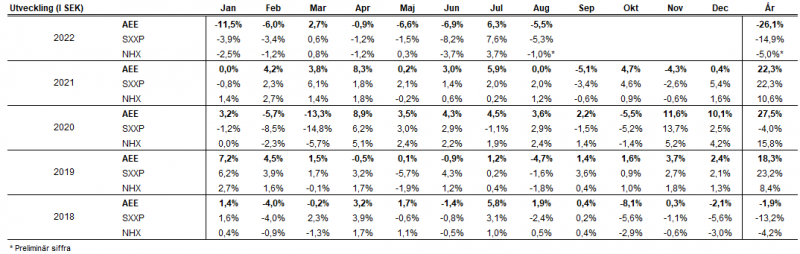

Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class' return. The information below regarding returns therefore differs from the returns in other share classes.

Before making any final investment decisions, please read the prospectus, its Annual Report, and the KIID of the relevant Sub-Fund here

This material is marketing communication

Monthly Newsletter Coeli Absolute European Equity – August 2022

AUGUST PERFORMANCE

The fund’s value decreased by 5.5% in August (share class I SEK). The Stoxx600 (broad European index) decreased during the same period by 5.3% and HedgeNordic’s NHX Equities declined provisionally by 1%. The corresponding figures for 2022 are a decrease of 26.1% for the fund, -14.9% for the Stoxx600 and -5% for NHX Equities.

EQUITY MARKETS / MACRO ENVIRONMENT

The beginning of August was an extension of July's optimism and the world's stock markets continued to climb. After a week or so the momentum of the rally started to wane and in a market with little liquidity (most of Europe was on holiday) it didn't take much selling volume to move share prices down. US Speaker, Nancy Pelosi's, visit to Taiwan unnerved investors (and China) and as energy prices continued to soar, risk appetite was dampened further. When US Federal Reserve Chairman, Jerome Powell, on Friday 26th of August was more hawkish compared to a month ago, we had the worst daily performance on the US stock markets since the beginning of June (Nasdaq -3.9%).

The broad European index fell by 5.3% in August compared to the fund's value, which fell by 5.5%. As an asset class, small caps were worst in class, e.g., the SEB Small Companies Index fell by 9%. The broad Swedish index fell by 7.1%. In such an environment, the Swedish krona is usually under pressure. This time was no exception and the Swedish krona fell in August by 3.2 and 4.7% against the euro and the US dollar respectively. The UK currency, which is the western country most severely affected by strong inflation (expected to rise to 20% in 2023e), also fell by 3% against the euro. The fund's exposure to these two currencies is roughly 45%, with the largest exposure to GBP. Taken together and in isolation, it led to a negative profit contribution in August of just under 1.5%. We want to believe (wishful thinking?) that it will be reversed in the future.

The big talk of the month was rightly the skyrocketing energy prices in Sweden and in large parts of Europe. Slightly dizzy politicians began mixing ignorance, lies and facts in front of their voters in an increasingly hysterical election debate. There is no doubt that large amounts of support are needed to literally get people and businesses in southern Sweden to survive. The Social Democrats' initial proposal of 30 billion in support for consumers and the same amount for companies is a lot of money, but unfortunately only a drop in the ocean to cover the greatly increased costs (there has now been a new proposal of 45 plus 45 billion).

If you assume that out of just over two million villa households, 1.5 million are in price range 3 and 4 and each villa consumes 25,000 Kwh per year, then it becomes 37 billion Kwh. Then it is enough to reduce the electricity cost by just over a krona per Kwh. After tax and VAT, it looks like a private person has another SEK 7-8 left to pay. The state takes 15% of the price shock and the consumer in southern Sweden the remaining 85%, and much of it is pure tax. The price difference compared to northern Sweden today, when this is being written, is about 20x. Electricity-intensive companies in southern Sweden do not have a chance to compete with companies in northern Sweden. Absolutely horrible and within a few weeks the risk of layoffs will pour in due to the cost explosion. It's going to be a long and cold winter.

Source: Steget efter

The difference between strategic thinking and naive energy policy becomes clear when you read in Helsingin Sanomat that Finland's new nuclear power plant, which cost the owner approximately 5.5 billion euros, has a payback period of three years and seven months with today's conditions. Even if it were a few years longer, it's a brilliant investment. Feels like a better capital allocation than sending away 50-100 billion to people and companies just to be able to survive the winter months and keep your fingers crossed that it’s windy.

Below German energy prices which also had an explosive development. It will affect the country's GDP significantly and if the country is not to end up in a deeper recession, the state must take a large part of the increased costs. It is very difficult to understand that even after Russia's entry into Crimea in 2014, they continued to build critical infrastructure together with Putin. The pressure on people and companies in Germany increases with each passing week and we hear more often comments that the price of helping Ukraine is too high. European solidarity is being tested and the fact that Putin on Friday evening, September 2nd completely shut off the gas tap to Europe does not make matters better.

Source: Bloomberg, Holger Zschaepitz

Part of the explanation for the violent price rise is the targets that Germany has set for winter stock. They are at least two weeks ahead of their plan when the gas stocks were already up to 75% a few weeks ago. By October 1st, at the latest, they must reach 85% (they will soon be there) and by November 1st, 95%. They have aggressively purchased gas from other countries and paid little attention to the price. The EU goal of reducing consumption by 15% also seems to be achieved. The latest assessment by Goldman Sachs says that if Russia does not turn the gas back on or there is a cold winter, Germany will be without gas in the first half of 2023. With normal weather and 20% flows from Russia, they will manage, but possibly have problems next winter. In winter 2025, significantly more capacity will come in and the situation will therefore be significantly better for Europe.

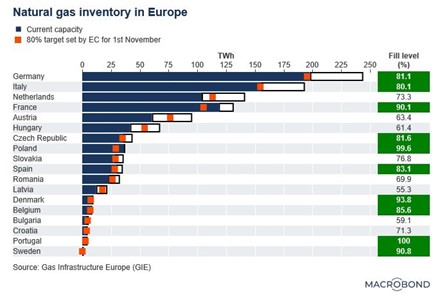

When the President of the European Commission, Ursula von der Leyen, announced a few days ago that the EU will come up with a crisis measure and some kind of price ceiling, gas prices fell by almost at most 50% in a few days. Who decides the price of electricity in Europe? Are we all in the hands of speculators? Say what you want about Europe, but you have experience with crisis packages. Below are the gas stocks of various European countries. Sweden is in principle completely independent of gas.

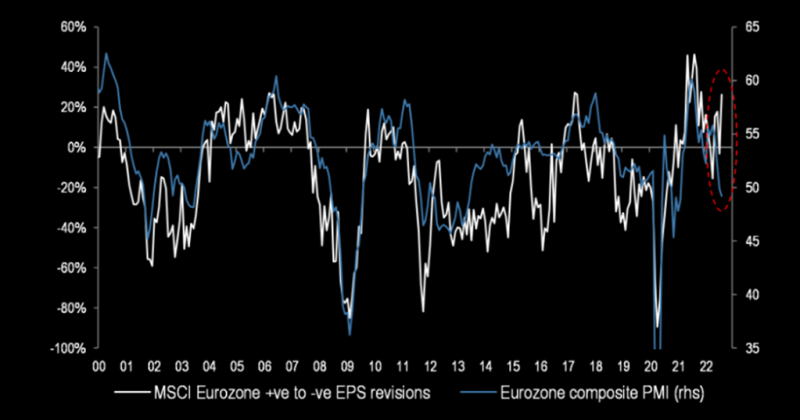

Below is the purchasing index for the Eurozone, combined with earnings per share for European companies. Consensus expectations for profit growth in Europe are currently 17.7% and 2.7% respectively for 2022-2023e, which feels optimistic. The covariation has currently been broken (circled in red on the right), which supports our thesis that the estimates are generally too high.

Source: JPM

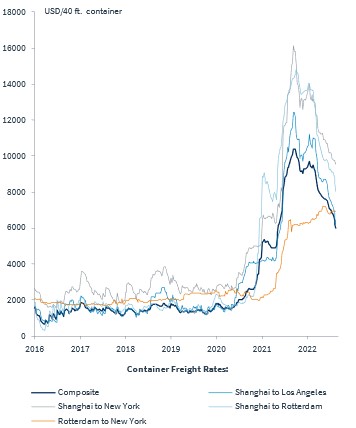

Although inflation is more persistent and broader than most of us thought a few months ago, there are an increasing number of good signs. Here, too, the USA is ahead of Europe in development. Below are shipping rates that keep falling.

Source: Kepler Chevreux

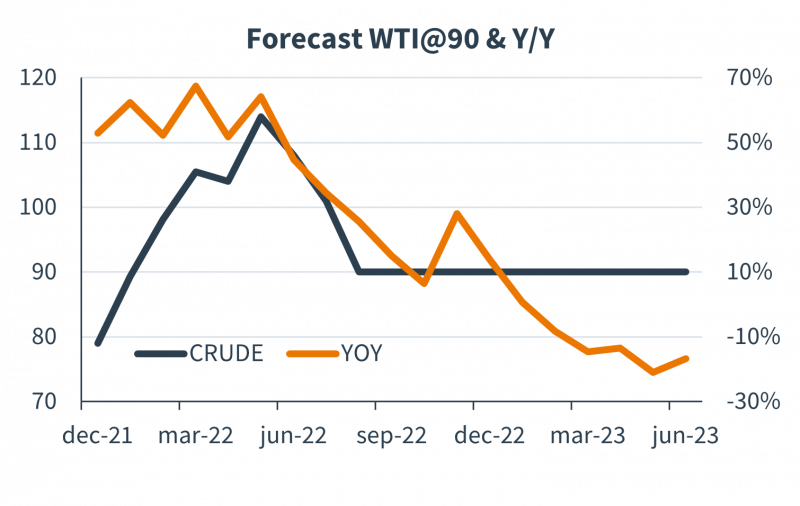

If the oil price remains around USD 90 per barrel (black, left), the YOY contribution to inflation will go from plus 60% to minus 20% (orange, right). Energy is about a third of US core inflation. At the time of writing, the price of oil is only a few percent higher than it was before Russia invaded Ukraine. The definition of Putin prizes is becoming difficult to discern.

Source: Kepler Cheuvreux

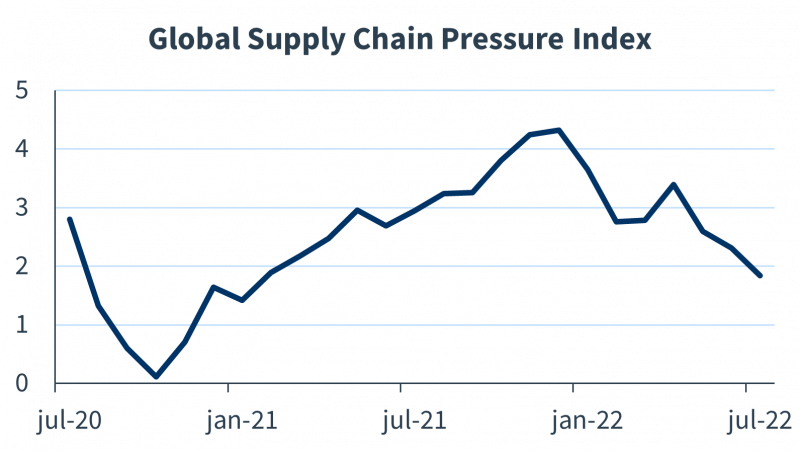

In addition, more and more companies are reporting a positive development in terms of various bottleneck problems, which will also contribute to a certain dampening of price levels. The image below illustrates this well.

Source: Kepler Cheuvreux

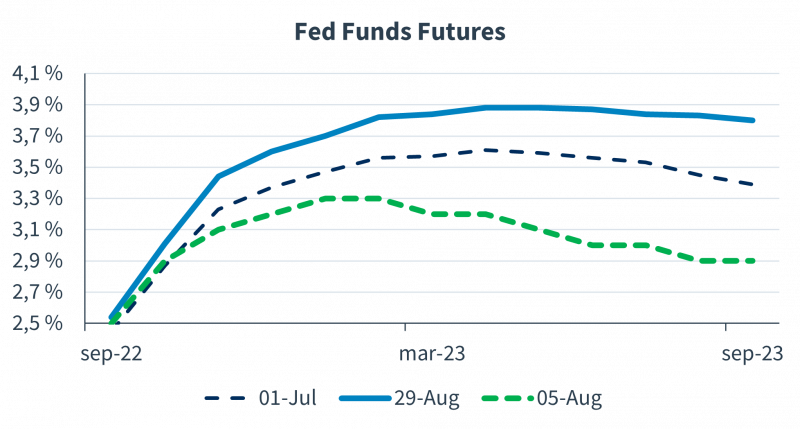

What currently affects market sentiment by far is the aftermath of the US Federal Reserve Chairman's speech on August 26th in Jackson Hole. The speech lasted eight minutes and when finished, we had the biggest drop in the stock market in months and not since 2010 has a Jackson Hole speech received such a negative reaction in the market. The Fed will continue raising interest rates as long as necessary to get down to two percent inflation ("will keep at it until we are confident the job is done"). He also said that the development to tame inflation "falls far short of what the Committee will need to see before we are confident that inflation is moving down".

The speech led to sharply rising interest rates, and below is shown how the market has forecast the key interest rate for the past two months. It is very unusual for the differences to be so large in such a short period of time, which is a large part of the explanation for the slightly neurotic development of the stock market during the same period of time.

Source: Kepler Cheuvreux

Source: Economist

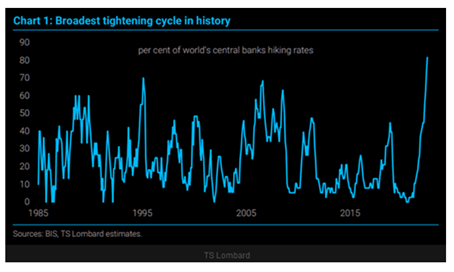

We live in unusual times in many ways. Below is the force of tightening by the world's central banks over the past 40 years - strongest ever.

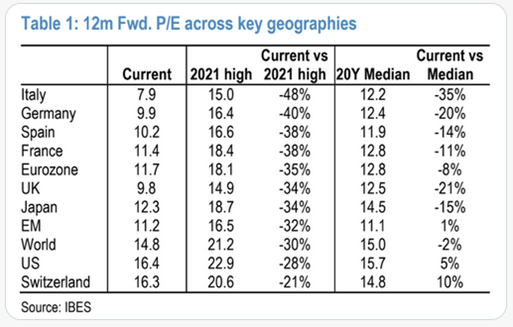

A snapshot of the valuation of a number of different stock markets around the world. The multiple contraction has been compressed by approximately 20-50%. As we mentioned earlier, the problem going forward is not the valuation but how much the companies' earnings should decrease.

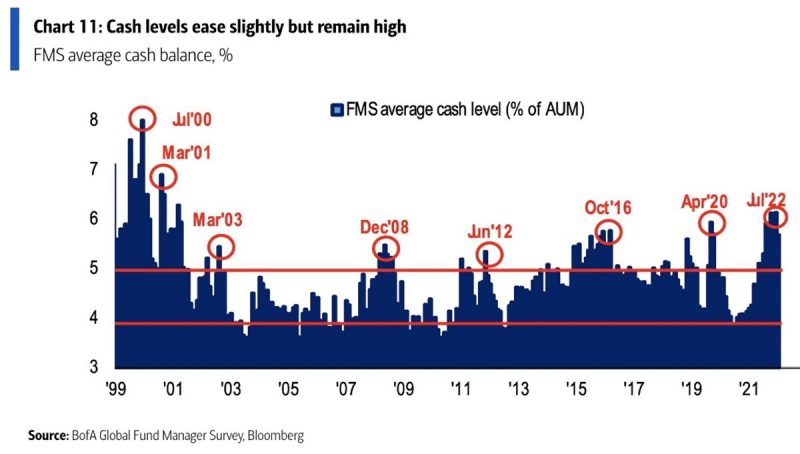

The cash levels of the world's stock managers are, from a historical perspective, still high, see image below.

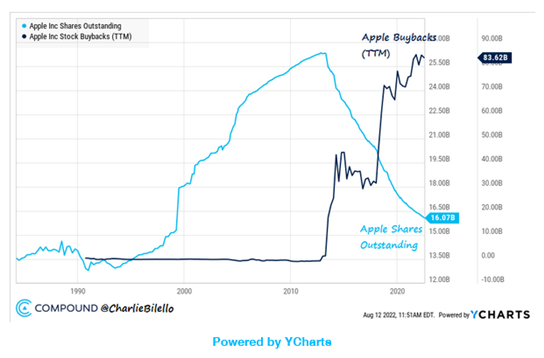

A company that has a large cash register is Apple. This despite the fact that in the last 10 years shares have been bought back for SEK 5,500 billion, which is more than the total market value of 494 out of 500 companies included in the S&P500. Impressive to say the least.

Long positions

Sampo

Since the beginning of the year, we have had a position in Finnish Sampo. After the sale of the company's Nordea holdings, Sampo now consists of some of the world's finest insurance assets. The Q2 report in August was impressive. The main asset, insurance company “If”, impressed the most with strong profit growth. The Sampo holding has been one of the fund's better ones this year. (That's not particularly surprising since it can still be described as a defensive holding.) The stock rose by 7% in August.

London Stock Exchange

Another defensive holding that delivered in August was the London Stock Exchange. Just like Sampo, we took on the share at the beginning of the year. The stock market has long been skeptical of the company after it completed a gigantic acquisition. The market saw integration difficulties and a risk that the costs related to the acquisition would be worse than communicated. However, after several reports, the management has proved the skeptics wrong, and the share had risen 16% in 2022 as of the end of August. During the month, the share rose by around 1%.

Musti

We continue to follow the "pet market" closely and made a short visit to Finnish Musti in August. Before the Q2 results, we thought the market was very gloomy. The number of newly registered dogs in at least Sweden continues to be higher than before the pandemic, although the levels are lower than the record year 2021. We also noted insider buying among the management team and thought analysts' expectations were low. Combined with a valuation that looked more appetizing than in a long time, we bought shares around EUR 17. After the report, the share price rose rapidly, and our investment thesis was fulfilled in a few weeks (definitely faster than expected). We have therefore liquidated the position and are looking further at other opportunities in the sector.

4imprint

For some time now, we have been buying shares in London-listed 4imprint. Really, it's only the share price that has anything to do with the UK, as basically all the business is based in the US. 4imprint is a distributor of "give aways", typically products that are used for marketing purposes, for example at conferences and events. After a couple of very tough pandemic years, 4imprint has come back strong in 2022.

In a normal world, 4imprint has a return on capital employed of more than 80%. At the same time, sales grow by more than 10% per year (pandemic years excluded). Every year the company takes market shares that they can use to create economies of scale: with its size, the company can negotiate down its supplier costs, which they can in turn use to lower the price to customers and thus take even more market shares.

After several positive report surprises, the share has risen around 27% this year. Despite this, we think the valuation is low. If we are correct in our estimates, the share will trade at a valuation of approximately EV/EBIT 12x 2022e, which is clearly lower than historical levels. The 4imprint share rose by 19% in August.

ISS

At the beginning of the month, ISS came out with yet another update that added flavor to the market. The organic growth was strong, and the operating result was somewhat better than the market's expectations. The outlook for the full year was raised and the company is now forecasting sales for 2022 to grow by more than five percent. We like free cash flow to continue to improve and debt to decrease. A large part of the investment thesis is about investors regaining confidence in the company, which underperformed for several years under its previous management. As ISS continues to deliver on its goals, more people should gradually become more positive about the company. ISS shares rose 3% in August and have risen 4% in 2022.

Short positions

The short portfolio contributed to a positive result during the month. The biggest positive contribution was made by our short positions in a Swedish small company index and in the German DAX. A couple of stock-specific short positions that contributed positively to the result were Finnish Qt Group and Swedish Mips.

Exposure

The net exposure, adjusted for our unlisted holdings, at the beginning and end of the month was 52%.

Summary

Since the outbreak of Covid-19 2.5 years ago, we have experienced the fastest 30% decline on record, the shortest recession on record, the most aggressive monetary and fiscal policy response on record, the fastest/strongest stock market recovery on record, the highest inflation in decades, the sharpest tightening by the US central bank in at least a generation and the worst first half for stocks in 50 years. In addition, we have had a war in Europe. At least these are not uninteresting times in which we live.

The reporting season for the fund was, with a few exceptions, good for the fund and our companies. As for our large positions, it passed with flying colours. We have limited knowledge of how the shares develop in the short term after the quarterly reports, but if the reports correspond to or are better than our expectations, we know that our analysis process is working and then the probability also increases significantly that our long-term investment theses will be fulfilled over time.

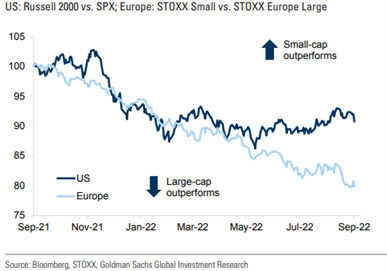

Despite a strong reporting season, the net development for the fund during July and August was relatively unchanged, which is of course frustrating. Two clear movements affected us negatively in August. The first is the asset class small caps, which again (see June) had a very weak development and even though we have reduced our exposure to these types of companies a lot throughout the year, we are still exposed.

Below is a shorter time series and with Europe included. You can clearly see the last month's weak development in Europe.

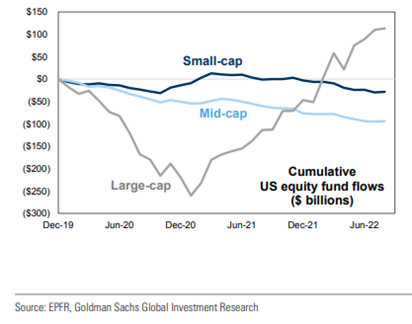

The picture below confirms what we just said. Investors are looking for liquidity and then the capital is allocated to the larger companies, and this also applies to our fund. We have significantly larger companies in the portfolio today compared to a year ago.

The other external factor that negatively affected our returns in August was the currency movements mentioned in the introduction of the letter. The negative profit contribution for August was just under 1.5%.

That there is no more discussion about the chronically weak Swedish krona is strange to us. Either the politicians do not understand the seriousness (quite possible), or they are busy putting out fires elsewhere. Below is the development against the US dollar since November last year, which quickly and unpleasantly became 27% more expensive. If nothing else, the weak Swedish krona is excellent fuel for the inflation fire. For Swedes who save and have parts of their capital in a typical global index fund, this is positive. 60% of the world's shares are denominated in USD. Since November, you have received a 17-18% return just from a strong USD (or a weak SEK, however you choose to look at it). These are huge numbers. And finally, the CHF passed SEK 11 in August. 50 years ago it was 1 krona.

Source: Bloomberg

All of our large holdings are companies that have good conditions to continue to have a certain level of growth under tough circumstances, that have stable or in best cases rising gross margins and where the balance sheet is strong. In addition, the valuation is attractive by our standards.

It is no surprise that the consumer is in record depression right now and it looks more or less the same in Europe. Below the mood of German consumers and they are currently significantly more depressed than during the Covid crash. Realistically, one can hope that the curve will turn upwards as early as in the spring, but as always, the stock market is ahead of reality.

Source: Bloomberg

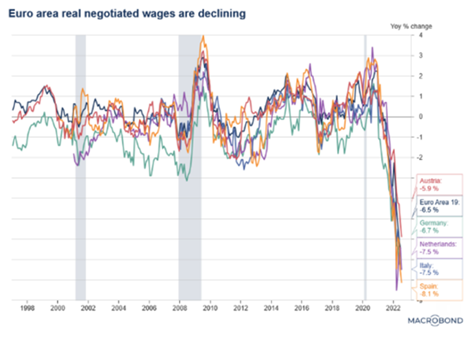

Below is the development of real wages over the past 25 years. A brutal awakening this year with sharply falling real wages.

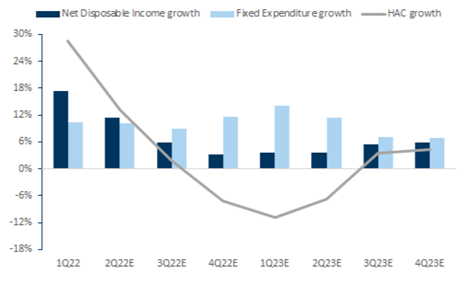

Below is an interesting analysis from Goldman Sachs where HAC stands for "Household Available Cash Flow". The lowest point will be in Q1 next year and then we'll go up again. It sounds reasonable with an expected slowing inflation and later in 2023 falling interest rates. There is hope!

Source: Goldman Sachs

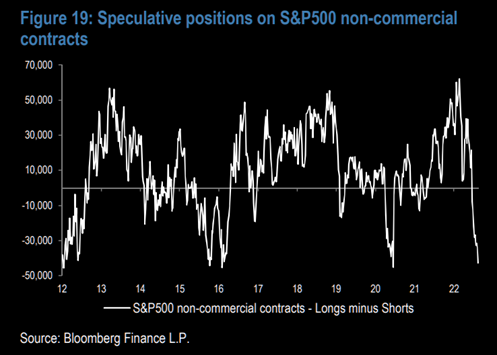

In conclusion, we continue to hold to our view of a range bound market and we note that we now again look set to test the lows from June. We also maintain our view that the US Federal Reserve's announcement at the end of September will likely determine how the year ends. Undoubtedly, the positioning in the market is cautious and investors are sitting on a lot of cash. Below, long minus short positions on the S&P500 and aggregated are at historically very low levels.

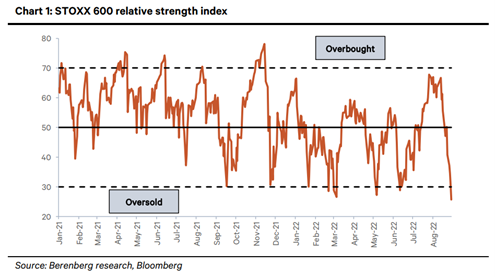

Last chart of the week from Berenberg. In recent years, it has been a reliable buy signal when we have been at these levels.

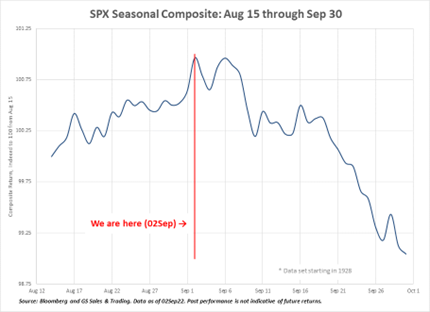

September is traditionally a weak month and there is currently low liquidity in the market. On the other hand, we have had a significantly weaker end to August than we usually have. In the second half of August, for example, SXXP600 had a negative return of just over 6%.

The S&P500 has this year had its fourth worst performance ever YTD. For those interested in statistics and history, returns from here have been positive for 7 of the 8 historically worst years to date. 1974 is the only year with a negative return from here and it was -5%.

In conclusion, the fact that Putin cut off the gas to Europe on Friday, September 2nd is hardly something that helps, although we think few are surprised. With no flows coming from Russia, we would like to think this is the end of negative news. In the slightly longer term, Europe will win and overtake Russia, which is putting itself 50-100 years behind in economic development. The last few weeks have been weak, and it is tight on the downside. That should mean we're in for a pullback soon, but as I said, we live in unusual times. The next big data point is inflation data from the US which is announced in about two weeks.

We are grateful for your continued trust and patience and are working hard to have a good end to the year.

Mikael & Team

Malmö on 6th of September 2022