Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class' return. The information below regarding returns therefore differs from the returns in other share classes.

August performance

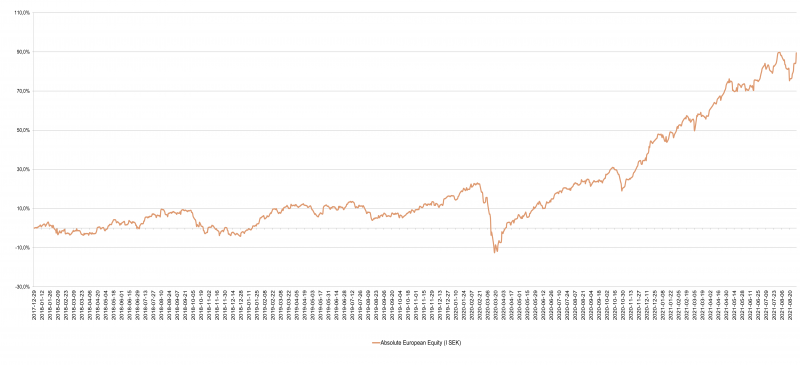

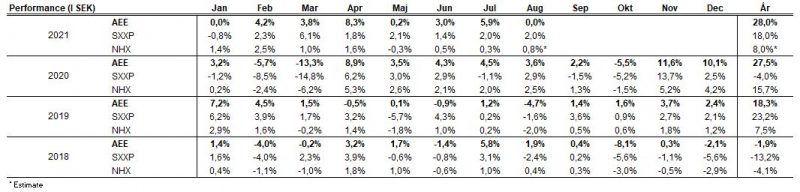

The value of the fund was unchanged in August (share class I SEK). The Stoxx600 (broad European index) increased during the same period by 2.0 percent and HedgeNordic's NHX Equities tentatively rose 0.8 percent. The corresponding figures for 2021 are an increase of 28.0 percent for the fund, 18.0 percent for Stoxx600 and 8.0 percent for NHX Equities.

Equity markets / Macro environment

There were still cheerful tones in the world's stock markets in August. The broad European index rose by 2.0 percent and the S&P500 by as much as 2.9 percent. Continued strong company reports followed by new repurchase programs contributed, among other things, to the positive attitude. In the middle of the month some turbulence arose when it became increasingly clear that the delta variant has serious consequences in parts of the world. Rising nervousness ahead of the Fed's meeting in Jackson Hole at the end of the month most likely also played a role. The turbulence lasted (as usual) only for a couple of days.

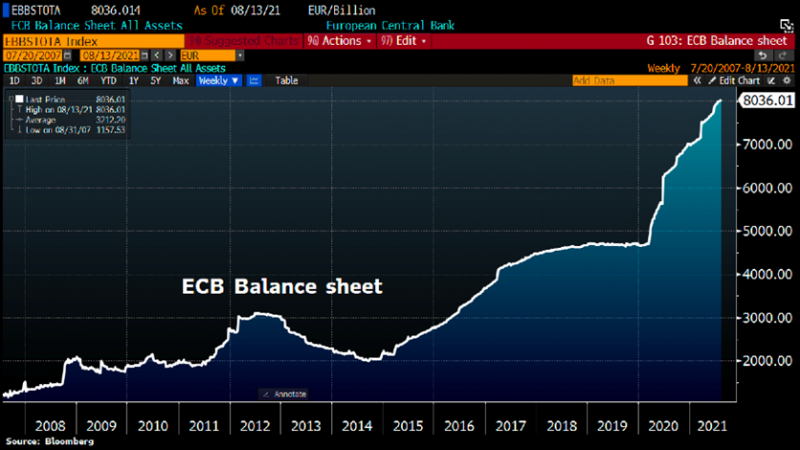

The central banks' balance sheets around the world continue to support different asset classes, of which the market is well-aware. Below is the ECB's balance sheet, which now exceeds EUR 8 trillion (12 zeros) and is just over half of the eurozone's GDP. The Fed's balance sheet corresponds to about 36 percent of US GDP.

Source: Bloomberg

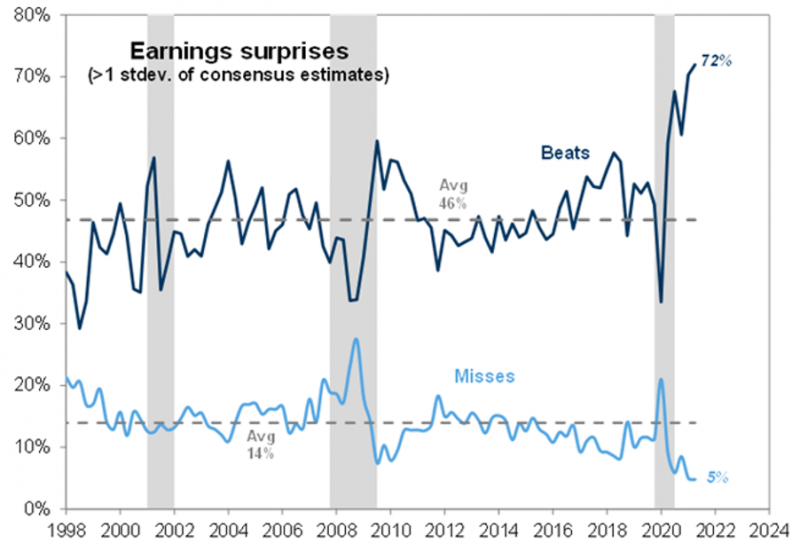

With a report season now over, it can be concluded that the market was right. It was a historic summer and a victorious party. 72 percent of American companies beat the market's already high expectations.

Source: Goldman Sachs

Until 27 August, the S&P500 had hit a new all-time high 52 days this year or just over 31 percent of this year's trading days. The previous record is from 1994 when new all-time highs were hit as much as 34 percent of the days of the year.

Source: Goldman Sachs

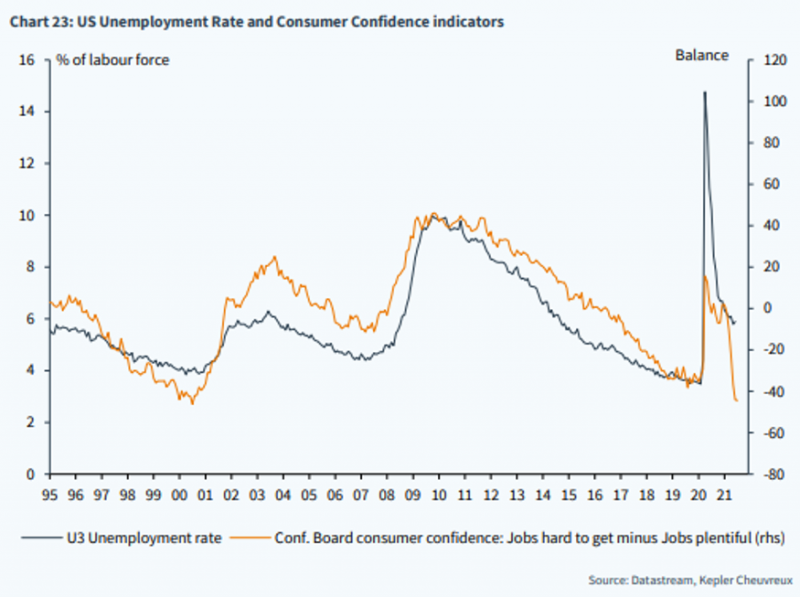

US Federal Reserve Chairman Jay Powell's speech on August 27 clearly signalled "clear progress" in the recovery of the labour market. The stock market interpreted this as meaning that the stimuli will start to be reduced at the beginning of next year. We are now at the beginning of the end of the unprecedented stimulus shock that began last spring. Below is the development of American unemployment.

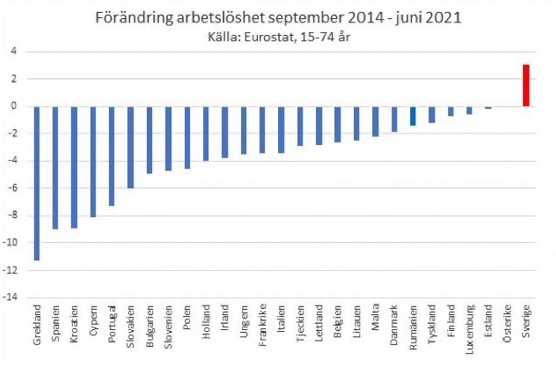

Sweden's evolution of unemployment is not as impressive. Between 2014 and 2021, 27 of the 28 countries in the EU had reduced their unemployment. Only one country showed a clearly negative development - Sweden! Depressing and a defeat to everyone involved.

Source: Eurostat

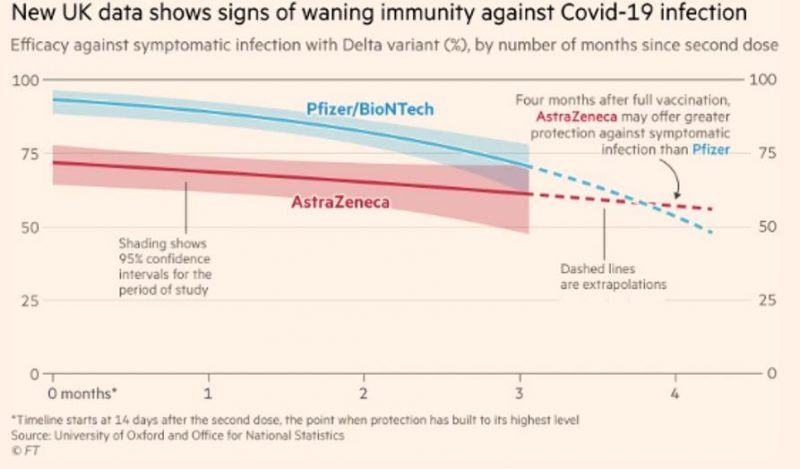

After a quiet summer, covid-19 development began to go in the wrong direction again in August. In Israel, which is at the forefront of vaccinating its population, almost 60% of those who have recently been hospitalized due to covid-19 were fully vaccinated. 87 percent of those affected were over 60 years old. These figures indicate that the virus is more malicious and difficult to stop than previously feared.

The picture below shows that the vaccine's effectiveness decreases faster than previously thought. This finding is hardly desirable and will probably contribute to increased uncertainty in the autumn, although new shutdowns are unlikely to take place.

Source: https://www.ft.com/content/23cdbf8c-b5ef-4596-bb46-f510606ab556

The picture below shows the evolution of American air travellers since the beginning of last year. In the last week of August, 1.47 million passengers flew which was the lowest level in three months and about 0.6 million fewer than the month before (see red arrow). This is partly because people have started working again after their holidays, but the airlines are also reporting a slowdown in leisure travel and an increase in cancellations due to the spread and fear of the delta variant. The same effect can be seen in terms of restaurant and hotel bookings, which is clearly reflected in these types of stocks. Ryanair, on the other hand, expects "a very strong recovery" in the coming months, according to the company's legendary CEO Michael O'Leary. Capacity is expected to return to pre-covid-19 levels in October.

Source: Transportation Security Administration, Bloomberg

German industrial production continued to decline and fell for the third month in a row. Bottlenecks among components (semiconductor biggest problem) is the main cause and capital goods including cars were the most negatively affected sector. Construction investment also declined slightly, while consumer goods grew by 3.4 per cent. European politicians are now urging to expand microchip capacity in Europe to reduce dependence on Asia and the United States. Chip manufacturing can now be classified as socially critical infrastructure.

We are pleased to note that on 10 September, Denmark will open its society completely and all Covid-19 restrictions will be removed. "The epidemic is under control, we have record high vaccination figures," says Minister of Health Magnus Heunicke. Covid-19 is thus no longer categorized as a socially critical disease. It does, however, in New Zealand where during the month one (1!) case of the delta variant was discovered and the whole country was shut down for a week. Sounds like an insanely expensive medicine.

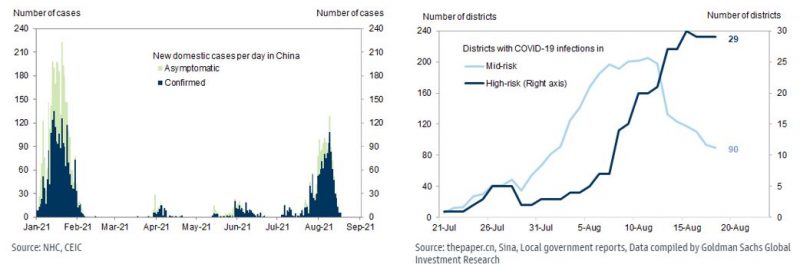

Also pleasing was the development in China, which in August showed clear signs of improvement in the covid situation. The development so far has, for example, led to certain closures of ports in China, which has contributed to the global component shortage.

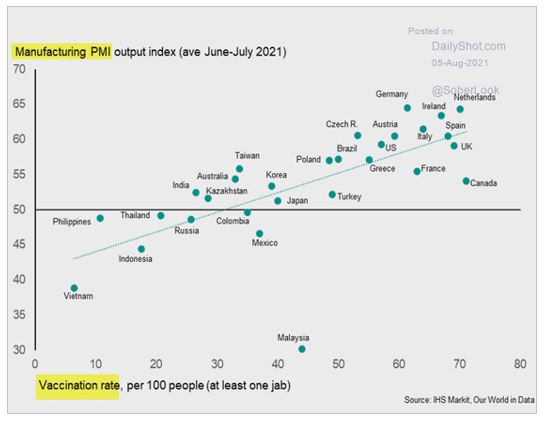

The figure below shows the relationship between the vaccination rate (at least one shot) and the purchasing index for the domestic manufacturing industry. The correlation is high. During the measurement period below (June/July), Sweden was at around 70 percent and with a PMI of just over 65 it signals a very strong economy.

We have all seen horrific images from Afghanistan where the Taliban have now taken power. It is a gigantic failure for the entire western world that has spent time, money and human life (including Swedish) and where darkness is now descending on the population. President Biden is rightly under heavy criticism at home, and this is his first, but major political crisis. The images of a chaotic airport and attempts at evacuation will affect the United States' credibility globally and for a long time to come.

President Putin is likely feeling comfortable thinking of the Afghan-Soviet war that took place between 1979 and 1989, in which the Marxist-Leninist government in Afghanistan was supported by the Soviet Union and the rebels were supported by the United States. The Russian embassy in Kabul is currently protected by the Taliban. He is probably wondering whether the United States would intervene if Russia were to do something in Kiev, Tbilisi or the Baltics. China's Xi Jinping is probably thinking along the same lines about Taipei and Taiwan. Developments in Afghanistan clearly signal that it is free to start provoking the world community. The US withdrawal has created political consequences far beyond Kabul Airport.

Source: CagleCartoons.com

On 9 August, the United Nations Intergovernmental Panel on Climate Change (IPCC) released its latest climate report.

Finally, a very positive article from Reuters which describes how Sweden became the Silicon Valley of Europe. There is hope!

Long positions

ISS

Loyal readers know about ISS, a Danish facility management company. We have, in previous years, been short the stock. Today, it is instead one of the fund’s largest holdings since we believe the market is underappreciating the company’s turnaround. The company released its earnings report for the first half in August. Sales were in line with expectations while the adjusted operating result was 18 percent better than expected. The cash flow generation continues to improve and the company updated its guidance for its free cash flow in 2021. We were happy about the results and note that this is the third consecutive quarter the company releases solid earnings.

To our big surprise, the stock fell in connection with the release. We have identified four possible reasons for this:

- Management chose to keep its guidance for the operating margin for the full year, but the market was hoping for positive revision of the guidance

- A goodwill write-down of 450 million Danish kroner related to ISS’ French business

- A dispute between a third-party service provider has led to management not recognizing revenues related to some specific contracts

- The share had performed well prior to the report being released

We are conscious of our bias, but we think that the three first points are more reflective of management cautiousness rather than a deteriorating business. Given ISS’ lumpy history, management ought to know that the best way forward is to stay conservative regarding both communication and accounting. These are two areas where previous management teams at ISS have failed to impress, to say the least. We have taken advantage of the recent share price weakness and added to our ISS position. The stock was down 2 percent in August and has risen 37 percent for the full year.

Photocure

One of the fund's larger holdings, Photocure, released earnings during the month. Sales were in line with expectations, but expenses were a bit higher than expected. Overall, we thought the report was decent, but it did not have many “exciting” ingredients. Instead, management warned about continued uncertainty related to Covid-19 which is affecting the sales. Furthermore, cystoscopy partner Karl Storz has recently decided to upgrade the cystoscope with which Photocure’s product is sold. This will delay some of the current year’s sales into the next year, as many end customers will wait for the updated cystoscope (which has not been updated since 2005). We think the updated cystoscope will have a significant, positive effect on 2022 sales.

We continue to have a positive stance on Photocure which has many attributes we like; high growth, high gross margin, low capital intensity, high returns on capital employed, a low relative valuation, optionality (Cevira, M&A, and more) and a unique asset in Hexvix/Cysview. We are also confident in CEO Daniel Schneider. We bought shares for eight consecutive days, each day with some increased frustration, as the stock continued to weaken. We were rewarded on the last day of the month when the stock appreciated by 8 percent. For the month in total, the stock was down 8 percent. For the full year, the stock is up 15 percent. The graph below shows the experienced volatility in August.

Source: Bloomberg

Atai

Atai had a good August as the share rose six percent. Since the IPO in June 2021, the stock has risen 9 percent. We invested in Atai in 2018 when it was private. The stock has risen approximately 1100 percent since. As is customary in these situations, we entered a six-month-long lock-up in the Atai share in connection with the IPO. Hence, we cannot sell any shares during this period. We are comfortable with the company’s development. In its recent half-year report, the company announced 18 “triggers” for the coming 18 months. We are looking forward to the journey.

Sedana Medical

Sedana Medical released several good news in August. Among other things, the company received market approval for inhaled sedation in France, which was earlier than expected. The company also released a good quarterly report which exceeded our expectations. Lastly, Sedana communicated that one of their studies will be published in Lancet. Hat trick! We continue to be impressed by this company which is improving bit by bit. The stock rose by 11 percent in August, which follows an appreciation of 20 percent in July. For the full year, the stock has risen 11 percent.

Rugvista

Many market participants seem to have “feared” Rugvista’s report. When the company released numbers that were in line with expectations the share rose in relief. As we mentioned in our previous monthly letter, Rugvista’s share price had suffered some weakness during the summer after the e-commerce “market participant” Desenio's profit warning. This release should clear the worst worries, even if concerns related to the weather and the Covid-19 recovery remain. The share was unchanged in August.

Surgical Science

Surgical Science (SUS) shares had a very volatile August. From the previous month to the lows in August, the stock fell 17 percent, before turning around and closing the month at the same levels as by the end of July. We bought more shares at the lower levels since we thought the main reasons for the share price decline were technical and related to the capital raise that was performed in connection with the acquisition of Symbionix. During the month, SUS released another good report. As many readers know by now, SUS has been a very good investment for the fund. We highlight the last sentence in Gisli Hennermark’s CEO letter: “It is a great feeling to dare think big, and, by doing our homework and working hard, succeeding in what we set out to do.” We can only agree and applaud.

ArcticZymes

One of the fund’s largest losers in August was Norwegian ArcticZymes. The company develops enzymes and has some similarities to Swedish Genovis, which some of you know we have had interests in before. ArcticZymes is a growth company with gross margins close to 100 percent. We have a middle-sized position in the company (3-4 percent of our assets). One negative aspect of the business is its lumpiness. For the second quarter, the pendulum swung in the wrong direction and its earnings were worse than expected. The stock price fell 20 percent on the day of the report. At the same time, we note that management released guidance for the full year that was in line with analyst expectations before the report. Since we thought the market overreacted to the report, we added to our position.

Knaus Tabbert

Our holding in the German RV-manufacturer Knaus Tabbert saw its share price rise 3 percent in August as the company communicated new financial goals. Management is now aiming for sales of 2 billion euro by 2025, which is equivalent to annual growth of about 20 percent. This should be compared to analyst expectations, which are assuming 10-15 percent growth in the coming years. To reach its growth target, Knaus will invest 220 million euros in production capacity. The “problem” for Knaus has historically been that the manufacturing capacity has been lower than demand, which the company is now trying to fix.

Immunovia

In connection with the second-quarter results, CEO Patrik Dahlen communicated that the first blood tests were now being analyzed in Immunovia’s American laboratory and the first invoices had been remitted and paid. The long-awaited commercialization phase has thus begun. Immunovia is the first company in the world with a test like this, which is a big achievement.

There are several positive factors to consider ahead, which will likely lead to increased interest in the share. During the second half of the year, Immunovia will present actual sales numbers and in the fourth quarter, we can expect sales guidance for 2022. The company is initially targeting individuals with hereditary risk for pancreas cancer and where two relatives have had the disease. This group is made up of approximately 350 000 individuals in the USA, who should have the test twice a year. If the target group is expanded to individuals who only have one case of pancreas cancer among relatives, Immunovia reaches an addressable market of c. 1.5 million individuals (or 3 million tests). The price per test was earlier communicated to be 600 US dollars, but early tests have been sold for 995 US dollars. As a comparison, an MRI scan costs about 6000 – 7000 US dollars and a market study showed that there was a possibility to raise the price per test up to 3 000 US dollars at current demand. Furthermore, the company has communicated that they can increase the performance of the test by removing individuals with a specific gene type. Strong support from key opinion leaders and high interest from patient organizations means we look forward to the sales numbers in the second half. News regarding the commercial launch in Europe, Asia and an updated timeline for reimbursement are upcoming events to monitor.

The share has had a horrible development during the last year (here, we deserve some criticism), and even though the share rose 33 percent in August the market price is only 3 billion Swedish kronor. The market is there waiting and now it is up to the company to deliver on its commercialization plans. If they are at least partly successful, the share price potential is significant.

Short positions

The short portfolio contributed with a negative result during the month. Our short-term negative positions in the German DAX caused the most drawdown. Some stock specific short positions that contributed positively to the result were Swedish Dometic, German Henkel and Norwegian NEL.

Exposure

The net exposure, adjusted for our unlisted holdings, at the beginning and end of the month was 76 and 74 percent, respectively.

Summary

After a very strong development in the first seven months of the year, we experienced some volatility in the portfolio during the month of August. After many of our holdings had a strong development during the summer, August began with several retracements among the holdings. It was topped off with almost exclusively negative price reactions on the reporting day for our companies. The result was an unusually heavy period for the first 20 days of the month. We scrutinized our research thoroughly but found no errors in our analysis (we are very critical!). In most cases, we were genuinely unaware of how the shares were traded in the market after the news.

Our conclusion was that it was largely flow-driven and in a thin summer market, not much is needed to move prices. The combination and consequence of the above meant that in several cases we increased our positions at levels that we consider to be very advantageous. Our conviction, which is based on our own analysis, paid off quickly as the share prices in several holdings turned sharply upwards, last week of August, and the fund experienced a very strong end of the month. One rule we follow is to never be fully invested in a position. We always want the capacity to be able to buy more shares if something unforeseen happens. The biggest failure is not the loss in the first phase of decline but lacking the strength or capacity to buy more at low levels (or even worse, panic and sell). That rule worked flawlessly in August and despite a zero result for the fund, the “engine” in our business (analysis/decision) has had one of its best months since the start 3.5 years ago. It bodes well for the future.

If we zoom out a bit and assess how we have performed during different time periods, we get the following independent data. Note that this is based on the performance as of July this year. We clearly see that the fund's return has been constant in the upper part, 83%-98%, of global equity hedge funds. For example, the first column shows that in July, only two percent of 412 funds with the same strategy had a stronger return. This shows that the fund, over time, can generate returns that are well above average and steadily at the top in relation to other funds in the comparable universe.

Source: HFR

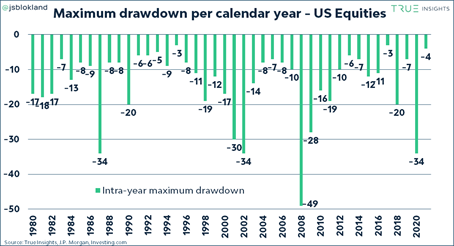

Our market view becomes humbler with each passing month as it is an unusually long time since a major correction has taken place. It has now been almost 200 days since we had a relatively modest five percent decline in the market. Most people probably expect that the typically weak September/October period will offer a bit of turbulence as usual. We currently do not have a strong opinion about this but are prepared to act if this happens when opportunities arise. As usual, we own put options that will provide some protection to the portfolio. The 200 days are illustrated below in a historical context.

Illustrated in another way. The biggest decline of the year of 4 percent is modest from a historical perspective. We have also never had so much stimuli and profit growth going on at the same time.

Source: Trueinsights, JP Morgan, Investing.co.

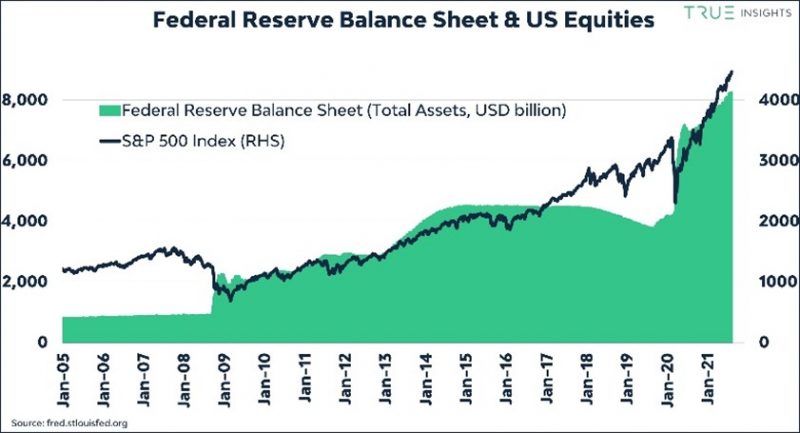

The connection between the expansion of the central banks' balance sheets and share prices is very clear. Within six months, the US Federal Reserve is expected to reduce its expansionary policy. It would be strange if the adaptation goes smoothly.

Source: fred.stlouisfed.org

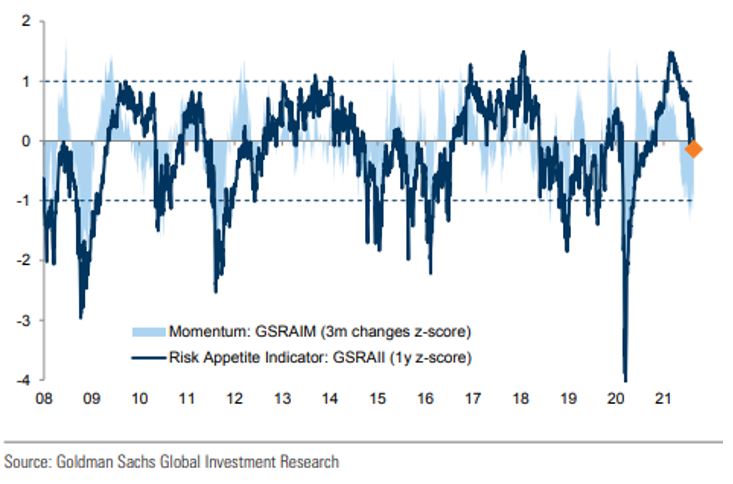

A relatively unusual phenomenon is that while we have reached new record levels, risk appetite has decreased. We guess that this is because it is the largest companies that drive the high levels and that there are more quant and index funds out there. Many smaller companies have had a more modest development over the summer. One of many examples is Swedish Embracer, which is a big retail favourite. The share price reached its peak at the end of April and is down about 15 percent since then.

This is also clearly seen when studying Russell2000, which is a broad American small company index. The levels are the same today as six months ago.

Source: Bloomberg

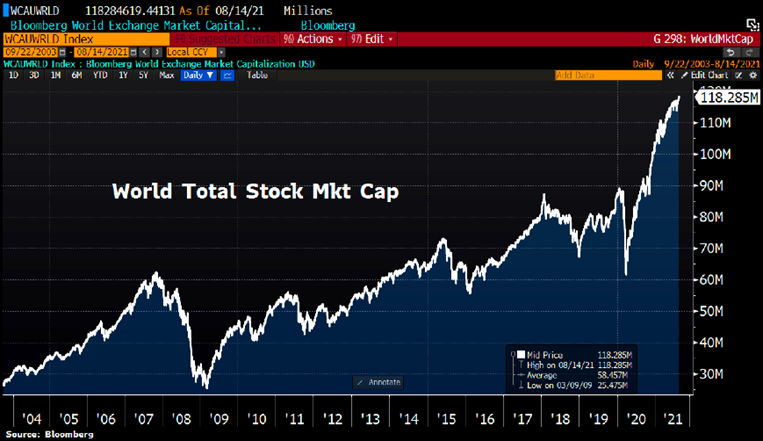

Compare that with the world's total market capitalization.

Source: Bloomber

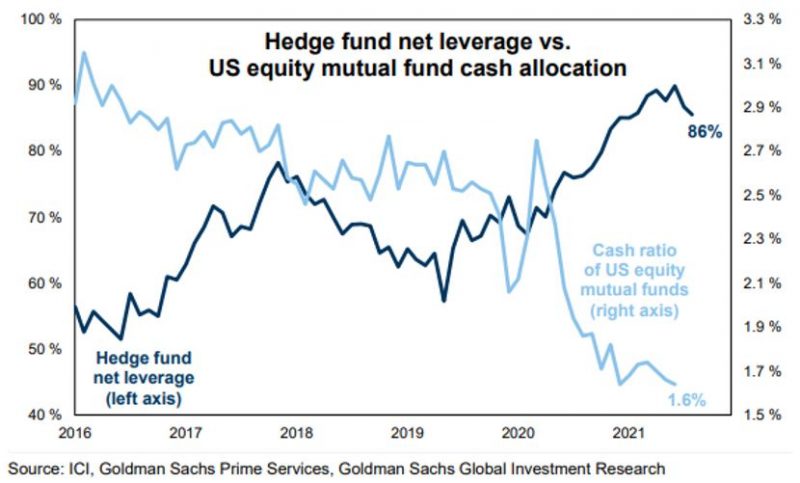

All aboard! Hedge fund exposure is at high levels (left axis) and traditional equity funds are at as low a cash position as is practically possible (right axis).

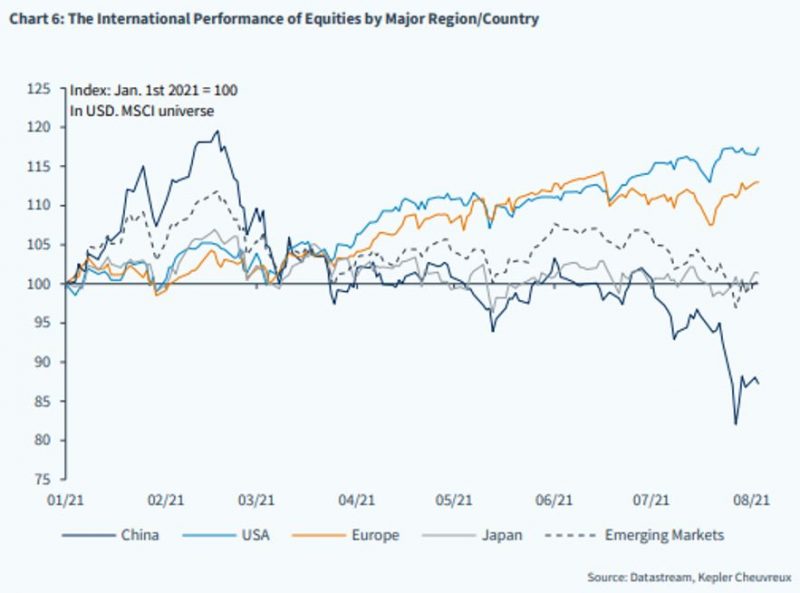

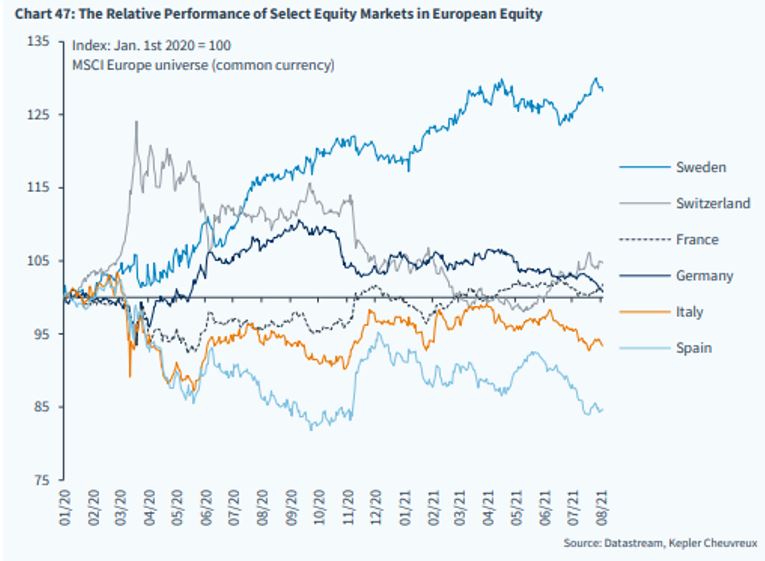

Below are two pictures that show the global development during the year, and Europe since 2020. The USA and Europe are at the top and in Europe, Sweden is in a superior first place. Not bad.

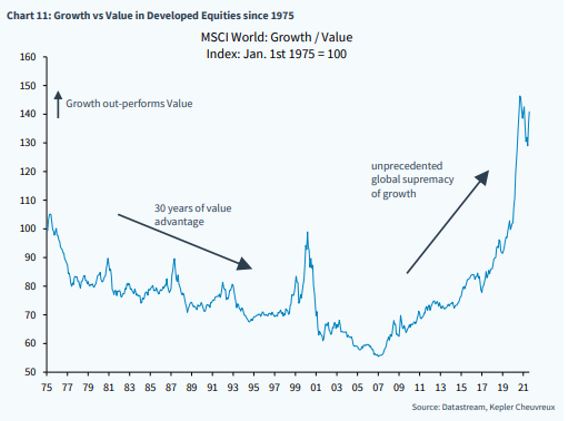

It is clear which type of share has had the strongest development in the last 15 years.

Small caps are rock stars! Since the financial crisis, smaller growth companies have overtaken more traditional larger value companies. A big reason why we ourselves prefer to invest in smaller companies that typically provide a stronger return than a classic equity holding.

The consequence of all the above is that we have increased concentration of our long-term portfolio and invested more in several of our core holdings. On the short side, we have purchased additional external analysis capacity that will give us more ideas and data to be able to have larger short positions. So far it has been a great source of information. We have also bought more put options as we would be surprised if we did not get some turbulence in the next 1-2 months. Israel's development of the delta variant could very well create more problems in the western world, which would then probably lead to increased volatility in the market. If we look further, our best qualified guess is that the market at the turn of the year is at a slightly higher level than today.

Last but not least; if our companies deliver, short-term turbulence does not matter. What we saw from our companies during the second quarter makes us confident that we will see further good news this autumn.

Many thanks again and for the confidence in trusting us with parts of your capital.

Malmö, September 3rd.

Mikael & Team