This material is marketing communication.

Note that the information below describes the share class (I USD), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class return. The information below regarding returns therefore differs from the returns in other share classes.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

1) Share Class I USD

FUND MANAGER COMMENTARY

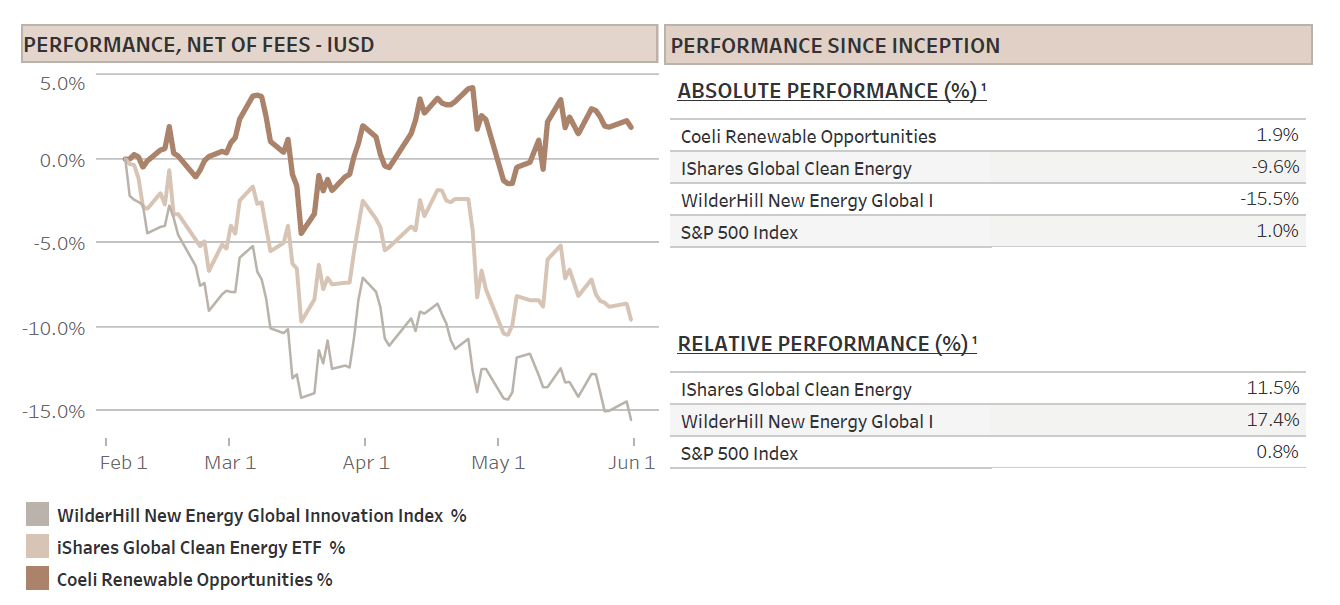

The Coeli Renewable Opportunities fund lost 0.4% net of fees and expenses in May. It is up 1.9% since the inception on February 6, 2023.

The fund has outperformed the most relevant reference indices, the Wilderhill New Energy Global index (NEX) by 17.5% and the iShares Global Clean Energy (ICLN) by 11.5% since inception. During May, the fund outperformed the NEX and ICLN by 3.0% and 1.5%, respectively.

As renewable energy stocks overall fell, our longs lost 1.2% while the shorts gained 0.8%. The ‘Solar’ theme, which is skewed long, added 2.6% of performance despite the main solar index (the TAN ETF) declining by 3% during the month. The outperformance can be attributed to many of our solar holdings benefiting from the release of the detailed guidelines provided for the Inflation Reduction Act.

The renewable energy sector sold off during the month, due to concerns that the industry would be heavily impacted if the debt ceiling discussions should lead to a renegotiation of the IRA.

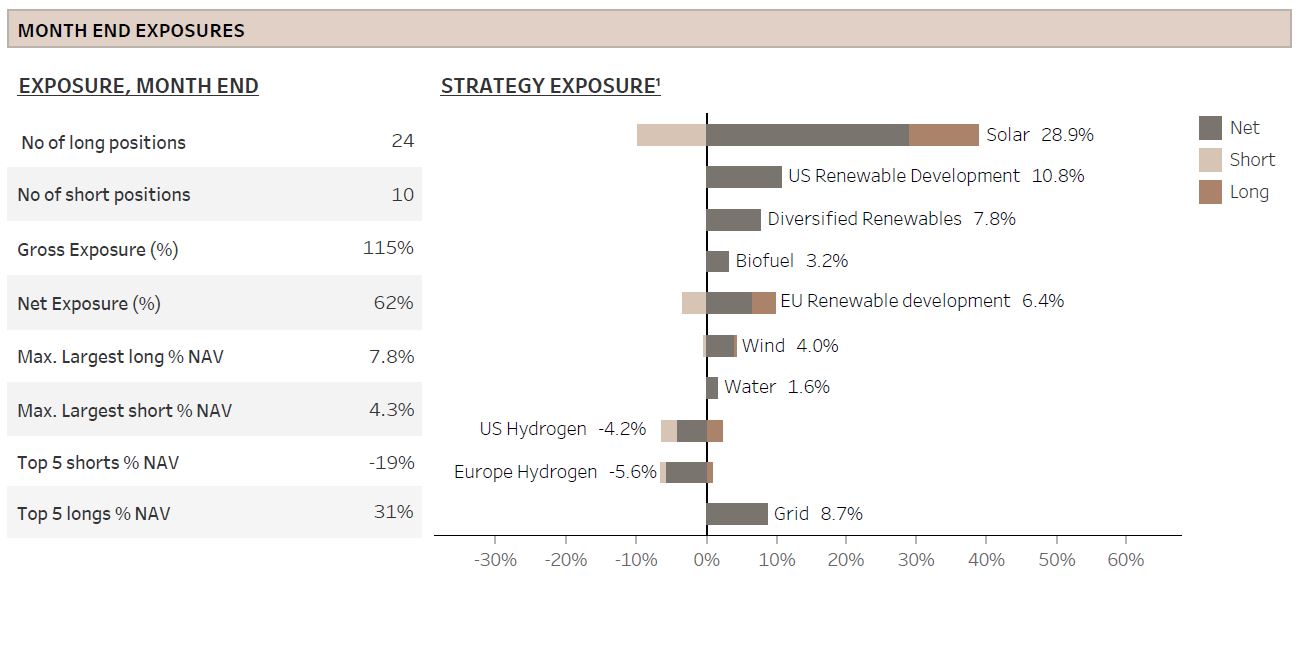

As we deemed the risk of IRA cuts to be low, we increased the fund's average net exposure to around 60%, surpassing the 40-50% range we have held over the last months. Note that our target net exposure ranges from 40% to 80%. At the end of the month, our net and gross exposure stood at 62% and 115%, respectively. More detailed information on the fund's performance can be found below.

MARKET COMMENT – ARTIFICAL INTELLIGENCE FUELLING THE TECH RALLY

The S&P 500 was up 0.3% in May and has increased by 8.9% in the five first months of the year. However, the market breath remains concerning with the top 15 companies in the US driving 100% of the S&P's performance, while the other 485 stocks in aggregate are flat on the year. Furthermore, the VIX (the volatility index of the S&P 500) is trading at pre-pandemic levels for the first time in four years.

There were several reasons for the calm and relatively strong markets. First, the month started with a fully priced in interest rate increase that was believed to be the end of the FED hiking cycle. Second, the mini-banking crisis of March is perceived to be in the rear-view mirror, at least for now. Third, the debt ceiling negotiations were less tumultuous than expected, resulting in lower volatility and a favorable outcome for financial markets. Fourth, investor positioning was bearish heading into the month with many expecting a recession. However, as first quarter earnings season was better than expected, investors were forced into the market again.

Nevertheless, the primary driver of the rally was undoubtedly artificial intelligence (AI) and the expectation that its advancement would fuel a new era of profitability. This is evident from the tech heavy Nasdaq 100 outperforming the S&P 500 by the largest margin in over 20 years. At present, the potential of AI appears to be more important for tech stocks than the risks associated with higher interest rates or prolonged elevated rates.

While the market in early May expected nearly three interest rate cuts by the end of the year, the current outlook indicates only a 50% chance of a new rate hike by July, with no rate cuts anticipated until 2024. The market is once again pricing in a soft landing for the economy, with inflation expected to fall to FED’s 2% target without any further substantial increases in interest rates and only a mild recession, if any.

However, considering that certain key macro indicators (PMIs) are signaling a potential recession, the unemployment rate is at historically low levels, last witnessed in the late 1960s, and core inflation remains elevated exceeding the Federal Reserve's base rate, we believe this optimistic view may prove challenging. Nonetheless, our optimism continues to grow in the renewable energy sector, both in the short, medium, and long-term.

RENEWABLE ENERGY – THE STARS ARE ALIGNING?

Investors in renewable energy and decarbonization have faced many false starts ending in bubbles bursting in the past. However, as we have discussed in previous monthly reports, the long-term structural growth in these areas is virtually assured. The energy transition has evolved from merely combating climate change to safeguarding energy security and ensuring resilient supply chains. Consequently, we have entered a more potent and transformative phase of investments in alternative energy and decarbonisation. This is particularly evident in the Western world where the transition is accelerated by legislative acts such as the Inflation Reduction Act (IRA) in the US and RePowerEU and the Net Zero Industrial Act (NZIA) in Europe.

Despite these positive developments, stocks in the sector have not performed that well in recent times. However, we believe this is about to change and we foresee a positive shift in renewable and clean technology stocks in the short, medium, and long term.

The long-term case is well-established as we outlined above and specifically in our February monthly letter. In the medium term, into 2024 and 2025, we anticipate an improvement as inflation and interest rates normalize resulting in increased valuation of long-duration assets, which form a substantial portion of the renewable stock universe.

Furthermore, progress is being made on the NZIA, the European version of the IRA. Germany is preparing to announce a series of legislative measures, including the introduction of a "German IRA." This involves classifying renewable energy sources as "assets of national and strategic interest," a crucial designation that effectively protects renewable energy developers from legal challenges brought by municipalities or households citing concerns such as wind parks being too close to residential areas or endangering certain bird species. This change is crucial for reducing delays in the development of renewable energy and it is expected to unleash significant investments in the sector. Goldman Sachs predicts a potential of up to 250 billion euros in Germany alone.

Many European countries are likely to follow Germany's example, leading some to believe that the European IRA will mobilize greater investments than its American counterpart. Given that the US IRA is not capped like the NZIA in Europe, we are not convinced. Nonetheless, it is undeniable that both legislative packages will trigger investments in the trillions.

There are also some important developments worth noting in the short term. First, US clean technology stocks significantly underperformed in April and May as investors were on a “buyers’ strike”. As we discussed in last month’s letter, investors feared that the IRA would be entangled in discussions regarding the US debt ceiling. Fortunately, this did not transpire. Second, the specific guidelines for the IRA tax credits are currently being released, which means that investments will start to flow to projects and equipment, benefiting the involved companies. Third, permitting bottlenecks are about to be removed on both sides of the Atlantic. There are still four times more wind projects waiting for permitting than under construction, which should indicate the importance of streamlining the process.

To sum up, while our optimism initially revolved primarily around the longer-term prospects, we are increasingly becoming more optimistic about the investment opportunities in renewable energy across the long, medium and the short term.

FUND PERFORMANCE – SOLAR SPACE BENEFITS FROM IRA GUIDELINES

The fund lost 0.4% (I USD) in May. Six out of ten themes were profitable, but two of the losing themes or in fact two losing stocks, had relatively large drawdowns. The large winner was the ‘Solar’ theme adding 2.6% to NAV.

Utility scale focused solar stocks like Array Technologies (ARRY) and Shoals Technologies (SHLS) did particularly well as the details on domestic content credits in the IRA triggered a rally in most of the utility scale names. ARRY, with 70-75% of its supply chain based in the US benefitted from the strong emphasis on domestic content and emerged as a significant outperformer. The company even has the potential to scale the supply chain to 95% domestic content. However, we are still awaiting some additional details before ARRY's customers can confirm a substantial backlog of orders. While we have slightly reduced our ARRY position, it remains one of our preferred companies within the solar industry this year.

Two other solar stocks, First Solar (FSLR) and Enphase (ENPH), made positive contributions in May after experiencing significant losses in April. As we have previously highlighted in our monthly reports, FSLR is likely the largest beneficiary of the IRA. The newly released details played right into its hands and the stock rose 11% in May. On the other hand, ENPH is still awaiting the IRA guidelines regarding manufacturing tax credits for inverters. Nonetheless, it had a positive month following the sharp decline in April.

The performance of the broader solar sector in May was mixed. The concerns over the debt ceiling negotiations led to a sell-off in some highly leveraged companies. The TAN index’s 3% decline vs our ‘Solar’ theme’s 2.6% rise highlights the significance picking the right stocks.

The theme that had the largest negative impact was 'Diversified Renewables', which contains only Chart Industries (GTLS), deducting 1.7% from the overall performance. GTLS is one of our favourite energy transition plays, and we have previously discussed its strong market position in our monthly letters, in particular the March report. The stock had rallied into April, reaching recent highs, but declined by 18% on no significant news during May, trading near its lowest point of the year by the end of the month. So far in June, the stock is up more than 20% on no other news than that it has repeated its full year guidance.

GTLS is one of our largest positions and we expect the stock to break out of its recent month’s trading pattern when it confirms that the integration of last year’s Howden acquisition is going according to plan, it delivers on this year’s guidance, and it continues to book high order intake positively influenced by the IRA and other government initiatives.

The second largest losing theme of the month was US Renewable Development, which lost 1.3%. This theme contains no shorts and only two longs: Nextera Energy (NEE) and AES. Both are large utility companies with a strong focus on transitioning to clean energy and exiting fossil fuels. AES pulled down the performance in May as the company at its early May Investor Day conference issued growth targets slightly below the market expectations. However, these reduced targets were solely due to the company's accelerated coal exit plan by 2025.

Considering that the lower EPS growth is a result of the coal exit, we believe that AES' earnings should trade at a higher multiple after 2025. This would suggest a reduction in the ESG discount associated with the company. AES has outlined ambitious plans to expand its renewable capacity threefold by 2027, reaching 40-45 GW and supporting a 19-21% EBITDA CAGR for its renewable energy segment. The company boasts a robust pipeline of projects both domestically and internationally, although a significant portion of its current operations generate revenues in USD. Furthermore, AES has made substantial investments in new energy technologies, including battery companies like Fluence (FLNC), as well as various green hydrogen projects.

AES is one of two of our portfolio companies that screens poorly on ESG metrics due to its involvement in coal. The other one is RWE, one of the world's largest renewable energy companies, which is also in the process of exiting its legacy coal business, although negotiations with the German government are required and likely to prove cumbersome. Despite their current ESG ratings, we view both AES and RWE as exemplary transition companies and we have deliberately chosen to overlook the ESG ratings. We strongly believe it is crucial to be actively engaged and support companies that are transitioning from brown to green energy.

We believe this is worth highlighting as RWE was one of the companies that helped Europe through the energy crisis last year. The German government required RWE to increase coal fired power generation despite previous requirements to do the opposite. The ESG exclusion dilemma has seldom been more apparent.

We look forward to updating you again at the end of June.

Sincerely,

Vidar & Joel

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Over 15 years of investment experience spanning both public markets and private equity.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Spent six years at Horizon Asset in London, a market-neutral hedge fund.

- Started working with Vidar Kalvoy in 2012.

- Five years in Private Equity at Morgan Stanley.

- Began his investment career in the technology sector at Swedbank Robur in Stockholm in 2006.

- Holds an MSc in Engineering from the Royal Institute of Technology (KTH), Stockholm.

- Portfolio Manager and Founder of the Coeli Energy Opportunities Fund.

- Has managed energy equities since 2006 and brings more than 20 years of experience in portfolio management and equity research.

- Managed the Coeli Energy Transition Fund from 2019 to 2023.

- Head of Energy Investments at Horizon Asset in London for nine years, a market-neutral hedge fund.

- Experience from energy investments at MKM Longboat in London and equity research in the technology sector in Frankfurt and Oslo.

- Holds an MBA from IESE in Barcelona and a Master’s in Business and Economics from the Norwegian School of Economics (NHH).

- Before entering finance, he served as a lieutenant in the Royal Norwegian Navy.

IMPORTANT INFORMATION. This is a marketing communication. Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/. Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested. Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.