Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class' return. The information below regarding returns therefore differs from the returns in other share classes.

Before making any final investment decisions, please read the prospectus, its Annual Report, and the KIID of the relevant Sub-Fund here

This material is marketing communication

Monthly Newsletter Coeli Absolute European Equity – June 2022

JUNE PERFORMANCE

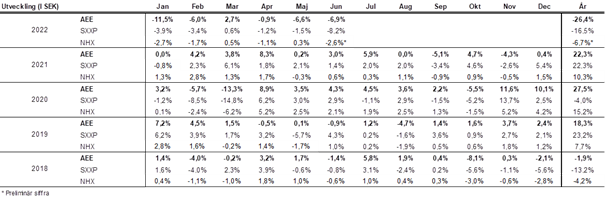

The fund’s value decreased 6.9% in June (share class I SEK). The Stoxx600 (broad European index) decreased during the same period by 8.2% and HedgeNordic’s NHX Equities decreased with preliminary 2.6%. The corresponding figures for 2022 are a decrease of 26.4% for the fund, 16.5% for Stoxx600 and 6,7% for NHX Equities.

EQUITY MARKETS / MACRO ENVIRONMENT

Those with good memory remembers the strong end to May, which was followed by a calm beginning of June. It lasted only a week and then a new turbulent period began. It was more of the same as earlier in the year with poor inflation data and a rising fear of its consequences. The turbulence reached storm strength a few days ago when spreads in the credit market rose sharply. As usual, it was the biggest budget sinners who felt the most. Below is the Italian 10-year interest rate and two things are clear. First, the sharp rise in the first half of June, which was followed by an equally sharp decline in the second half. We'll be back soon on why.

Source: Bloomberg

It also became degradingly clear how far from reality the central banks have been, and it is best shown by our own Riksbank (Swedish Central Bank) which last week made its first double increase (50bp) in 22 years. It is only a few months ago (!) that the same Riksbank announced that an interest rate increase would not take place until the second half of 2024. Both astonishing and incomprehensible. The Fed made its first triple increase (75bp) since 1994 on June 15th. The ECB is expected to raise rates in July and in anticipation of this they will continue with their asset purchases in the market…

The Executive Board of the Riksbank is appointed by the General Council of the Riksbank, which in turn is appointed by the Riksdag. The Riksdag is led by the government, which is in full swing desperately sending out checks so that people can afford to pay electricity bills, refuel the car, etc., which, all other things being equal, drives inflation. Say what you will, but economics and politics are not directly like a Swiss clock movement. By the way, Switzerland also raised the interest rate for the first time since 2007 by 25bp. Inflation there is a moderate 2.9%. A small, export-dependent, and well-managed country of the same size as Sweden. The difference in the development of each currency says a lot. In the last 50 years, the Swedish krona has lost just over 90% in value against CHF. Imagine if the summer holiday in Mallorca would cost SEK 5,000 instead of SEK 50,000. In just seven months, the Swedish krona has fallen in value by 23% against the US dollar! We will not ruin your possible holiday abroad and leave the subject quickly.

The picture below shows the US two-year interest rate since 2016. This is one of the better pictures when looking for an explanation of the development in the world's stock markets over the past 2-3 years. Also note the sharp decline that has taken place in the past week.

Source: Bloomberg

Another explanatory picture of how the stock market correlates with the fixed income market. The S&P500's development in relation to the inverted US two-year interest rate.

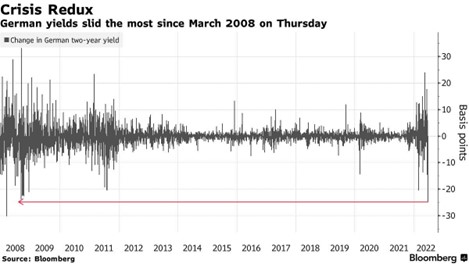

What happened at the end of the midsummer week (third week of June) was simply that the market went from fear of inflation to fear of recession. The opportunities for central banks to avoid a recession are becoming increasingly difficult, and the decline in long-term interest rates is a clear indicator of this. As an example, the US 10-year interest rate, in just 10 days, has fallen from 3.5% to 2.8%. Below is the same drama, but for the German two-year interest rate. Largest decline since the financial crisis in 2008.

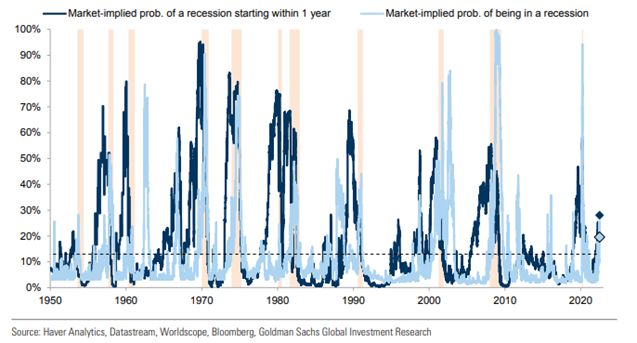

The risk of a recession within a year according to Goldman Sachs is now close to 30%.

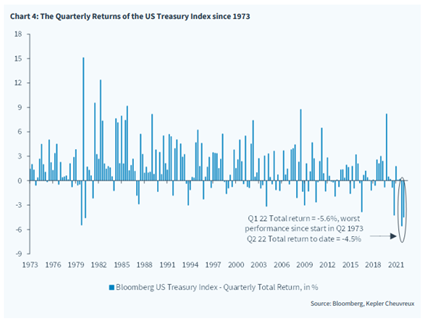

It is not just in the stock market that a sharply rising interest rate has had an impact this year. US bonds (looking more or less the same in Europe) have had the worst development since data from 1973. The end of the first six months, however, finished strongly when interest rates fell sharply.

Source: Kepler Cheuvreux

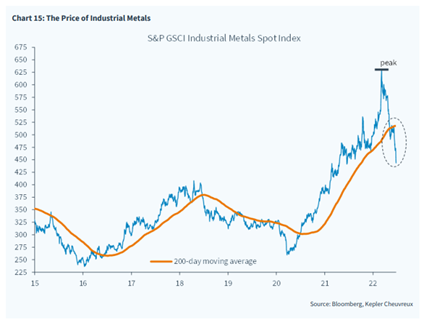

Another excellent indicator is metal prices, where copper is the best economic indicator. During June, the price of copper fell by 13% and most raw materials (except oil) have fallen sharply since the price peaks a few months ago. It is, of course, gratifying in many ways and helps to curb inflation.

Source: Kepler Cheuvreux

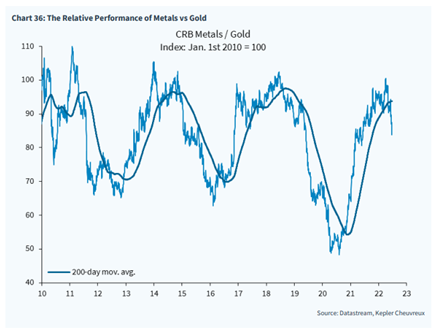

A longer time series that shows the relative development between metals ("growth") and gold ("secure supply").

Source: Kepler Cheuvreux

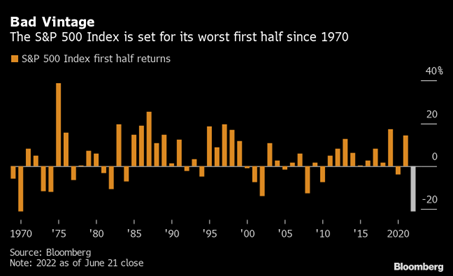

If one is to summarize the development of the first half of the year in the stock market and put it in a historical perspective, it has been an extremely challenging six months. The last time the US stock market had such a weak start to the year, Richard Nixon was president. The technology-heavy Nasdaq index is down 30% during the same time period. An American 60/40 portfolio (equities/bonds) had its second worst start since 1900, i.e. 122 years ago! Only the depression of 1932 was worse. The Swedish small company index has fallen by about 31-33% and the real estate index by as much as 46% in six months.

But after sun comes rain, right? The picture below is from June 11th, when the S&P500 had fallen by about 18%. It was then the fourth weakest start of the year ever. When June ended, the corresponding figure was about 21%. Only the year of the Depression of 1932 and World War II in the first full year of 1940 were worse! Reality (our view) is not so bad, but we are recovering from the greatest party of all time with a monumental hangover. To cheer you up a bit on the day after, on all occasions below, the return during the second half of the year has given a good positive return, something we believe will also be the case this time. We will return to that.

Source: Compound

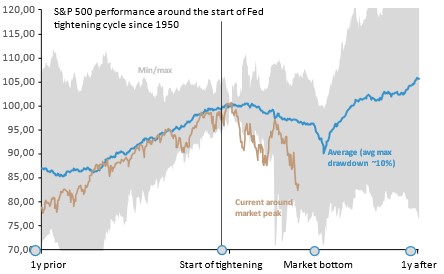

Another picture to further understand the power of this year's decline compared with other periods when the Fed began to raise the key interest rate. Data is from 1950 onwards. The decline this time is significantly stronger than the historical average and the picture also illustrates that we are close to the time when we have historically had a lasting rise.

Source: UBS

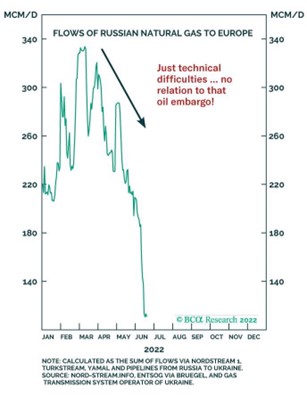

It looks like it will be a cold winter, especially in Germany. The Russians claimed that it was maintenance work that caused the gas to be throttled in June. It was, of course, a lie like everything else coming out of that country.

Source: BC@ Research

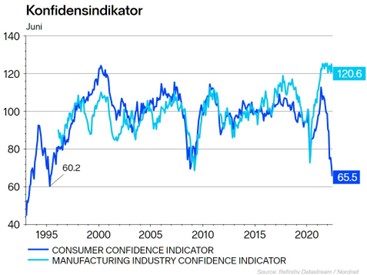

All of the above means that people are seriously depressed, while manufacturing is still in a good mood. The curves will converge again in the coming quarters (our view).

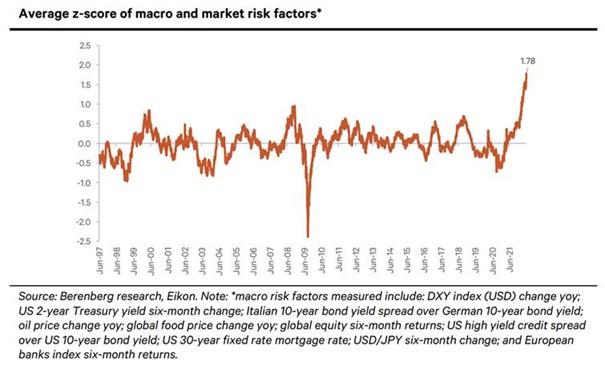

Berenberg has compiled a number of different factors that together form the micro/macro graph below. The conclusion is that we are currently in a perfect storm and therefore people are depressed as the picture above shows.

The Eurozone manufacturing and service PMI (Purchasing Manager Index). It is clear that activity has fallen this year but is still over 50 which indicates growth.

Source: Kepler Cheuvreux

Here at home, most people continue to be amazed at the political development. The political savage and former guerrilla soldier Kakabaveh who sits in Sweden's Riksdag and at least for us ordinary people give the impression of not only having Sweden and Swedish citizens in focus, has since last autumn had a major impact in Swedish politics. That she, expelled from the Left and a pronounced Marxist, has such a great influence on the biggest change in Swedish defence policy in 200 years is nothing but a disaster and internationally deeply embarrassing. It seems that the Social Democrats finally pulled a stop loss and broke agreements with her so that Turkey (an authoritarian alpha male who has an extreme influence over Swedish politics right now) agreed to begin the process of becoming a full member of NATO. Kakabaveh was named Swede of the Year 2016 by the magazine FOKUS. Thanks for the coffee!

Source: Steget efter

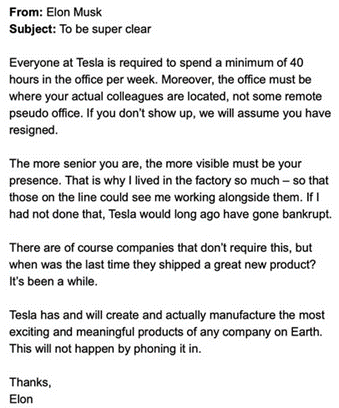

Two years ago, Zoom's market capitalization was greater than Exxon's. It feels very distant.

Elon Musk: to be super clear

Source: Twitter

Long positions

There were unusually few company specific news during June, but here are some events worth mentioning.

Tate & Lyle

Tate & Lyle (T&L) presented its year-end report in June, which was in line with expectations, including the guidance for 2023. The “Sucralose” business segment has previously been a cash cow without growth for several years. Interestingly, the business grew 15% in 2022, despite both price and currency headwinds. This was driven by continued market growth, but also an accelerated trend to use domestic suppliers where Tate & Lyle is the only player in the production of Sucralose in North America. We continue to like the stock, which has now begun to be revalued against its historical multiples, despite a significant discount to other ingredient companies. The share has risen about 15% this year and is now traded at P/E 16x for next year's profit.

Getinge

Getinge gave the market a real cold shower in the June heat when they adjusted down the forecast for 2022. We had a relatively new position that we halved just before the profit warning came in that evening. The previous forecast was a growth of 4-6%, but now sales are expected to be in line with 2021. The long-term goals remain. The share has almost halved since the earnings report in April, but we, like the market, look beyond 2022 and think that Getinge is now attractively valued. In addition, their business is relatively cyclical. Several insiders bought a lot of shares during May and June. The share has since risen by just over 15% and is traded at P/E 13 on next year's profit.

Lindab

Lindab held a capital market day in Grevie where we participated. Even though we have followed the company for several years, it was a good exercise which gave us and others incremental knowledge. In general the management team gave a confident impression and the demand for its products, which is somewhat late cyclical, remains strong . The share traded down as much as 22% in June and is down 55% this year. That is significantly more than many relevant peers and we believe it is clearly excessive. If we look forward a little, Lindab's business is driven by continued and intensified interest in sustainability and energy consumption.

The company is trading on single-digit forward-looking multiples, even though analysts have now begun (as we expected) to adjust down the estimates for the coming years. CEO Ola Ringdahl has done a fantastic job within the group, and we struggle to see that this would be a bad investment at these levels.

Short positions

The short portfolio gave a significant positive contribution in June at +3.6%. Many of our stock specific shorts was under a lot of pressure. Our negative position in SEM Small Cap gave isolated a contribution of +0.8%. Our largest contribution came from our put position in German DAX which added +1.0% to our result. We have now sold some of the options with a high delta and bought some with a lower delta. It has increased our net exposure somewhat, but our notional position has increased. Today we have a total position in puts in notional value of slightly more than 40% compared to our normal size of 30%.

Exposure

The net exposure, adjusted for our unlisted holdings, at the beginning and end of the month was 62% and 52% respectively.

Summary

After the first five months, the start of the stock market year was a record low. In June the trend accelerated, and we had to make do with the worst month of the year. Below is a selection of indices and their development in June measured in local currencies:

- SXXP600 -8.2%

- DAX -11.2%

- S&P500 -8.4%

- Nasdaq -8.7%

- Stockholm main index -11.8%

- Carnegie small cap index -14.5%

- Carnegie real estate index -26.2%

These are very sharp declines by all measures and the power at the end of the period surprised most, including us. It even becomes difficult to put on new short positions when share prices in most cases plummet. The fund was down -6.9% and few holdings made a positive contribution during the month. There was a negative price development from all sides with Lindab as the largest negative contributor. The few stocks that made a positive contribution were Tate & Lyle (+13% YTD), the London Stock Exchange (+10% YTD) and LVMH (-20% YTD) which we sold at just over 600 euros and bought back at around 545 the following week. The share closed the month at 582 euros and was thus down just under 3% per month. Enormous movements even for one of the world's largest companies such as LVMH.

So how do we think the second half of the year will turn out? The short answer is significantly better, but we will try to go through the conditions below.

The picture below shows the sector distribution and its development during the first half of the year. There has only been one sector to hide in during the first half of the year and that is the oil companies. The combination of sharply rising oil prices, a forgotten and undervalued sector, has attracted a lot of capital this year. Oil is also very political, which we have all become painfully aware of this year, and given the geopolitical situation, the risk premium has decreased. Even we, who are usually not interested in a sector where neither we, nor the companies, can influence the price of the product, have allocated capital to the sector and we have since February a medium-sized position in French Total (+12% YTD). With a constantly rising profit estimate, the share is traded according to consensus at 4.2x P/E 2022e. A high dividend and substantial repurchase mandates contribute further. The market capitalization is just over EUR 130 billion, which corresponds to almost six Ericsson and the company is expected to earn EUR 12 billion in the second quarter alone.

Source: Bloomberg

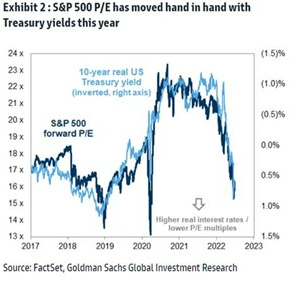

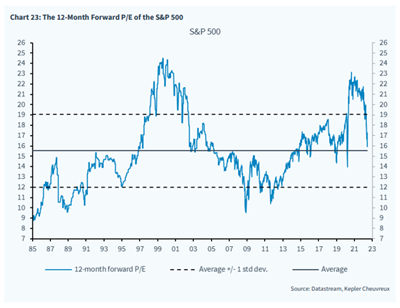

Falling rates have pushed multiples down considerably. Below is the S&P500 which is now at about 16x the next 12 months' earnings. It is a historical average based on almost 40 years of data. From 1985 to 2008, we had a completely different interest rate situation than today. Another relevant comment (we think) is that if you remove the largest technology companies (Apple etc), the other 495 companies are traded significantly below 16x. The corresponding multiple for Europe is currently around 12-13x, which is very low. The summary of this is in our opinion that 1) the multiple contraction is largely completed 2) now comes the next challenge in how much and where the estimates should be adjusted down.

As you can see in the picture below, analysts have trimmed their earnings expectations throughout the year, and especially recently. In the United States, however, not much has happened yet. The clip below the picture is from June 29, where CNBC gives an update on the profit estimate.

Here you can watch the clip from CNBC.

As you know, people are very depressed, and one can perhaps understand that. Many are of the opinion that we should go down another 10-15% before it turns around. We are not of that opinion, but still believe that we will tread around down here over the summer and then have enough inflation data that will stabilize the PMI and fixed income market, which will then be able to lift the stock market.

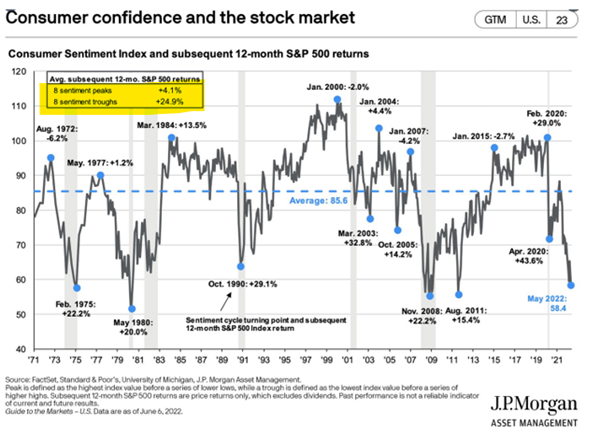

It is darkest before the sun rises. Fifty years of data on consumer confidence and returns on the stock market are shown below. On eight occasions, confidence has been at its peak, which has led to a return of a mediocre +4.1% in the next twelve months. On the eight occasions that confidence has bottomed out and most have thrown in the towel the return was +24.9% during the same time period. In addition to remaining humble, it is important to be able to look up. It is in periods like these that you make the best investments. It did not look brilliant in March 2003 or March 2009 either, but what a return was waiting. No guarantees that it will be like this this time, but if, for example, a small company index falls by 15% in one month, that says a lot about the optimism in the market.

In addition to the above, one can draw two conclusions from studying previous inflation peaks in the United States from 1940 onwards. The bad news is that the probability of a recession following an inflation peak is close to 50%. The good news is that when inflation peaks, the stock market tends to rise regardless of whether there is a recession or not.

The challenges in the market up to the peak of inflation are often significant with clearly negative sentiment among investors and rising interest rates. The central bank is putting the brakes on, the stock market is moving south, and the fear of recession is rising sharply. It is an excellent summary of what it has looked like this year and if history provides any kind of guidance, it is on these occasions when inflation peaks that you typically get a strong return in the coming years. Take, for example, Lindab, which has fallen by 55% this year and is trading around 10x P/E this year. If the share rises 50% from here, we are back where we were at the beginning of May. It had been a non-event and it still would have been down nearly 30% on the year.

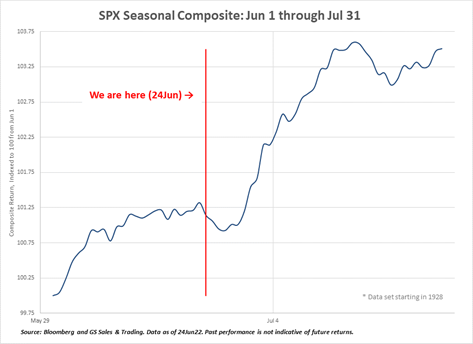

In the short term, it is currently impossible to have a strong opinion, but the picture below shows that the first two weeks historically are the best two weeks of the year. Best not to promise anything, but soon we will know more.

Source: Goldman Sachs

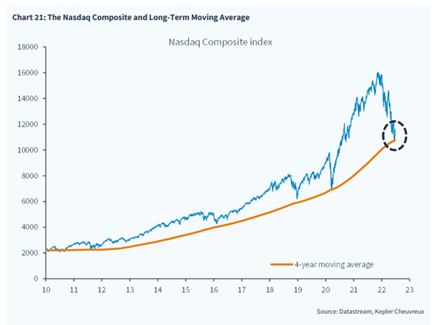

The sharp decline on Nasdaq has meant that the levels are just around a 4-year rolling average.

When June came to an end, we received inflation data from Spain which showed a new high level of as much as 10.2%. Germany, on the other hand, received lower inflation for the first time, 8.2% against the expected 8.8%. Apparently, there were one-off effects that included free local transport (it is unclear what would be cleared for this), but a step in the right direction.

On June 30th, data came from the US showing lower private consumption for the first time and on July 1st, several different economic data showed that activity is retracting (from high levels), which caused the US market to regain momentum and rise.

We repeat our view from recent months, but with an addition. We have had a view that the low level in Europe was set on March 7th. Some (not all) of the major European indices have now just traded below that level, so this thesis is currently under some pressure. In other respects, we still believe that we are around maximum inflation levels right now and that the interest rate has peaked. We also continue to believe that we need a few more months before we can consider whether we can now have a more lasting upswing in the stock market. We are now rolling into the most exciting reporting season in a long time, and it will be very interesting.

Finally, we are pleased and very proud to announce that our team has received a new substantial European equity mandate for a large sovereign wealth fund. We have received this mandate in the absolute highest international competition, and we want to believe that it has to do with all the excess returns we have created for many years. We are well aware that we have not created any added value so far this year, but we have been through periods like these at least three times before in the last 20 years or so. The holdings in the new mandate will reflect this fund's large long positions well and we will go live on August 1st. We also take the opportunity to thank Coeli, who is now putting a lot of effort into the implementation.

We wish you a really nice July and we will hear from you again in a month.

Mikael & Team

Malmö, 6th of July 2022