Before making any final investment decisions, please read the prospectus, its Annual Report, and the PRIIP of the relevant Sub-Fund here

This material is marketing communication

An article focusing on the unique tailwinds the renewable energy sector is facing.

Europe is facing a two-pronged energy challenge that will accelerate the shift toward renewable energy sources. First, the region's dependence on fossil fuels from politically unstable countries has unravelled the security of energy supplies. Second, the expected increased electrification of industries, homes and the rising number of electric vehicles imply a massive change in direction for the energy system. For instance, Sweden is consuming about 140TWh of electricity per year and has been at this level since the late 1980’s. However, the current expectations are that the consumption will more than double to over 300TWh by 2045. Obviously, this will require a significant effort and large investments.

While the fight against climate change drove the first phase in renewable energy developments, the next phase is likely to be far more significant as it will be driven by energy security.

Prior to the Ukraine war, the opportunity to invest in renewables was strongly linked to tackling climate change. However, since many still doubt that global warming is man-made and others believe that it is futile to try to slow down the warming, the transition to renewable energy faced many obstacles. However, this has changed drastically since the Russian invasion of Ukraine.

Europe, and particularly Germany, has learned the hard way not to be too dependent on energy suppliers that might not share their common interests and values. Europe has been successful replacing Russian energy in the short term, but the longer-term solution is increased electrification, mainly through accelerated renewable energy deployments. The urgency has increased and the energy transition is accelerating.

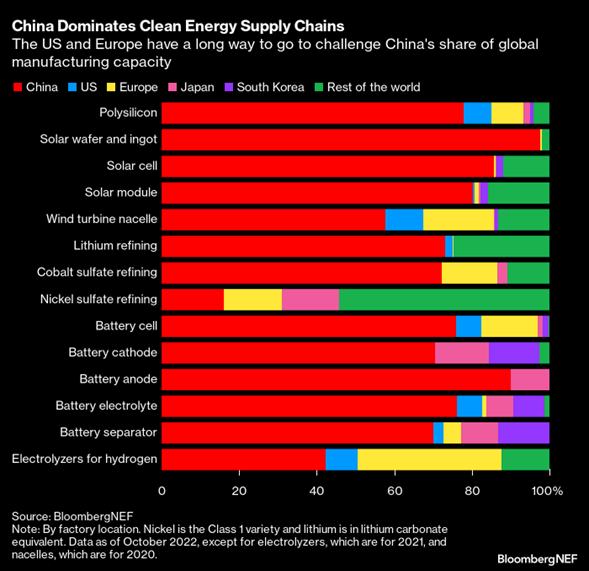

Unfortunately, while Europe was dependent on Russia for almost 50% of its gas consumption, it is even more dependent on China for equipment and components needed to build renewable energy. See the below graph from Bloomberg New Energy Finance (BNEF)

To make it worse, according to the International Energy Agency (IEA), China accounts for most of the announced global manufacturing capacity expansion plans to 2030. For example, for solar PV components, China is behind about 85% for cells and modules, and 90% for wafers; for onshore wind components it is expected to supply about 85% of growth in blade supply and around 90% for nacelles and towers; while for EV battery components, China control about 98% for anode and 93% for cathode material expansions. With that in mind and the risk of a conflict with Taiwan sometime this decade, Europe seems to be in a perilous situation again.

Nevertheless, when IEA updates these numbers early next year, we expect China’s relative share of new expansions to be lower as we are starting to see an acceleration of new capacity announcements in the US. One of the goals of the US’ Inflation Reduction Act (IRA) was to move supply chains home to the US for energy security reasons. Although it is better for Europe to be dependent on the US than on China, it will take years before the US has sufficient export capacity to relieve Europe from its dependence on China.

The European Union is working on new legislation (Net Zero Industry Act or by many called EU IRA) to counter both the Chinese dominance and to reduce the risk of European capacity moving to the US to collect manufacturing tax credits. The leaks from the European commission’s draft proposal, which is due on the 14 th of March, reveals that one of the targets is that Europe should produce at least 40% of its annual deployment needs of certain renewable energy components like solar PV. For wind and batteries, the goal is supposedly 85%. Those are not easy targets considering the BNEF graph above.

The devil is of course in the details, and we are not blue eyed enough to believe in every EU target. However, such ambitious targets will have to come with economic incentives to make it attractive to manufacture components in Europe instead of in low-cost China or heavily subsidized USA.

The same proposal is also expected to include new rules aimed at accelerating permitting of renewable energy projects in Europe. According to Vestas, there are currently four times more wind projects in Europe waiting for permits than there are projects under construction. Since most wind and solar projects in Europe are profitable on a standalone basis without any subsidies, we believe a radical shortening of permitting time is the most important trigger for renewable energy developers and the universe of renewable energy companies.

With significantly increased incentives to build out a renewable energy supply chain both in Europe and the US, we believe the sector is facing unique tailwinds.

Joel Etzler

Portfolio Manager Coeli Renewable Opportunities

Vidar Kalvoy

Portfolio Manager Coeli Renewable Opportunities