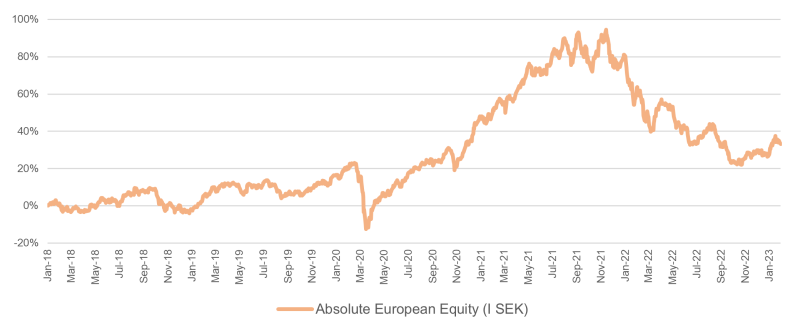

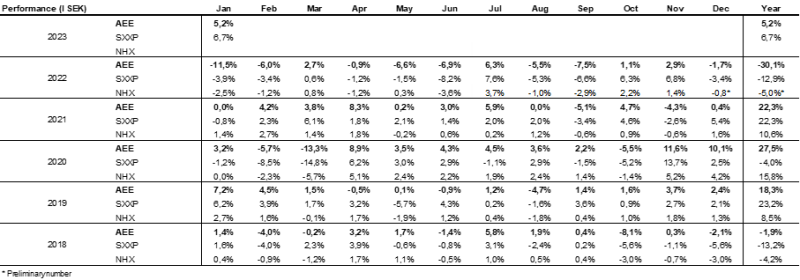

Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class' return. The information below regarding returns therefore differs from the returns in other share classes.

Before making any final investment decisions, please read the prospectus, its Annual Report, and the KID of the relevant Sub-Fund here

This material is marketing communication

Monthly Newsletter Coeli Absolute European Equity – January 2023

JANUARY PERFORMANCE

The fund’s value increased by 5.3% in January (share class I SEK). The Stoxx600 (broad European index) increased during the same period by 6.7%. At the time of publication of this letter, no data was available for HedgeNordic's NHX Equities.

EQUITY MARKETS / MACRO ENVIRONMENT

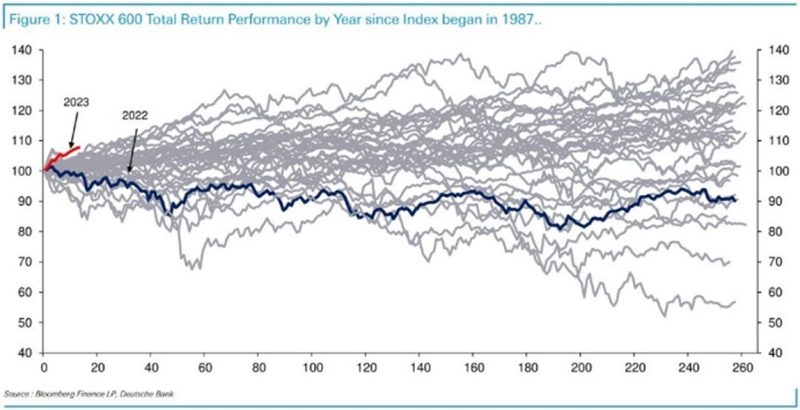

The last 5-6 weeks have seen several positive events in the world economy and many of the European companies are now more optimistic compared to last autumn. Europe's stock markets have started the year strongly, which surprised the large investor collective. The image below shows the broad European index which has had its best start since the index was introduced in 1987.

The reasons for greater optimism include: 1) Continued strong order books 2) A maintained pricing power 3) A collapse of energy prices 4) A surprisingly rapid opening up in China, which increases the likelihood that growth will accelerate 5) Continued impressive resilience among companies 6) An inflation that is declining.

Somewhat of a setback occurred on Monday, January 30, when Spain, which had been the first to show falling inflation in Europe, reported higher than expected inflation - 5.8% against the expected 5.0%. The ECB will with a very high probability raise the key interest rate by another 50bp on February 2nd.

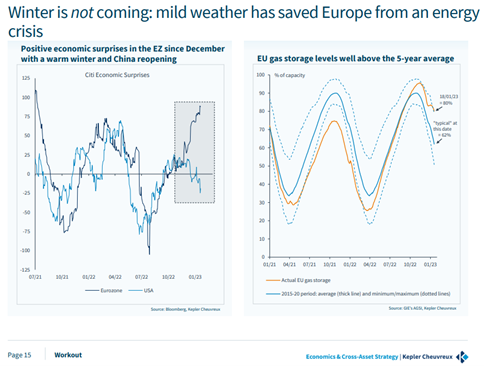

At the end of January several green shoots could be discerned in American and Chinese GDP data for the fourth quarter, which surprised positively. Purchasing indices in both the US, Europe and China were also better than expected. Below left shows Citi's Economic Surprise Index. In recent months, Europe has had significantly more positive news than the US. On the right, the EU's well-filled gas storage is shown.

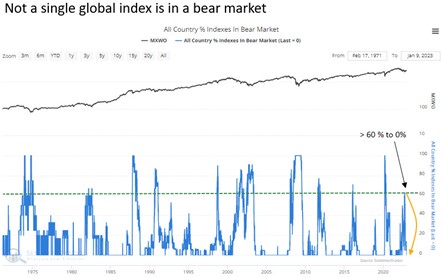

None of the global indices are now (end of January) by definition in a "bear market". A few months ago, 60% of the global indices were in a bear market. Such a development has only occurred 11 times in the last 50 years, see picture below.

Source: Sentimenttrader

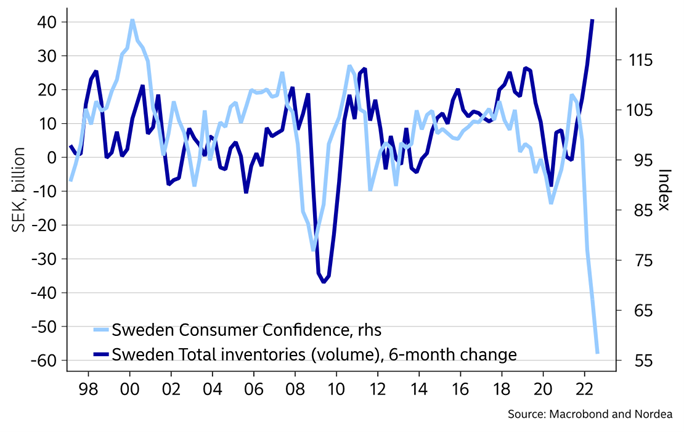

Although many Swedish companies continue to be profitable, it is less cheerful for the country of Sweden. Sweden currently has the highest inflation in the Eurozone and with a chronically weak currency inflationary pressure increases further. Sweden has the sharpest decline in property prices in Europe and an energy system that is dysfunctional in large parts of the country. The consumer is under heavy pressure, see picture below. Sweden ranks fifth in Europe in terms of unemployment after Spain, Turkey, Italy and Greece. However, we have the world's highest marginal tax (source OECD) and Europe's lowest growth in both 2022 and 2023 (source EU Commission). We also have the highest deadly shootings per inhabitant in the EU. How did we end up here?

On Monday, January 30, data was also published for GDP growth in Sweden for the fourth quarter. Growth for the fourth quarter ended at -0.6% against the expected +0.2%. An unusually strong deviation and the Swedish krona came under renewed pressure. In the last 15 months, the krona has fallen against the euro for a full 12 months. A disaster created by the Riksbank and our elected politicians.

US ETFs, which rise in value when the market falls, have had a record inflow in the first few weeks of the year. So far it has been completely wrong, but the year is long.

Source: Bloomberg

Undoubtedly, cautious positioning among investors has pushed share prices upwards. Generally speaking, the stocks with the highest proportion of short positions and with a weak development last year have been this year's winners. The blue curve shows the development during the first weeks of the year for the 50 stocks on the American stock exchange that were the most heavily shorted.

Source: The Daily Shot

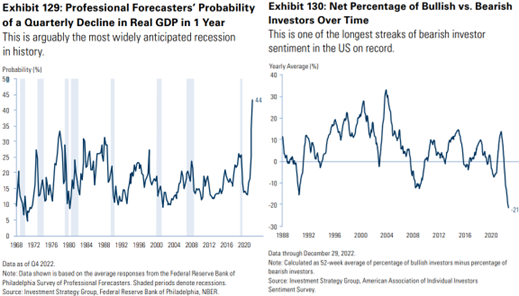

The image on the left below shows that it is the most expected recession since the US Federal Reserve began keeping statistics in 1968. That, combined with a record depressed mood among investors, right-hand image, has contributed to the rise in January. When everyone expects the same thing, it rarely happens. There will of course be occasions for reversals during the year.

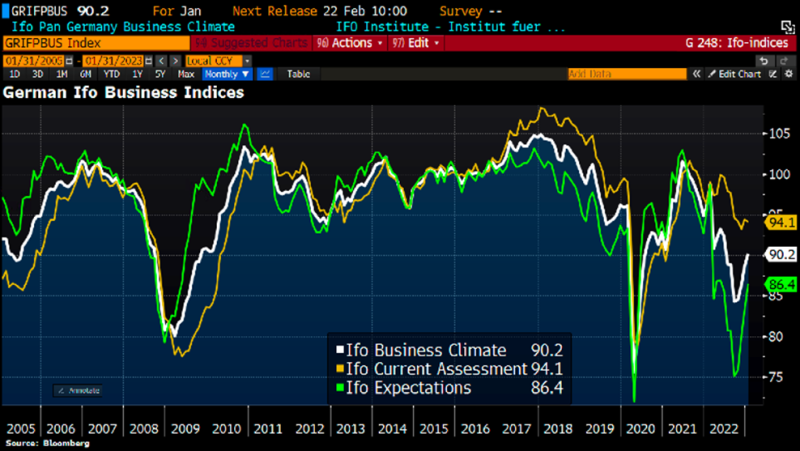

"I'm absolutely convinced that this will not happen - Germany going into a recession". This is what German Chancellor, Olaf Scholz, expressed when the world's politicians and business leaders, after a two-year hiatus due to the pandemic, were once again in place in Davos. The IMF took the opportunity to upgrade its outlook of the world economy for 2023. Instead of expecting a tougher climate as previously forecasted, the IMF now expects an improvement in the second half of this year into 2024. German optimism recoiled somewhat when GDP data for the fourth quarter on January 30th showed a mild contraction of 0.2% against expected unchanged growth.

Below, German business climate index (Ifo) where you can see a clear improvement since the end of last year.

Source: Bloomberg

At the end of the month, the Lloyds Bank Business Barometer and its UK Business Confidence were also published. Somewhat surprisingly, 2023 has started with the highest optimism in 6 months among UK companies. The companies are more optimistic - they expected to hire slightly more staff at the same time as wage inflation decreased somewhat.

The reasons why the IMF and others are now revising up the growth forecasts for 2023 are, among other things, China's dismantling of strict Covid controls, the US's upcoming giant green investment boom, falling energy prices in Europe, and the fact that, a year after Russia's attack on Ukraine, Europe's companies have adapted to that new reality. The fact that Russia gradually appears to be losing the war surely also plays a role. Russia as a great power does not exist and the only thing the country can do is send in old scrap for weapons that destroy schools, hospitals, residential buildings and injure and kill innocent civilians. There are many of us in the world who are looking forward to the upcoming court hearings with Putin and his entourage on the front row.

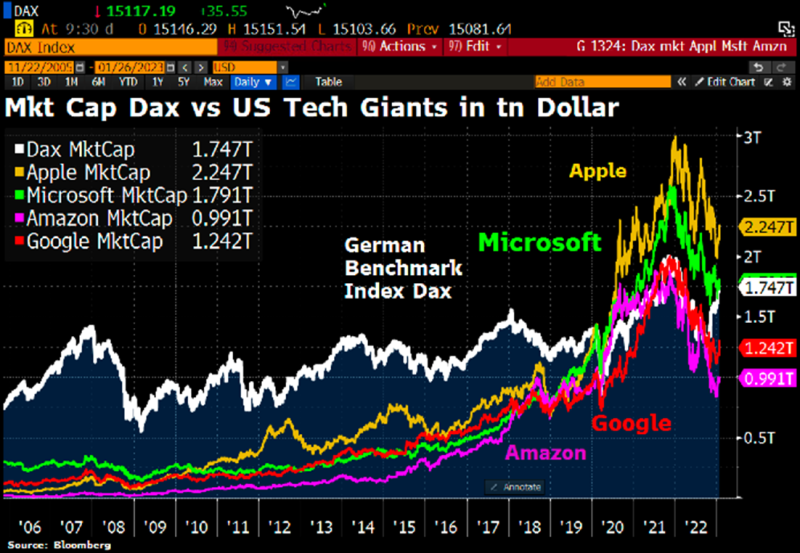

The total value of the German stock market (white line) rises relative to American technology companies and now corresponds to, for example, the value of Microsoft and is greater than Google and Amazon respectively.

Source: Bloomberg

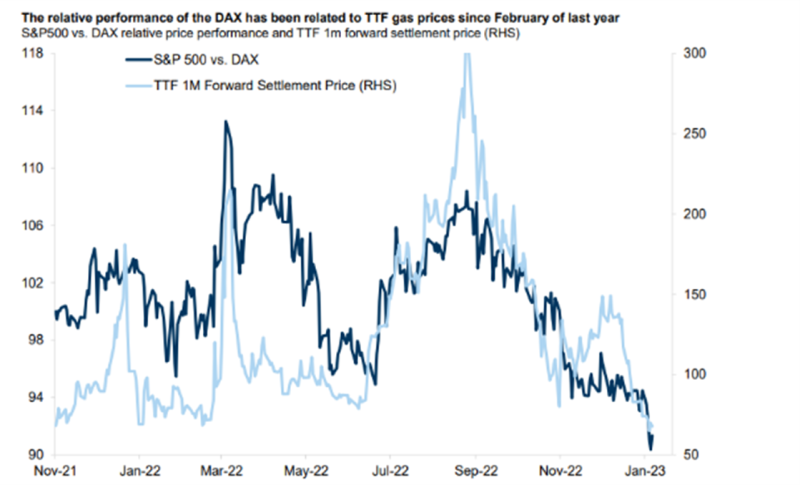

Since the beginning of October, when gas prices began to fall sharply, the American stock market has been significantly weaker than the German one (dark blue line).

Source: Goldman Sachs

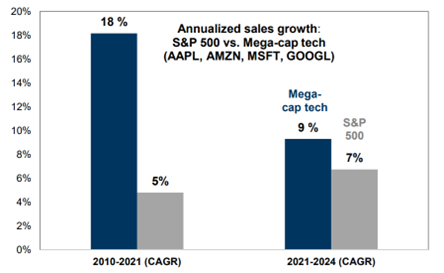

In last month's newsletter, we argued that the heyday of the major American technology companies on the stock market was probably over, partly because of the image below.

Source: Goldman Sachs

So far it has been wrong as several of the FAANG companies had a very strong start to the year. That Tesla’s share has risen by 41% since the beginning of January is a strong indicator of a rising risk appetite. At the time of writing, the market value of Tesla is approximately SEK 6,000 billion.

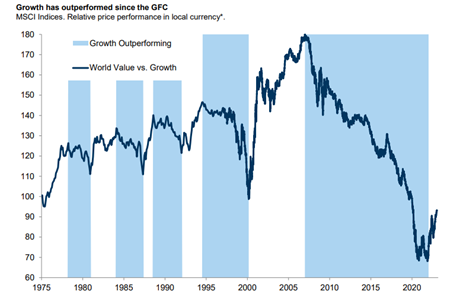

Since the financial crisis 15 years ago, the relative return for growth companies compared to value companies has been enormous. Last year the trend was broken.

Source: Goldman Sachs

2023 is the Year of the Rabbit and started on January 23rd according to the Chinese calendar. The rabbit is a symbol of a long life, peace and prosperity. We hope for a happy rabbit in 2023.

Source: Twitter

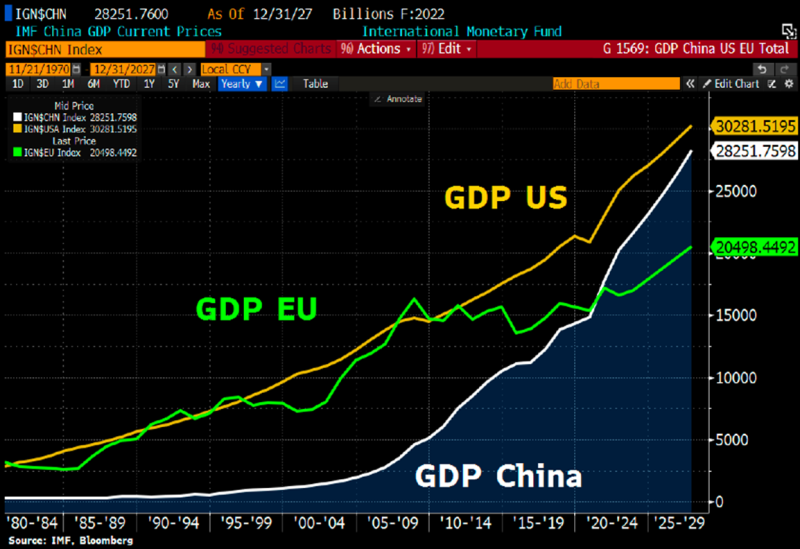

An interesting picture that shows the economic development of the EU, USA and China. In 2009, the EU was at the top.

Source: IMF, Bloomberg

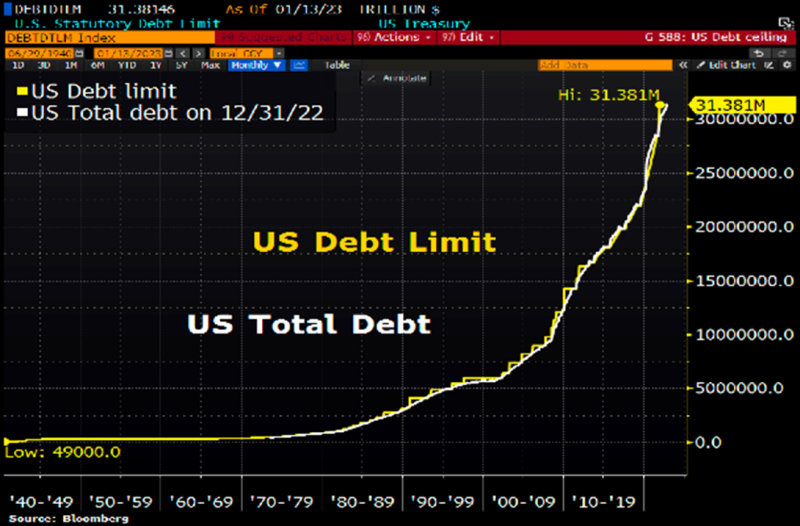

Prepare for the US debt ceiling to be discussed in the spring. Soon Treasury Secretary, Janet Yellen, may have to take unusual measures which could include delaying federal employee pensions. Congress must reach an agreement before the summer, which will surely be a duel between Republicans and Democrats. To be continued.

Source: Bloomberg

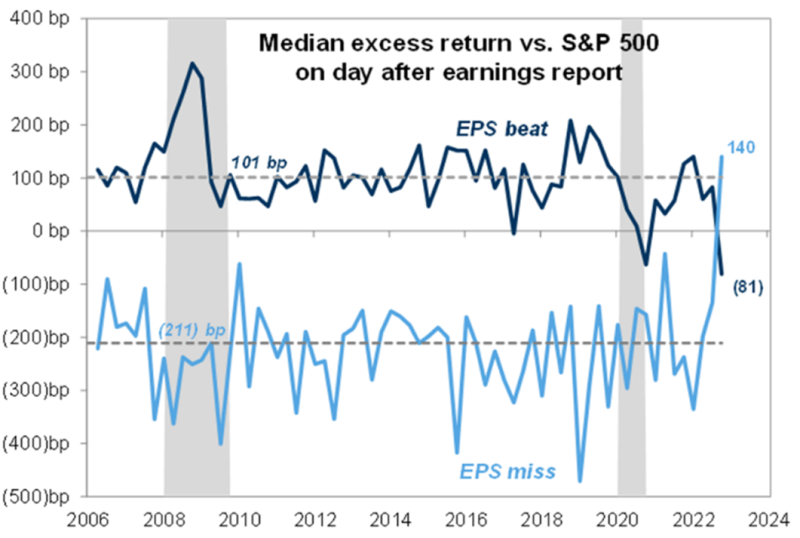

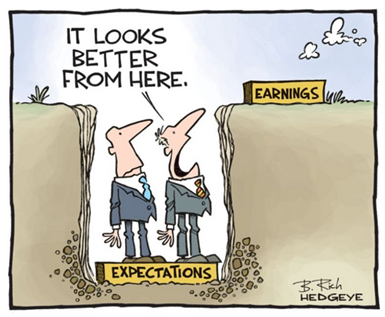

At the time of writing, only 25% of the companies in the S&P500 index have reported. Weak reports and clear misses against expectations have initially played less of a role as share prices have risen in the first weeks of the year.

Source: Goldman Sachs

Expectations have come down, but is that enough?

Source: HEDGEYE

Long positions

Pets at Home

We wrote about Pets at Home as recently as in our December newsletter. You will find a more detailed description of why we like the company there. In short, the investment thesis is about what we believe to be a high-quality company whose share price has fallen too much because of its shop tag. In the short term, we have been right in our thesis, as the share price rose 24% during the month. Pets at Home thus became the holding that contributed the most to the month's results (just over one percent).

The price rise came after the company released its Q3 report covering October – December. With eight weeks left in the financial year, the company upgraded its full-year profit outlook with around four percent. Comparable store growth rose 8.3% in Q3, compared to 6.8% and 6.0% in the previous two quarters, respectively. We were even more impressed by the growth in the company's veterinary segment, which amounted to a whopping 18%. This is a high-margin business which, over time, will constitute a larger part of the turnover and a disproportionately larger share of the profit.

Interestingly, sales of discretionary products (purchases that are not critical, such as pet food or cat litter) also rose in the third quarter. These products have higher margins than other product categories. Many have believed in a large decline in sales of these high-margin products as the economy worsened, but that has not yet happened. We also note that the business continues to take in more than 20,000 newly registered puppies and kittens a week, well above pre-pandemic levels.

In January, a record number of dogs were newly registered in Sweden. It wasn't quite what we expected after a downward trend last year (even 2022 was strong compared to the years before 2020). We'll see if the January figure is indicative of the rest of the year. If this is the case, it is obviously good for a pet company such as Musti, with its Nordic exposure. But this data can probably also be indicative of Great Britain and thus Pets at Home. Despite a strong price rise since the lows last autumn, we still think the company looks attractively valued.

Source: Coeli European

Commerzbank

Commerzbank continued its journey during December and was once again one of the fund's top contributors in January. The company disclosed an update at the end of the month where it showed positive EBITDA two years in a row, which is one of the criteria to be included in the DAX 40, where Commerzbank is now a candidate. Preliminary figures were in line with expectations and the full report will come on February 16th. We continue to think that Commerzbank is an interesting restructuring case trading at very low multiples, despite strong profit growth in the coming years. The stock rose 18% in January after rising 10% in December.

Source: Bloomberg

SLP

Real estate had a good month in January and our holding in SLP was one of the top contributors to the fund's performance in January. There are many indications that SLP is attractively positioned in the coming years. The company has a strong balance sheet which it used to acquire properties from distressed sellers. Almost all leases are indexed to inflation, which mechanically gives +11% in rent growth in 2023. We believe that the yield gap between logistics and other properties will decrease, where SLP with relatively high yield requirements in the valuation should be a relative winner against, for example, housing and offices in big cities that have significantly lower yield requirements.

Bonesupport

Bonesupport had a weak December but bounced back in January to become one of the fund's strongest contributors. There hasn’t been any news, but we look forward to the report coming in February.

Lindab

The Lindab share also had a strong development during January and thus became one of the fund's strongest contributors. After a very weak 2022 where the price was heavily pressured by what appeared to be forced selling, the stock rose 14% in January.

Short positions

The short portfolio contributed negatively during the month. The biggest negative contribution came from our short positions in a Swedish small company index.

Summary

The world's stock markets had a great start to the new year with significant gains. The reasons were, as previously mentioned, several positive and significant news for the world economy combined with extremely gloomy investors with a cautious positioning, and not least a large element of psychology when the annus horribilis, 2022, had finally ended.

Europe continued to develop stronger than the broad indices in the US, even though the Nasdaq rose a whopping 10.6% and thus the index took its first revenge on last year's weak development (-28.7%). The Dow Jones rose by a more moderate 2.8%. As such it was the strongest start for the Nasdaq since 2001. Those who were around at the time will remember that the performance for the full year of 2001 ended at -21% (after falling by 39% year 2000) and was followed by 2002's development with a further -32%. It was the same year that Ericsson came close to bankruptcy, but that's a completely different story.

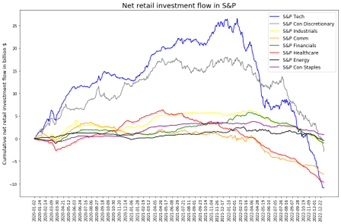

With January's developments behind us, it is interesting to study the huge selling wave of technology stocks by US private investors over the past year (blue line). In the end, there were no more shares to sell and there was a strong recoil.

Source: Goldman Sachs

We are satisfied with the fund's return of 5.3%, even though we gave back a little from the intra-month highs. Our companies that reported came with strong numbers and in many cases with significant price reactions in the market (Tate & Lyle and Pets at Home). All company news was positive during the month, and, with some exceptions, all long positions made a positive contribution. Of course, the short positions cost a lot when the market rose.

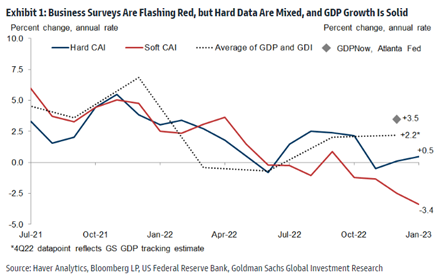

The image below shows that despite various surveys and forecasts that indicate clear declines in the American economy, GDP growth remains strong. Interesting and unusual that it differs so much over such a long period of time. "If the map and reality do not match, the map is the one that applies". An old military joke and so far, many investors have worked from the map.

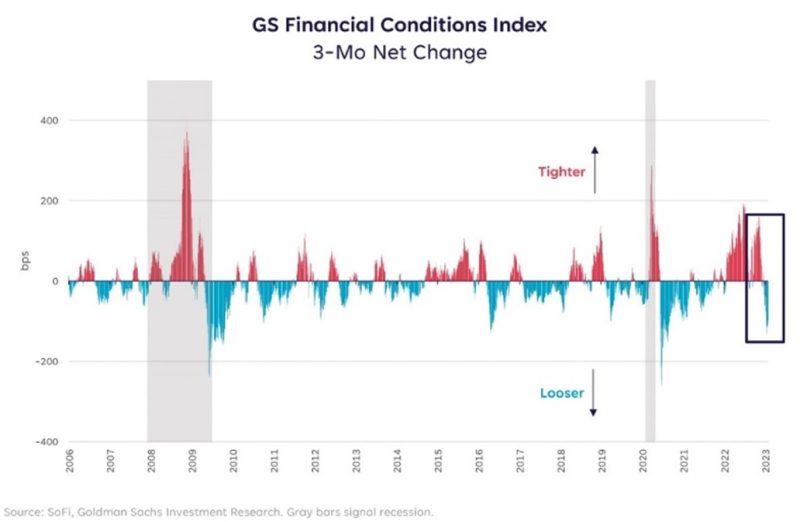

The Goldman Sachs Financial Conditions index, which is a weighted average of risk-free interest rates, exchange rates, equity valuations and credit spreads, has eased significantly over the past three months. The corresponding change has only happened twice before, first during the financial crisis in 2008 and then during the Covid crash. Positive for risk assets such as stocks.

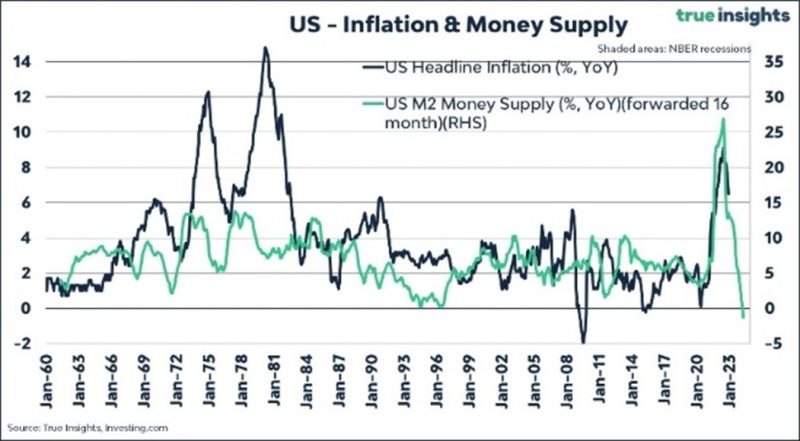

The money supply in the US has collapsed in recent quarters. That should mean inflation will follow suit (see image below). The last time there was a corresponding sharp decline in the money supply was during the depression of 1929-1930! At the same time, we have the strongest inverted yield curve in over 40 years, one of the most reliable indicators of an impending recession. Consumers are holding back on purchases and many raw materials have fallen sharply. The Fed should soon be able to pause its rate hikes. That they will release the brakes too late feels almost a foregone conclusion.

Source: trueinsights

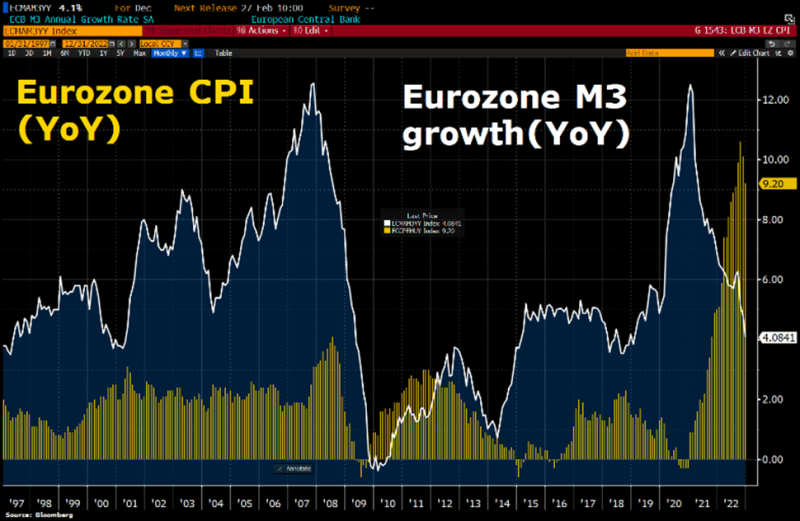

In Europe it looks similar, with the difference that we are a few months behind the USA. White line is money supply and yellow bars show inflation.

Source: Bloomberg, Holger Zschaepitz

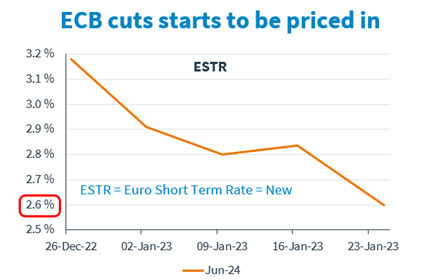

In the past month, the European money market has lowered the forecast for the level of the key interest rate in the summer of 2024. From 3.2% to 2.6% in one month! Even more likely than the Fed in the US, the ECB will act too aggressively and hurt the economy unnecessarily and start tapering too late. It feels a bit like watching a head-on collision in slow motion. The Riksbank's (Swedish Central Bank) actions are like watching a head-on collision in real time. Negative GDP growth in the last quarter and they are still eager to raise interest rates several more times during the year. Less than a year ago, they believed in a zero-interest rate until the second half of 2024.

Source: Kepler Cheuvreux

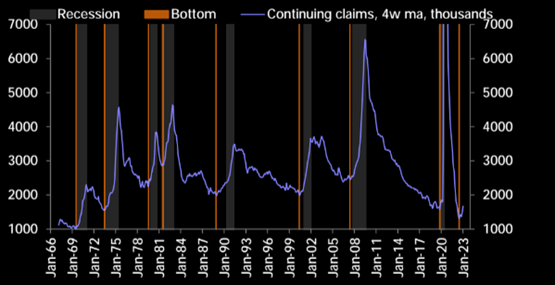

The number of people seeking unemployment benefits is another reliable indicator for forecasting an upcoming recession. You can see an increase in the last month in the picture below at the bottom right, but the level is still at very low levels.

Source: Themarketear.com

In addition to raw materials and freight rates, wage inflation now also appears to be falling in the US.

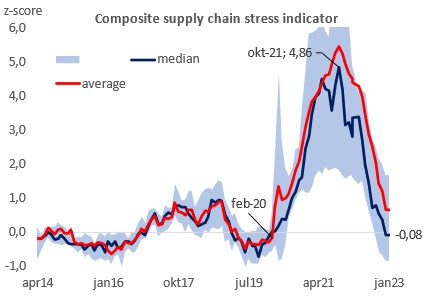

The stress level in terms of delivery problems for various components has come down significantly in the last year and is back to pre-pandemic levels. A very positive development for the world economy, including inflation.

Source: UBS

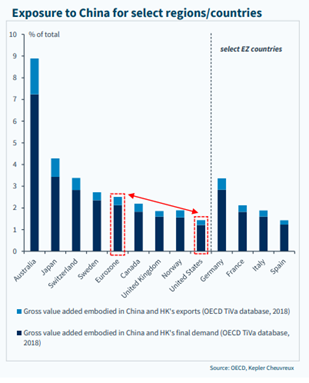

One of the reasons why Europe's stock markets have developed stronger than the US's recently is that China changed its Covid policy. The image below shows the exposure of different countries to China. Germany, which continues to be Europe's engine, has the biggest exposure together with Switzerland (watches). Sweden also stands out, which is positive as people now expect accelerating growth in the Chinese economy.

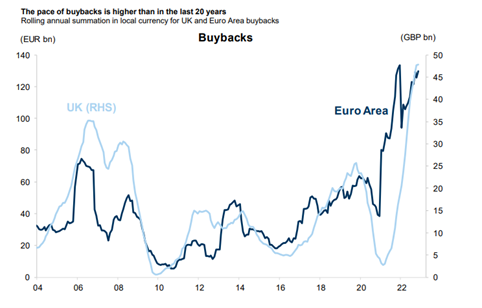

Soon the buyback programs will start again after the companies report for the fourth quarter. The levels in both the US and Europe are still very high.

Source: Goldman Sachs

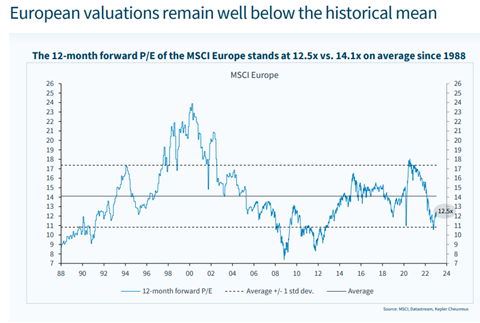

Despite a strong start to the year, European valuations are still at very low levels.

Source: Kepler Cheuvreux

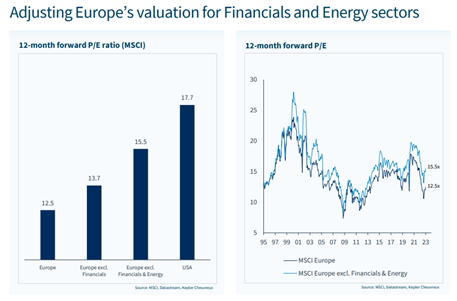

Europe has a large element of undervalued banking and energy stocks. If you adjust for these, you get the adjusted P/E ratio levels below.

Source: : Kepler Cheuvreux

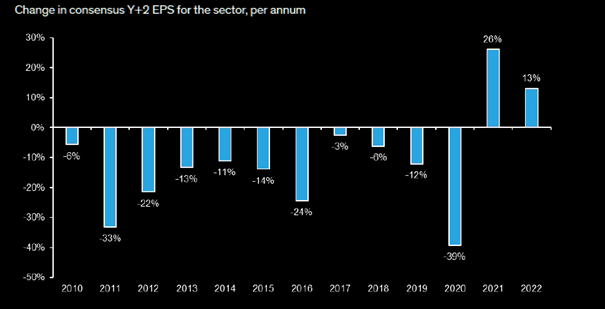

Below one of the favourite pictures of the month! It shows analysts' EPS revisions two years ahead for European banks since 2010. After 11 dismal years of earnings growth, European banks have finally started delivering profits to their hard-pressed owners. Our own Commerzbank is a shining example of just this. This could be an engine for Europe's stock markets (and economies in general) in the coming years as valuations are still at very low levels. In addition, at the time of writing, major European banks such as Italy's Unicredit and Spain's BBVA have just delivered very strong reports with large capital transfers to owners.

Source: Themarketear.com

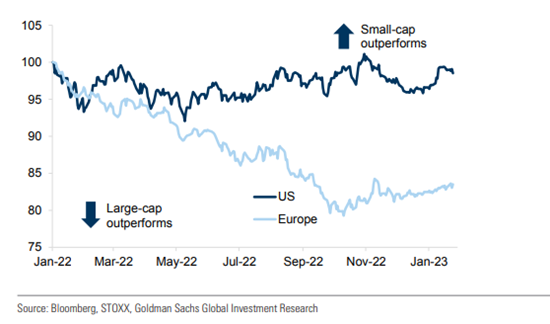

European small companies are gradually starting to recover lost ground from last year. The potential remains significant if we are to return to the same relative valuation as a year ago.

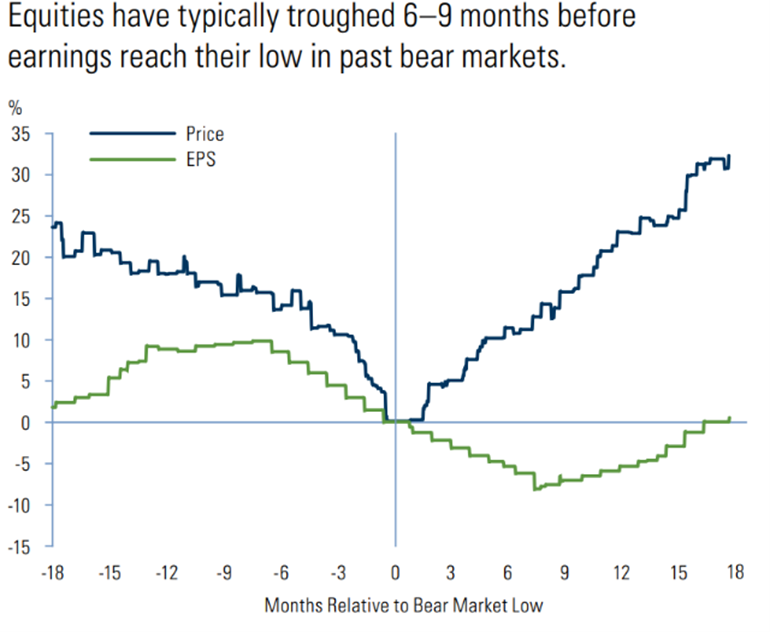

The market does not fall when a recession is confirmed. The last picture for this time shows that stocks normally reach their lowest level 6-9 months before the company's earnings reach their lowest level. The daily discussion in the financial industry is when it intends to appear. Our humble view is that there will be a slowdown in the coming quarters, but that any recession is likely to be mild.

Source: Goldman Sachs

We continue to have a positive view of the stock market, well aware that things went quickly initially. As usual, it is the companies' delivery to their owners that is the most important and we continue to have high pressure in the analysis factory with several new investments underway. February will be a report-heavy month for us, and we look forward to reading all the reports.

We are quickly moving towards brighter times and soon it will be spring!

Mikael & Team

Malmö on 2nd of Febuary 2023