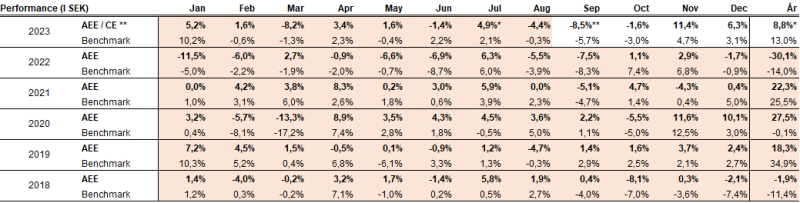

Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class' return. The information below regarding returns therefore differs from the returns in other share classes.

Before making any final investment decisions, please read the prospectus, its Annual Report, and the KID of the relevant Sub-Fund here

This material is marketing communication

Monthly Newsletter Coeli European – December 2023

DECEMBER PERFORMANCE

The fund’s value increased by 6.3% in December (share class I SEK), while the benchmark increased by 3.1%. Since the change of the fund’s strategy at the beginning of September this year, the fund’s value has increased by 6.8% compared to a decrease of the benchmark by 1.5%. Both measured in SEK.

*Adjusted for spin-off of Rejuveron.

** AEE: Absolute European Equity, CE: Coeli European, Benchmark: MSCI Europe SMID Cap Net Total Return SEK.

Please Note: On the 4th of September 2023, the strategy of the fund officially changed from a European long biased equity long/short fund to a European active long only fund. Simultaneously, the name changed from Coeli Absolute European Equity to Coeli European. The track record highlighted in colour in the table above is that of Coeli Absolute European Equity.

EQUITY MARKETS / MACRO ENVIRONMENT

The year ended sour for most asset classes. In the FX market, the US dollar continued to weaken against the euro which is typically good for risk appetite. The Swedish krona had the opposite movement and continued its remarkable recovery, which also reflects increased risk-taking. Both of these currencies began their respective reversals in mid-October which was concurrent with the beginning of the world’s stock markets strong rally. Oil plummeted at the same time, from around $90 a barrel to $76 10 weeks later. Most notable, and the trigger for all of the above, was the US 10-year treasury note which fell from 5% to 3.87% on the last day of the year. Unbelievable!

The fund had another strong month with a positive return of 6.3% and since we changed our strategy on September 4th, we have generated an excess return of 8.3%. Developments for other relevant indices in December were Stoxx600 +3.8%, Nasdaq +5.5% and MSCI SMID +7.0%, all measured in local currencies. The fund's return during the autumn has benefited from our overall macro view, which included falling inflation and interest rates. This, in particular, has fuelled the valuation increase of small and medium-sized companies from low levels but as common in a concentrated portfolio it is the selection and composition of companies that has been vital.

After a very strong November, the fund's biggest short-term risk at the beginning of December was that our holdings would retract. Until December 8th, it was quiet with few company and macro news stories. On the afternoon of December 8th, US labor market data was released showing unemployment at a low 3.5%, versus expectations of 3.7%. Interest rates shot up immediately and some turbulence was also felt in the FX market. For three days we were not in sync with the rest of the market, but when Fed Chairman, Jerome Powell, began his press conference on the evening of December 13th, he was surprisingly soft in tone and the stock markets began to rise. On the morning of December 14th, Swedish inflation data was published and it was as good as we had hoped for. From that point until the end of the year, we generated our entire December return and adjusted for our spin-off of Rejuveron, the fund rose by 8.8 percent in 2023. Since the lowest level in October, the fund returned approximately 25% and contributions came from all corners. Several price reactions that stand out during that period are Bonesupport with 65%, Cargotec with 48%, Carel with 38% and Corem with a modest 100% (!)

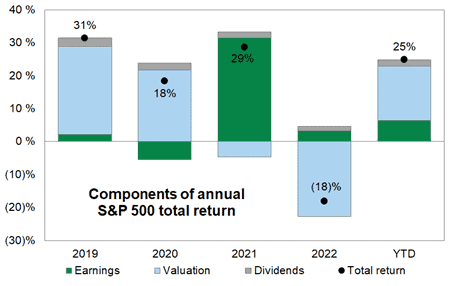

Most people have probably been surprised by the strength of the stock market in 2023. Despite a limited profit growth, the annual return was good and the biggest chunk came from an expansion in multiples. The image below shows where the returns came from in the US market.

Source: Goldman Sachs

During the year the fund has had an overexposure to Sweden with an exposure in recent months of around 35%. There are several reasons for this, but the main one is that Sweden is our home market and we like to think we have an edge there because of that. In addition, it is a market that has many interesting companies and from a European perspective is clearly the leader in terms of technology companies. As an asset class, small companies and in particular Swedish ones has, since January 2 2022, 22 months ago, been frozen out while inflation and interest rates have rocketed but is now finally starting to thaw. When we review the December events, it can be concluded that Sweden was probably the world's best stock market during the last month of the year with +12% for OMX30 (Stockholm Stock Exchange) measured in USD.

Below is December returns across various regions. The penultimate column to the right measured in local currency and final column to the right measured in euros. Note the difference in Sweden between SEK and EUR returns.

Source: Bloomberg

A strong recovery for a severely battered Swedish real estate sector helped drive returns. Of the 10 best real estate stocks in the Stoxx600 last year, half were Swedish. That says a lot about how underweighted and shorted the Swedish real estate companies have been. Our own holdings in SLP and Corem had an annual return of 33% and roughly 34%respectively (including dividends). The companies have completely different profiles and risk levels, but the returns were roughly the same. Adjusted for volatility, SLP was the clear winner, likely across all of Europe. During the year, we had an overexposure to the real estate sector (a total of 11%of the fund). A mistake on our part was that we were invested too early, as the sector, especially in the first half of the year, was under pressure. However, we were more than compensated in the second half of the year, especially in November and December. Our view of the real estate sector ahead of 2024 remains positive, driven by a falling interest rate. We're happy to note that Blackstone invested more in European real estate than any other geographic region in 2023. They also say they have an additional $40 billion to invest.

Source: Bloomberg

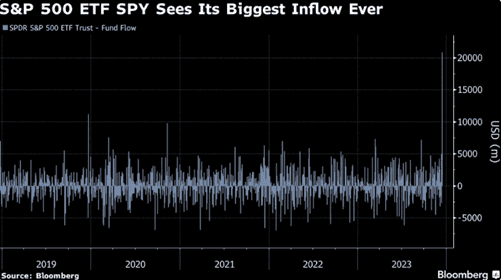

Hop on the bandwagon! After the Fed meeting on December 13th, Wall Street's largest and oldest ETF, SPY (S&P500) received the largest inflow ever. Almost USD 20.8 billion was received in one day and USD 24 billion in one week which was the biggest weekly inflow in 30 years. This created some pressure in the market.

Source: Bloomberg

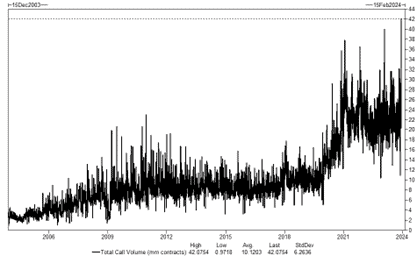

Further evidence of beta hunting came in the options market. Never before has the volume of call options been higher than on December 14th - 42 million contracts.

Source: Goldman Sachs

A lot of financial history was made in December. The Russell 2000 technology index outperformed the broad Nasdaq index by 3.3% points on December 13th , which was the sixth-largest difference in more than 20 years. The Russell 2000 set a new 52-week high after making a 52-week low just 48 days earlier. It was the shortest turnaround time in the index's history, which dates back to the 1970s. Unbelievable.

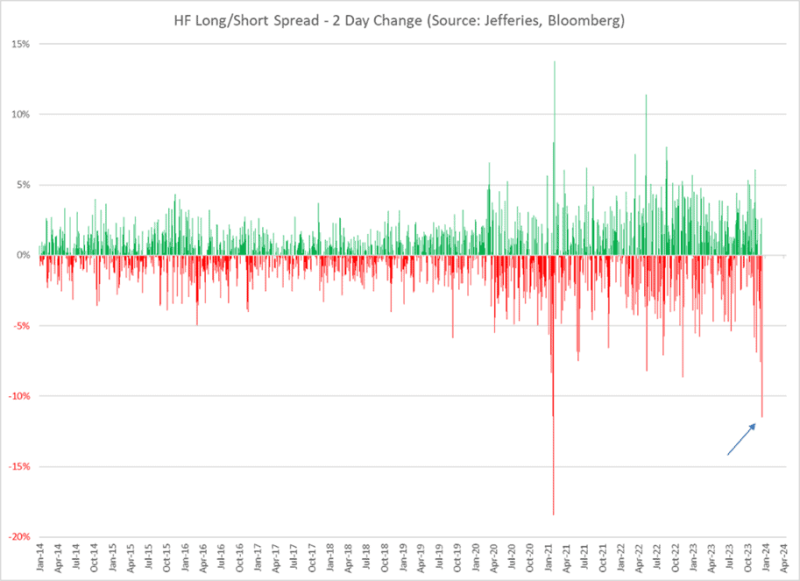

The Fed's clear change of tone created big losses in certain places. The difference between the returns of Jefferies' hedge fund clients' long and short positions was -11.5% over two days in December (13-14th)! The second worst performance in 10 years and only the time when Gamestop (remember the madness?) was up 355%in two days was worse.

Source: Jefferies, Bloomberg

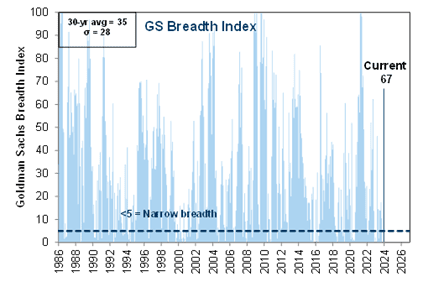

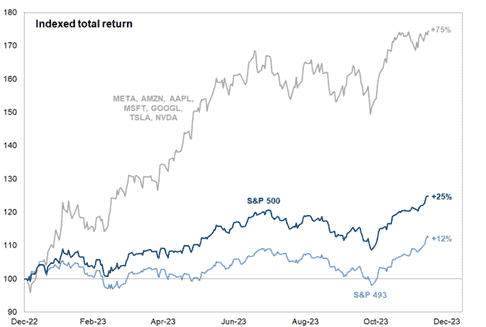

The breadth of the stock market improved significantly during the fourth quarter. In the US, the concentration was sky high with the big technology companies as the superior winners, but at the end of the year more stocks started to participate in the rise. In mid-December, the S&P500 rose for one day while all of the Magnificent7 fell. That had not happened since July 2022 and it was becoming increasingly clear that investors were beginning to change their minds about an imminent recession. The image below shows the Goldman Sachs Breadth Index for the US market. Corresponding developments were also seen in Europe.

Source: Goldman Sachs

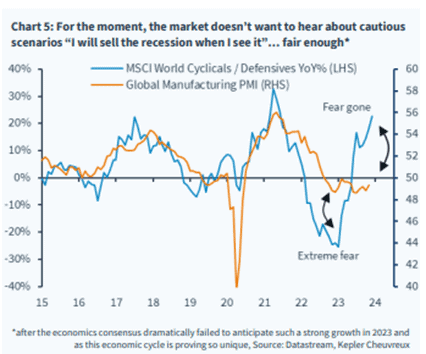

Investors continue to ignore weak activity indicators (PMI) and have increased sharply to cyclical companies at the expense of more defensive companies. Worth noting is that January 3rd this year had its worst cyclical day against defensive companies since August last year, but the year is still long.

Source: Datastream, Kepler Cheuvreux

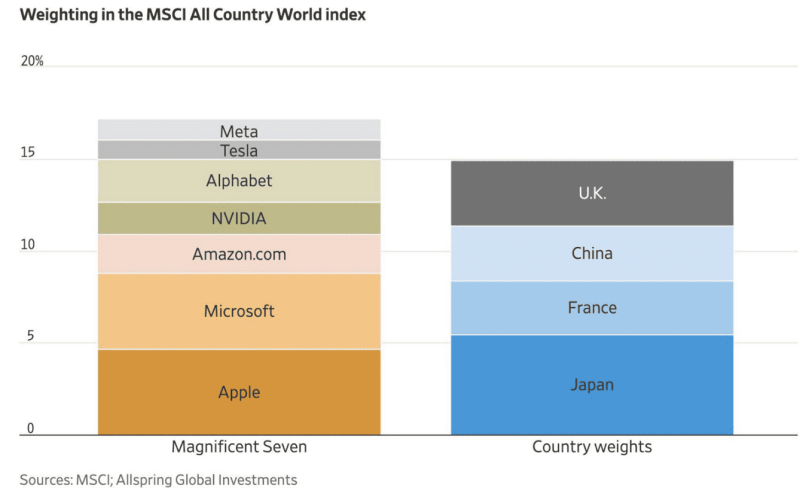

To put things in perspective. The image below shows the weight in the MSCI world index, for the large technology companies on the left and for some countries on the right. Apple's weight is almost as large as all the companies in Japan, and Alphabet's weight is roughly the weight of all the companies in Great Britain. Almost unimaginable.

Much has been written about the progress of the big tech companies in 2023 so we won't bore you too much, but they are important to the world's stock markets. Most people have probably forgotten that Nasdaq had a super-heavy 2022 with -33% in return. Viewed over two years, the recovery is almost perfect and complete, having risen by a whopping 43% in 2023, second best to the memorable 1999, and thus has had a positive return 14 out of 15 years. The total development since the financial crisis in 2008 is 1517%…

Source: Bloomberg

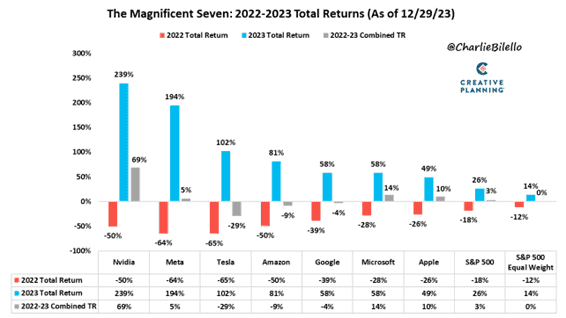

Same message broken down at company level. The return over two years feels more remarkable than last year in isolation. Collectively, over two years, the yield has been a modest 3.5%.

Source: @CharlieBilello

But 2023 was phenomenal for Magnificent7. A rarely seen concentration of returns from seven companies compared to the other 493 included in the S&P500.

Source: Goldman Sachs

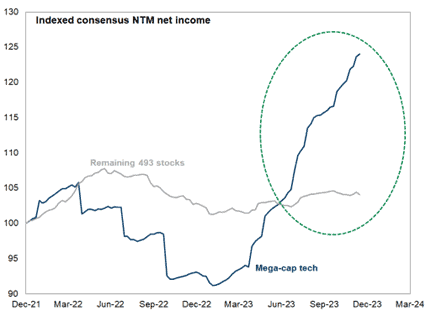

A large part of the explanation for the difference in returns is shown in the image below. Impressive to say the least.

Source: Goldman Sachs

We note that our view a year ago that the large technology companies were unlikely to deliver any significant returns in 2023 was completely wrong. Lucky that our focus is not American technology companies.

Despite all the drama and stress, the American 10-year treasury note closes at 3.87%, exactly at the same level as it was on the last day of the year in 2022! How is that possible? Almost like a bad movie and you do best to avoid thinking about all the stress caused by the development last year when the level was unchanged a year later.

Source: Bloomberg

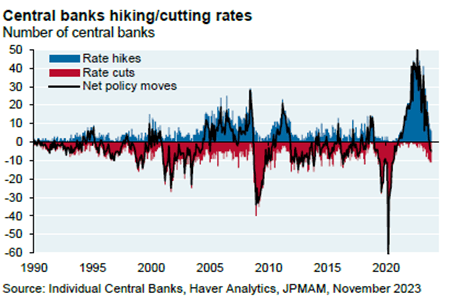

The war on inflation is over (at least for now). A razor-sharp image that captures much of the extreme drama we have all experienced in the past two years with historically very strong interest rate increases.

Source: Individual Central Banks, Haver Analytics, JPMAM

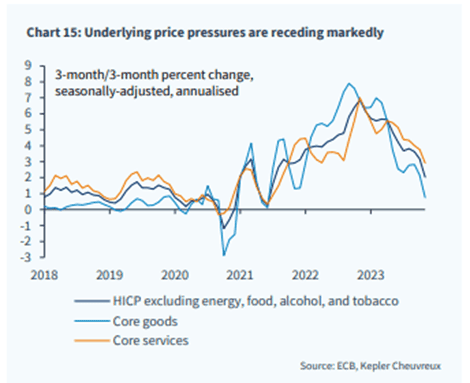

Price pressure falls significantly within the Eurozone.

Source: ECB, Kepler Cheuvreux

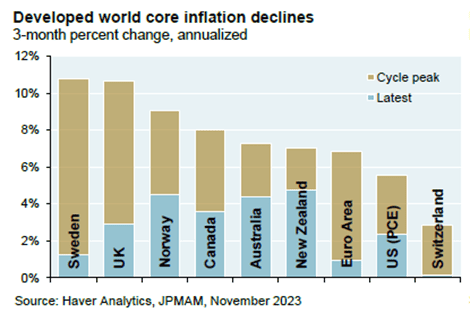

Falling prices lead to the next important picture that explains much of last year's strong performance in the stock market. In the US, we are impressed by the symbiosis between the Fed and the US economy. In Sweden, we can take our hats off to Erik Thedéen's work since he took office as Governor at the Swedish Central Bank. The starting position was grim, but most things have gone in the right direction. In most parts of the world, inflation continues to fall back and soon it is likely and hopefully close to the target levels.

Source: Haver Analytics, JPMAM

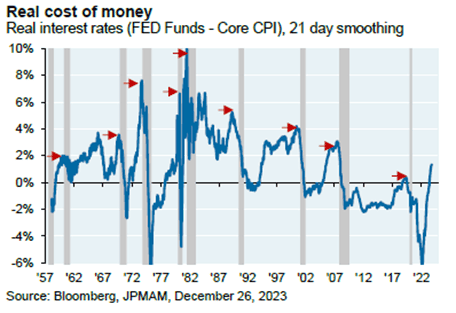

This has contributed to falling real interest rates. If one zooms out it shows that German real interest rates were in positive territory only for a short period. The German 10-year government bond is now below 2%, which is the same level as inflation expectations.

Source: Holger Zschaepitz

Illustrated differently and for the United States. Financial conditions have improved rapidly.

Source: Bloomberg, JPMAM

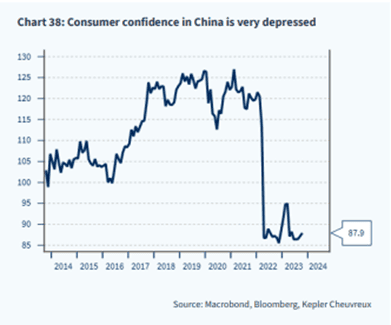

We must also mention China when summarising the past year. After a deranged Covid policy, the country finally opened up at the beginning of last year. Hopes were high for a kick start, but it turned out to be more of a melancholy deflation. Geopolitical tensions and all the logistical problems that arose as a result of the extreme Covid policy have brought China's growth to a standstill (by Chinese standards). Direct investment in the country has basically crashed and the political party is now whipped to speed up growth with various stimulus packages. Our simple assessment is that there is more upside than downside from here, but we take no active positioning based on that view. Within our portfolio LVMH is the company that benefits the most from increased economic activity in China.

Last but not least, there is activity in the French luxury and cosmetics sector. A new owner is on the way to Hermes! Nicolas Peuch, a childless 80-year-old heir to the Hermes empire, plans to adopt and then gift his 12 billion euro fortune to his 51-year-old gardener from Morocco. The Isocrates foundation that Peuch founded in 2011, which was supposed to promote good journalism among other things, opposes this, but seems to be advised to seek new sources of capital.

There was also news surrounding L'Oreal, where Francoise Bettencourt Meyers in December became the world's first woman to pass 100 billion euros in wealth. Her grandfather founded the company in 1909 and is undoubtedly one of Europe's most successful companies over many years. We recommend The Bettencourt Affair on Netflix.

If you, like Blackstone, are the world's largest asset manager with USD 1000 billion in assets under management, you a) have good self-confidence b) are self-deprecating and c) can spend time and resources to create the attached Christmas greeting https://www.youtube.com/watch?v=CbqqAAgN-dI

PORTFOLIO COMPANIES

Volution

In December, Volution released a financial update for the period August to November 2023. Organic growth was +3% compared to the previous year, which was better than the market expected. Three percent is a very strong figure given the company's high exposure to new construction and renovation. If Volution manages to grow in what is described as a very tough market – how fast can it grow when the economic situation normalises? The company also reported rising margins compared to the last accounting period. Strong price discipline, internal efficiency programs and a better product portfolio were cited as reasons.

Volution stock rose 19% in 2023 and remains one of the fund's largest holdings. We have great confidence in the company's management and appreciate the structural growth, the well-thought-out business model and, not least, the share's low valuation.

Rugvista

The Rugvista share rose 58% in 2023. It sounds like a high number, but you have to remember that the rate was very low at the beginning of the year. Today, the stock continues to trade significantly below its IPO price. The valuation remains low at around 10x EBIT for 2025 (our estimate). The company has made major improvements in a challenging environment and in the coming quarters we expect continued organic growth, mainly thanks to higher conversion rates. If we get our investment thesis right, the market should revalue the company upwards.

Accelleron

We rarely write about Accelleron. It is partly a function of the fact that the Swiss turbo engine company only reports figures every six months, and partly a function of the company's high degree of maturity: Accelleron is a stable player that should be able to grow organically by 2-5% per year with increased margins and strong cash flows. On top of this, there is an ambition to carry out acquisitions. A large proportion of sales come from the after-sales and are therefore defensive in nature. During the year, the share rose 37% in Swiss francs, or as much as 45% measured in euros, and was thus the fund's second best contributor in 2023.

SLP

The company carried out a rights issue on the last day of November, which affected the share price in the short term. This was regained with flying colors in December, when the share rose a whopping 17% and was thus the fund's second best contributor in December. Like other real estate companies, SLP will benefit from lower interest rates. If the company can grow the net operating income in line with its target of 15% and a return requirement that will gradually decrease, then we will see a huge result on the NAV. With strong cash levels and many investment opportunities, we are convinced that SLP is headed for a bright 2024. The stock rose 33% in 2023.

Corem

Corem became the fund's best share during the last month of the year with a rise of 20%. There have been no company-specific news that lifted the share. On the other hand, continued falling interest rates and, at least as important, that the main owner Rutger Arnhult bought a lot of shares. In addition to the usual positive signal value of insider buying, the effect here is double. The stock has for a long time been burdened by the fact that the main owner has been (or at least considered to be) under financial pressure. He probably isn't anymore, as the total purchase value for the businesses in December was around 850 million. On the other hand, there were two withdrawals from the letters of intent signed at the end of October. Financially, it was probably good for us as owners as they are in a completely different interest rate situation. Despite an increase of 34% in 2023, Corem is still traded at around a 50% discount to NAV.

Cargotec

Cargotec shares continued their journey upwards during December, closing the month at +14%. The subsidiary, MacGregor, continued to receive significant orders during the month and the valuation remains low. On our estimates, the EV/EBIT valuation is 7x on 2025 figures. As we previously wrote, there are several triggers in 2024 which will hopefully mean that the company continues to be valued by the market. Since we wrote two months ago that the valuation was so low that "it's almost hard to believe it's true", the share has rebounded around 50%. The stock rose 27% in 2023.

Bonesupport

Bonesupport was once again a strong contributor to the fund in December, but it was also the fund's best stock in 2023. It was also the best performing stock on the Stockholm Stock Exchange last year. When we did our initial analysis and met with management, there was no doubt that the stock would be higher, the only question was how quickly the revaluation would happen. It is difficult to find anything to complain about in terms of the company's delivery over the past two years.

The launch of Cerament G in the US exceeded not only our expectations, but also the company's own. At our initial investment, our sales estimates for 2025 were more than 50% higher than consensus. Now the market has caught up and the share rose a whopping 134% in 2023. With a rising valuation, the burden of proof on the company increases, but we still believe that the market underestimates the company’s long-term potential. Without any vivid imagination, one can see the company's turnover of 5 billion within 10 years, which implies a turnover growth of 20% per year starting in one year. It does not feel aggressive given all the new markets that will be successively available and new indications. Given the above conditions, we still believe that Bonesupport will be a winner on the stock market, albeit at a more modest pace going forward. We present below a graph.

Source:Bloomberg

SUMMARY

Another intense year is now behind us. We experienced a short but intense American banking crisis in March. A China that opened up after the pandemic, but whose economy did not recover. For the first time in over 20 years, returns were negative on the Chinese stock market for three consecutive years.

In Europe, Greece (+44%) was the best stock market after Italy (+32%), where Greece has shown the strongest GDP growth in Europe in the last two years. Who would have thought? In the US, the housing developers were the real winning sector with 82% in return. In Europe, the best sectors were retail, construction-related companies and technology. Probably also surprising to most.

Geopolitically, the curtain was firmly closed with Russia's brutal assault on Ukraine and October 7th, unfortunately, will forever be associated with Hamas's horrific act of terror against Israel.

The starting position, a year ago, was inflation which was around the highest levels in several decades. Interest rates skyrocketed and in Europe the energy crisis was a reality. In the US, the Nasdaq had just finished 2022 with -33% and investors were more or less wounded.

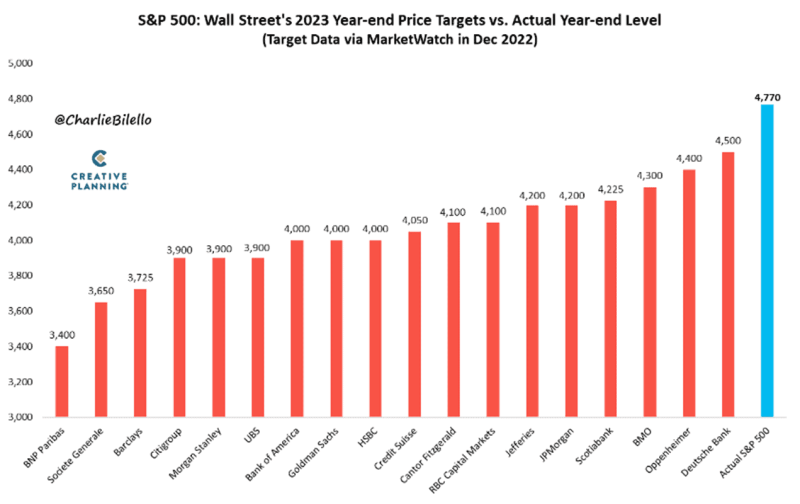

12 months later, it can be stated that the outcome for 2023 was significantly better. Below are a number of well-known strategists' target price for the S&P500 at the end of 2022. Everyone was too cautious as the outcome was a whopping 18% better than the average forecast.

Source: @CharlieBilello

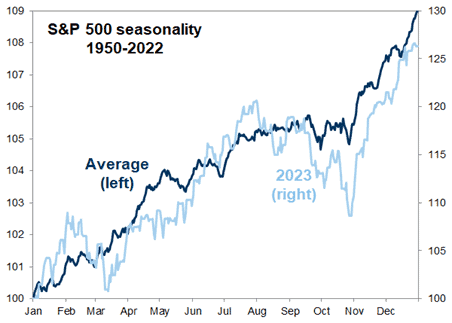

The year ended as usual. We have had the below picture here for the last two months and it was an exceptionally good time to increase the risk at the end of October. Something we did and one of the reasons for our strong end to the year.

Source: Goldman Sachs

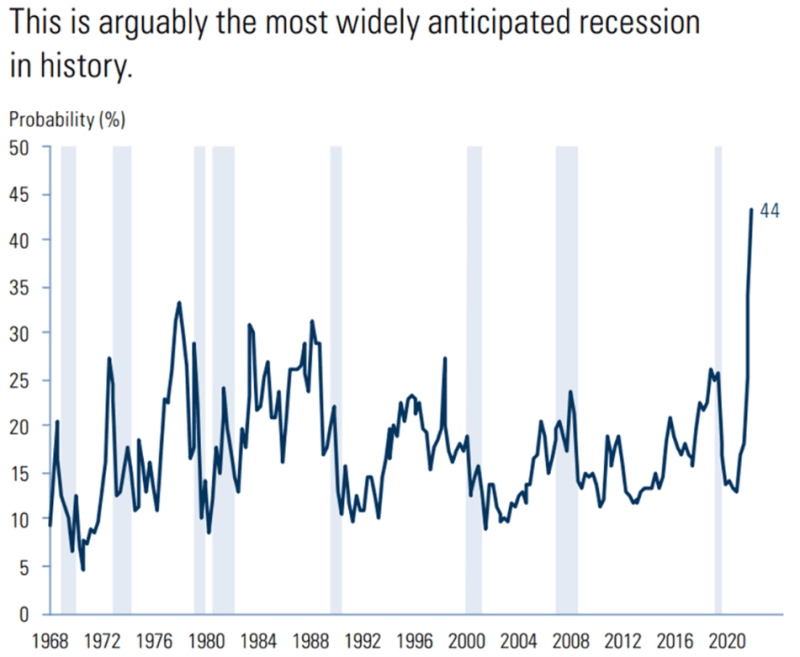

For about two years, the market has been waiting for an American recession, which still hasn't happened. The most anticipated recession ever? 44% expected a US recession a year ago. The corresponding estimate today is around 50%, but will likely (in our view) drop in the coming months. The US economy has once again surprised in an impressive way to say the least. Here and now, it can be stated that the market was once again absolutely right.

Source: Goldman Sachs

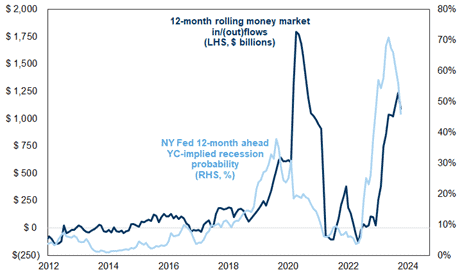

The cautious view of the economy has led to huge inflows into money market funds.

Source: Goldman Sachs

The inflow into equity funds has been considerably less despite a strong development last year. The lowest in four years.

Source: Goldman Sachs

That should mean investors still have plenty of capital left to put to work when the time is right. The last time when inflows to money market funds sharply reversed was 2009, which was a very strong year for the world's equity markets. It was followed by more outflows in 2010 and 2011. The probability that we will see corresponding outflows in 2024 flowing into the equity markets feels high. Despite a strong last quarter in 2023, one can hardly discern any change in the pace of deposits, see the image below.

Source: Goldman Sachs

In addition to available capital as stated above, the image below is also interesting for understanding the starting position. It shows the exposure of Goldman Sachs clients to smaller companies, and it is clear that it is very low. Despite a strong end to the year, our assessment is that a large part of available capital is outside or has low exposure to this asset class. Historically, smaller companies have always had a strong development when inflation and interest rates fall.

Source: Goldman Sachs

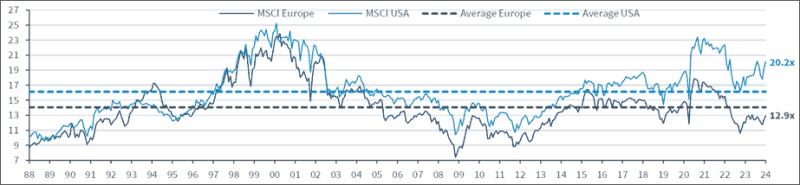

So after updating capital flow and positioning, what does the valuation look like? The image below shows the difference in valuation between the American and European stock markets. Barely P/E 13x for 2024 in Europe hardly feels challenging and is clearly below the historical average level.

Source: Kepler Cheuvreux

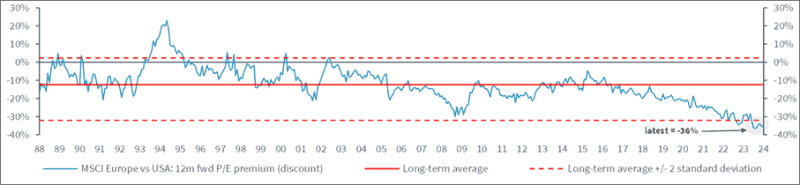

The difference in valuation between the American and European stock markets is at a record level and increased further last year, mainly because Europe does not have any defined AI companies. That there is a very large difference even after removing technology and other sectors is easy to see when BP and Shell are traded at P/E 7x 2024e while Exxon and Chevron are traded at 11x.

Source: Kepler Cheuvreux

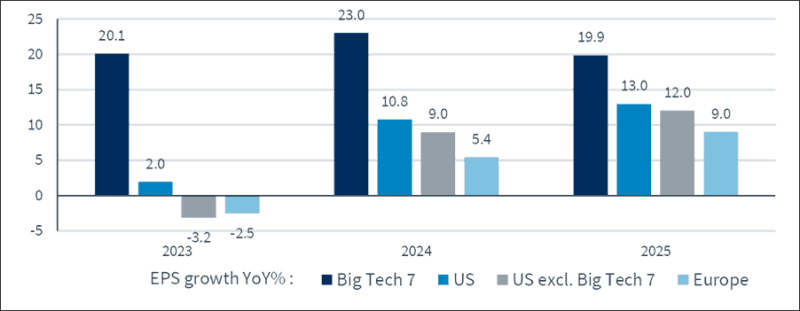

The biggest explanation for the valuation difference between the US and Europe is profit growth, see below.

Source: Kepler Cheuvreux

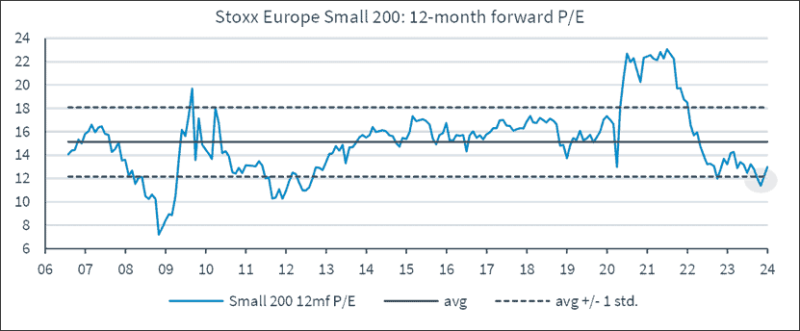

The valuation of European small caps rose slightly at the end of last year (P/E 12.7x), but remains below the historical average and should rise 30% to reach pre-Covid levels.

Source: Kepler Cheuvreux

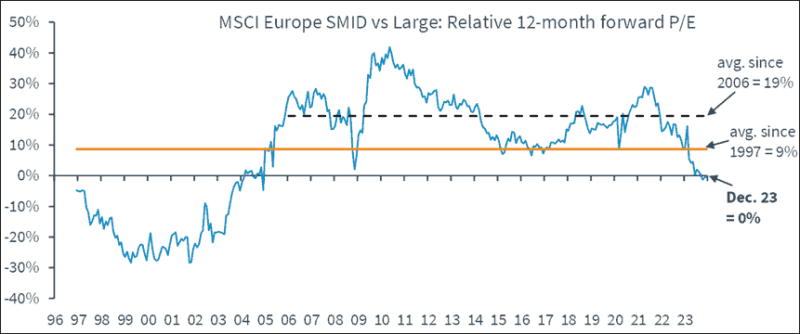

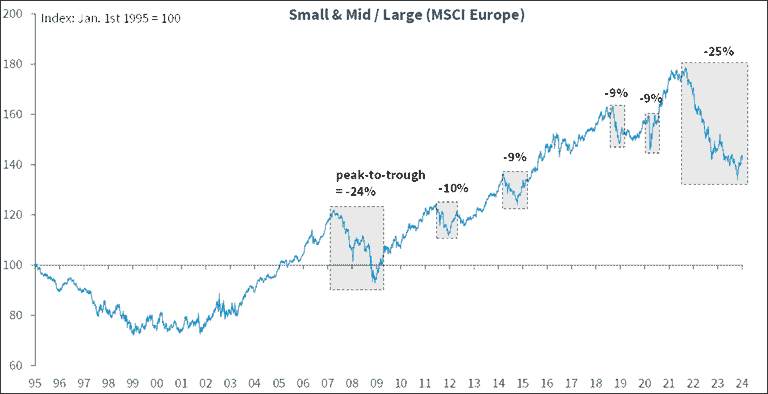

The European small companies have not been valued so low in relation to the larger companies in 20 years.

Source: Kepler Cheuvreux

So the starting point for the new year is as follows:

• The odds for a reversal of flow from money market funds to equity funds during the year are considered good.

• The positioning in small companies as an asset class is low.

• European companies are trading at a record discount relative to American ones.

• European small caps are trading relative to larger companies at their lowest level in 20 years.

Conclusion: The starting position looks attractive.

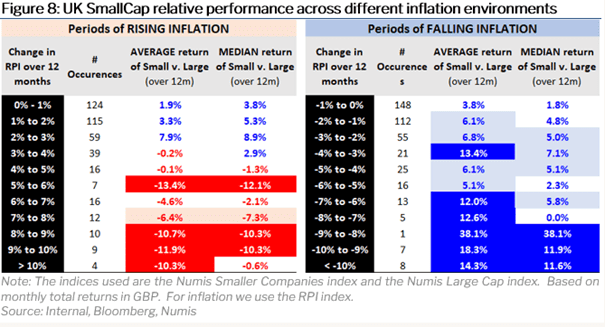

We take the liberty of copying one of last year's best images which we featured in our letter two months ago. How have smaller companies developed in different inflation scenarios? Historically very good and we are now experiencing a historic decline in inflation. We have endured 22 months of rising inflation and now know what that meant and we got a taste of the opposite in November and December.

Source: Bloomberg, Numis

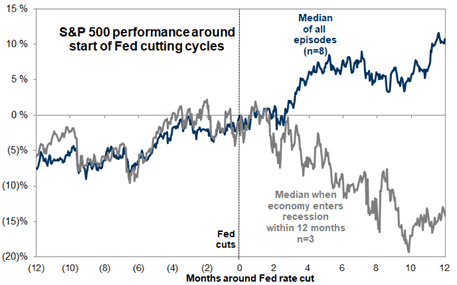

How has the S&P500 performed as the Fed begins to cut interest rates. It depends very much on whether there will be a recession or not. Our basic view remains positive, insofar as we do not expect any deeper recession in the economy.

Source: Goldman Sachs

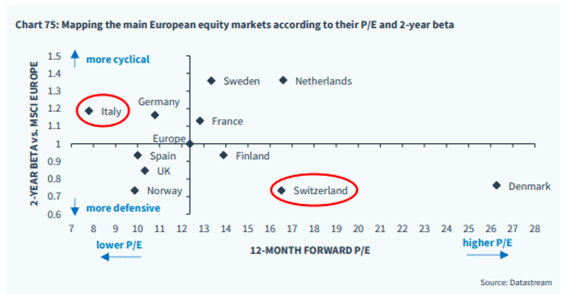

Below is an overview of the valuation and beta of the various European markets. Denmark stands out because of Novo Nordisk's weight in the index.

Source: Kepler Cheuvreux

The new year has started on a weak note but as we have just completed nine positive weeks in a row, you probably shouldn't rush to conclusion after only two trading days. We had to wait for over a year until we got a new high on the leading exchanges. In the United States, it has happened 14 times since 1954, and after such an event there has often been a tepid development in the short term, but after a year the median return has been just over 13%(13 out of 14 occasions).

Geopolitically, it looks worrying and the risks are probably greater today than in any other post-war year. According to themselves, Israel is now under attack from seven different directions: Gaza, the West Bank, Lebanon, Syria, Iraq, Yemen and Iran. The common denominator and major sponsor is Iran. Putin's barbarism continues and we hope and believe that the West will continue to pump resources into Ukraine. In addition, it is a super election year when half of the world's population goes to the polls. The election in the USA in the autumn will of course be the most interesting.

Our conclusion is, all in all, and despite the geopolitics, that we are likely facing a decent stock market year. This applies above all in the areas of stock picking and small and medium-sized companies, our core business. The image below shows the relative valuation for small and medium-sized companies that continue to trade at, historically, very low levels.

Source: Kepler Cheuvreux

We don't expect a recession, at least not a deeper one, and then the P/E of 13x for the European stock market is cheap. Falling interest rates and inflation will make people happier, not least in Sweden, and economic activity may start to pick up in a few quarters.

We are thankful and appreciate the interest shown and for all the support during the last year. Onwards and upwards!

Mikael & Co

Malmö January 8th, 2024