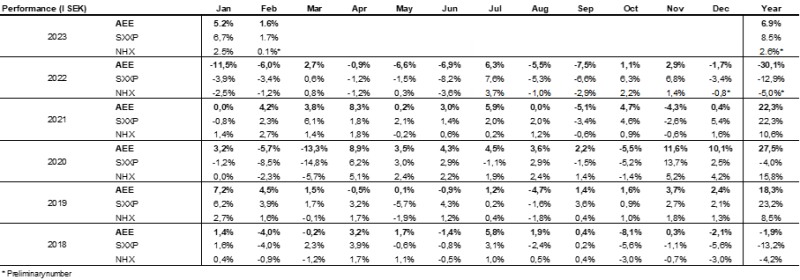

Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class' return. The information below regarding returns therefore differs from the returns in other share classes.

Before making any final investment decisions, please read the prospectus, its Annual Report, and the KID of the relevant Sub-Fund here

This material is marketing communication

Monthly Newsletter Coeli Absolute European Equity – February 2023

FEBRUARY PERFORMANCE

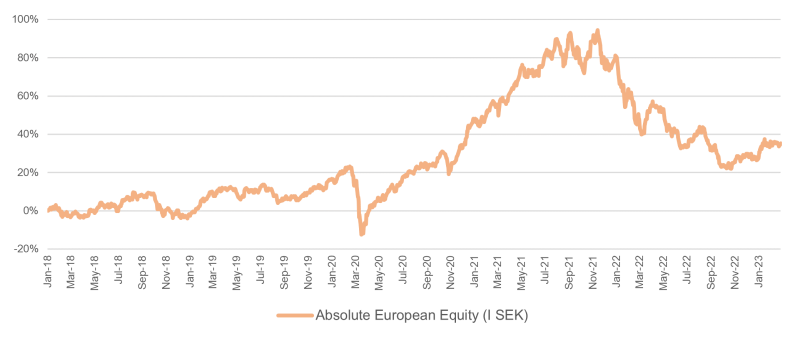

The fund’s value increased by 1.6% in February (share class I SEK). The Stoxx600 (broad European index) increased during the same period by 1.7% and HedgeNordic’s NHX Equities increased provisionally by 0.1%. The corresponding figures for 2023 are an increase of 6.9% for the fund, 8.5% for the Stoxx600 and 2.6% for NHX Equities.

EQUITY MARKETS / MACRO ENVIRONMENT

The strong start to the year on the world's equity markets continued into February. A surprisingly strong US economy combined with an inflation rate, which in several countries declined slower than expected, contributed to the risk premium rising and share prices retreating in the second half. Before the last days of the month, the Dow Jones index had fallen for four straight weeks. The S&P500 and Nasdaq showed the same pattern, albeit with a somewhat stronger development. Overall, the S&P500 was down 2.6% in local currency. Europe continued to develop significantly stronger than the US and the broad European index SXXP600 rose by 1.7%. Admittedly measured in local currency, but it is very unusual for such large differences in broad major stock indices. The fund returned +1.6% in February and it was across the board a very good reporting season for the fund, with the exception of Norwegian Photocure which came in with a surprisingly weak report. More on this in the Long Positions section.

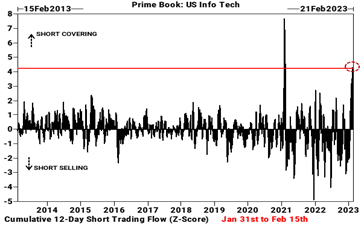

Significant contributing factors to the strong development at the beginning of February was the huge amount of short covering and in particular among US technology stocks. According to Goldman Sachs, there has only been one occasion in the last 10 years where there have been larger volumes than during these days in February. Volumes were in the 99.5th percentile!

Source: Goldman Sachs

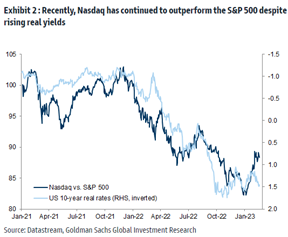

Despite rising interest rates, the Nasdaq has had a stronger development than the S&P500 recently. The correlation below has been at least temporarily broken. They will meet again, and the question is whether it is the interest rate or the Nasdaq that drops back first.

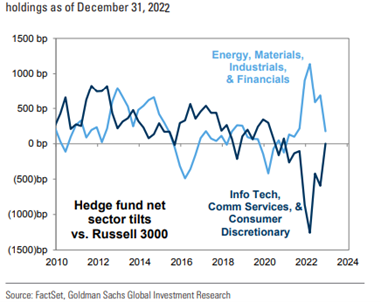

The chart below shows hedge funds' increasing exposure to technology and consumer stocks in recent months at the expense of oil/mining companies, industrials and banking stocks. Last year's winners have clearly been replaced by last year's losers.

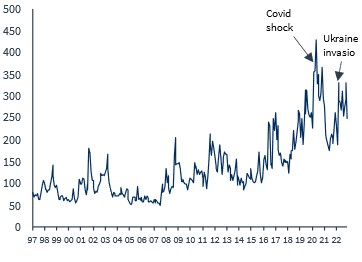

The global economic policy uncertainty index unfortunately shows with undoubted clarity that we are still at historically high levels of uncertainty with all that that entails.

Source: Kepler Cheuvreux

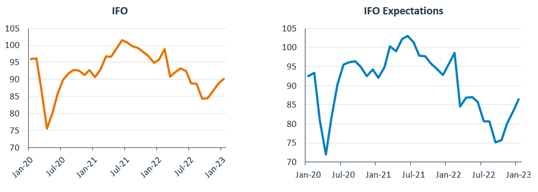

On a more positive note is the rising confidence of the German business community (left image) and perhaps even more gratifying, the companies' expectations going forward (right). A clear improvement is visible, even if we are still at low levels.

Source: Kepler Cheuvreux

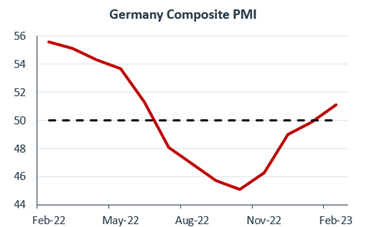

Even the purchasing managers in Germany show some resumed growth in busing activity.

Source: Kepler Cheuvreux

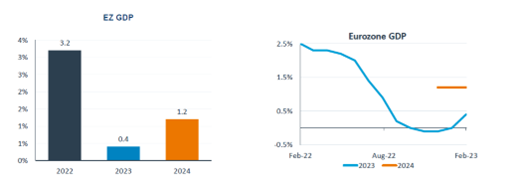

Economic growth in the eurozone is expected to accelerate after the summer.

Source: Kepler Cheuvreux, Consensus Economics

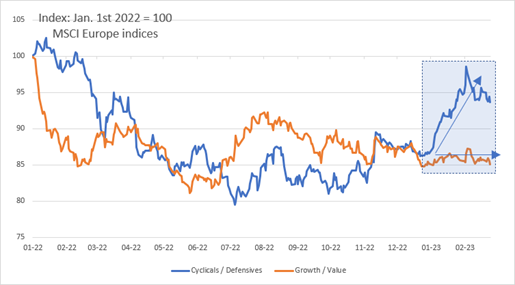

The expected economic growth has contributed to cyclical companies in relation to defensive companies (blue line) having a significantly better return during the beginning of 2023. Growth companies in relation to value companies have, after a tough 2022, had a similar development during the first two months of the year.

Source: Kepler Cheuvreux

The big gossip of the month was, as so many times before, the rising interest rate. Expectations at which level the Fed will end interest rate hikes have been gradually rising for a long time. In February, expectations took a substantial step upwards from 4.6% to 5.4%. A very strong increase. We note that the European and American stock markets in this climate had significantly different returns with the US as a clear loser. For example, the French CAC rose by 2.6% while the S&P500 fell by 2.6% in February.

Swedish interest rates also rose significantly during the month. A year ago, the Swedish two-year-old was negative, but since then the picture has changed radically. Note the rise in recent weeks. From 2.35% to 3.25% in three weeks!

Source: Bloomberg

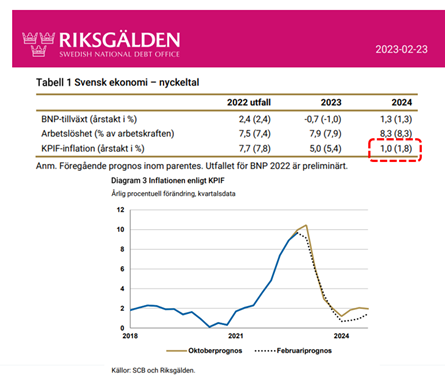

The National Debt Office presented new forecasts at the end of the month in which they halved their inflation forecast for 2024 to only 1%. Even before Christmas this year, they expect inflation to fall below the target of 2%. We hope they are right. That inflation will drop significantly from here is fairly certain, but the speed is unclear. Regardless, it bodes well for hard-pressed Swedish borrowers.

In Germany, people are not as optimistic about the inflation trend. However, it is not newsworthy and a troubled past on the subject is likely playing a role in that.

Source: Bloomberg, Holger Zschaepitz

European gas prices have collapsed and are now at the same level as in the fall of 2021. This is probably the single strongest contributor of the European economy unexpectedly outperforming in recent months. In the long run, this is likely the reason why European stock markets had large inflows at the expense of above all American ones.

Source: Bloomberg

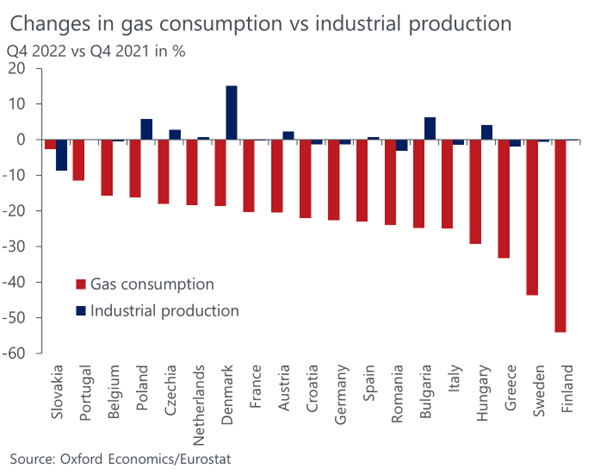

Picture of the month! Despite 20-30% less gas consumption in Europe, industrial production is basically unchanged. Every cloud has a silver lining. The European companies show great flexibility and an impressive resistance to rising costs. The obedient may wonder how much coal consumption has increased? We don't have the answer, but it has certainly increased.

Sweden is gaining international attention in terms of the sharply falling prices for villas and apartments. Sweden together with Norway, Canada, Australia and New Zealand now form the abbreviation CANNS with particularly high vulnerability in private indebtedness. There's even an ASR Canns House Price Index to follow for those interested. Kick the can down the road - economies.

“There is no sign of aliens or extraterrestrial activity in connection with the recent shootings. Wanted to make sure the American people understood that”. The reassuring words were conveyed by the White House press secretary after the United States shot down some balloons at the beginning of the month. How lucky! One was a Chinese spy balloon and another three were balloons of unknown private origin. US Secretary of State, Antony Blinken, had to cancel his trip to China at short notice.

Source: Fox News, Twitter

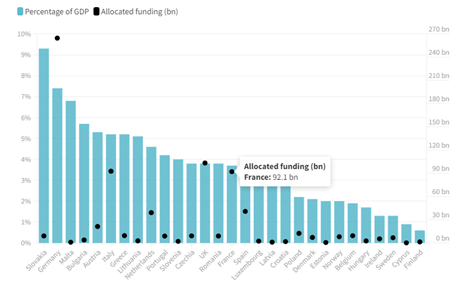

So, the long-awaited electricity support finally begins to reach hard-tested electricity customers. The image below shows how much different European countries support consumers in relation to their respective GDP, as well as in absolute numbers in billions of euros. Most EU countries have removed or greatly reduced VAT. Sweden makes it easy and keeps 25% VAT, it gets so complicated otherwise. The energy tax has also been greatly reduced in many countries. In the country “Differently”, Sweden, as the only country in the EU, raised the energy tax at the turn of the year from 45 to 49 öre per kWh because of rising inflation. Fair is fair.

Source: Bruegel

The UK surprised the financial market positively in February with a strong recovery in consumer confidence. Optimism is still well below historical averages, but the strong rebound surprised many and the pound strengthened against both the dollar and the euro.

UK Prime Minister, Rishi Sunak, and European Commission President, Ursula von der Leyen, met at the end of the month to discuss and try to resolve the tainted Northern Ireland issue. "A new chapter between the EU and Great Britain has now begun," Sunak said at the press conference held at Windsor Castle outside London. The tone was more cordial than it has been for years and let's hope he also succeeds in the next step in the process which is to get unionists and Tory politicians to accept the deal. "Hard core" Brexiters are still probably more interested in buying an old colony or similar from the British Empire and dreaming of bygone times.

About as unusual as the northern lights in southern Sweden (which we got to experience at the end of February), is that the Swedish krona strengthens against the euro. When the new Governor of the Riksbank (Swedish Central Bank), Erik Thedéen, during his first press conference on the 9th of February, said some warm words about the Swedish krona, it had an immediate effect and the krona's strengthening against the euro during the month ended at +2.7%. It wasn't a year too early and the fact that the previous management until recently scattered kronor to spread the risks (!) despite a record low level for the Swedish krona appears completely inconceivable. It is the same board that bought most of what was available in Swedish housing bonds in an overheated housing market well into 2022. This contributed to an unrealized loss of 81 billion for the Riksbank in 2022 and the state will probably have to contribute with capital. Erik Thedéen will not come to a set table, and we wish him the best of luck with his mission, which now thankfully also seems to include strengthening the Swedish krona. The image below shows EUR/SEK since autumn 2021 and the circle on the right in the diagram shows the time of Thedéen's first press conference - a clear strengthening of SEK.

Source: Bloomberg

Long positions

Tate & Lyle

We introduced British food company Tate & Lyle to our readers in our February 2022 monthly newsletter, which is exactly one year ago. Our investment thesis at the time was basically based on the fact that the company's value would become evident after the sale of roughly 50% of one of their business divisions ("Primary Products") which had volatile earnings with dull growth prospects. The remaining business clearly has much sophisticated financial characteristics and with a clear exposure to ingredients for sugar reduction, which is a fast-growing market.

If we look at the share's performance since a year ago, we were right: The share held up very well during a difficult stock market last year and has risen by around 13% this year. Operationally, the company has delivered on its projections. At the same time, we have seen how the company's valuation multiple has risen somewhat.

February was a joyful month for those of us who like the company, when a capital market day was held for the first time in five years. Among other things, we were offered updated financial targets, which included annual sales growth at group level of 4-6% combined with a profit that should rise by around 7-9% per year. This implied an upgrade against the analysts' estimate. In addition to the financial aspects, a deep dive into more qualitative matters such as product portfolio and research/development was offered.

With our estimates, Tate & Lyle now trades at EV/EBIT 12x for the financial year 2025e, which ends in March. We think the share deserves further appreciation, and with a target multiple of EV/EBIT 15x, we reach an upside of 20% in just over a year's time. If you want to dream, you can look at other ingredient companies that enjoy significantly more generous valuation multiples and think about where Tate & Lyle might be valued in a few years, given a longer history then with the new company structure. The share price increased almost 7% during the month.

ISS

One of our larger holdings, ISS, has risen 4% so far in 2023, compared to the European index (SXXP600) of 9%. The corresponding figures for 2022 are 18% and -13%, respectively. After a strong year in 2022, the ISS share has thus begun 2023 hesitantly. It's not surprising given how the market has been so far in 2023. The tune has been to sell last year's winners in favor of last year's losers. If we look at similar shares, such as French Sodexo or British Compass Group, ISS has the best performance this year.

Focusing on the important aspects: After a positive sales update for the full year 2022 in January, we got our hands on the company's annual report in February. An important update was the company's guidance for 2023. The expectation is now that ISS will be able to grow organically by 4-6% this year, to be compared to the analysts' expectation of 4%. We note that ISS managed to raise its renewal rate (the percentage of existing customers who do not leave ISS) to a whopping 94%, higher than 92% and 91% in 2021 and 2020, and also in the years before that.

The stock is still trading at multiples that are lower than history, while the company's talented management has delivered on everything that has been communicated so far. We are still satisfied owners and think that the share should initially be traded above 200 Danish kroner, which is an upside of around 30% from today's levels. We have taken advantage of ISS stock's relative weakness this year to increase our position at prices around 145.

Pets at Home

The fund's strongest contributor in 2023 continued to go deliver in February with no particular news to justify it. On the contrary, a couple of brokerage houses have actually chosen to take profit by closing their buy recommendations. We think it is premature, even though we also sold some shares as the price had risen 36% at of the end of February this year.

Wincanton

Despite a perfectly acceptable earnings update in January, Wincanton has had a gutsy 2023 so far. We believe it is due to the fact that there was a large individual seller in the stock. The fund bought shares in a larger transaction that we believe was the seller's last shares. The stock rose 5% in February and the rise in price came after the seller appeared to have finished. It is often the flows of buying and selling that determine the price in the short term in illiquid shares.

Lindab

Lindab also released its Q4 report in February. The company's operating profit of SEK 244 million was around 11% below the preliminary estimates. It emerged later during the report presentation on the same day that the operating profit had been charged with 25 million kroner of costs that many other companies would have treated as one-offs, but Lindab; however, did not do in this case (exemplary!). It is therefore not possible to call the report a disappointment.

On the contrary, we note that Lindab's large inventory, which was greatly inflated by higher raw material prices, finally fell from Q3 to Q4. For a few quarters, Lindab's margin has been squeezed by buying material at high prices to ensure delivery security. Sometime during Q2 2023, the negative effect should be phased out. In his CEO speech, Ola Ringdahl was determined that the company will reach its goal of at least a 10% margin in 2023, which the analysts still do not seem to believe if we look at the consensus estimate. If he is right and the sales estimates hold, then positive estimate revisions could be in the cards for 2023. We increased our position in February and the stock is up 14% so far this year.

Photocure

The big disappointment of the reporting period came from Photocure. The company's sales figures came in a bit below analysts' expectations. At the same time, the company's guidance for 2023 was below market expectations, but expected growth of 20% and profitability at EBITDA level before "one-off costs" (which we interpreted as relating to acquisition costs et al.). In short, the report was not good and therefore the stock fell 24% in February. As such, Photocure was also the fund's largest negative contributor.

BoneSupport

BoneSupport delivered another record quarter coming in 6% above consensus. Adjusted for a few non-recurring items, the operating profit was reasonably in line with expectations. The company is growing sales by 49% organically on an annual basis. Cerament G was launched in the US during the quarter and got off to a good start in the first two months. Sales are focused on the large university hospitals and their "key opinion leaders" to increase speed and penetration in the sales process. It is a long process to become the standard treatment in a large hospital and we expect slightly bumpy but continued rising sales of Cerament G in the coming quarters. According to the company, the company has received very positive feedback from surgeons, and we feel confident that the company will deliver over time. It was also pleasing that the standard product (Cerament BVF) continues to grow sequentially, which indicates that there is still a lot for BoneSupport to do in the US. The company's unique product and position, its strong momentum and an attractive valuation if our long-term estimates are reasonably correct, mean that BoneSupport continues to be one of the fund's largest positions.

SLP

Our logistics property company SLP also reported during February. It was a strong end to the year where we saw positive changes in the value of properties despite the yield requirement being raised by 20 basis points. This is the core of the investment case where new lettings, acquisitions and CPI adjustment of 2023 rents drive NAV growth. SLP's balance sheet is strong and the company is ready to capitalize on a messy real estate market where several players have gone from net buyers to net sellers in the past year. We continue to like SLP and would rather own high-yielding logistics properties that are largely 100% inflation-indexed than many other property-related properties that have lower yields.

Corem

The real estate company Corem also reported during February. Operationally, the report was somewhat better than expected. The weakness was a NAV development that was below our expectations, driven by higher yield requirements (20 basis points higher) and write-downs in the associated company Corem Kelly. Having said that, we do not own Corem primarily because of the NAV development in the first place, but a strong operating net in combination with a sky-high risk premium. The financing cost in the quarter was also slightly higher.

In recent months, the company has sold properties which, together with its holdings in Castellum, are expected to bring in a total of over 7 billion. The biggest deal was with Blackstone, where cash is to be exchanged at the beginning of April. So far, all properties have been sold around book value, which is in stark contrast to the discount to NAV, which is still around 65%. That the share is not traded at a higher level despite these sales may seem a little strange to us, and we have therefore continued to increase our holding. We also note that Corem, after the Blackstone deal, owns logistics properties for 11-12 billion. These properties are traded at a 65%discount in relation to the net asset value, while logistics properties in Sweden and Europe are traded at a premium of 20-30%. Here, it should be possible to create shareholder value with some kind of structural transaction, we think.

The market's perception of Corem is almost exclusively how to deal with its bond maturities and general financing. Our view is that after the Blackstone deal, the company largely control their own destiny and have several options, including buying back the bonds in their entirety.

An investment in Corem has a higher risk than, for example, SLP or our previous holding in Wihlborgs, but the potential is also significantly greater in the short and medium term. With inflation expected to drop significantly for the rest of the year, that should lead to pressure on interest rates after the summer, which in turn should increase interest in a stock like Corem. The stock fell by 5% in February and has fallen and risen by 8% this year

Saint Gobain

The fund invested in Saint Gobain in December when we scanned for low-valued cyclical companies with an attractive risk/reward. At the time of our initial investment, the company was valued at a very low 7x 2023e net earnings. The return on equity was 12-13% and all this with low debt. It was clear that the market did not believe that the transformation the company has made since 2018 will significantly improve earnings quality going forward. At meetings with the company, there was a certain frustration about this.

This year will be an important test for the company. So far, the market has been far too skeptical, which has benefited us. At the end of the month, an excellent quarterly report was published that beat low expectations, and in addition, a relatively optimistic forecast for the full year was communicated, which led to consensus expectations being subsequently raised by 3-5%. The stock has risen by 23% this year, of which 7% came in February.

Commerzbank

For the third month in a row, we have reason to mention Commerzbank. Although the fund has only been an owner since mid-November, the share has nearly risen by 50% since then. The reasons why the stock continued to rise by 11% in February, after rising by 10% in December and 18% in January, are several: 1) Continued rising interest rates that are burning the net interest income 2) Commerzbank was included in the important index DAX30 3) A very strong quarterly report that led to analysts on average adjusting earnings estimates by 10-15%.

The image below shows that in December the share traded below 8 euros per share compared to today's 11.60 and that the profit per share in a few months has been adjusted up by as much as 25% for the current year.

Source: Bloomberg

Short positions

The short portfolio contributed with a minor negative result for the month. The largest positive contribution came from our short futures position on the OMX Stockholm index and the biggest negative contribution was our short position in a Swedish small company index.

Exposure

The net exposure, adjusted for our unlisted holdings, at the beginning and end of the month was 72% and 77% respectively.

Summary

Since the lows at the end of September last year, the DAX has risen by 27% compared to the S&P500's more modest 2%, measured in euros. That's a huge difference in just five months and is mainly due to:

• The big American tech companies have had problems with growth and thus their valuation

• The difference in valuation between Europe and the US was initially record-breaking

• Europe as an asset class was considered a pariah for most of last year due to war and energy supply

• Europe experienced a mild winter and thus significantly less energy problems

• The European economy has been much more resilient than predicted

• China has opened up the country, which benefits Europe more than the US (greater exposure)

Source: Bloomberg

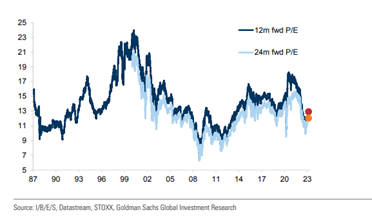

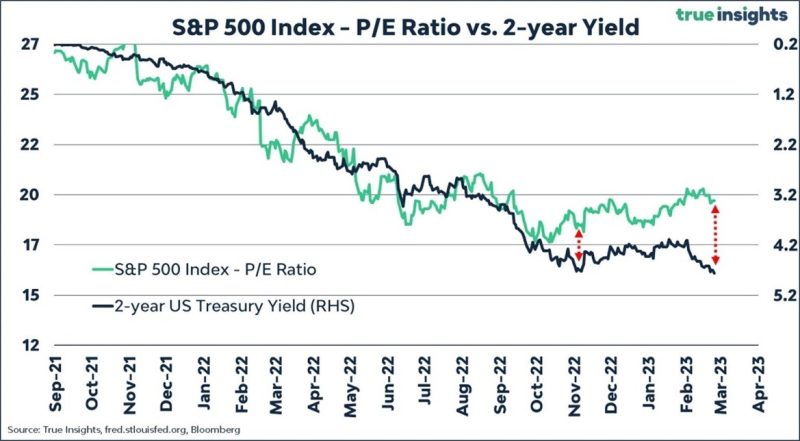

The European stock market is currently trading around 12-13x forward-looking 12-month P/E. The recent rise in the stock market can barely be glimpsed in the image below, which shows 36 years of valuation history.

Despite a strong development last year, the UK is still the lowest valued stock market, while the US is the highest. Also note the difference in return on equity. The USA is in a class of its own and thus deserves a higher valuation.

In addition to the above explanations for why Europe has been much stronger than the US, it may also be that the terminal rate in the US is a bigger problem than the terminal rate in the Eurozone. At the time of writing, the expected terminal interest rate is 5.4% in the US compared to Europe's 3.9%. The American economy continues to be under pressure with unemployment that is non-existent. In Europe and not least in Sweden, we now have a growth rate that implies an ongoing recession and thus it may be that the interest rate is less of a threat to the stock market in Europe than in the USA. Below US unemployment for the last 50-60 years. We are witnessing historic lows.

Source: Bloomberg

The rising interest rate in the US does not seem to be fully reflected in the stock market. This could mean that the US stock market is facing a serious headwind. Another scenario is that inflation suddenly drops and pulls down interest rates. Or the historically high correlation between the interest rate and the P/E ratio will not return, but that does not seem likely. At least the current valuation of the S&P500 does not leave much room for multiple expansion, but the development is more dependent on earnings growth. Europe is in a completely different situation.

Source: True Insights, fred.stlouisfed.org, Bloomberg

A large part of US GDP is private consumption. We note that hard-pressed US consumers are finally experiencing positive real wage gains. Developments in real wages have historically, with a 6–9 month lag, been a strong leading indicator for developments on the stock market. However, it does nothing to tame inflation. In Europe, real wages are expected to rise after the summer. The trade sector is this year the third best sector in the broad European index, so investors have paid attention to this.

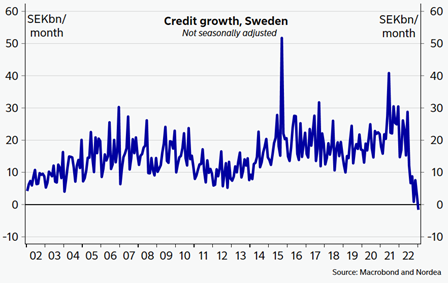

20 years of loan growth in Sweden now down in negative territory. A fascinating picture of a head-on collision in the Swedish consumer sector. It is not really this dramatic in the rest of Europe.

Source: Macrobond, Nordea

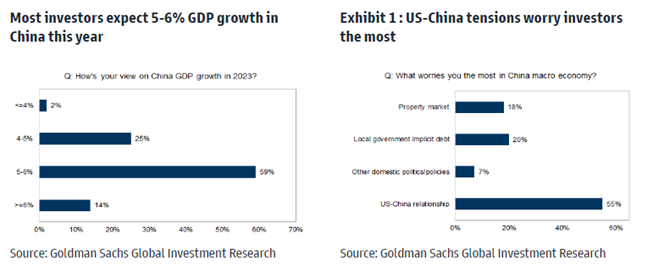

When it comes to fighting inflation, China is currently the big winner as they have no inflation to speak of. In contrast to the rest of the world, they have not had the same expansive economic policy as in the West, but they took the hits right then and there. The last few years, on the other hand, have been the most difficult ever. However, expectations for a quick start are high with expected growth of 5-6% this year. At time of writing in the morning of March 1st China released their PMI data which showed the highest activity since April 2012! The Asian stock markets reacted positively with Hong Kong at +4.2%.

Liquidity in the Chinese economy has increased substantially and is of course orchestrated by the Chinese state. It would be surprising if this does not lead to increased global economic activity within a few quarters.

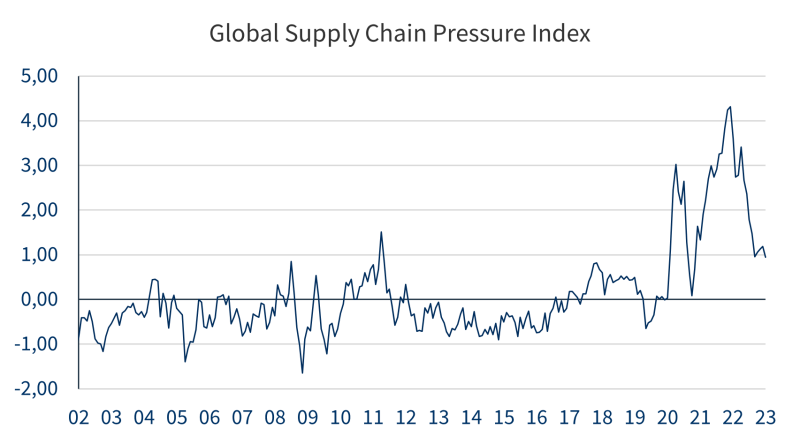

The bottleneck problems continue to decrease in the economy, which is a major contributor to global economic development, while the inflationary pressure on the margin decreases.

Source: Kepler Cheuvreux

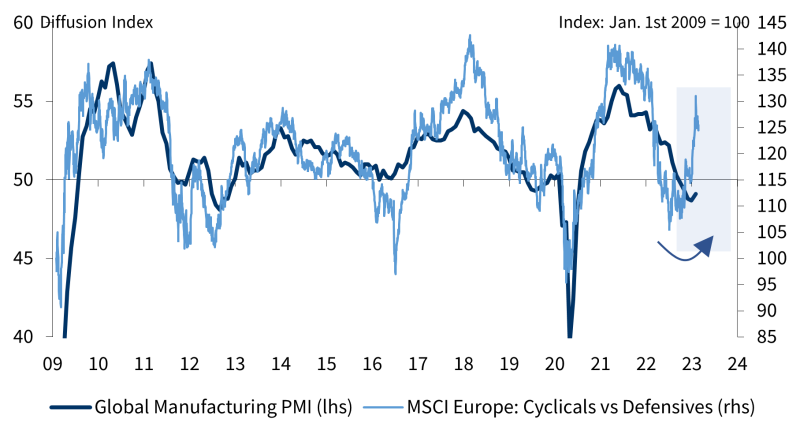

The global purchasing index has historically been an excellent indicator for predicting the share price performance of cyclical companies relative to more defensive companies. What is a little strange is that the optimism below is not reflected among the large investor collective. It appears that the shares were bought under duress.

Source: Kepler Cheuvreux

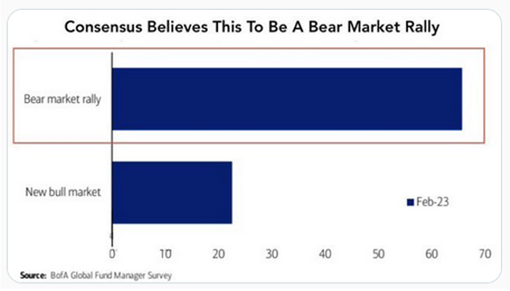

An overwhelming majority still believes that we are in a bear market rally and that share prices will therefore drop significantly. Some days bad news is good news and vice versa depending on the mood. Right now, the recession in the US is being pushed forward all the time and that is considered a problem. Many challenges remain, but the positive is that the bottleneck problems are significantly reduced, China is picking up speed, the oil price is stable and inflation, despite several setbacks recently, is likely to continue to fall. And perhaps most important of all, the companies as a collective have so far mastered the challenges well or very well.

Another picture on the same theme. Pessimism continues to dominate.

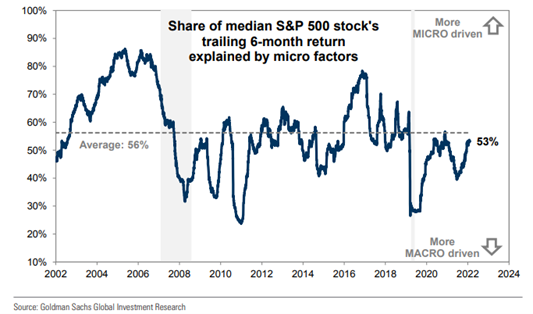

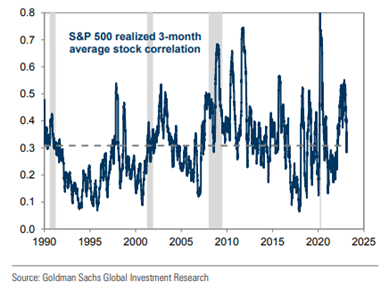

As we wrote about in the annual letter, our view this year is that it will be a significantly better "stock picking" year. The image below shows that company-specific news increases in importance when it comes to driving the share price. It benefits our business and thus also the return on our investments.

The covariation between different stocks is also falling, which is positive. In the Covid crash three years ago, the correlation was 0.8, i.e., it mattered little how the company delivered. Almost all shares were traded down outright.

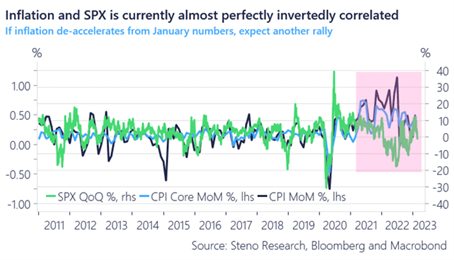

The biggest reason for the general pessimism among investors is inflation. The bow is tight and when the data starts to surprise positively, which we actually think is possible, there will most likely be a big buying pressure. We saw that, for example, on November 10th last year when the Nasdaq rose by 7.5% in one day. The image below shows the inverse correlation between the S&P500 and inflation.

In conclusion, we maintain our positive fundamental view even though we see a number of significant challenges. We do not have a strong idea of whether we will go up or down in the short term, however, our belief is that we are at a higher level than today when the year is over.

Those interested in history and statistics may note that when the return on the S&P500 after 25 days of the year has risen more than 5%, the median return for the rest of the year has ended at 17.6%. As many as 16 out of 17 times this has been true, with 1987 being the only exception.

We continue working on our company analyses, which is the most important thing for our result. It is therefore gratifying to state that, with only one exception, our reporting season was very good, which means that the company analyses were accurate.

Finally, we are very pleased to share with our readers that Norges Bank Investment Management appointed us as one of their external managers during 2022. The mandate encompasses an active long only European equity portfolio, and we are humble and very proud to have received such as prestigious instruction.

Enjoy the spring which is around the corner!

Mikael & Team

Malmö on 3nd of March 2023