Before making any final investment decisions, please read the prospectus, its Annual Report, and the PRIIP of the relevant Sub-Fund here

This material is marketing communication

An article underscoring the challenges and future opportunities in offshore wind.

Offshore wind technology plays a pivotal role in the drive to decarbonize our electricity supply. Although it today generates less than 1% of total electricity production, there is an ambition that it should account for approximately 15% of a much larger total electricity production in 2050.

Governments on both sides of the Atlantic have optimistic capacity targets. The EU Commission’s latest is for installed offshore wind capacity to grow from 16GW in 2022 to as much as 111GW in 2030 and 300GW in 2050. In the US, the Biden administration is targeting 30GW in 2030, up from a paltry 0.1GW generated by only seven turbines last year.

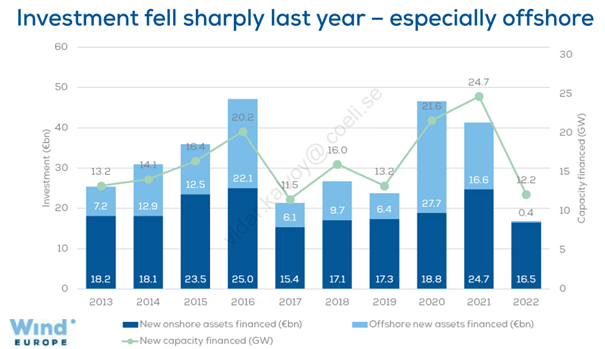

However, despite the increased urgency following the Russian invasion of Ukraine and the skyrocketing energy prices, investments in wind capacity, particularly offshore, slowed down significantly. As can be seen from the graph below from Wind Europe, a European industry lobbyist, offshore wind investments were virtually non-existent last year.

To make it worse, the wind developers are also trying to renegotiate previously entered contracts that are no longer profitable. Last month, Vattenfall, Sweden’s largest utility, decided to suspend development of its UK Norfolk Boreas 1.4GW offshore wind farm. It will impair the project by as much as SEK 5.5bn (USD 520m) as development and capital costs have soared since it won the tender only a year earlier.

Similarly, in the US, Iberdrola, through its subsidiary Avangrid, recently paid a USD 49m penalty fee to exit a 1.2GW offshore wind program in Massachusetts. Bloomberg New Energy Finance (BNEF) calculated that the levelized cost of energy (LCOE) for the project has increased by 48% from the time it was signed in 2021. The investment tax credit in the meantime increased from 30% to 40%, but without this lift, the LCOE would have increased by as much as 57%.

It is evident that wind fundamentals have deteriorated despite improved government incentives. The main problem for all developers is the soaring cost inflation in the wind supply chain. Post-pandemic, prices for steel, labour, and transportation have surged, adversely affecting anticipated internal rates of return (IRR). The second problem is the increased funding cost. Offshore wind projects are very capital intensive with most of the capex upfront. With aggressive interest rate hikes over the past 18 months, projects grapple with greater interest payments, and the weighted average cost of capital (WACC) has risen with an elevated risk-free rate.

The difference between the expected IRR and the WACC is the profit for the developers. This spread is likely negative for some offshore wind projects entered into in 2020-2022, which often, but not always, means that it is better to write off the loss and exit the project.

To top it off, the industry in Europe also suffered from regulatory uncertainty in 2022. As power prices spiked due to the Ukraine war, European politicians introduced wind-fall taxes on renewable energy to subsidise energy demand, often generated by fossil fuels. Although the final tax burden was relatively small in the end, it sent a signal to the industry that the regulatory framework is uncertain and could be swayed by populist politicians. The risk premium in the cost of capital must go even higher.

While the wind sector seems inundated with discouraging news and headwinds, there are however glimmers of hope and signs of some tailwind.

First, we believe it is positive for the industry that developers chose to write off costs and pay exit fees rather than continuing with unprofitable projects. Most of the developers with projects facing negative profitability will try to renegotiate the existing contracts, which we believe will have mixed success, but we are confident this will help accelerate the recalibration of price expectations on future contracts. In fact, according to LevelTen Energy, a renewable energy consultancy, the average purchasing power agreement (PPA) for offshore wind is up as much as 85% since 2020.

Second, although Vestas, the largest wind turbine installer, increased prices on new orders by 20-30% year over year for three quarters in a row, the average selling price have stabilized in the last two quarters. Steel and other commodity prices have also decreased and supply chain issues that impacted margins for both turbine manufactures and the developers in 2022 are in the rear-view mirror.

Third, there are also regulatory tailwinds. We have in previous monthly reports discussed the strong focus on speeding up permitting for renewable projects. Considering that a typical wind project takes nine years, with only two years dedicated to construction, faster permitting could speed up projects significantly and boost projects profitability.

On that note, Germany has taken the lead in making the new EU regulation agreed upon in January this year into national law. Some of the most important changes are the introduction of a two-year binding deadline for permits, expedited permitting in designated 'acceleration areas', and a digitalisation requirement for a process that remains largely paper based. This has already resulted in 65% more permits issued in Germany in Q1/23 than in the first quarter of 2022 and 2021. The other EU nations are expected to introduce similar regulations in the forthcoming months.

Similarly, in the US, the Federal Energy Regulatory Commission (FERC) some weeks ago issued a sweeping new rule aimed at speeding up permitting for interconnection to the US power grid, a very important development for all renewables including offshore wind. We discussed this in our march-23 monthly report ‘Grid connection the next bottleneck?’ and expressed that we were hopeful this reform would be implemented.

The essence of the new rules is that projects will be assessed on its readiness and not when it entered the queue. The US will go from ‘first come, first serve’ to ‘first ready, first serve’. The new framework also imposes penalties on developers for retracting speculative projects, potentially reducing future wait times. Simultaneously, FERC will penalize transmission providers failing to complete timely interconnection studies. This reform marks one of the most substantial shifts in FERC's near half-century history. As of the close of 2022, over 2000GW of generation and storage projects awaited connection, equivalent to the entire existing US power generation capacity. Clearly, an accelerated permitting process that trims years of development will boost profitability (IRR), reduce the uncertainty (lower cost of capital) and result in more value creation for the developers.

Finally, a last positive factor worth mentioning is that most European countries are moving to contract for differences (CFDs) as the favoured method for awarding offshore wind projects. CFDs ensure a fixed price for developers; when spot energy prices exceed this rate, the excess is returned to the government, but if prices drop below, the shortfall is covered by the government. Essentially, the government absorbs the price risk and the developer bear the volume risk.

Wind Europe, a wind lobbyist, has calculated that in today’s debt market a typical project's breakeven might be EUR 92/MWh, but it would drop by almost 80% to EUR 50/MWh if the price risk was carried by the government. This should be a low hanging fruit for any country keen on expanding offshore wind capacity.

To sum up the potential tailwinds, as price expectations are reset higher and developing costs are declining, developers’ profitability (IRR) on new projects is likely to improve. IRRs will be further boosted by accelerated permitting reducing the development time of projects. Funding costs will come down as CFDs become the preferred way to award government contracts. If forecasts about the FED slashing interest rates five times next year are accurate, we can anticipate a further drop in capital costs for upcoming projects, enhancing the cash flow value of future offshore wind projects.

Certainly, it will take some time before you see the effect of higher prices, lower funding cost and faster permitting in the accounts of the likes of RWE (RWE GR), EDP RENOVAVEIS (EDPR PL) and Orsted (ORSTED DC). However, as the stock market’s current valuations assigns limited value to any capacity growth, we believe the risk reward of investing in this area is improving.

Joel Etzler

Portfolio Manager Coeli Renewable Opportunities

- Portfolio Manager Coeli Renewable Opportunities

- Joined Coeli in 2019

- More than 13 years of experience from the financial industry

- MSc from the Royal Institute of Technology

Joel Etzler is Portfolio Manager and Founder of the Coeli Renewable Opportunities fund and has more than 13 years in the industry, with investment experience from both the public and private equity side. Etzler joined Kalvoy at Horizon Asset in London in 2012 and spent five years before that within Private Equity at Morgan Stanley. Etzler started his investment career within the technology sector at Swedbank Robur in Stockholm, 2006.

Vidar Kalvoy

Portfolio Manager Coeli Renewable Opportunities

- Portfolio Manager Coeli Renewable Opportunities

- Joined Coeli in 2019

- 25 years of experience from the financial industry

- MBA from IESE, MSc from Norwegian School of Economics and Business Adm.

Vidar Kalvoy is the lead Portfolio Manager and Founder of Coeli Renewable Opportunities fund. He has 25 years of experience from portfolio management and equity research. For nine years he was responsible for the energy investments at Horizon Asset in London, a market neutral hedge fund. Kalvoy also did energy investments at MKM Longboat, another hedge fund in London. He started his financial career as a sell side equity research analyst focusing on the technology and telecom sector, working six years in Oslo and Frankfurt. Prior to working in finance, he was a second lieutenant in the Norwegian Navy.