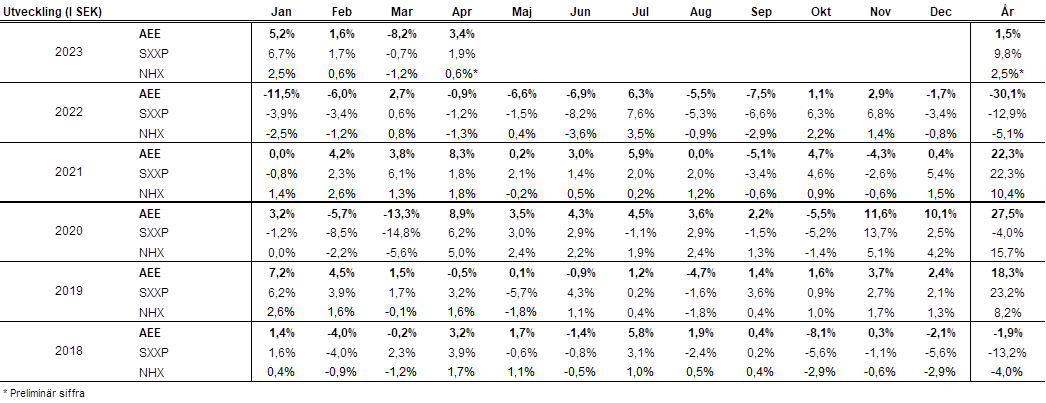

Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class' return. The information below regarding returns therefore differs from the returns in other share classes.

Before making any final investment decisions, please read the prospectus, its Annual Report, and the KID of the relevant Sub-Fund here

This material is marketing communication

Monthly Newsletter Coeli Absolute European Equity – April 2023

APRIL PERFORMANCE

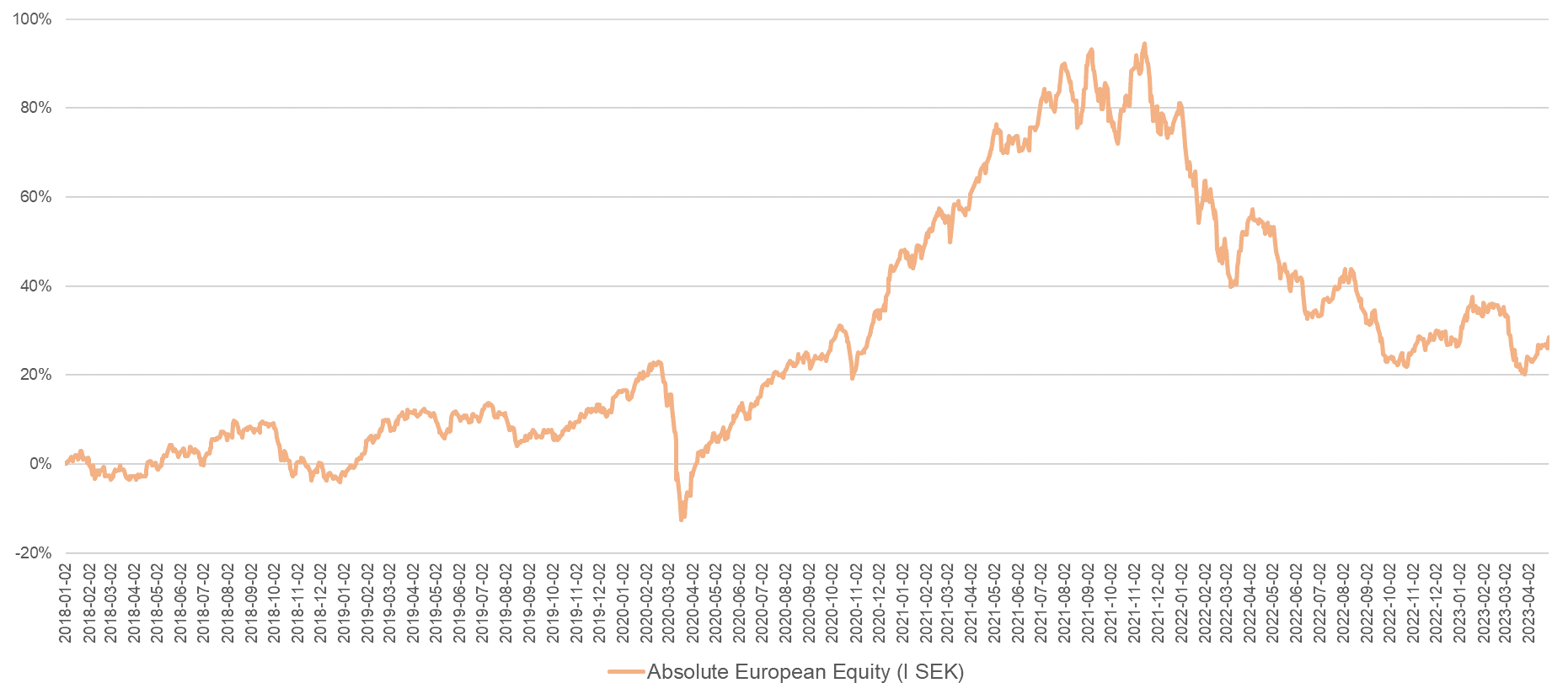

The fund’s value increased by 3.4% in April (share class I SEK). The Stoxx600 (broad European index) increased during the same period by 1.9% and HedgeNordic’s NHX Equities increased provisionally by 0.6%. The corresponding figures for 2023 are an increase of 1.5% for the fund, +9.8% for the Stoxx600 and +2.5% for NHX Equities.

EQUITY MARKETS / MACRO ENVIRONMENT

The world's stock markets came up for air again after the banking turmoil, temporarily, subsided. Apart from that it was unusually quiet in terms of major macroeconomic news, which was appreciated by the world's investors. The broad European index rose 1.9% in April compared with the S&P500, which rose 1.4%, both in local currencies. Measured in euros, the S&P500 was unchanged and the European stock markets continue to develop stronger than their American counterparts. The fund rose by 3.4% and several positive company news contributed to the good performance, more about that in the long positions section.

Our thesis last month that the reporting season would be strong has so far played out. Large companies such as LVMH, Hermes, L'Oreal, BASF, Volvo, Atlas Copco and several European banks all came in with very strong reports.

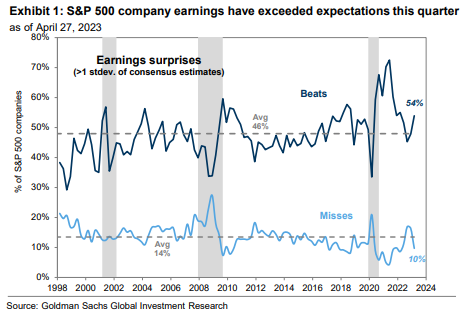

In the US, expectations were low with consensus expecting a seven percent drop in profits for the first quarter. After 64% of companies reported, 54% of companies have surprised positively, which is above the historical average of 46%. Both turnover and margins have been better than expected and the profit reduction is at the time of writing minus five percent.

The best sector in Europe in April was real estate, which rebounded by 5.2% after a weak development last month. The fund's two investments in SLP and Corem participated in the rise and increased by 10 and 12% respectively. The bank index rose by just over two percent and the worst sectors were technology and raw materials, which fell by around five percent.

Source: Bloomberg

"The banking crisis is over". Politicians and bank CEOs have been vocal in the media in recent weeks saying that the problems with the American smaller banks were a temporary blip and that it is now behind us. In the past week, it was the managements of BNP Paribas, Nordea and Standard Chartered who proclaimed it. On May 1st, US authorities approved JP Morgan's purchase of troubled First Republic, which is arguably a big step in the right direction. Admittedly, he speaks for himself, but when CEO Jamie Dimon says “the system is very, very sound" and "this is getting near the end of it", you listen a little extra. Obviously not everyone did. On Tuesday, May 2nd,several regional banks came under renewed pressure with large declines as a result. It would be strange if three out of 4,600 regional banks failed while 4,597 escaped unscathed. The probability that the Fed's aggressive interest rate hikes left a deep impression on several banks' balance sheets is probably high, and tonight there will be another expected increase of 25 basis points.

The tougher conditions for the American banks are now reflected in less lending. Lending is likely to slow down considerably in the coming quarters (forecast blue dashed line) and the banking crisis has likely removed, at least, one interest rate hike from the Fed.

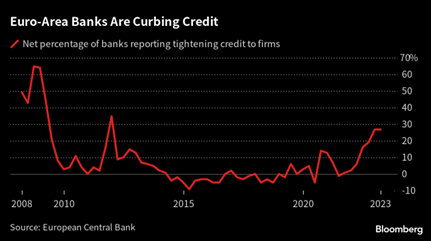

On Tuesday, May 2nd, the ECB published statistics showing that European banks also saw a clear slowdown in new credit. The sharply rising interest rates are now leaving increasingly clear traces in the economy, and continued falling inflation will lead to falling interest rates. The picture below shows the percentage of banks that have tightened corporate lending.

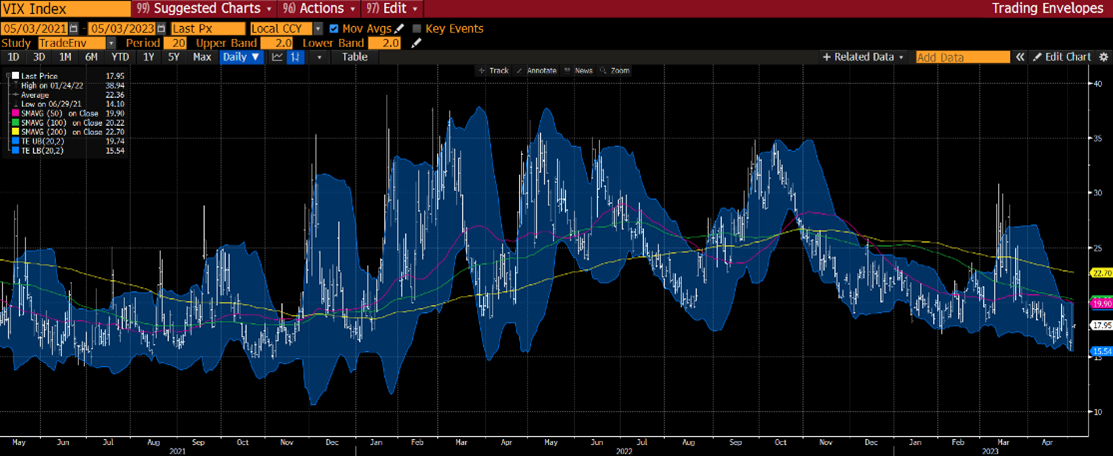

The volatility index, VIX, is at surprisingly low levels considering all that is happening on both the macro and micro levels. However, the bank stress in March is clearly visible.

Source: Bloomberg

The Riksbank (Swedish Central Bank) raised the interest rate by a further 50 basis points in April, and the key interest rate is now 3.5%. There was no clear agreement as two of the members wanted to increase by only 25 basis points. The image above and below reinforces our view that the Riksbank should hold off on further interest rate increases and give the process more time to study how much inflation slows down with interest rate increases that have already been made.

Below is a fascinating and positive picture of Swedish PPI since 1976. The price that is measured is the price that Swedish producers receive when they sell their product versus the price that the buyer pays when the products enter Sweden. A genuine collapse that will eventually filter down to the consumer level.

Source: Bloomberg

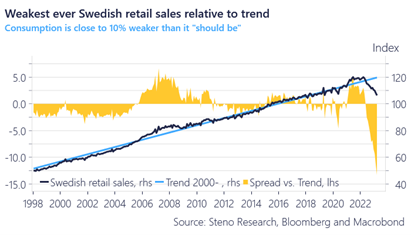

Swedish consumers are on their knees. Unlike both American and European consumers who have started to wake up, Swedish consumers are still experiencing what could be called a perfect storm. The latest data point shows that Swedish consumption is approximately 13% below the long-term trend line. These are very dramatic deviations.

The money supply in Sweden is decreasing at a rate rarely seen. The development looks about the same in the US and it is likely a major contributor to the bank stress we have seen in recent weeks. If inflation follows the development of the money supply with a certain time lag (as it has done historically), inflation will soon drop sharply.

As we mentioned a few months ago, the tone regarding the US debt ceiling is now starting to increase in intensity. We note that CDSs on the US government have risen very sharply in a short time, i.e., the cost of insuring against the US government going bankrupt has risen. If the politicians do not resolve the situation soon, for example, hundreds of thousands of government employees may soon risk not getting their salary paid. The last word has not been said in this drama and we will have reason to revisit it soon.

Source: Bloomberg

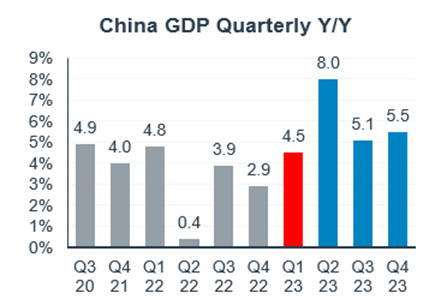

A little more cheerful tone from China, which in April published a strong Q1 GDP figure and activity data for March. GDP rose by 4.5% y/y (consensus: 4.0%) while inflation is below 1%!

Source: Kepler Cheuvreux

President Macron and Ursula von der Leyen made a joint visit to China during the month and met President Xi Jinping. Much of the meeting was about Ukraine and how the situation should be resolved – the outcome was poor. China has not condemned Russia's terrorist acts and wants peace through negotiating with Ukraine giving up some territorial areas. Ukraine refuses to give in for good reasons. In the coming weeks, a major offensive from Ukraine is likely to take place with the help of an enormous number of new weapons that have just arrived from the West.

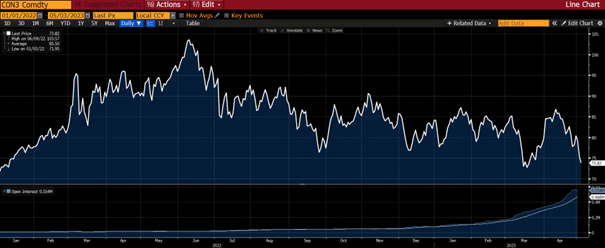

OPEC had a meeting on April the 3rd where they surprised the market with new production cuts. Oil rose 6% that day but is now, a month later, lower than before the meeting. Certainly, both surprising and annoying for the oil producers, but good for their customers and inflation.

Source: Bloomberg

Long positions

Bonesupport

After, in our opinion, an unwarranted 20% loss after last quarter's report, there was a cascade of upgrades from analysts ahead of the 2023 first quarter report. Despite inflated expectations, the company came in with a really strong report, which sent the stock up another 6% on the day of the report. Sales came in 10% higher than expected and the company showed a profit for the first time. Turnover grew by 66% (!) adjusted for currency, an unparalleled feat. The highlight of the report was that Cerament G is growing strongly in the USA, where the product was recently launched. In five months, the product already sells for SEK 50 million in the US, rolling 12 months.

We wrote in the September 2022 monthly newsletter that we thought the market underestimated the opportunity which had opened-up in the US. So far, we have been right given how the revisions to the estimates have been. We also hope that the market begins to realize the elegantly designed business model that enables this growth as well as the possibility of rolling out new products through the same channel. Europe (which almost gets a little forgotten in the context) is slowly but surely starting to loosen up after being heavily affected by the pandemic. During the first quarter, the company grew in Europe 32% in a constant currency context. We continue to like Bonesupport and follow its journey.

SLP

Our favorite little real estate company reported their Q1 results in April, and they delivered, in our opinion, the sector's strongest quarterly report. The company released a report which, despite increased yield requirements (+20 basis points), had positive value changes on the properties because of positive net letting, off-market acquisitions and higher rental income. The management result came in well above expectations and grew 35% compared to last year. This year, the company has acquired properties for just over 1 billion. SLP has a strong balance sheet and is one of the companies that could take advantage of the stressed situation in the real estate sector and acquire at a good yield. The company trades at a premium of 18% to the latest reported NAV, but we believe that the valuation will fall quickly as the company grows. On May 3rd, the company announced and carried out a directed issue of 550m to a limited number of institutional investors. The price was SEK 25 per share to be compared with the latest NAV figure of SEK 22.40, so an immediate value creation. The next step will be to acquire properties at attractive levels from stressed sellers. To be continued.

Corem

Corem's report came in slightly better than expected on underlying operating results and the stock was basically unchanged on the day of the report. So far this year, the company has sold properties for SEK 7.6 billion, most of them at book value, which is a brilliant deal for shareholders when the stock trades at a 68% discount to NAV. Financial aspects aside, the operating net number was strong, and the company also had a positive net rental in the quarter of 33m. This suggests that the underlying business is still fit and healthy. Interest costs were somewhat higher than expected. This was a theme we saw in several real estate companies. The company announced that it will continue to sell real estate and the sales it made this year are enough to cover bond maturities in 2023. After all the sales at attractive prices, Corem controls its financial situation better and can hopefully enter a calmer phase.

Sedana Medical

After an incredibly tough 2022, 2023 has started out more promising in terms of share price after a rise this year of 37%. The report for the first quarter of 2023 proved that Sedana can grow again. In the first quarter, the company beat expectations when sales grew by 5% organically, despite the market still being difficult in many geographies. The new management has also done a good job of cost control.

Much of the equity story for Sedana Medical is about the USA, where a market launch is expected in the first quarter of 2025. At the same time, we believe that the European launch has clear relevance for the USA - if you succeed in commercializing the product in Europe, you increase confidence that you can succeed with the same thing on the other side of the Atlantic. With the new management in the company, we feel secure that Sedana's organization has changed to be more commercial. The share rose 20% in April and made a nice contribution to the result despite the small position size at entry.

CVS Group

During the month, we received a nice contribution from the British veterinary company CVS Group, which rose by 14%. To be honest, it wasn't really the company's merit. Essentially, the price reaction came from EQT making a bid at a 51% premium for Dechra Pharmaceuticals, a British pharmaceutical company focused on animals. Although CVS Group is hardly in the business of drug development, the bid clearly gave a boost to the sector that spilled over to CVS Group's share price.

LVMH

In April, LVMH reported that it once again released a fantastic report, which sent the stock up 6%. YTD, the share has risen a whopping 28% and the market capitalization passed 500 billion euros for the first time ever for a European company. Acceptable.

Sales came in about 6% higher than expectations, driven by significantly better organic growth than forecasted. Concerns about a weaker China and general macro worries were as if blown away, especially when the company confirmed that the strong development was expected to continue.

Kion

Kion, where we have been invested since the beginning of the year, had a reverse profit warning during the quarter. This is especially pleasing as Kion is a German, very cyclical company and is undergoing extensive restructuring after a challenging 2022 to say the least. Operating profit for the first quarter was approximately 30% above consensus and the full-year forecast was revised upwards. The major part was driven by the ITS (industrial trucks segment) because of simplified supply chains and better operational mobility. The free cash flow was also better than expected, which is an important part of the equity story. Their other segment SCS (the service segment) is still weak, but the full-year forecast is maintained and there are hopes that things will ease towards the end of the year and that the company will measure against simpler comparative figures. After completed upward adjustment, the company is valued at approximately 9x P/E 2024e, well below the historical average of around 15x.

Short positions

The short portfolio contributed with a small negative result during the month. The main drivers for the negative result was our short positions in a Swedish small company index and on the Swedish OMXS30 index.

Exposure

The net exposure, adjusted for our unlisted holdings, at the beginning and end of the month was 76% and 77% respectively.

Summary

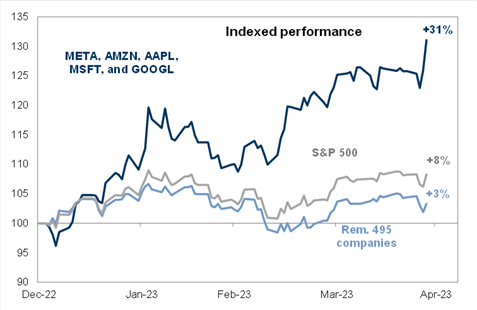

After the first four months of the year, it can be concluded that European stock markets continue to develop stronger than the American ones and the beginning of the year relative to the USA is the strongest since 2012. What is astonishing in the USA is the concentration of the rise with a very strong price development for the five major technology companies. The month's picture below shows that they rose on average by 31% compared to the other 495 companies that only rose by 3%. Measured in euros, the development for the 495 companies is plus or minus zero so far.

Source: Goldman Sachs

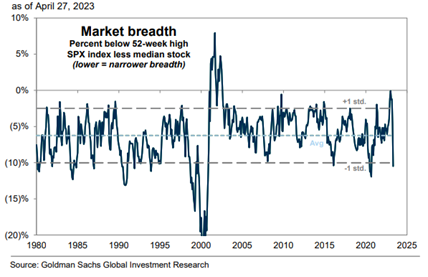

The image below shows the breadth of the market. The lower the curve, the fewer companies that are behind the development of the index. Only 11 times previously in the past 43 years has the index been so dependent on so few stocks. All other things being equal, this means that the upswing is fragile, and this can have a negative impact on future development. On nine occasions since 1980 (out of the 11), the development in the subsequent time period has been lower than the average.

In Europe, one of the big positive surprises has been the strong reports from industrial companies which included healthy increasing order books. Gloomy investors had low expectations going into the report season, and the fact that Sweden's most valuable company, Atlas Copco, rises by a whopping 15% on report day, says a lot about investors, analysts, and the company itself.

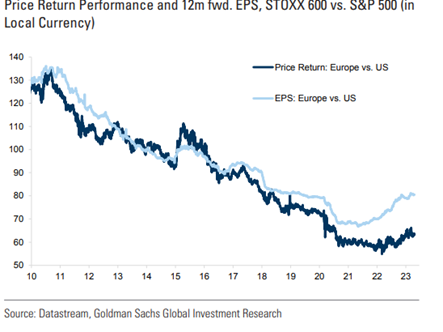

Europe's strong development is fair when you study the picture below, which shows the profit development for European companies in relation to American ones. The dark blue line shows Europe's return relative to the American one and the light blue the relative profit development.

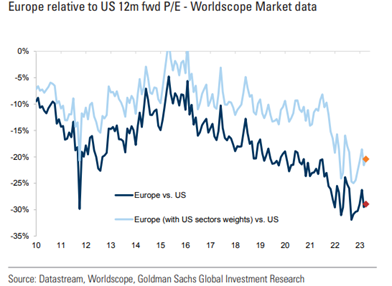

Despite a strong development, the valuation difference with the US is still at high levels. Below is the difference in percentage of twelve-month forward-looking P/E ratios for Europe compared to the US. The light blue line is adjusted for different sector weights.

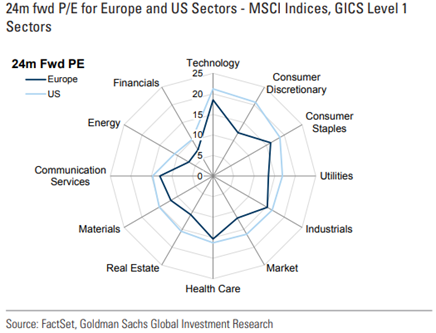

Below is a spider diagram showing the difference in valuation for each sector. All sectors are valued higher in the US. For example, energy in Europe is valued at 7x, while the corresponding multiple in the US is 11x.

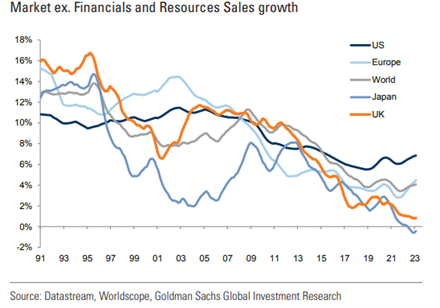

There are, of course, various reasons why American companies typically have a strong valuation. One is growth, and the sales trend for different geographic regions is illustrated below. Japan feels like so so….

The American companies also invest more than the European ones. This contributes to the stronger sales growth and a higher return on capital, which in turn determines the valuation.

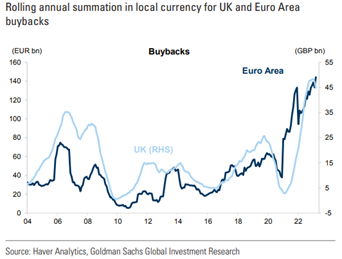

It is pleasing to note that share buybacks have increased in Europe in recent years. In most cases, it creates significant shareholder value without any operational risk. In some countries, such as Germany, it is still regarded with great skepticism. The German stock market is also one of the lowest valued in Europe. In Sweden, buybacks are significantly more common, and the Swedish stock exchange also has a better valuation. Several factors impact valuations, but buybacks often create shareholder value.

In summary, we will soon be through an unusually strong reporting season with relatively little impact on the broad index levels, but often with a large impact on individual stocks. In a short time, bids for various companies have poured in after an M&A activity that for a long time was conspicuous by its absence. In fact, I cannot recall that there have been so many takeover offers in such a short period of time during my almost 30 years in the industry. It indicates a latent need, strong balance sheets and greater optimism among companies than among investors.

Earnings estimates will be adjusted up slightly after the reports and the buybacks will start rolling again. There are several significant macro and geopolitical challenges that are dampening risk appetite and we are now entering the summer period, which has historically had a weaker development compared to the winter term. As for the American banking crisis, the last word has probably not been said.

The central banks led by the Fed are now close to their interest rate peak, which has been a huge headwind for risk appetite in the past year. Once the central banks stop, they usually never stay there for long. They are normally positioned in some form of direction, and we believe that interest rate cuts will come earlier than expected. The next challenge is to balance the interest rate weapon against a possible recession. We continue to focus on our company analysis, where we had a high level of precision this reporting period as well.

We wish you a wonderful May with hope for lots of sun and warm temperatures!

Mikael & Team

Malmö on May 5th, 2023