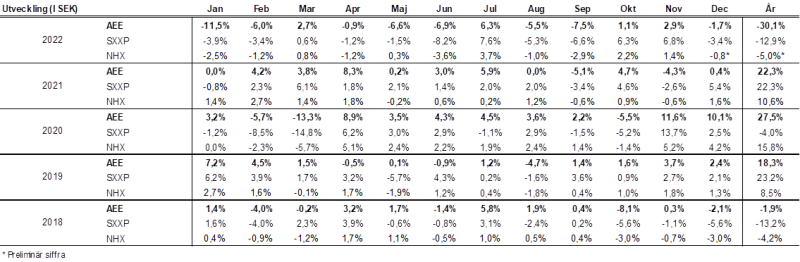

Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class' return. The information below regarding returns therefore differs from the returns in other share classes.

Before making any final investment decisions, please read the prospectus, its Annual Report, and the KID of the relevant Sub-Fund here

This material is marketing communication

Monthly Newsletter Coeli Absolute European Equity – December2022

DECEMBER PERFORMANCE

The fund’s value decreased by 1.7% in December (share class I SEK). The Stoxx600 (broad European index) decreased during the same period by 3.4% and HedgeNordic’s NHX Equities decreased provisionally by 0.8%. The corresponding figures for 2022 are a decrease of 30.1% for the fund, -12.9% for the Stoxx600 and -5.0% for NHX Equities.

EQUITY MARKETS / MACRO ENVIRONMENT

The strong development that began on November 10th, ignited by low US inflation data, was abruptly cut short when the ECB raised its key interest rate by another 50 basis points on December 15th. The day before, the FED had announced its interest rate hike, which was generally well received. The Fed's interest rate hike rate decreased and there were no negative surprises. The president of the ECB, Christine Lagarde, on the other hand, had a much more hawk-like use of language. The message was that the policy rate is expected to rise significantly from current levels as inflation is far too high and is expected to be so for far too long. This meant that the broad European index fell by just under three percent that day, and the more cyclical German index fell by nearly four percent.

On the same day, the Bank of England held a meeting where they raised the key interest rate for the ninth time this year. However, the executive board was non-consensual, which immediately weakened the British pound (again). During the day, the British pound fell by 1.5 percent against the euro and by 2 percent against the US dollar. It is a huge movement in the currency world. That day, the much-anticipated Santa Claus Rally plummeted. Measured in local currencies, the decline in December was 3.4 percent for the Stoxx600, 2.8 percent for the OMX, 5.9 percent for the S&P500 and 9.1 percent for the Nasdaq. The fund's development during the same period declined by 1.7 percent.

The stock market in 2022 has basically been completely dictated by the inflation trend and thus rising interest rates. December was no exception but was more like a crescendo of the year that had passed. It is clear that the ECB's polemics and language used on 15 December was a political fog curtain to try to hide its grave mistakes made in recent years. Having said that the best prognosis is that they will react too late this time too, with an obvious risk of unnecessarily creating an avoidable large economic damage in parts of the European economy.

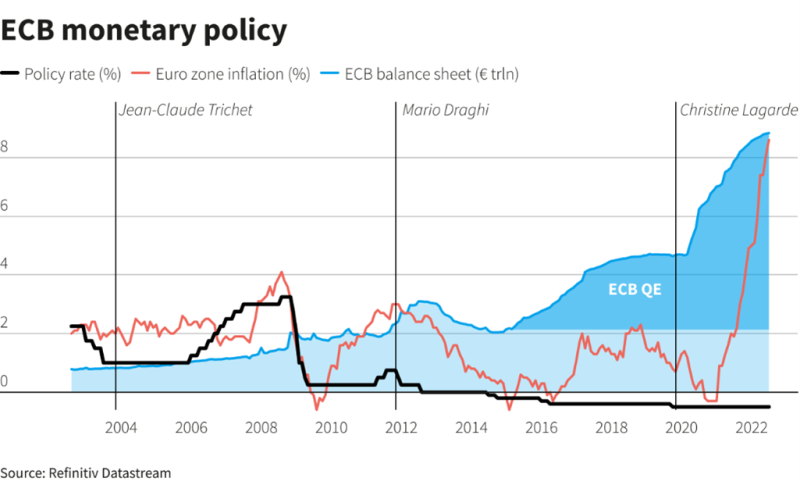

Study the image below and think about what made the ECB: a) keep interest rates high for far too long in 2008 before Lehman crashed b) had zero interest rates until 2015 and then negative interest rates for seven years c) why for the first time in 11 (!) years started raising the key interest rate only in July this year (!). When you have thought it through, you add to that that the ECB's primary goal is to maintain price stability. The policy rate is now 2.5%, inflation around 10% and the grim conclusion is that most things have gone wrong in recent years.

A more positive development is that inflation in the US is clearly declining. As recently as last summer, the view was that inflation was out of control. The other day we noted inflation forecasts from the Federal Reserve Bank of Cleveland. Their models indicate that consumer prices are now at a low rate of 0.12%, which simply means an annual rate of a low 1.4%. Read more

It strengthens our belief that inflation in the coming months will drop sharply and our humble guess is that we can be down around three to four percent by summer. IF that turns out to be true, European inflation is likely to follow with a lag of about six months and in that case the ECB (and the Swedish Riksbank) have once again been monumentally wrong in their forecasts.

Our increased exposure to the real estate sector clearly indicates what our view is, and, in a few months, we will know significantly more. A factor that is likely to have a negative impact on the reduction in the inflation rate is that the globalization trend is waning while green conversions / investments can contribute to rising inflation.

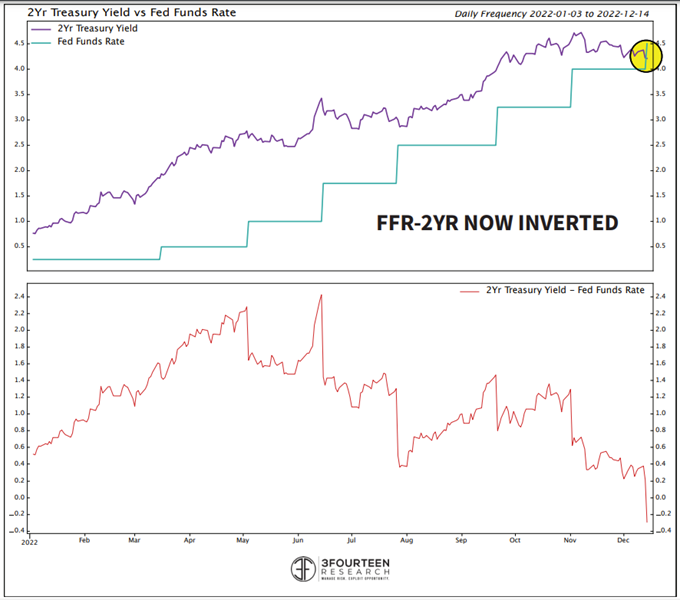

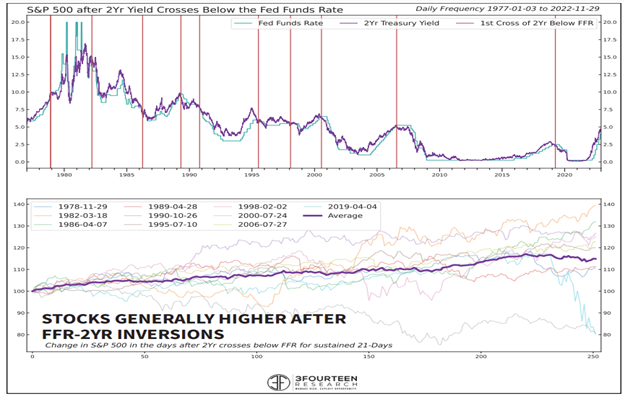

The US two-year interest rate has fallen recently and is now below the Fed's policy rate. Historically, this has signalled a shift in the FED's policy, which in turn has been positive for both bonds and stocks.

Source: 3Fourteen Research

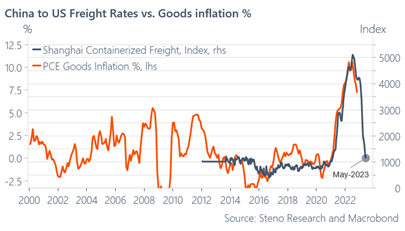

The figure below shows the correlation between a Chinese freight index and US commodity inflation. If the correlation turns out to be positive, inflation will be down around zero percent in May.

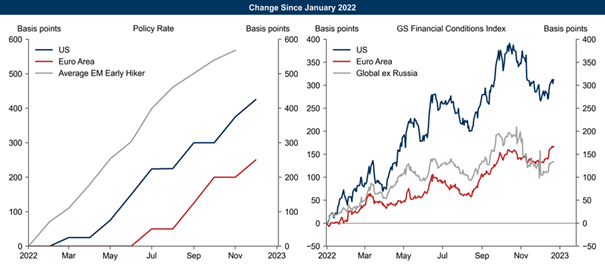

The picture below on the left shows the key interest rate for the USA and Europe and on the right the Goldman Sachs financial index where you can now see that the condition has eased somewhat in the USA.

Source: Goldman Sachs

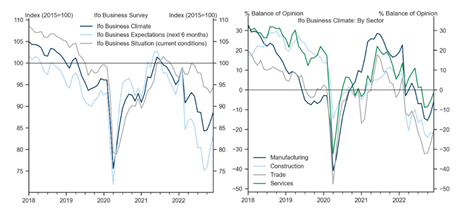

Another positive development aside from falling inflation is the resilience of the European economy. During December, the German Ifo index was published, which showed an improvement compared to the previous month. The probability of a European recession remains high, but it need not be either prolonged or deep. Compared to, for example, the financial crisis, the engine of the economy, the banks, is in significantly better condition.

Source: Goldman Sachs

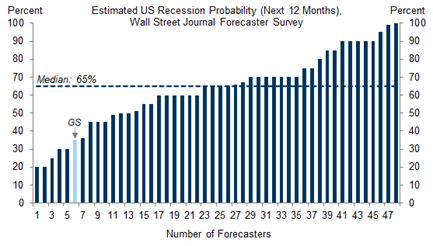

The US economy is also holding up well and Goldman Sachs gives only a 35% probability that the US economy will enter recession within 12 months. That must be considered a positive!

Is the recession discounted?

Source: Twitter

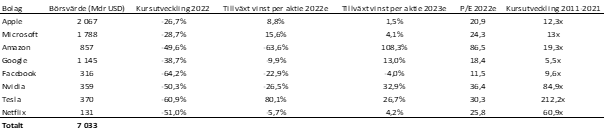

First the soldiers fell and in December the generals capitulated. Apple and Microsoft's share prices fell 13.3% and 7.3% respectively in December, while Tesla fell by as much as 38%. Elon Musk thus became the person in world history who lost the most money in the shortest time. However, he is still the world's second richest, but was surpassed in December by Bernard Arnault, founder and main owner of LVMH.

It is telling that on the first two days of the year in 2023, the broad European index had risen by just over two percent, while Apple's share price fell by just under four percent and Tesla's by as much as 12%. If you study the profit growth for these large companies, it is not so strange. Apple and Microsoft are expected to have profit growth of a few percent while the multiple exceeds 20x. Just a few years ago, when growth was strong, companies traded around 15-17x earnings and interest was lower. Notice the table below on the far right. We use x instead of percent when calculating the return and measure the return up to one year ago. There will be too many numbers otherwise, and one can conclude that a lot of wealth has been created.

Source: Coeli European

Apple's stock price compared to Alibaba and JD.Com. The latter two are giant Chinese online shopping companies. Apple's share price has fallen by 17% in two months, while Alibaba and JD.Com have risen by 67 and 80%, respectively! Apple has been loved by everyone and Chinese companies the other way around, until recently.

Source: Themarketear.com

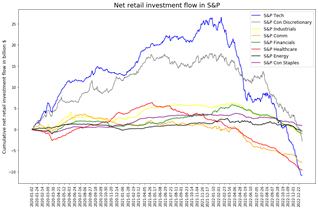

American private investors as a collective are the largest owners of American stocks. Since the spring of 2022, they have sold enormous amounts of technology shares (blue line) and, according to Goldman Sachs, have now net sold everything they bought since covid broke out almost three years ago. When does it turn?

Source: Goldman Sachs

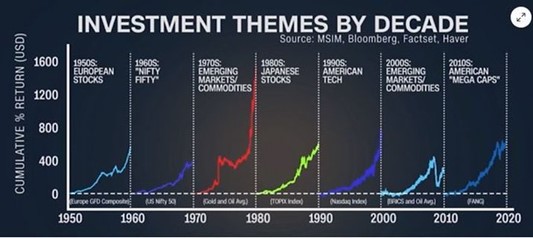

Thanks for the show! An extremely relevant question is what the theme should be for the next 10 years? Technology is likely involved in some way, but energy is also close at hand. Right now, 60 nuclear power reactors are being built in the world (440 are in operation). Of these, one is built in Slovakia, one in France and two in Great Britain. The remainder is mainly built in China, Russia, India and the rest of Asia. A further 100 are planned and 300 are proposed. It feels like an interesting sub-sector. The antipode of that, Sweden, the elected officials have chosen to shut down 6 out of 12 nuclear power plants, with enormously negative consequences for society. Traditional oil companies continue to trade at very low multiples, despite having developed very strongly in 2022. Green energy stocks will continue to be interesting, but often have high expectations priced in, which makes future returns more uncertain.

Source: MSIM, Bloomberg, Factset, Haver

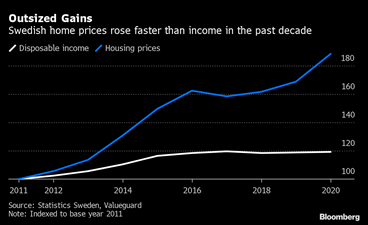

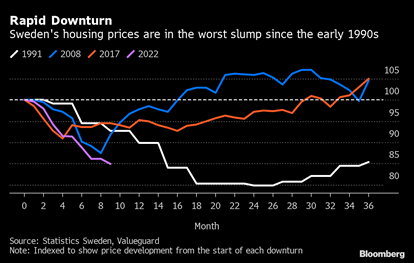

Unfortunately, Swedish citizens are among those who stand out globally in terms of vulnerability in the private economy. Sweden is international front-page news and international economists follow developments closely. Our house prices have risen more than in most other comparable countries and we are at the top in terms of loan-to-value in relation to disposable income and a high proportion of variable loans. Forecasters are now starting to think about whether the 20% expected price drop in the forecasts is enough (-17% since March 2022). The decline in the market in the early 1990s, when housing interest rates were close to 15% and the key interest rate for a few days at 500%, ended at -20.6%.

Although interest rates are still at low levels today, it is a big problem for many when the interest rate has now risen 3x in a short time. However, the real interest rate is still at very low levels (-6-7%) and at the same time inflation is eating up part of the debt. What used to be called non-durable goods (because you bought these goods less often) is going to decrease somewhat. With around 5000 billion in housing loans, it will cost the government a lot of money when the interest subsidies also rise 3x. The interest subsidies should now be around 50 billion at an annual rate (own estimate) and it was of course economic madness not to reduce the interest subsidies when we had zero interest.

Swedish real estate prices are so far maintaining the same rate of decline as during the 2008 financial crisis (purple line). This time the Riksbank will not lower rates but, on the contrary, will raise them further.

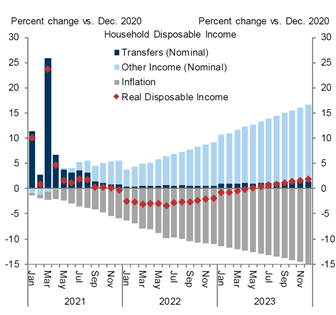

But after sun comes rain! Below Goldman Sachs estimates for the development of disposable income for the average American. Falling inflation, increased contributions and falling interest rates mean that the situation is expected to improve after the summer. For Europe, the big problem is energy costs, but Europe's politicians are likely to routinely increase national debt and give subsidies to appease their voters.

Source: Goldman Sachs

The warm weather in recent weeks has contributed to a collapse in European gas prices which is extremely welcome for Europe and prices are now at the same level as a year ago. Very good for both consumers and producers and, not least, it gives Europe extra time to build up reserves for next winter 2023–24. The following year, the supply increases, mainly from new capacity from Qatar, and things then look significantly better

Source: Bloomberg

Europe's political leaders caught up a few weeks ago when it was announced that they had agreed on a price cap on gas prices that will come into effect on February 15. The price ceiling is set at 180 euros per MWh. If it had been in place this summer, it would not have been possible to fill up the stock levels before the winter, and Europe would probably have already experienced major problems with electricity supplies to residents and businesses. The price ceiling thus limits Europe's ability to pay what is required to ensure the volumes before 2023. Another engraved and hard-to-understand solution by Europe's power elite. You have a deficit on something and at the same time you think you can dictate the price!

President Xi Jinping conceded defeat to Covid-19 after violent protests among citizens, and after a huge U-turn by Chinese leaders, society quickly opened up in December. It was all very unusual for China and suddenly Chinese could start traveling again. On the first two planes that arrived at Malpensa in Milan, 50 percent were infected and a certain feeling of déjà vu crept in. The image below shows that traffic in some major Chinese cities increased in the last week of December. The continued development here will have a major impact on global growth after almost three years of lock downs (to varying degrees).

Source: Bloomberg

In Germany on December 7th, 3,000 police officers took part in a crackdown on armed right-wing extremists who were planning a coup d'état! Terrible and crazy. The biggest crackdown on extremists ever in Germany. Democracy is unfortunately under great pressure in many parts of the world.

Relations between China and the United States are more strained than in a long time. In December, however, China and Saudi Arabia concluded a global partnership where Saudi Arabia will now start trading its oil on the Shanghai stock exchange as a first step. Both countries have, to say the least, fuzzy concepts of morality and go against the values of the entire Western world. Cheap oil from Saudi Arabia fuels the Chinese economy while China helps Saudi Arabia with technology including weapons. This probably means that the old US-Saudi Arabia axis pact is now weakening, and arms purchases from the USA (Saudi accounts for 12% of all world arms purchases!) have already decreased. It is hardly a long shot that China is prepared to help meet and thus the world order is moved a little further towards the East. Asia's population amounts to approximately 4.5 billion compared to just over a billion for Europe and the United States combined.

Finally, we unfortunately have to state once again that the Swedish krona became the worst western currency in 2022. During the year, we have all become 8% poorer compared to our European surroundings. Since 2013, the Swedish krona has decreased in value against the euro 8 out of 10 years. One euro cost SEK 8.30 in 2013 and now SEK 11.25, which is roughly 35% more.

All other things being equal, this means that investments in Sweden by the margin decrease, inflation rises via imports and qualified labour chooses to move abroad. There will be holidaying in Romania and Turkey in the future. The average salary in Denmark and Norway is at least 20-30% higher than in Sweden. We have turned into the poor cousin of the country and our elected officials stick their heads in the sand or don't understand better. At the same time, the Riksbank has sold large amounts of kronor during 2022, which contributed to the weakening and thereby increased inflationary pressure. The whole thing is like reading a Franz Kafka novel.

Source: Bloomberg

Long positions

Pets at Home

2022 was a year when consumer stocks were one of the worse categories of stocks to own. Perhaps worst of all fared the British consumer shares. Goldman Sachs' basket of UK consumer stocks fell 45% in 2022. The country has been particularly hard hit by gloomy inflation headlines. The weak pound has also made imports more expensive. And it didn't help with the uproar in Parliament, where Liz Truss's tax proposals raised inflationary fears quite unnecessarily.

You can often create excess returns by buying the finest companies in unloved sectors. We believe that the pet company Pets at Home is one of those. We picked up our first shares in September above £3.20. It turned out to be too early because the share then fell sharply in the weak stock market that started in the autumn. We seized the opportunity and increased our position sharply, bottoming out at levels around £2.64. The stock has recovered somewhat and was one of the fund's strongest contributors in December, rising 8%.

The biggest concern the market has regarding Pets at Home is whether people can afford to continue buying pet-related products. The company's management usually emphasizes that the majority of revenue comes from products that have a repetitive nature, for example animal feed or cat litter. The remaining part consists of more profitable product categories such as dog toys. These revenues will be less in 2023. But we do not think that the effect will be particularly large when Pets at Home also has a large veterinary business that will grow nicely next year. We believe the veterinary leg constitutes a third of the operating profit before group costs this year.

So far this year, they have managed to maintain growth. Comparable growth has been just over 6% in the first six months of the fiscal year ending in March. In previous recessions, the pet industry in particular has done well. In the last quarter, it even welcomed more new customers to the company's membership club for owners of kittens and puppies than it did during the pandemic. The management recently flirted with the idea that people will continue to buy pets after the pandemic as it is now known that employers are allowing work from home to a greater extent. We'll see if that thesis holds up.

In the short term, we are more concerned about the cost situation. Rising energy costs, wage inflation and a weak pound will make it tough for many retailers in 2023. Pets at Home is no exception. However, much of our concerns seems to be accounted for in the analysts' estimates today. Moreover, these are external problems that are largely (hopefully!) temporary in nature.

If you dare to take a step back, you will see a company that has amassed strong market share for several years. The company should be able to sustainably grow by more than five percent per year. This at a return on capital employed that exceeds 25%. The cash flow generated can be reinvested in store renovations at a good return.

The charm of the business model is that the company's store operations feed the veterinary operations and vice versa with traffic.

The stock now pays a low EV/EBIT of 8x on our estimates ending March 2025. A low multiple of 10x gives a potential of around 37% over 1-2 years. If we assume a multiple of 12x, the return instead lands at around 60%.

Commerzbank

The fund's best contributor in December was the German Commerzbank, whose share rose by just over 10% and thus contributed around 0.5%. It is one of the fund's most recent investments, as we started investing as late as mid-November after the stock was curiously under significant pressure following their quarterly results. The share then traded around 7.50, closed the year at 8.84 and is currently trading around 9.50.

The investment thesis was and continues to be, a combination of rising earnings as interest rates rises, a significant restructuring which contributes to strong profit growth in the coming years and that the bank can also be included in the German bank consolidation and then in the form of a takeover. The share rose 32% in 2022 but is still valued at low levels. The P/B for 2023e and 2024e is around 0.40 and the corresponding P/E numbers are just over 7x and 6x, indicating continued significant potential. In connection with the purchase of Commerzbank, we sold our holding in Nordea.

Corem

During December, we built a position in the Swedish property company Corem. The stock was among the worst performing real estate stocks in Europe in 2022, down nearly 75%. A large part of the explanation for this is Corem's bond maturities of SEK 11.4 billion 2023-2025, which of course have become significantly more expensive and more difficult to refinance in recent quarters. In addition, the main owner Rutger Arnhult has been under considerable financial stress, which has further had a negative impact. Corem is now embarking on a major restructuring where we think we see a stable underlying cash flow that the market seems to be overlooking.

The restructuring program got off to a good start when at the end of last year, they sold properties worth nearly 7 billion (in total they owned properties worth 81 billion at the end of the third quarter). A significant portion of the sale proceeds will be used to settle upcoming bond maturities and we expect the restructuring to continue this year. Worth noting in this context is that only 25% of Corem's debt is bonds, which is less than many other listed real estate companies, and that the amounts in relation to the total loan market are not significant. The equivalent for, for example, Balder is 60% and 74 billion. Corem has a reasonably stable and strong cash flow and the share costs around SEK 10 compared to the latest net asset value of just under SEK 30 which, in our opinion, today's valuation does not reflect.

Private Investments

After updating our valuation model in December, we chose to reduce the valuation of Rejuveron by approximately 10%. The main reason is rising interest rates. Our initial investment was made three years ago at CHF 19 per share. Last spring, the company took in more capital at CHF 120 per share and added additional capital at the same valuation in July. Our holding is now booked at around CHF 90 per share. Our Bullish holding went in the opposite direction after we exercised a repurchase clause at a premium. Our investment was made at $100 per share and the valuation rose to $114 per share. The total negative contribution was approximately 0.6 percent in December.

Short positions

The short portfolio contributed with a positive result during the month. The biggest contribution was made by our short positions in a Swedish small company index and in the larger Swedish OMXS30 index.

Exposure

The net exposure, adjusted for our unlisted holdings, at the beginning and end of the month was 79% and 72% respectively.

Summary

With the conditions that were presented in December, we are reasonably satisfied with the month. The fund fell by 1.7% which includes a write-down of a total of -0.6% in our unlisted holdings. In addition, the performance was affected by a record weak Swedish krona and the weak British pound. The aggregate negative contribution from currencies in December in isolation was approximately -0.8% and underlying performance for our holdings was therefore, in a market which fell by 3.4%, approximately -0.2%.

We have left a heavy and challenging year behind us. The war has made us all sad and it has contributed to high volatility and stress in the financial system, which in turn has greatly affected the fund's performance. We are of course deeply disappointed with last year's returns and our big mistake was not being aggressive enough in the first quarter to sell out previous years' winners. The common denominator for these companies was simplified: smaller companies with a strong return over a longer period of time, high multiples and growth companies. As much as 60% of last year's total loss came during January and February.

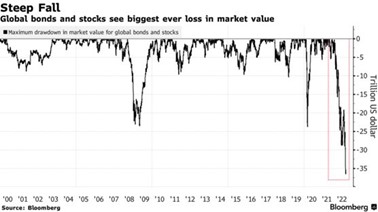

On the global stage, losses in total value were greater than ever before. Both stocks and bonds had an extremely weak year.

Since then, we have worked methodically to change the structure of the portfolio. Compared to a year ago, the portfolio is significantly different with a materially higher exposure to larger companies with lower valuations and more predictable earnings. A third of the fund's capital is currently invested in ISS, Tate & Lyle, Accelleron, BoneSupport and Commerzbank. With the exception of BoneSupport (growth company), the absolute valuation is low (Tate & Lyle) or very low (ISS, Accelleron and Commerzbank). A year ago, the largest holdings for the fund were: CVS, Lindab, Victoria, Surgical Science and Truecaller. Lindab continues to be a significant holding for the fund, and we have been an owner since summer 2019.

Volatility for the fund has gradually decreased during the fourth quarter, while the return has improved. In addition to the gradual improvement of the market, it leads us to believe that our adjustments to the portfolio were correct. We also note, with a large dose of humility, that as weak as last year started for the fund with 6 negative days in a row, this year has started just as strongly. But at the time of writing, we have only harvested one percent of the trading year.

With all the above said, how do we see 2023? It will be significantly better than 2022 is the short answer. So far, the decline in the stock market has been almost exclusively about valuations coming down. The companies’ earnings capacity has surprised positively so far and since late summer we are now in the next phase of the decline process which is about how much the earnings will fall before the market turns up again. Here, the differences between companies and sectors will be enormous and we will have to navigate the landscape before we are out on the other side. But this is a significantly better environment to work in as a stock picker, compared to large parts of last year (especially the first half of the year) where share prices fell across the board.

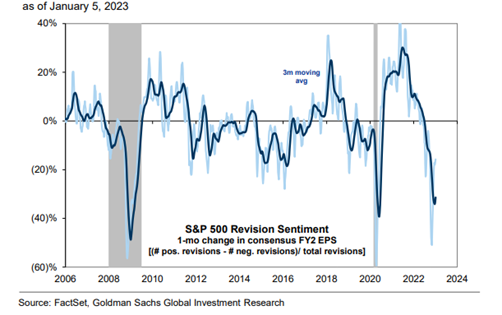

A graph from January 5 of this year shows the one-month trend of earnings per share for the S&P500 2024e. With a whopping 31% downward adjustment, it is the sharpest downward adjustment of the profit estimate since 2008 and 2020. The market has therefore in a short time begun to prepare for expected sharply declining profits.

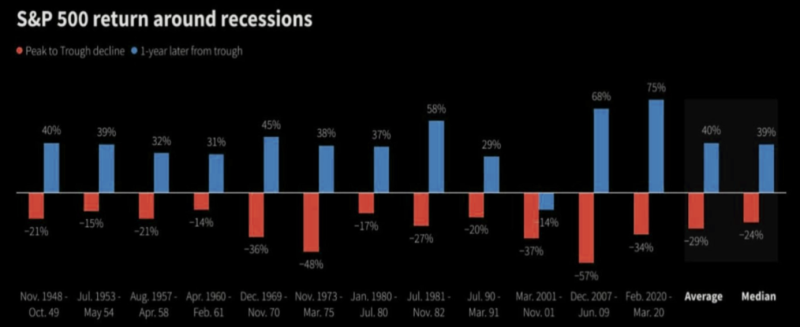

The image below shows how the stock market has developed since 1948 in periods of time around a recession in the economy. The median decline from the highest level has been 24% and the rise thereafter 39%. The decline as it currently stands is 25%.

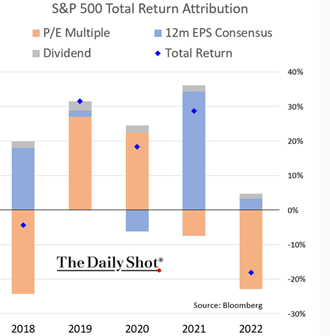

Below is an excellent illustration of what drives share prices in different years and in different conditions. 2020 clearly shows that it is possible to have a positive return one year despite the fact that companies generally have declining earnings. An even better example is 2009. Our assessment is that we will have a positive year in 2023, driven primarily by rising multiples despite declining earnings. That is, the reverse relationship compared to 2022.

Source: The Daily Shot

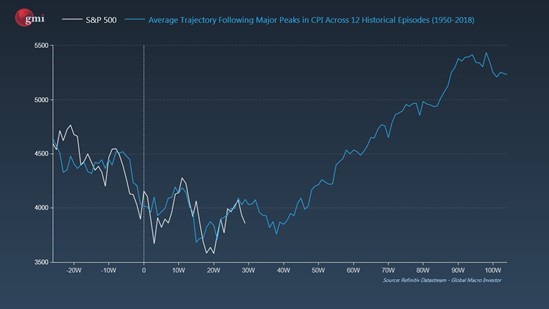

Historical data from 1950-2018, but zoomed in on a weekly basis, shows how the stock market in the US developed after inflation reached its highest level (0 on the x-axis). It doesn't necessarily have to be that way this time, but it is likely that inflation has already passed its highest level. Should history repeat itself, we have a 25% rise ahead of us in 2023.

Source: Julien Bittel, gmi

The image below shows that when the US two-year interest rate has fallen below the policy rate, the stock market usually rises by an average of 15% after 6-9 months (purple line).

Source: 3Fourteen Research

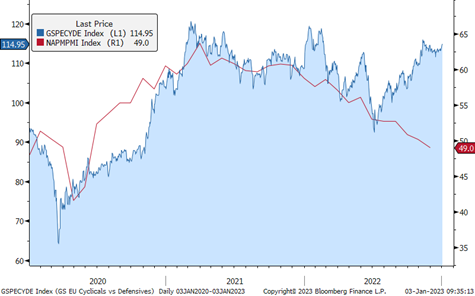

A good barometer of the stock market cycle is the difference in price development between defensive companies and cyclical companies. Cyclical companies have performed about 25% better than defensive companies since last summer, despite all economic doomsday prophecies.

Source: Goldman Sachs

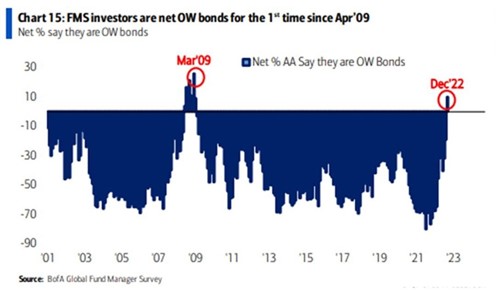

Investors are overweight bonds for the first time since March 2009 (!). The interest rate must go down!

The coming and announced recession among economists and strategists is the most anticipated we’ve experienced in almost 30 years. The cash balances of the world's investors have until the turn of the year been at record high levels, people are gloomy and short positions in many companies are at very high levels. The market view is that it will fall another 10 percent in the first half of the year, and then turn around.

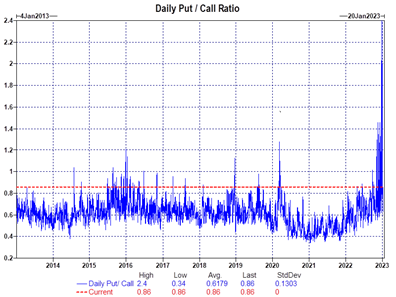

The exceptional image below shows the explosion in the purchase of put options over the past month. Not even during the financial crisis was the relationship between put options / call options as skewed as at the end of 2022. The investor collective was prepared for a sharp decline and instead 2023 has had the strongest start since 2009. This in turn creates stress for the investor collective who have a lot of cash and in many cases too defensive holdings and many have not even finished the Christmas break.

Source: Goldman Sachs

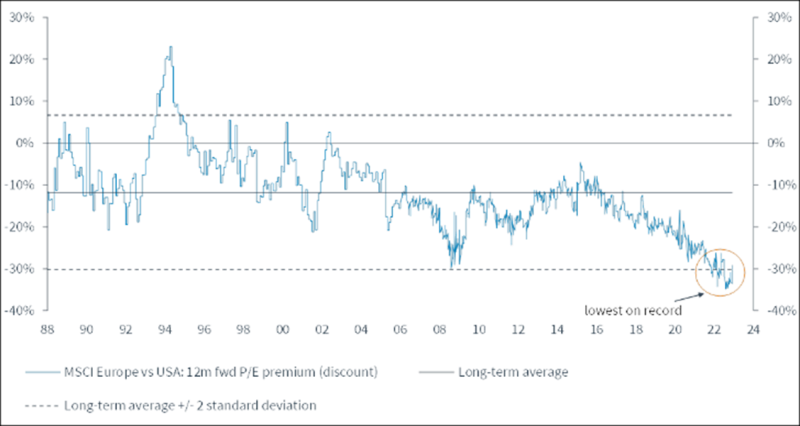

We have a strong opinion that the conditions for European shares compared to American ones are better than they have been for a very long time. Below, a time series from 1988 that speaks its own language, showing that the valuation difference has never been greater. Add in a continued strong dollar that is expected to decline as interest rates move lower. At that point, the risk premium will probably also drop, which in that case gives a double effect.

Source: Joakim Tabet Kepler Cheuvreux

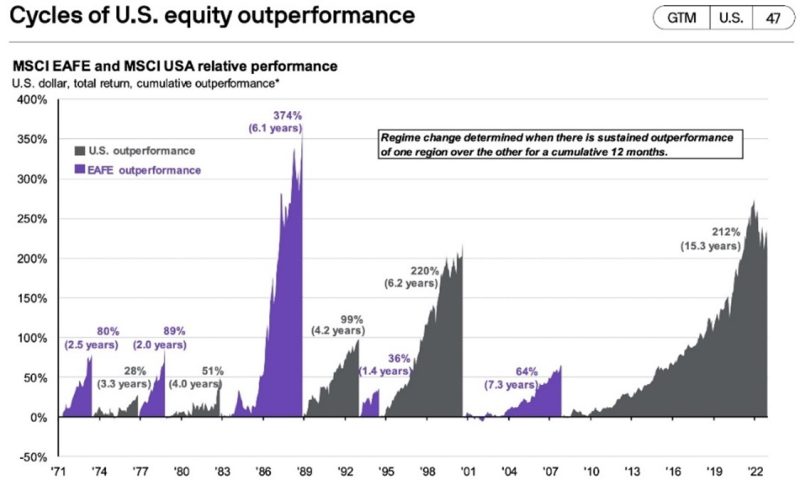

It feels like it's time for a purple bar in the chart below. According to recent data from Goldman Sachs, there were outflows from US equity funds in the first week of 2023, which is unusual.

Source: JPM

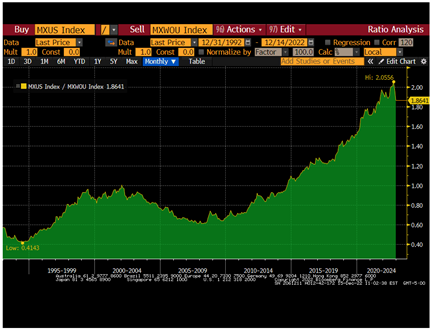

US stocks relative to global stocks since the early 1990s. Note the decline on the far right of the graph. Something happened at the end of 2022.

Source: Bloomberg, Goldman Sachs

The white line below shows the relationship between the Eurostoxx and the S&P500. The green line is the price of gas. Since the start of October 2022, Eurostoxx has performed 15% better than the S&P500. At the same time, energy prices have fallen sharply.

Source: Bloomberg, Goldman Sachs

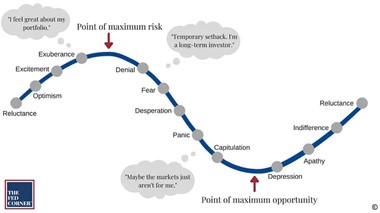

It is easy to state that the point of maximum risk in the classic image below was in the fourth quarter of 2021. That changed literally overnight on January 2, 2022 when American long-term interest rates suddenly started to surge upwards. We note that this year, since a few days back, has started with a diametrically opposite trading pattern. Country after country is now showing signs of declining inflation, and China has made the biggest U-turn ever in their Covid policy, dramatically increasing the chances of an economic recovery.

So where are we in the cycle? One data point is that the stock market generals of the last 10 years, US megatech companies, finally capitulated at the end of 2022. A blowout is almost always necessary to clear the air and begin a gradual recovery. Our best assessment (simplified) is that it is well illustrated in the picture above and we have since two months ago, as communicated in the last two monthly letters, a significantly more positive attitude towards the stock market.

Should we be right in the above, we have rolled into the point of maximum opportunity. Today's situation, with in many cases very low share prices and lethargic investors, is largely similar to the landscape as it looked in the spring of 2003 and the spring of 2009. An important difference then compared to now is that we do not have the central banks with us.

The last question then becomes how long does the point of maximum opportunity last? The ingredients and response to it is a cocktail consisting of inflation, central banks and geopolitical developments, but this phase in a cycle usually lasts 6-12 months and offers some turbulence at times.

The headwinds for an upswing continue to be that Europe is heading for recession and that central banks are raising interest rates too much. The tailwind is that country after country is now reporting falling inflation, expectations are low, investors are sitting with excess cash and stocks are underweight, and that the persistence of corporate profits has proven to be significantly more resilient. That you should take more risk now than you did in the last year appears to be highly reasonable.

In conclusion, I would like to extend a big thank you to Cecilia, Fredrik and Gustav who, despite headwinds during the year, have always remained focused on taking us forward and improving our business.

We wish all our readers Happy New Year and success in 2023!

Mikael & Team

Malmö on 10th of January 2023