This material is marketing communication.

Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class’ return. The information below regarding returns therefore differs from the returns in other share classes.

Before making any final investment decisions, please read the prospectus, its Annual Report, and the KID of the relevant Sub-Fund here.

May Performance

The fund’s value increased by 3.3% in May (share class I SEK), while the benchmark increased by 2.2%. Since the change of the fund’s strategy at the beginning of Septemer this year, the fund’s value has increased by 21.7% compared to an increase of the benchmark by 9.9%.

Source: Coeli European

* Adjusted for spin-off of Rejuveron

** Includes September 1 (strategy change to long-only implemented September 4 2023)

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

Equity Markets / Macro Enviroment

The fund had a good month, rising 3.3% compared to our benchmark which rose 2.2%. The corresponding figures for the full year are 14.0% and 9.2%. The three biggest contributors to May's results were BoneSupport, Biotage and Diploma which together made a positive contribution of around 2 percentage points. The three weakest were all Italian in the form of Carel, Campari and Stellantis which together made a negative contribution of around 0.5 percentage points. More about this under the portfolio company section.

In simple terms the past month's development can be described as a strong first half, mainly driven by falling interest rates. After that, interest rates rose again, and the stock market came under some pressure. On the last day of the month, US inflation data was reported in line with market expectations and thus another step in the right direction. The stock market is still largely in the hands of the fixed income market. Below is a one-year development for the US 10-year interest rate.

Source: Bloomberg

If you zoom out a bit and study the US stock market you can see that the beginning of the year, the first 100 days, have been the best ever during an election year. Since 1950, there have been 21 occasions when the S&P 500 rose more than 10% at the end of May. Only on two of these 21 occasions has the return been negative at the end of the year. It was in 1987 (-13%) and 1986 (-0.1%). The median return for June-December on these 21 occasions has been just over 13%. History thus clearly points to a continued strong stock market.

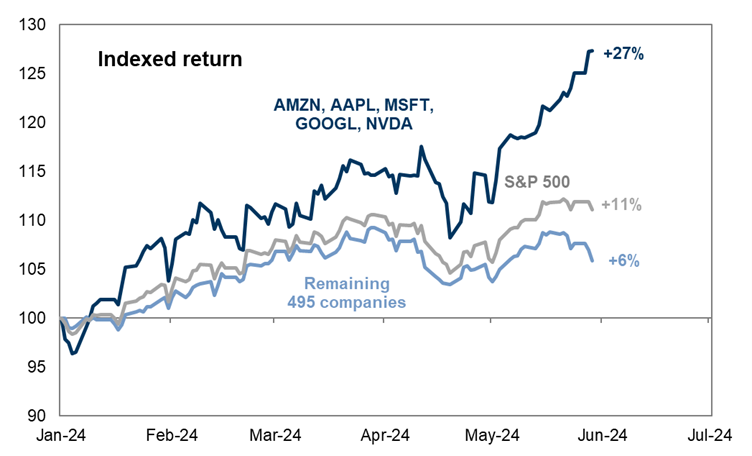

Note that the contributors to this year's return in the US are still very concentrated to the large technology companies where Nvidia has, in record time, become the world's most important stock. The return for the other 495 companies included in the index is a modest 6%.

Source: Goldman Sachs

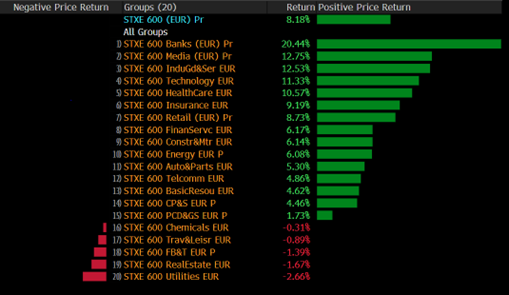

The European stock markets are keeping up well and sector-wise it is banking that is, so far, the clear winner. Banking is the best sector in Europe for the third year in a row.

Source: Bloomberg

We note that the clear losers among the European banking stocks are the Swedish ones with a mediocre or even negative return so far this year. Our own Commerzbank, which came out with its quarterly report at the beginning of May, rose by a further 11% and has thus risen by 46% this year including dividends. Since we made our first investment in November 2022, the stock has risen by just over 100% excluding dividends. Outstanding for a former chronically ill stock.

Below is the price development for Commerzbank since 2006, the year before the financial crisis began. This is how it looks for many European bank shares and with the best conditions in 20 years there is some potential. The 100% that we earned can barely be deduced in the picture below. It is also a big reason why Europe lost so much competitiveness after the financial crisis. The European banking index is still 60% lower than before the financial crisis. JP Morgan has risen by 400% during the same period. Compared to the US, there has been a lack of capitalism and too much regulation and stagnation in Europe.

Source: Bloomberg

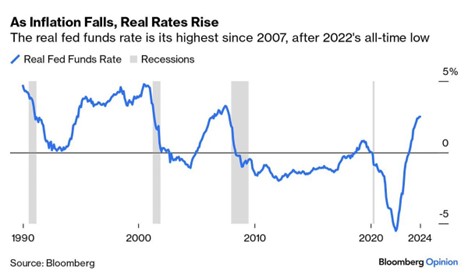

Falling inflation and sustained central bank interest rates push up the real interest rate, below the American one.

Source: Bloomberg

The Riksbank (Swedish Central Bank) did as expected and lowered the interest rate by 25 basis points at the beginning of May. To add to that positive development, three weeks since the announcement, the Swedish krona has strengthened by just over two percent against the euro and almost five percent against the US dollar. We are not surprised, and it goes hand in hand with a general increased appetite for risk.

At the end of May, data was also released regarding Sweden's GDP growth during the first quarter. Unchanged levels were expected, but the outcome was +0.7%. It is very positive and benefits our property companies, among other things. As we have said before, several factors are now reversing for the better and Sweden's economic growth will likely be at the top tier in Europe next year. Reasonably, one of the effects should be a continued strengthening of the Swedish krona.

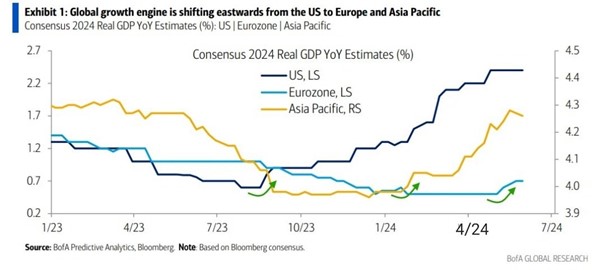

Below are Bank of America's economic forecasts showing that global economic growth is moving geographically eastward. Europe appears to be gearing up while there are signals to the contrary in the US (from a high level).

Below are GDP forecasts for the US and Europe respectively. A significant improvement is expected next year in Europe. For comparison, the Swedish Ministry of Finance expects an economic growth in Sweden of 2.5% for 2025.

Source: Kepler Cheuvreux

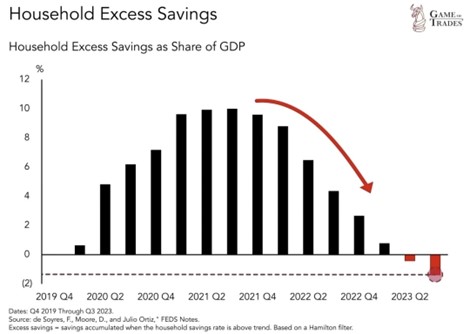

Reality check. The US government will soon pay more in interest payments than in its defense spending. It is an unfamiliar territory.

One should never doubt the vital American consumer, but savings are starting to run dry. Maybe gains in the stock market will solve the problem? In Europe it looks a little better.

Source: de Soyres, F, Moore, D, and Julio Ortiz, FEDS Notes

From six expected interest rate cuts at the beginning of the year to currently two. Members of the Fed express some disappointment that inflation is taking longer to reduce to two percent than previously expected.

Source: HEDGEYE

Elon Musk looks set to get through his modest $56 billion remuneration package for a job well done and for taking the company forward. That is just over 10% of Sweden's GDP and can be considered substantial.

"I skate to where the puck is going to be, not where it has been..." Private Equity firm, Funecap, embraces Wayne Gretzky's quote outright and capitalizes on Europe's declining population. Unlike the USA where there is plenty of space to bury people, in Europe there are limited spaces. Funecap has bought more than 300 crematoria and funeral centers for a total of 1 billion euros. Life is full of possibilities!

Portfolio Companies

Euronext

In May, Euronext, which owns several European exchanges, reported. The operating profit was around 6% better than the preliminary estimates thanks to slightly higher sales than expected and good cost control.

After Euronext acquired the Milan Stock Exchange from the London Stock Exchange a few years ago, the market's focus has been on how to integrate such a large piece. In 2024, the monumental integration work will be completed, which has been very successful. The share of volume-related income (such as ordinary stock trading) now amounts to just over 40%, compared with just over 60% 10 years ago. The fact that the percentage decreases is good, because it makes earnings more predictable.

Even more important is that the share of revenue that comes from trading, specifically, now makes up just under a fifth of revenue, compared to around 40% 10 years ago. This is a revenue stream that the stock market has historically undervalued because it is volatile and unpredictable. The Euronext share is now valued in line with its historical average, looking back 10 years, at a forward P/E ratio of around 15x. However, we believe that the company deserves to be valued at a premium to its historical average because the company today is better in many respects than it has been historically.

In the short term, we can see that volumes during April on Euronext's exchanges are showing growth. It follows a full 21 months in which volumes on Euronext's exchanges have fallen. If volumes continue to rise, the sales forecasts for this year will probably need to be adjusted upwards. Even small revisions make a nice contribution to the profit estimate given the company's high margins of around 60% (and vice versa).

The stock has outperformed the index by about 20% since we first invested about 8 months ago. In addition, Euronext has rewarded shareholders with dividends and a major buyback program that was opportunistically initiated at attractive price levels last year. In May, the share rose by 7% and, including dividends, the corresponding figure this year is 18%.

4imprint

During the month, gift promotion company, 4imprint, released an update on results for the first four months of the year. Revenue grew by 6%, which was slightly better than we expected. The growth rate should rise gradually during the year because the comparative figures become simpler as the year goes on. At the same time, it was announced that the company's esteemed CFO will retire after 27 years in the company. The stock initially reacted negatively to that announcement, but recovered some of the fall and closed the month with a 3% gain. The corresponding figure for the first five months of the year is 42%.

Carel Industries

Carel is one of the fund's worst performing holdings so far in 2024. The last two quarters have seen weak organic growth. The main reason for that is Carel's exposure to heat pumps. After several strong years, the market for heat pumps weakened significantly during the end of 2023 and the beginning of 2024. (Many of you readers have probably followed Nibe's recent price declines, which is due to this.) However, Carel only has 10% of its sales exposed to heat pumps and in the long term it is a market that is expected to grow well above GDP growth.

Our mistake has been that we understood too late the power of the decline in the heat pump market. In addition to the sharp drop in demand, Carel as a subcontractor is struggling with several customers who have overstocked inventory. However, this effect should be transient. Since Carel has several heat pump manufacturers as customers, investors also mitigate the brand risk that comes with investing directly in, for example, Nibe or the Italian Ariston.

During the month, we met Carel at an investor conference in Milan. There, it became clear that the company sees the weak results as temporary. They continue to add developers to the workforce, which they probably wouldn't have done otherwise. There are also segments, such as data centers (about 10% of sales), which accelerate the rate of growth. We are also starting to pick up signs that the company's business division, which is exposed to cooling, is starting to pick up again after a couple of years of relatively stagnant sales levels.

Over time, Carel should be able to grow with high single-digit numbers driven by a series of structural trends that we judge to be sustainable. This makes for a very nice return on the capital employed. The company is family-owned and is being managed with a very long-term view. Presumably, during the second half of the year, we will begin to see signs that the company's end markets have started to pick up again, which we believe could fuel the share again following its weak development. In May, the share fell by 8% and YTD the development is –30%.

Diploma

The serial acquirer released its half-year results in May. The numbers were as the market expected, but Diploma also offered an upgrade to its full-year guidance. For the fiscal year (which ends in September), organic growth of 6%, 10% acquisition-related growth, and an operating margin of 21% are expected. This pleased the market and the stock rose by 13% during the month of May. For the full year and including dividends, the share has risen by 16%.

Biotage

Biotage held its first ever capital markets day in Cambridge in May. In attendance was a small crowd of investors and analysts, including ourselves. Much focus was on the recently acquired company, Astrea, and its future. Our first general impression was that the management team is of very high quality. Many felt well qualified for a company with a turnover of around SEK 2 billion a year, but that probably indicated that Biotage/Astrea has something special.

No new figures were communicated but the new financial targets from the year-end report remain, double-digit growth and a profitability target of a high twenty percent. However, we got a much better feel for the growth drivers in Astrea and how they work commercially.

The company spent a lot of time explaining its competitive workflow solutions in each modality (such as Small Molecules, Peptides, Plasmids and Proteins). The company also emphasized its exposure to peptides, where Biotage has a strong position. One also sees great growth potential within PFAS.

Management also told the story of how Astrea began manufacturing high-quality products for internal research when the company was part of the company Prometic. The products were of such high quality that they could be used for other drug development projects. Prometic lacked the ability to commercialize the products whereupon Gamma Bioscience (backed by KKR) bought the segment. By receiving 17% of Biotage as payment Astrea ended up in Biotage's ownership, since a year ago.

Astrea has grown revenue at an annual average growth rate of 72% since 2021. In that time, it has tripled the number of customers and increased the size of each deal by approximately 60%. There was also a lot of focus on Astrea's new product, AstreAdept, which has the potential to revolutionize the production of cell and gene therapy drugs (mainly lentiviruses). With today's methods, only 20% of the desired number can be used. Purification is the biggest cost during drug development, and this is one reason why cell/gene therapies cost >1 million dollars per patient. AstreAdept should be able to clear 60-70% of the vector and this will provide significant cost benefits for customers.

In summary: We thought the management team gave a confident impression, both in the short and long term. Astrea is well positioned, and growth will continue to be high. Despite a challenging market for the company, we believe that there is a greater risk on the upside than the downside in the estimates.

Biotage shares rose by 10% in May and have risen by 39% for the full year.

Cargotec

Finnish Cargotec also held its capital market day in Helsinki in May. The capital market day was divided into two days, the first about Hiab and the second about Kalmar. The plan continues to list Kalmar on the first of July this year. The sale process of MacGregor has started, and the company says there is enough interest for a deal in the second half of this year.

Hiab: It all started with Hiab presenting its long-term goals. Annual revenue growth above 7% over an economic cycle, operating margin over 18% and return on capital employed over 25%. This is quite a bit above what consensus expected before the capital markets day. Hiab will focus on four key markets, Waster & Recycling, Defense Logistics, Retail & Final Mile, and Construction. These areas will drive growth where M&A is a central part. The balance sheet will be well capitalized after a sale of MacGregor. Hiab is either number one or number two in all its operating segments and a strong market position is a good basis for future success as an independent company. The most important component will be to grow the service part of Hiab. Connected devices have grown from around 10,000 to 39,000 between 2020-2023. The goal is 90,000 in 2028. This should lead to more service, which today accounts for around 25% of turnover.

Kalmar: Kalmar presented the financial targets in connection with the publication of the prospectus which was released before the capital market day. Sales growth must average 5% over an economic cycle, the operating margin must be 15% and the return on capital employed over 25%. Clearly, there is more potential for improvement in Kalmar than Hiab. The big driver for Kalmar will be an underlying market that is expected to grow 5%, driven by electrification.

Like Hiab, but perhaps even more clear in Kalmar, is that the company should grow its service business. It is easy to understand how this should happen. With higher electrical content, more service will be required. Above all, customers will use Kalmar to a greater extent instead of servicing the units themselves. A bit like a private person not tinkering with their electric car like one could do with a car from the 90s. Kalmar has an installed base of 65,000 units and is the global market leader in several segments. The company has a strong position in electrical products and as the devices become more connected, service revenues should increase.

The Cargotec share rose by 3% in May and has risen by 45% for the full year. After rising over 100% since last fall, the stock is valued at EV/EBIT 9x and 8x for 2025e and 2026e, respectively.

Summary

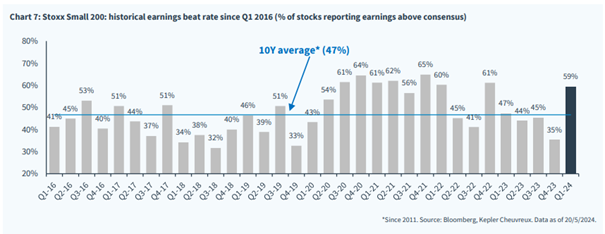

The reporting season is over and passed with honors. 59% of the companies in both the Stoxx 600 and the Stoxx Small 200 beat expectations, which for small companies in particular is significantly better than the historical average. See pictures below.

In the last 18 months, American small-caps have had substantial downward adjustments to their profit estimates for 2024 (-30%). Over the same period, US and European large-caps have essentially unchanged estimates.

Even more remarkable is that even the European small-caps, in general, have unchanged profit estimates. The explanation is mainly because American small-caps to a greater extent than European ones consist of biotech and technology companies that have had a tough time. Since the beginning of 2023, European small-caps have performed about 5% better than American ones, measured in the same currency.

Compared to the valuations of larger companies, European small-caps are now trading at a discount. It is the first time since the financial crisis 15 years ago. Given that small-caps is the asset class most affected by interest rate changes and given where we are in the interest rate cycle, it feels strange. But that is also the reason why we have been, and continue to be, more positive about small-caps now than we have been in many years.

The correlation between small-caps and the interest rate is almost 1.0. Interest rates will with a high probability come down in the coming months, quarters and (perhaps) two years.

Large difference in returns over the past three years between small and large companies.

Source: Win Smart, CFA

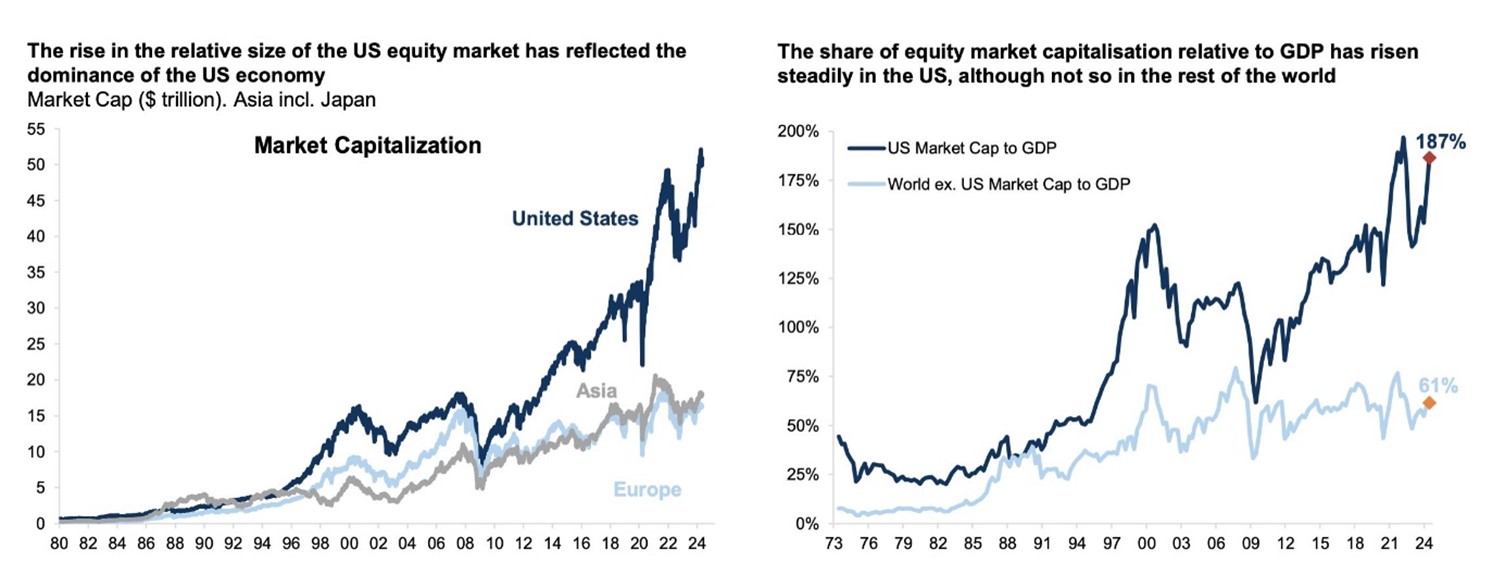

The image below is thought-provoking in many ways. The combined value of all US listed stocks is now 187% of the US economy. The corresponding figure for the rest of the world excluding the USA is 61%. 15 years ago, levels were equal.

Source: Goldman Sachs, Holger Zschaepitz

The one explanation for the above is the senseless success of the big American technology companies. Nvidia's market capitalization is now in line with the combined market capitalization of the entire French stock exchange. The corresponding relation compared to the German stock exchange is 30% higher value for Nvidia. The world has never before seen such a rise for a single company. In 1.5 years, the market capitalization has increased by about 2.5 trillion USD or close to 9x and huge fortunes have been created.

Source: Kepler Cheuvreux

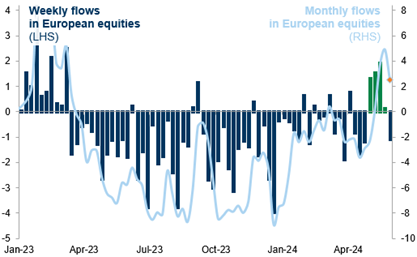

Net inflows to the European stock markets have finally, after massive outflows for several years, turned positive.

Source: Goldman Sachs

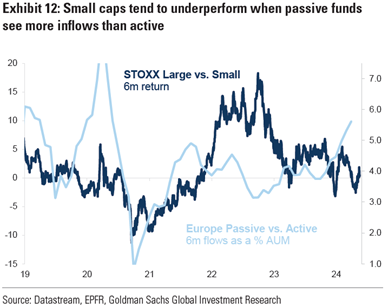

But small-caps is where it really happens. Nice to see that our message six months ago is now becoming a reality. And it's probably just the beginning.

Source: Goldman Sachs

Our conclusion is that the conditions for us as stock-pickers with a focus on European small-caps are better than they've been for several years. In addition to upcoming interest rate cuts that will drive price performance, the increasing share of passive capital is something that creates mispricing and opportunities for investors like us. Not thinking about valuation and risk when making investments, but blindly buying because the company weighs a certain number of basis points in an index doesn't feel optimal.

Below is the image of the month. It shows that especially small companies with a high return on their capital are valued at an undeservedly high discount in relation to larger companies with the same type of return. A very large interest in and focus on the largest technology companies means that smaller, but inherently attractive companies are often overlooked. In addition, when investors allocate to different ETFs, often no time is spent on company analysis, but only on the weight of an index. It is in those situations that, for example, you can find a BoneSupport for SEK 70 two years ago that today costs SEK 250 and which on May 31 was included in an MSCI index.

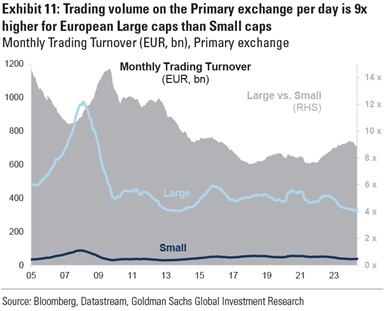

Illustrated another way, see picture below.

It also requires greater craftsmanship to trade small-caps. Trading volumes are 9 times greater for larger companies compared to smaller ones. It is easier to buy Ericsson at the closing price at 17.30.

Finally, we include an article from the Financial Times published on June 4th. Hedge funds have been badly burned by shorting British small-caps that are bought up every two weeks at hefty premiums.

"Shorting any UK mid-cap is insane, literally insane, said one hedge fund executive who specializes in shorting stocks". "The numbers are so low in the vast majority of cases that a $2bn UK company is peanuts for any mid-sized American company."

We agree and our own Wincanton was bought out in January with an initial bid premium of 54%, which then rose to just over 100% after a bidding war. We wouldn't be surprised if we got some more bids on us this year. https://www.ft.com/content/e4d32fb6-4f42-41bc-adf1-9a10edec4928

We thank you for your interest and wish you a fantastic June with school graduations and Midsummer. Don't forget the herring!

Mikael & Co

Malmö on 5th of June 2024

IMPORTANT INFORMATION. This is a marketing communication. Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/financial-and-legal-information/.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested. Please note that the management company of the fund may decide to terminate the arrangements made for the marketing of the fund in one or multiple jurisdictions in which there exists arrangements for marketing.