflects that both indices were up significantly in January, the key driver was the stronger than expected economic datapoints. The labour market is showing no sign of weakness, economic activity indicators are stronger than anticipated and inflation is not falling as fast as in the previous months.

The market rightly fears that the FED will have to raise rates further and keep them extended for longer to ensure that inflation expectations do not become unanchored. Moreover, as the economy seems to be handling higher interest rates much better than projected, it is not unlikely that the FED’s new neutral base rate is significantly higher than in the years prior to the pandemic. If so, this would indicate lower market valuation multiples going forward.

ENERGY SECURITY HAS TOP PRIORITY

Europe is facing a two-pronged energy challenge that will accelerate the shift toward renewable energy sources. First, the region's dependence on fossil fuels from politically unstable countries has unravelled the security of energy supplies. Second, the expected increased electrification of industries, homes and the rising number of electric vehicles imply a massive change in direction for the energy system. For instance, Sweden is consuming about 140TWh of electricity per year and has been at this level since the late 1980’s. However, the current expectations are that the consumption will more than double to over 300TWh by 2045. Obviously, this will require a significant effort and large investments.

While the fight against climate change drove the first phase in renewable energy developments, the next phase is likely to be far more significant as it will be driven by energy security.

Prior to the Ukraine war, the opportunity to invest in renewables was strongly linked to tackling climate change. However, since many still doubt that global warming is man-made and others believe that it is futile to try to slow down the warming, the transition to renewable energy faced many obstacles. However, this has changed drastically since the Russian invasion of Ukraine.

Europe, and particularly Germany, has learned the hard way not to be too dependent on energy suppliers that might not share their common interests and values. Europe has been successful replacing Russian energy in the short term, but the longer-term solution is increased electrification, mainly through accelerated renewable energy deployments. The urgency has increased and the energy transition is accelerating.

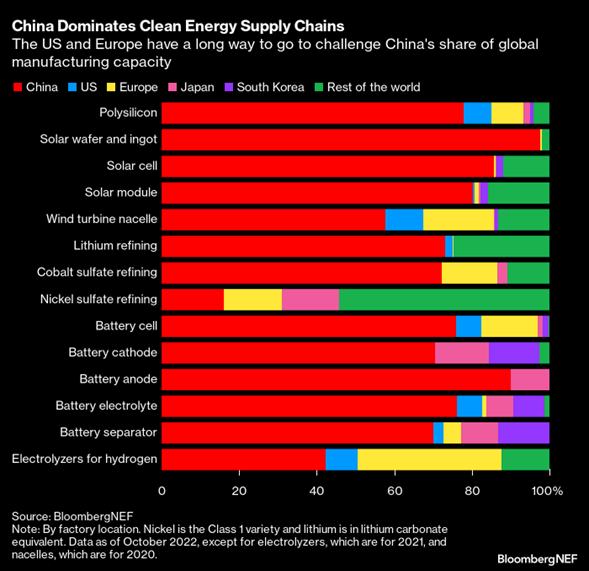

Unfortunately, while Europe was dependent on Russia for almost 50% of its gas consumption, it is even more dependent on China for equipment and components needed to build renewable energy. See the below graph from Bloomberg New Energy Finance (BNEF)

To make it worse, according to the International Energy Agency (IEA), China accounts for most of the announced global manufacturing capacity expansion plans to 2030. For example, for solar PV components, China is behind about 85% for cells and modules, and 90% for wafers; for onshore wind components it is expected to supply about 85% of growth in blade supply and around 90% for nacelles and towers; while for EV battery components, China control about 98% for anode and 93% for cathode material expansions. With that in mind and the risk of a conflict with Taiwan sometime this decade, Europe seems to be in a perilous situation again.

Nevertheless, when IEA updates these numbers early next year, we expect China’s relative share of new expansions to be lower as we are starting to see an acceleration of new capacity announcements in the US. One of the goals of the US’ Inflation Reduction Act (IRA) was to move supply chains home to the US for energy security reasons. Although it is better for Europe to be dependent on the US than on China, it will take years before the US has sufficient export capacity to relieve Europe from its dependence on China.

The European Union is working on new legislation (Net Zero Industry Act or by many called EU IRA) to counter both the Chinese dominance and to reduce the risk of European capacity moving to the US to collect manufacturing tax credits. The leaks from the European commission’s draft proposal, which is due on the 14 th of March, reveals that one of the targets is that Europe should produce at least 40% of its annual deployment needs of certain renewable energy components like solar PV. For wind and batteries, the goal is supposedly 85%. Those are not easy targets considering the BNEF graph above.

The devil is of course in the details, and we are not blue eyed enough to believe in every EU target. However, such ambitious targets will have to come with economic incentives to make it attractive to manufacture components in Europe instead of in low-cost China or heavily subsidized USA.

The same proposal is also expected to include new rules aimed at accelerating permitting of renewable energy projects in Europe. According to Vestas, there are currently four times more wind projects in Europe waiting for permits than there are projects under construction. Since most wind and solar projects in Europe are profitable on a standalone basis without any subsidies, we believe a radical shortening of permitting time is the most important trigger for renewable energy developers and the universe of renewable energy companies.

With significantly increased incentives to build out a renewable energy supply chain both in Europe and the US, we believe the sector is facing unique tailwinds.

FUND PERFORMANCE – DECENT START FOR THE NEW FUND

The fund ended the month up 0.4% (I USD) from the inception on the 6 th of February. The outperformance against the Wilderhill index was 8.2% and iShares Global Clean Energy ETF (ICLN) was 5.7%. As we launched the fund in the middle of the earnings season and following one of the strongest January stock markets over the last decades, we decided to add positions and gross up gradually. We believe this served us well.

The fund ended the month with a gross exposure of 90% and a net of 49%. The aim is to have a net exposure between 40% and 80%. Although we are very optimistic to the renewable energy space, we strongly believe that it makes sense to have a strategy that can generate alpha on a standalone basis on the short side. In February this worked well as the short contribution was 2.5% and the longs lost 2.1%.

The best performing themes in February were US Hydrogen and EU Hydrogen. Both themes were skewed short, and all shorts were down by low double digits after having rallied by 20-30% in January. We are still skeptical to the valuations in the hydrogen space and believe many will face issues as they start delivering on large industrial orders over the next year. Large amounts of green hydrogen will be needed in the energy transition, but the extent to which it will be used is wildly overstated, we believe. The obvious use cases are to decarbonize the existing grey hydrogen which is used in chemical processes like fertilizers and other refining processes. This hydrogen is currently produced from natural gas and highly pollutive. Many of the other use cases like transportation are much less obvious and, in some cases, nonsensical to us.

We are much more optimistic to the solar space both short and long term. In the near term, we believe utility scale is the most attractive segment as Chinese supply chain issues are easing, IRA kicks in and there is significant pent-up demand from US renewable developers who were forced to delay projects last year due to uncertainties around panel availability.

On the other hand, residential solar is facing some short-term demand issues as new regulation is introduced in California and higher interest rates make financing of residential solar more expensive. However, this is only a temporary set-back as the penetration in the US market is still only about 4% and electricity prices are likely to increase for years to come as utilities will be allowed to increase prices to pay for required grid upgrades and investments in clean energy. Rooftop solar is a great way for people to lower their utility bill and the more a home is electrified, the more it makes economic sense.

“Solar” is our largest theme accounting for more than a third of our gross exposure and it was long biased by 20-30% most of the month. Our largest position in the solar space and our second largest position in the fund is Array Technologies (ARRY), one of the global leaders supplying solar tracking systems to utility scale solar projects. Unfortunately, the stock declined by 16% in February as there was uncertainty around reporting of the fourth quarter results. Also, its largest competitor listed towards the end of the month and likely attracted some capital away from ARRY. The position cost us about 1% of NAV.

Despite the loss in ARRY and the heavy long skew in “Solar” (the Solar index, TAN ETF was down 7%), the theme was flat on the month due to strong performance from one short within the US residential space and the long position in First Solar (FSLR), the biggest IRA winner so far.

More importantly, ARRY has so far in March recovered most of the February decline as it issued solid preliminary Q4 results and removed the uncertainty regarding its earnings announcement.

The largest losing theme of the month was “US Renewable Developments”, which deducted about 50bps from the NAV. The theme consists of no shorts and only two longs, Nextera Energy (NEE) and AES Corp (AES). Both are utility companies with a strong exposure to renewable developments and will be big beneficiaries of the IRA tax credits. NEE is maybe the only US utility with a real zero plan which relies on a material buildout of renewables and storage as well as green hydrogen conversions of natural gas plants. NEE’s clean energy capex will increase from about 85% in 2022 to close to 100% in 2024.

We also own some renewable energy developers in Europe as we expect a positive tailwind from the likely ‘EU IRA’ on permitting of renewable energy projects. If, as proposed in the leaked document, allowed approval time is reduced to maximum 18 months, it will be a major improvement versus the current average of 4-5 years. Costs will be reduced, but more importantly, it would reduce uncertainty and increase returns.

We look forward to updating you again at the end of March, our first full month of trading.

Sincerely,

Vidar & Joel

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Over 15 years of investment experience spanning both public markets and private equity.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Spent six years at Horizon Asset in London, a market-neutral hedge fund.

- Started working with Vidar Kalvoy in 2012.

- Five years in Private Equity at Morgan Stanley.

- Began his investment career in the technology sector at Swedbank Robur in Stockholm in 2006.

- Holds an MSc in Engineering from the Royal Institute of Technology (KTH), Stockholm.

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Has managed energy equities since 2006 and brings more than 20 years of experience in portfolio management and equity research.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Head of Energy Investments at Horizon Asset in London for nine years, a market-neutral hedge fund.

- Experience from energy investments at MKM Longboat in London and equity research in the technology sector in Frankfurt and Oslo.

- Holds an MBA from IESE in Barcelona and a Master’s in Business and Economics from the Norwegian School of Economics (NHH).

- Before entering finance, he served as a lieutenant in the Royal Norwegian Navy.

IMPORTANT INFORMATION. This is a marketing communication.

Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the PRIIP of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/. Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested. Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.